Brainlabs study reveals three consumer search personas across 3,000 journeys

Research identifies traditionalists, augmenters, and dissenters as marketers face 2.5-platform purchase journeys with gender-based AI adoption gaps.

Research identifies traditionalists, augmenters, and dissenters as marketers face 2.5-platform purchase journeys with gender-based AI adoption gaps.

According to Brainlabs, a global performance marketing agency, consumers now use an average of 2.5 platforms when researching purchases in the US and 1.9 platforms in the UK. The findings, published on August 15, 2025, emerge from detailed analysis of 3,000 purchase journeys across both markets, revealing how search behaviors have fragmented into three distinct consumer profiles.

The study challenges prevailing narratives about Google's declining dominance while documenting the rise of AI and social search adoption. Rather than witnessing simple platform replacement, the research identifies a more complex landscape where different consumer segments follow entirely different research pathways.

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Will Akhurst, Chief Data Strategy Officer at Brainlabs, described the findings as revealing "three clear groups of users" rather than uniform behavioral shifts. The research categorized consumers into distinct personas based on their platform usage patterns and research preferences.

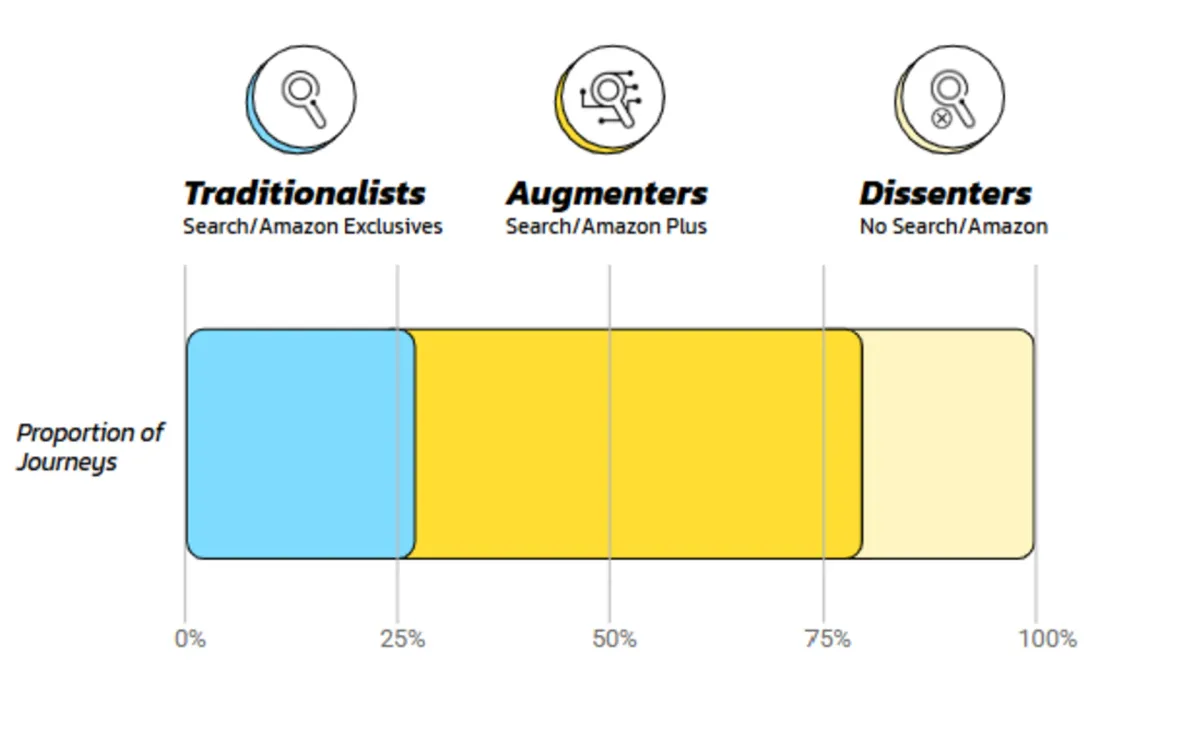

The Traditionalist represents older demographics maintaining exclusive loyalty to Google and Amazon. According to Brainlabs' analysis, this segment follows "the most direct path to purchase" without incorporating additional platforms into their research journey. These consumers demonstrate highly predictable behavior patterns, making them the most straightforward segment for marketers to reach.

The Augmenter constitutes the largest segment, primarily comprising mainstream consumers aged 25-44. This group begins their research on Google or Amazon but subsequently validates their choices across multiple platforms including YouTube and AI chatbots. The study found this approach represents the dominant consumer behavior pattern in both markets.

The Dissenter emerges as the most distinctive segment, with younger demographics bypassing traditional search engines entirely. These consumers discover products organically through social platforms like TikTok and Instagram, representing a fundamental departure from established search habits.

The research uncovered significant variations between US and UK markets, particularly in AI adoption patterns. AI platform search commands 7.9% share in the US compared to just 1.8% in the UK, indicating accelerated adoption rates among American consumers.

Social search adoption also varies geographically, with both markets showing high engagement but different platform preferences. The study found 69% of men and 66% of women use social platforms for product research, though specific platform choices differ between countries.

Brand websites demonstrate stronger performance in the UK market, representing 17% of search touchpoints compared to 8% in the US. According to Brainlabs, this disparity may reflect lower adoption of social and AI search platforms in the UK, allowing traditional customer journeys to maintain greater relevance.

The research revealed striking gender differences in AI tool usage for product research. Men demonstrate nearly twice the likelihood of using AI to supplement their searches compared to women, suggesting early adoption patterns may be gender-specific.

This finding carries particular significance for marketers targeting male demographics, especially in complex, information-heavy purchase categories such as finance, automotive, and technology. The data indicates these sectors may benefit most from Answer Engine Optimization (AEO) strategies targeting AI platforms.

Brainlabs documented category-specific platform preferences across different product types. Financial services showed heavy AI chatbot usage, while other categories demonstrated distinct platform clustering patterns.

The study found users develop "category-specific habits" rather than applying uniform search approaches across all purchases. This behavior suggests consumers instinctively select platforms based on the type of information they need and their confidence in different sources for specific product types.

Entertainment and lifestyle categories showed higher social platform adoption, while technical and financial purchases demonstrated greater AI chatbot engagement. These patterns indicate marketers must tailor platform strategies to specific product categories rather than applying universal approaches.

Buy ads on PPC Land. PPC Land has standard and native ad formats via major DSPs and ad platforms like Google Ads. Via an auction CPM, you can reach industry professionals.

Despite increased platform diversity, the research found Google and Amazon remain present in 81% of all user journeys. While these platforms represent only 45% of total touchpoints across the dataset, their widespread presence indicates continued importance for reaching maximum consumer audiences.

This finding suggests a nuanced relationship between platform diversification and incumbent dominance. Rather than losing relevance, Google and Amazon serve as foundation elements in most research journeys while consumers supplement these sources with additional platforms.

The data challenges assumptions about declining search engine usage while documenting the emergence of complementary research behaviors. Consumers appear to be expanding their research toolkit rather than replacing established platforms entirely.

Brainlabs commissioned the study to move beyond speculation about changing search behaviors. The research surveyed 3,000 representative consumers across the UK and US, focusing specifically on recent product purchase journeys rather than general search habits.

The methodology captured three key elements: purchase context across comprehensive product categories, complete platform toolkit usage, and journey start and end points. Participants identified which platforms they used for research, where their journey began, and where they completed their final purchase.

The study excluded frequency measurements, focusing instead on platform adoption patterns and journey complexity. This approach aimed to understand how traditional search habits evolve in an increasingly diverse platform ecosystem.

The research carries significant implications for media planning and budget allocation strategies. With Google and Amazon present in 81% of journeys despite commanding only 45% of touchpoints, advertisers face complex optimization decisions.

Akhurst noted that the findings reveal "the real story is one of curation, not chaos." Rather than navigating endless platform options, consumers develop efficient personal toolkits for specific research needs. This behavior creates predictable patterns marketers can leverage for targeted strategies.

The study suggests advertisers spending more than 80% of their budgets on Google and Amazon should consider diversification trials. However, the widespread presence of these platforms in consumer journeys indicates they remain essential foundation elements rather than optional components.

Consumer research journeys demonstrate sophisticated platform selection rather than random exploration. The study found users choosing specific platforms based on the type of information needed, personal preferences, and category-specific trust factors.

AI chatbot adoption varies significantly by product category, with financial services showing the highest usage rates. This pattern suggests consumers trust AI tools for information-heavy, comparison-driven purchases while preferring other sources for emotional or social purchase decisions.

Social platform research shows consistent adoption across genders but varies by product type. The data indicates social platforms serve dual purposes: inspiration for lifestyle categories and validation for mainstream purchases across demographics.

Despite increased platform diversity, the research documented surprisingly manageable journey complexity. The average research path involves fewer platforms than industry speculation might suggest, indicating consumers maintain focused rather than scattered approaches.

Platform combinations vary significantly between individual consumers, creating what Brainlabs describes as a "long tail" of personal research behaviors. This variation means marketers cannot predict specific journey paths but must prepare for multiple possible combinations.

The study found no dominant platform combination patterns beyond the presence of Google and Amazon in most journeys. This suggests successful marketing strategies require comprehensive platform coverage rather than optimized targeting of specific pathway combinations.

The research raises questions about whether observed differences between US and UK markets represent timing variations or fundamental cultural distinctions. US consumers show greater adoption of social and AI platforms, while UK consumers demonstrate stronger preference for direct brand and retailer relationships.

These patterns suggest two possible scenarios: either the UK market follows US adoption patterns with a lag, or fundamental cultural differences drive permanently distinct search behaviors. The data supports both interpretations, requiring continued monitoring to determine which proves accurate.

Current evidence indicates the transition away from traditional search duopoly follows different pathways in different markets. US dissenters migrate toward social and AI discovery platforms, while UK dissenters favor direct brand and retailer relationships.

The study positions current changes as fragments of a larger transition rather than temporary trends. Consumer behavior patterns suggest permanent shifts in how different demographics approach product research and purchase decisions.

Brainlabs data indicates successful marketing strategies must acknowledge these behavioral differences rather than assuming uniform adoption of new platforms. The research demonstrates that effective approaches require customization for specific consumer segments and geographic markets.

The findings suggest the future search ecosystem will remain fragmented rather than consolidating around new dominant platforms. This complexity requires marketers to maintain presence across multiple touchpoints while understanding how different segments navigate between platforms.

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Consumer Journey: The complete research and decision-making process consumers follow from initial product awareness to final purchase. Modern consumer journeys have evolved from linear paths through single platforms to complex, multi-touchpoint experiences spanning search engines, social media, AI chatbots, and direct brand interactions. The Brainlabs study reveals these journeys now average 2.5 platforms in the US and 1.9 in the UK, representing a fundamental shift from traditional single-platform research behaviors.

Platform Toolkit: The personalized combination of digital platforms each consumer uses for product research and information gathering. Rather than randomly exploring available options, consumers develop curated sets of preferred platforms based on category-specific needs, trust factors, and information types. This concept explains why users demonstrate consistent patterns in their research approaches while maintaining individual variations in specific platform combinations.

Search Personas: Distinct behavioral categories that group consumers based on their platform usage patterns and research preferences. The three personas identified by Brainlabs—traditionalists, augmenters, and dissenters—represent fundamentally different approaches to product discovery and validation. These classifications help marketers understand that consumer behavior has fragmented rather than uniformly shifted, requiring targeted strategies for each segment.

AI Chatbot Adoption: The integration of artificial intelligence-powered conversational tools into consumer research processes. The study found significant geographic and gender variations, with US consumers adopting AI tools at four times the rate of UK consumers (7.9% vs 1.8%) and men showing twice the likelihood of AI usage compared to women. This trend particularly affects information-heavy categories like financial services where AI tools provide comparative analysis capabilities.

Social Search: The practice of using social media platforms as primary information discovery tools rather than supplementary entertainment channels. Platforms like TikTok, Instagram, and YouTube serve dual purposes for product research and validation, with 69% of men and 66% of women incorporating social platforms into their purchase journeys. This behavior represents organic discovery methods that bypass traditional search engine intermediaries.

Google-Amazon Duopoly: The historical dominance of Google Search and Amazon in consumer research behaviors, representing the traditional foundation of most purchase journeys. Despite platform diversification, these platforms maintain presence in 81% of all consumer journeys while commanding 45% of total touchpoints. This persistent influence demonstrates their continued importance even as consumers expand their research toolkit with additional platforms.

Research Fragmentation: The division of consumer search behaviors into multiple distinct pathways rather than uniform adoption of new platforms. This concept explains why different demographic segments, geographic markets, and product categories show varying platform preferences. Fragmentation creates complexity for marketers who must prepare for multiple possible journey combinations rather than optimizing for single dominant pathways.

Purchase Context: The specific product category and buying situation that influences consumer platform selection and research intensity. Different categories demonstrate distinct platform clustering patterns, with financial services showing heavy AI usage while lifestyle categories favor social platforms. Understanding purchase context helps marketers predict which platforms consumers will likely use for specific product types and research phases.

Geographic Variations: The significant differences in platform adoption and consumer behavior patterns between US and UK markets. These variations raise questions about whether differences represent timing gaps in technology adoption or fundamental cultural distinctions in research preferences. US consumers show greater social and AI platform adoption while UK consumers demonstrate stronger preference for direct brand relationships.

Answer Engine Optimization (AEO): The emerging practice of optimizing content for citation and discovery by AI-powered search systems rather than traditional search engine rankings. This strategy becomes particularly relevant for brands targeting male demographics in complex purchase categories where AI tools provide comparative analysis. AEO represents a fundamental shift from ranking optimization to content authority and relevance for AI systems.

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Who: Brainlabs, a global performance marketing agency servicing clients including Capital One, Estée Lauder, and UNICEF US, conducted the research under the direction of Chief Data Strategy Officer Will Akhurst.

What: A comprehensive analysis of 3,000 consumer purchase journeys identifying three distinct search personas: traditionalists who rely exclusively on Google and Amazon, augmenters who validate choices across multiple platforms, and dissenters who bypass traditional search entirely.

When: The study was published on August 15, 2025, analyzing recent consumer behavior patterns to understand current search ecosystem dynamics rather than historical trends.

Where: The research covered both UK (1,000 respondents) and US (2,000 respondents) markets, revealing significant geographic differences in AI adoption rates and platform preferences between the countries.

Why: The study aimed to move beyond speculation about changing search behaviors and provide data-driven insights into how consumers actually research purchases in today's diversified platform ecosystem, helping marketers develop evidence-based strategies.