Australian digital advertising hits record $17.2 billion driven by video

Digital advertising spending in Australia reached $17.2 billion in FY25, growing 10.6% with video surging 21.9% and social platforms capturing 38% share.

Digital advertising spending in Australia reached $17.2 billion in FY25, growing 10.6% with video surging 21.9% and social platforms capturing 38% share.

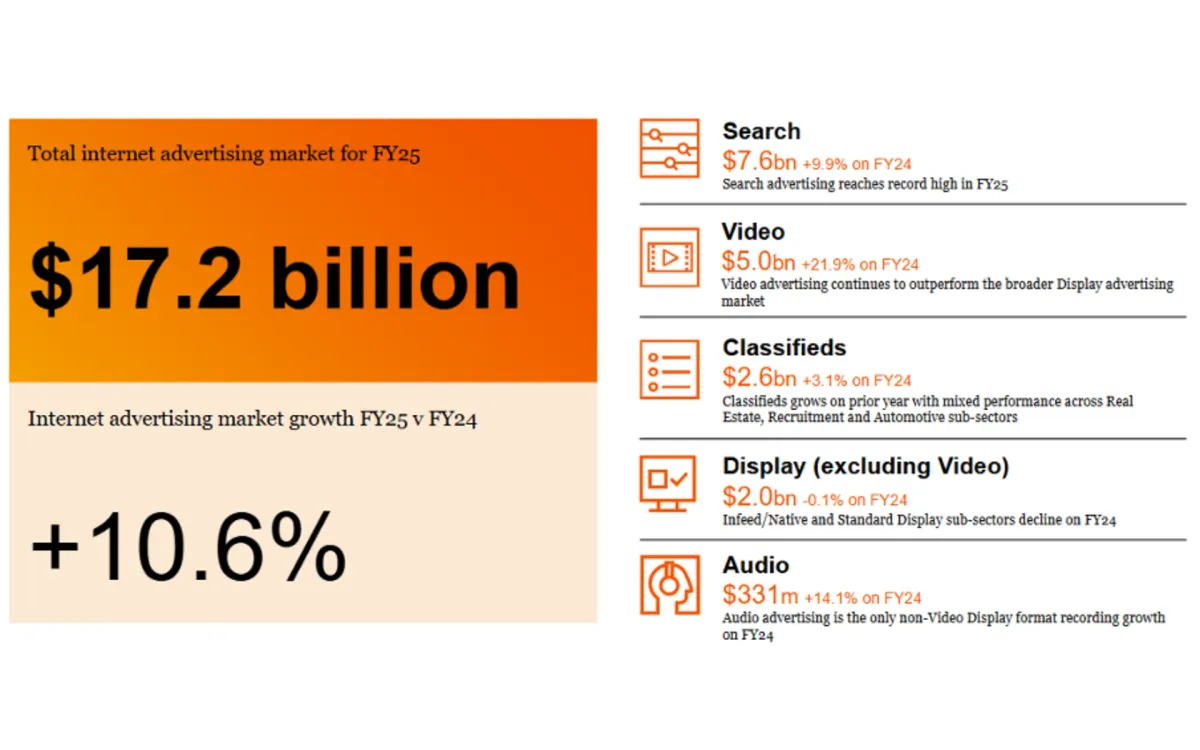

Australian digital advertising expenditure reached $17.2 billion for the financial year ending June 2025, marking a 10.6% increase from the previous year, according to the IAB Australia Internet Advertising Revenue Report released on August 28, 2025. The growth was primarily driven by summer Olympics coverage and election advertising spend, with video formats emerging as the dominant growth engine.

The report, prepared by PwC Australia, revealed video advertising increased 21.9% year-on-year to reach $5.0 billion, now representing 29% of total digital advertising expenditure. This substantial growth underscores the continuing shift toward video content consumption across all demographic segments in Australia.

Search advertising maintained its position as the largest category, commanding 44% of total market share at $7.6 billion. However, its share decreased by 0.4 percentage points compared to FY24, indicating relative growth in other advertising formats. Classifieds experienced the most significant share decline, dropping from 16.2% to 15.2% of total expenditure.

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Social media platforms demonstrated exceptional performance within video advertising, with spend increasing 36.7% year-on-year to reach $1.9 billion. This category now represents 38% of total video expenditure, highlighting the growing importance of social platforms in brand marketing strategies. The figure represents a substantial shift from traditional video advertising channels toward social media environments.

Broadcast Video On Demand (BVOD) advertising showed robust growth of 18.3%, reaching $500 million in total spend. Other video advertising categories, which represent 52% of video advertising, increased 13.5% to reach $2.6 billion. These figures indicate broad-based growth across multiple video advertising formats rather than concentration in specific platforms.

Audio advertising experienced significant expansion, growing 14.1% year-on-year to reach $331 million. This represents 4.7% of total general display advertising, suggesting audio content consumption continues gaining traction among Australian audiences. Podcasting emerged as a particularly strong performer within this category.

The June 2025 quarter demonstrated continued momentum with $4.6 billion in total spend, representing a 10.1% increase from the corresponding 2024 quarter. Search advertising grew 10.7% to $2.059 billion during the quarter, while video increased 25.4% to $1.368 billion. Display advertising excluding video showed modest growth of 0.7% to $516 million, and audio increased 8.5% to $86 million.

Election investment served as a primary driver for both video and general display advertising during the quarter. The correlation between major political events and advertising spend reflects the increasing use of digital platforms for political communication in Australia.

Connected television (CTV) investment represented 51% of content publishers' video inventory for FY25, down slightly from 55% in 2024. Desktop advertising share increased significantly from 29% to 37% of content publishers and local broadcasters' video inventory expenditure. Mobile advertising declined from 16% to 12% for FY25, indicating potential shifts in viewing patterns and advertising effectiveness across devices.

Programmatic buying continued expanding within content publishers' video inventory, with 60% purchased programmatically during the June quarter. Agency insertion orders remained the most popular buying format for content publishers' display inventory, suggesting different purchasing preferences across advertising categories.

Fast-Moving Consumer Goods (FMCG) expenditure increased substantially and entered the top five display advertiser investment categories with 6.4% share of spend. This growth was heavily oriented toward video advertising formats, reflecting consumer brands' recognition of video's effectiveness in product demonstration and brand awareness campaigns.

Finance sector expenditure also increased during the same period, reaching 8.6% share of total advertising spend. The traditional top categories of automotive, retail, and entertainment & media all experienced share softening, though this occurred against a larger overall spend base.

Retail maintained its position as the largest advertiser category with 17.2% share in FY25, compared to 17.7% in FY24. Automotive held 13.7% share, down from 15.4% in the previous year. Entertainment and media captured 10.8% share, slightly below the 11.0% recorded in FY24.

The top five industry categories remained unchanged from June 2024, with retail benefiting from strong end-of-financial-year spend. This consistency suggests established patterns in seasonal advertising investment among major industry sectors.

Gai Le Roy, CEO of IAB Australia, commented on the results: "It is pleasing to again see solid growth in investment in digital advertising in FY25. Brands, large and small, are using advertising investment as a way of assisting growth. The continued increase in video consumption as well as range of video ad products has underpinned the increase of nearly 22% for the digital video ad market."

The data provides significant insight into Australia's digital advertising landscape transformation. Video formats have clearly established themselves as the primary growth driver, while traditional display advertising faces continued pressure from more engaging content formats.

Buy ads on PPC Land. PPC Land has standard and native ad formats via major DSPs and ad platforms like Google Ads. Via an auction CPM, you can reach industry professionals.

This growth trajectory aligns with broader global trends documented by PPC Land's coverage of European markets, where video advertising similarly demonstrated exceptional performance across multiple quarters in 2024.

Podcasting's share of total online audio advertising peaked at 41% for the quarter, with total audio advertising worth $85.6 million in June 2025. This represented 4.5% of total general display advertising expenditure, indicating audio content's growing role in Australia's media consumption patterns.

The shift toward programmatic buying reflects broader automation trends in digital advertising purchasing. Sixty percent of content publishers' video inventory was bought programmatically during the June quarter, demonstrating increased efficiency in media buying processes.

Social display and video advertising increased its market share from 15.7% to 17.0%, representing a 1.3 percentage point gain. This growth occurred alongside the 36.7% increase in social video spending, highlighting social platforms' effectiveness in capturing advertiser attention and budget allocation.

The report's findings demonstrate Australia's digital advertising market resilience despite global economic uncertainties. The 10.6% growth rate substantially exceeds inflation, indicating genuine expansion rather than price-driven increases.

Major events including the Olympics and federal election provided additional advertising stimulus during FY25. These events created increased competition for audience attention, driving higher spending across multiple advertising categories and platforms.

The data suggests Australian marketers have embraced video advertising's measurement capabilities and performance tracking advantages. Video formats provide detailed engagement metrics unavailable through traditional advertising channels, enabling more precise campaign optimization and budget allocation decisions.

Industry observers note the continued fragmentation of video advertising across multiple platforms. Unlike search advertising's concentration around major players, video advertising spend distributes across social media platforms, streaming services, and traditional broadcaster digital properties.

The 21.9% growth in video advertising significantly outpaced overall market growth of 10.6%, indicating substantial budget reallocation from other advertising categories. This reallocation reflects changing consumer media consumption patterns and advertiser recognition of video's superior engagement capabilities.

Australian digital advertising market trends mirror developments in other advanced economies, where video advertising has consistently demonstrated superior growth rates. The Australian market's projected retail media expansion suggests continued evolution in advertising technology and targeting capabilities.

Connected TV's slight share decline from 55% to 51% of content publishers' video inventory may reflect increased competition from social media video platforms. However, CTV maintains the largest component of this market segment, indicating continued viewer preference for television-style content consumption.

The classification of video advertising into social and non-social categories provides clearer insight into platform performance. Social platforms captured $1.9 billion of the $5.0 billion video advertising total, while non-social video advertising reached $3.1 billion during FY25.

Audio advertising's 14.1% growth rate exceeded overall market performance, suggesting potential for continued expansion as podcast consumption and streaming audio services gain popularity among Australian consumers. The $331 million total represents substantial advertiser investment in audio content monetization.

Desktop advertising's significant share increase within content publishers' video inventory from 29% to 37% challenges assumptions about mobile-first consumption patterns. This trend may reflect workplace viewing habits or premium content consumption preferences on larger screens.

The report provides comprehensive benchmarking data for Australian marketers planning FY26 budget allocations. Video advertising's demonstrated growth trajectory suggests continued investment opportunities, while search advertising's stable performance indicates reliable audience reach capabilities.

Industry category performance revealed shifting priorities among major advertisers. FMCG's entry into the top five categories reflects increased consumer goods marketing investment, while traditional categories like automotive experienced relative share decline despite absolute spending growth.

Australia's digital advertising market demonstrated remarkable resilience throughout FY25, with consistent quarterly growth patterns indicating structural rather than cyclical expansion. The continued growth despite global economic uncertainties positions the Australian market among the most robust globally.

The integration of Olympics coverage and election advertising created unique viewing patterns and advertising opportunities. These major events provided advertisers with expanded audience reach and engagement opportunities typically unavailable during standard broadcast schedules.

Video advertising's transformation from supplementary format to primary growth driver represents a fundamental shift in Australian digital marketing strategies. Brands have recognized video's superior storytelling capabilities and measurable engagement metrics compared to traditional display advertising formats.

The data indicates Australian digital advertising's continued maturation, with sophisticated measurement capabilities and diverse platform options providing marketers with unprecedented targeting precision and campaign optimization opportunities. This evolution positions Australia's digital advertising ecosystem among the most advanced globally.

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Video Advertising: The dominant growth category in Australian digital advertising, encompassing promotional content delivered through moving images and audio across multiple platforms. Video advertising reached $5.0 billion in FY25, representing a 21.9% increase year-on-year and capturing 29% of total digital advertising expenditure. This category includes social media video, broadcast video on demand (BVOD), connected television, and other video formats. The substantial growth reflects changing consumer media consumption patterns and advertiser recognition of video's superior engagement capabilities compared to static formats.

Search Advertising: The largest single category of digital advertising spend, maintaining 44% market share at $7.6 billion despite experiencing a slight 0.4 percentage point decline in relative share. Search advertising encompasses promotional messages displayed alongside search engine results, typically triggered by specific keywords or phrases entered by users. This category includes both traditional search engine advertising and emerging retail search advertising, which has gained significant traction as e-commerce platforms develop sophisticated advertising products.

Social Platforms: Digital environments including Facebook, Instagram, TikTok, YouTube, and other social networks that have become crucial advertising channels. Social platform video advertising increased 36.7% year-on-year to reach $1.9 billion, representing 38% of total video expenditure. These platforms offer sophisticated targeting capabilities, detailed engagement metrics, and direct consumer interaction opportunities that traditional advertising channels cannot provide. The growth demonstrates the increasing importance of social media in brand marketing strategies.

Digital Advertising: The comprehensive category encompassing all forms of online promotional activities, including search, display, video, audio, and social media advertising. The Australian digital advertising market reached $17.2 billion in FY25, growing 10.6% year-on-year. Digital advertising offers precise audience targeting, real-time performance measurement, and flexible budget allocation compared to traditional media channels. The sector's continued growth reflects businesses' increasing reliance on digital channels for customer acquisition and brand awareness.

Connected Television (CTV): Streaming video content delivered through internet-connected devices to television screens, encompassing services like Netflix, Amazon Prime Video, and local BVOD platforms. CTV investment represented 51% of content publishers' video inventory for FY25, down slightly from 55% in 2024. This category bridges traditional television advertising with digital advertising's targeting and measurement capabilities, offering advertisers premium video inventory with enhanced audience data and performance tracking.

Programmatic Advertising: Automated buying and selling of digital advertising inventory using technology platforms and algorithms. Sixty percent of content publishers' video inventory was purchased programmatically during the June quarter, demonstrating increased efficiency in media buying processes. Programmatic advertising enables real-time bidding, precise audience targeting, and optimized campaign performance through artificial intelligence and machine learning technologies. This automation reduces manual processes and improves advertising effectiveness.

IAB Australia: The Interactive Advertising Bureau Australia, the peak trade association for online advertising in Australia and one of over 43 IAB offices globally. IAB Australia supports sustainable and diverse investment in digital advertising across all platforms and releases the authoritative Internet Advertising Revenue Report (IARR) prepared by PwC Australia. The organization provides industry standards, research, education, and advocacy for digital advertising stakeholders including advertisers, agencies, publishers, and technology providers.

Growth Rate: The percentage increase in advertising expenditure compared to previous periods, indicating market expansion and investment trends. The Australian digital advertising market achieved a 10.6% growth rate in FY25, substantially exceeding inflation and demonstrating genuine market expansion. Growth rates vary significantly across categories, with video advertising achieving 21.9% growth while other formats experienced more modest increases. These metrics provide crucial insights for budget allocation and strategic planning.

Market Share: The percentage of total advertising expenditure captured by specific categories, platforms, or industry sectors. Search advertising maintained the largest market share at 44%, while video advertising represented 29% of total expenditure. Market share analysis reveals competitive dynamics, emerging trends, and shifting advertiser preferences across different advertising formats. Understanding market share distribution helps stakeholders identify growth opportunities and competitive threats.

Expenditure: The total monetary investment in digital advertising activities, measured across categories, time periods, and industry sectors. Australian digital advertising expenditure reached $17.2 billion in FY25, with video advertising expenditure of $5.0 billion leading growth. Expenditure analysis provides insights into advertiser confidence, economic conditions, and strategic priorities across different business sectors. The data enables industry benchmarking and strategic decision-making for marketing budget allocation.

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Who: IAB Australia and PwC Australia released the comprehensive Internet Advertising Revenue Report, analyzing spending patterns across major advertisers including retail, automotive, entertainment, finance, and FMCG sectors.

What: Australian digital advertising expenditure reached $17.2 billion in FY25, growing 10.6% year-on-year, with video advertising surging 21.9% to $5.0 billion and social platforms capturing $1.9 billion of video spend.

When: The report covers financial year 2025 (ending June 30, 2025) and was released on August 28, 2025, with particular focus on Q2 June quarter performance.

Where: Australia's digital advertising market across all platforms including search engines, social media, streaming services, and connected television, with desktop share increasing from 29% to 37%.

Why: Growth was driven by summer Olympics coverage, federal election advertising spend, continued video consumption increases, and brands using advertising investment to assist business growth during economic uncertainty.