Consumer mobile app advertising budgets remain heavily concentrated on Google and Meta despite significant shifts in user behavior, according to new research released on August 12, 2025. The comprehensive study reveals that 88% of the $45 billion consumer mobile app advertising market flows to these major platforms, while marketers who diversify beyond these "walled gardens" achieve return on ad spend (ROAS) improvements of up to 214%.

According to the research titled Performance Through Independence: Unlocking Incremental App Growth Beyond Google and Meta, consumer app revenue experienced substantial growth in 2024. In-app purchase and subscription revenues climbed 25% to reach $70.5 billion, marking an acceleration that positions consumer apps to surpass gaming revenue for the first time within the next two years.

Subscribe the PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Subscribe

The disconnect between advertising spend allocation and actual user attention represents a critical opportunity for marketers. According to Moloco, the AI performance advertising company that conducted the research in collaboration with Sensor Tower and Singular, consumer app marketers allocate just 12% of their advertising budgets outside major walled gardens. This contrasts sharply with gaming marketers, who direct approximately 35% of their budgets to independent apps.

"Too many advertisers are still over-indexing on Google and Meta. But the biggest returns we are seeing are happening outside big tech," said Tom Shadbolt, Senior Insights Manager at Moloco. "The independent app ecosystem is quickly becoming the new engine for predictable and long-term performance. This research is a wake-up call for mobile app marketers."

Diversification delivers substantial returns across categories

The meta-analysis examined over $5 billion in ad spend across more than 2,000 gaming and consumer apps through Singular's client base. Results demonstrate clear advantages for marketers who expand beyond Google and Meta to include the Independent App Ecosystem—defined as millions of diverse mobile apps developed, published, and monetized by independent companies rather than major technology giants.

All gaming and consumer marketers who diversified their spending saw an average 48% increase in Day 30 ROAS. Consumer app marketers experienced even stronger performance, with an average increase of 116%. Among categories with statistically significant data, shopping, education, and health and fitness marketers achieved the strongest results, with average Day 30 ROAS improvements reaching 214%.

Mobile app usage patterns reveal fundamental changes in consumer behavior. While time spent on mobile apps has reached saturation in developed markets including the United States, United Kingdom, Germany, and Japan, emerging markets such as South Africa, India, and the Philippines continue experiencing surge in usage driven by expanding smartphone penetration.

More significantly, user attention within mature markets is fragmenting across diverse app categories. According to the research, time spent on social media apps declined by 2.4 billion hours year-over-year, while entertainment apps saw a 3.0 billion hour decrease. Conversely, gaming apps gained 1.2 billion hours, and generative AI apps surged by 1.3 billion hours.

The behavioral shift extends beyond simple category preferences. According to a Moloco/YouGov survey cited in the research, 53% of app users express desire to reduce social media usage. This sentiment intensifies among younger demographics, with 63% of 18-24 year olds and 65% of 25-34 year olds wanting to cut back on social platforms. The research attributes this trend to emotional fatigue, with 42% of 18-24 year olds reporting negative emotions when using platforms like Facebook or TikTok.

Independent apps reach massive scale

The Independent App Ecosystem captures significant mobile attention, reaching more than 2 billion daily active users (DAU)—comparable to TikTok and Instagram combined. This ecosystem encompasses over 3 million specialized apps that cater to specific interests, activities, and daily routines across diverse categories.

User behavior analysis reveals sophisticated patterns that challenge traditional targeting assumptions. E-commerce app users, for example, spend disproportionate time in casino games and news apps compared to the general population. Finance app users in Japan demonstrate significantly higher engagement with travel and sports apps than average users. These diverse usage patterns indicate that limiting campaigns to "relevant" categories leaves substantial opportunities unexplored.

The research demonstrates that high-value users interact with diverse app portfolios. E-commerce personas in the United States use an average of 21 Independent App Ecosystem apps monthly and encounter 13 ad opportunities within 24 hours. This fragmentation means successful user acquisition requires accessing varied publisher inventory rather than concentrating on narrow category definitions.

Contextual targeting gains prominence

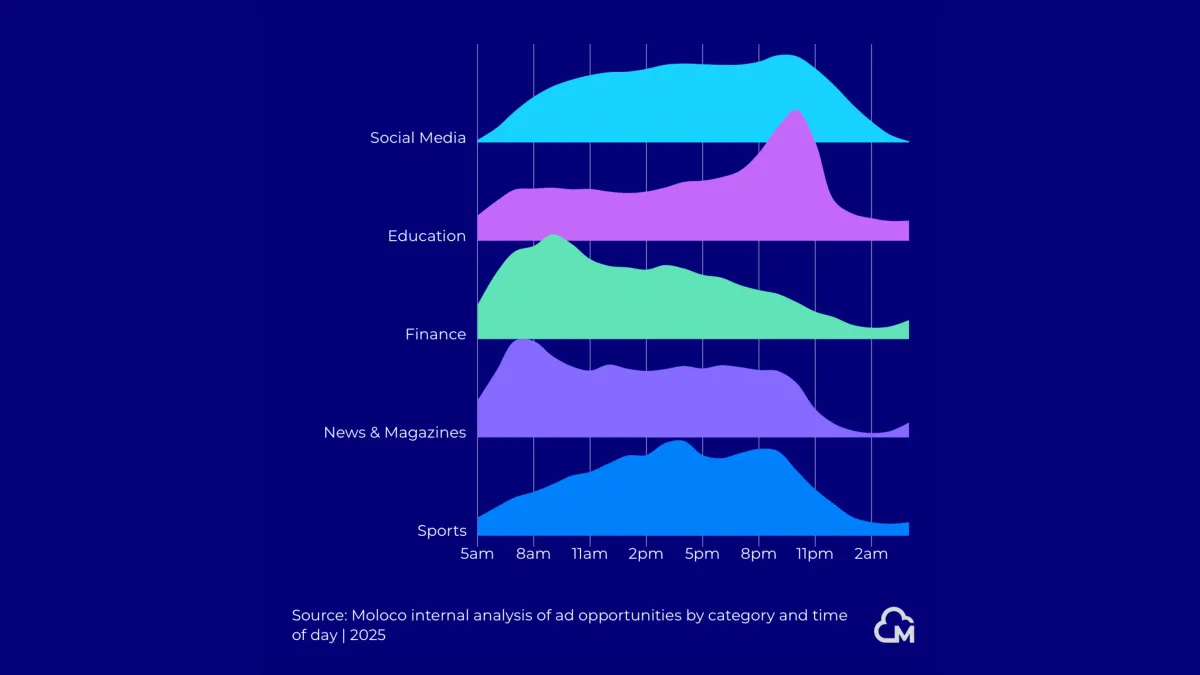

App usage varies significantly by time of day, creating distinct opportunity windows for marketers. Finance apps typically see morning engagement for market updates, while sports apps experience evening traffic spikes during live events. These temporal patterns influence user receptivity to advertising and conversion likelihood.

The research reveals that conversion patterns defy traditional category logic. Delivery and food marketers successfully acquire paying customers from utility apps. Travel app marketers generate conversions from productivity apps. Shopping app marketers discover buyers within gaming environments. These cross-category conversion opportunities highlight the value of broad reach across the Independent App Ecosystem.

"Since expanding our channels beyond social partners, we've seen an increase in platform bookings that we have been able to validate through incrementality modeling," said Valerie Castro, Acquisition Marketing Director at Turo. "We're excited to push performance further by increasing our creative velocity."

Privacy landscape drives ecosystem changes

App Tracking Transparency (ATT) opt-in rates for consumer apps averaged 36% in the first half of 2025, according to the research. This privacy-first environment accelerates adoption of alternative targeting methods including smart segmentation based on aggregated datasets, contextual targeting, and next-generation measurement solutions such as incrementality testing and marketing mix modeling.

The shift toward privacy-compliant advertising aligns with broader industry developments. E-commerce app installs dropped 14% despite 2% session growth as reported by Adjust, while partner diversification accelerated across e-commerce apps with median advertising partners increasing from 6 in 2023 to 7 in the first half of 2025.

Global market variations shape strategy

The research examined 13 countries including Australia, Brazil, Canada, France, Germany, India, Indonesia, Japan, Mexico, South Korea, the United Kingdom, the United States, and Vietnam. Regional differences in app engagement trends reflect distinct local preferences and behaviors.

The Asia-Pacific region demonstrates particular promise for Independent App Ecosystem growth. Finance apps experienced explosive growth with 119% revenue increase year-over-year in the first quarter of 2024, with APAC markets showing significantly lower effective cost per install metrics compared to global averages.

Consumer app growth trajectories vary substantially across markets, with emerging economies driving volume increases while mature markets focus on efficiency optimization. This geographic diversity creates opportunities for marketers to access growth markets through Independent App Ecosystem reach while maintaining presence in established territories.

Artificial intelligence integration emerges as a critical factor in advertising effectiveness across all app categories. The research notes how AI streamlines creative production by automating time-intensive tasks including ad concept generation and variant testing. Mobile advertisers increasingly integrate generative AI into creative development processes to accelerate campaign optimization.

Deep linking technology gains prominence as user journeys become increasingly complex across multiple touchpoints. According to the research, "The path to purchase is now multi-touch, multi-device, and increasingly shaped by omnichannel discovery." This complexity requires sophisticated attribution methods to accurately measure Independent App Ecosystem contributions to conversion outcomes.

The technological evolution aligns with industry-wide AI adoption trends. Nearly 90% of advertisers will use AI to build video ads by 2026 according to recent IAB research, indicating widespread acceptance of AI-powered creative tools across digital advertising channels.

Measurement challenges and solutions

Traditional marketing logic suggests concentrating spending within relevant app categories, but conversion data reveals different patterns. High-value users convert from unexpected sources across seemingly unrelated app environments. This diversity requires measurement approaches that capture cross-category attribution rather than relying on last-click models.

The research emphasizes the importance of incrementality testing to validate Independent App Ecosystem performance beyond self-reported metrics. Brands including Nestlé Purina and Turo have demonstrated measurable incremental performance gains through diversified media strategies that include independent apps alongside established platforms.

Performance measurement becomes increasingly sophisticated as marketers demand granular visibility into campaign effectiveness. According to testimonials in the research, marketers particularly value "reporting granularity—whether it's top-performing creatives or publisher-level insights" to enable confident testing and scaling decisions.

Industry implications for marketing professionals

The research findings present significant implications for digital marketing strategies. According to a 2025 Moloco/Marketing Dive study referenced in the report, nearly 50% of consumer app marketers have never explored advertising beyond Google and Meta. This gap represents substantial untapped potential for performance improvement.

The democratization of the digital advertising ecosystem, as evidenced by digital ad revenue hitting $259B with unexpected mid-tier growth, provides additional placement options beyond the largest technology platforms. Mid-tier companies increased market share by more than 3.1 percentage points compared to 2023, reaching 11% of total digital advertising revenue.

For marketing professionals operating in increasingly competitive environments, diversification beyond walled gardens offers both reach expansion and cost efficiency opportunities. The Independent App Ecosystem enables access to high-intent audiences during moments when they engage with specialized applications designed for specific tasks and interests.

The research methodology encompassed robust data thresholds including more than 30 apps and over $50,000 in ad spend or revenue per category. Results meet statistical significance requirements across multiple geographic markets and app categories, providing reliable benchmarks for strategic planning.

Consumer mobile app marketers face a critical decision point as user attention continues fragmenting across diverse digital environments. The research demonstrates clear financial benefits for brands willing to expand beyond traditional walled gardens to embrace the Independent App Ecosystem's reach and targeting capabilities.

Subscribe the PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Subscribe

Timeline

- August 12, 2025: Moloco releases research showing 88% of consumer mobile app ad spend concentrated on Google and Meta

- June 2025: Moloco/YouGov survey reveals 53% of app users want to reduce social media usage

- First half 2025: Consumer app revenue grows 25% to $70.5 billion, approaching gaming revenue levels

- 2025: App Tracking Transparency opt-in rates for consumer apps average 36%

- 2024: Independent App Ecosystem reaches over 2 billion daily active users

- 2024: Consumer mobile app advertising market reaches $45 billion globally

Related PPC Land coverage

Subscribe the PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Subscribe

PPC Land explains

Independent App Ecosystem: The Independent App Ecosystem represents millions of diverse mobile applications developed, published, and monetized by independent companies rather than major technology giants like Google, Meta, or Apple. This ecosystem encompasses over 3 million specialized apps that reach more than 2 billion daily active users globally. Unlike walled gardens, these apps operate independently and offer marketers access to highly targeted audiences engaged in specific activities, interests, and daily routines. The ecosystem provides contextual advertising opportunities across every app category, from finance and travel to gaming and productivity tools.

Return on Ad Spend (ROAS): ROAS measures the revenue generated for every dollar spent on advertising campaigns, serving as a critical performance indicator for marketing effectiveness. In the context of this research, Day 30 ROAS specifically tracks revenue attributed to advertising within 30 days of user acquisition. The study demonstrates that consumer app marketers who diversify beyond Google and Meta achieve ROAS improvements averaging 116%, with some categories reaching up to 214% increases. This metric validates the financial benefits of expanding advertising reach across independent apps rather than concentrating spend on major platforms.

Consumer Apps: Consumer apps encompass all mobile application categories outside of gaming, including entertainment, finance, delivery and food, productivity, social networking, health and fitness, and education apps. These applications generated $70.5 billion in combined in-app purchase and subscription revenue during 2024, representing 25% year-over-year growth. The research indicates consumer app revenue will surpass gaming revenue for the first time within the next two years, highlighting the sector's rapid expansion and advertising potential.

Walled Gardens: Walled gardens refer to closed ecosystems controlled by major technology companies, primarily Google and Meta, that maintain strict control over user data, advertising inventory, and campaign management tools. These platforms currently capture 88% of the $45 billion consumer mobile app advertising market despite user attention shifting toward more diverse app environments. The term emphasizes how these platforms limit advertiser access to external data and targeting options, creating dependency on their proprietary systems and measurement methodologies.

App Tracking Transparency (ATT): Apple's App Tracking Transparency framework requires apps to request user permission before tracking their activity across other companies' apps and websites. The research shows ATT opt-in rates for consumer apps averaged 36% in the first half of 2025, significantly impacting traditional advertising measurement and targeting capabilities. This privacy-first environment drives adoption of alternative targeting methods including contextual advertising, first-party data strategies, and incrementality testing to validate campaign performance.

Mobile App Revenue: Mobile app revenue encompasses all monetary income generated through mobile applications, including in-app purchases, subscription fees, and advertising revenue. Consumer mobile apps specifically achieved $70.5 billion in combined IAP and subscription revenue during 2024, demonstrating the substantial economic scale of the mobile app economy. This revenue growth trajectory positions mobile apps as critical channels for both user engagement and monetization, driving increased advertiser investment in mobile-first strategies.

User Acquisition: User acquisition refers to marketing strategies and campaigns designed to attract new users to download and engage with mobile applications. The research reveals that effective user acquisition increasingly requires reaching users across diverse app environments rather than concentrating efforts on major platforms. High-value users interact with an average of 21 Independent App Ecosystem apps monthly, creating multiple touchpoints for conversion across seemingly unrelated app categories.

Diversification: In mobile advertising context, diversification means spreading advertising budgets across multiple platforms and channels rather than concentrating spend on dominant players like Google and Meta. The research demonstrates that consumer app marketers who diversify their media mix achieve significantly higher ROAS compared to those maintaining majority spend on walled gardens. Diversification enables access to users during high-intent moments across specialized apps that serve specific functional and emotional needs.

Gaming Apps: Gaming apps represent the largest category within mobile app revenue generation, serving as a comparison benchmark for consumer app performance in this research. Gaming marketers have historically embraced diversification strategies, allocating approximately 35% of their advertising budgets to independent apps compared to just 12% for consumer app marketers. This category demonstrates mature advertising practices that consumer app marketers can adapt to improve their own performance outcomes.

Ad Spend: Ad spend represents the total monetary investment in advertising campaigns across all channels and platforms. The research analyzes over $5 billion in ad spend across more than 2,000 gaming and consumer apps to establish performance benchmarks. Consumer mobile app advertising specifically represents a $45 billion global market, with current allocation heavily skewed toward Google and Meta despite evidence supporting broader diversification strategies for improved returns.

Subscribe the PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Subscribe

Summary

Who: Consumer mobile app marketers, with research conducted by Moloco in collaboration with Sensor Tower and Singular

What: Study reveals 88% of $45 billion consumer mobile app advertising market concentrated on Google and Meta, while diversification to Independent App Ecosystem yields up to 214% ROAS improvement

When: Research published August 12, 2025, analyzing data from January-December 2024 across 13 countries

Where: Global study covering Australia, Brazil, Canada, France, Germany, India, Indonesia, Japan, Mexico, South Korea, United Kingdom, United States, and Vietnam

Why: User attention shifts away from traditional social media toward diverse app categories while advertising budgets remain concentrated on major platforms, creating performance optimization opportunities through diversified media strategies

Share this article

The link has been copied!