European retail media spending reaches €13.7 billion with 21.1% growth

IAB Europe reveals retail media now accounts for one-fifth of digital advertising as standardization challenges persist across 31 markets.

IAB Europe reveals retail media now accounts for one-fifth of digital advertising as standardization challenges persist across 31 markets.

European retail media advertising reached €13.7 billion in 2024, growing 21.1% compared to the previous year. IAB Europe released these findings on October 7, 2025, through its latest retail media statistics infographic compiled by Chief Economist Daniel Knapp. The data shows retail media now represents approximately one-fifth of total digital advertising expenditure across European markets, marking a significant milestone for the sector's maturation from experimental channel to strategic advertising infrastructure.

The growth trajectory contrasts sharply with broader market performance. While retail media surged by 21.1%, overall European advertising markets expanded at substantially lower rates, demonstrating retail media's position as one of the fastest-growing segments within digital advertising. This expansion reflects fundamental shifts in how brands allocate marketing budgets, with increasing emphasis on platforms that provide direct access to consumer purchase behavior and first-party data.

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

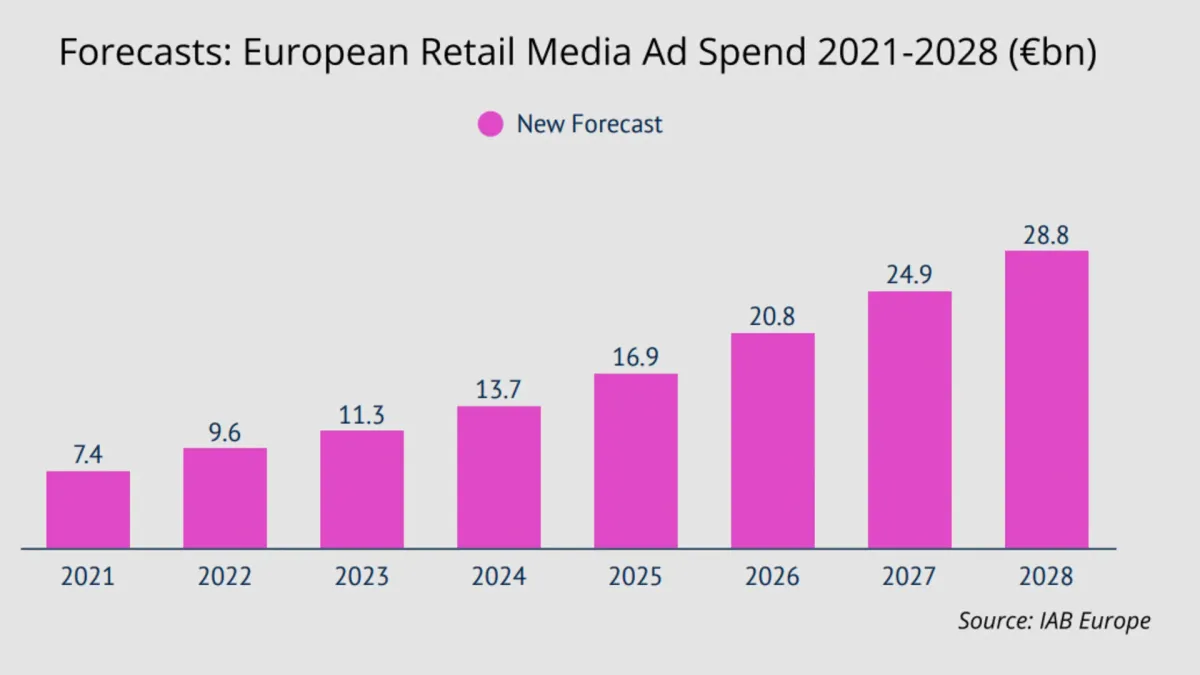

IAB Europe's forecast projects sustained expansion through 2028, with retail media spending expected to reach €28.8 billion. The projection indicates consistent growth patterns, with intermediate milestones including €16.9 billion in 2025, €20.8 billion in 2026, and €24.9 billion in 2027. These figures represent more than a doubling of retail media investment within four years, signaling structural changes in European advertising markets rather than temporary trends.

Historical data reveals the sector's rapid evolution. European retail media spending stood at €7.4 billion in 2021, climbing to €9.6 billion in 2022 and €11.3 billion in 2023 before reaching €13.7 billion in 2024. This progression demonstrates compound annual growth exceeding conventional digital advertising channels, driven by retailer monetization of customer data and digital properties.

The retail media channel now captures 20% of total digital advertising expenditure in Europe. Social media maintains the largest share at 32%, followed by search advertising at 28%, while other formats account for the remaining 20%. This distribution highlights retail media's emergence as a major advertising category comparable to established channels that required decades to achieve similar market penetration.

Budget reallocation patterns reveal how brands fund retail media expansion. Display advertising represents the primary source of shifted budgets, with 55% of advertisers redirecting spending from traditional display formats toward retail media platforms. Linear television follows at 45%, while programmatic advertising contributes 39% of reallocated budgets. Search advertising accounts for 24% of shifted spending, with print advertising at 21% and digital out-of-home at 21%. Connected television advertising contributes 5% of budget shifts, while other sources represent 3%.

European retail media partnerships extend as measurement challenges persist, with IAB Europe's Attitudes to Retail Media research revealing that brands working with four to six retail media networks doubled from 10% to 24% in 2025. This diversification strategy indicates advertisers seek broader reach across multiple retail environments rather than concentrating investments with dominant platforms.

First-party data access drives buy-side investment decisions. According to IAB Europe's Attitudes to Retail Media 2025 survey, 85% of buyers cite access to retailer first-party data as the key opportunity of retail media investment. This capability has become increasingly valuable as third-party cookie limitations expand across digital platforms, providing advertisers with alternative targeting mechanisms based on actual purchase behavior rather than inferred browsing patterns.

Standardization challenges represent the primary barrier to accelerated growth. The same survey indicates 53% of buyers cite lack of standardization as the key barrier to retail media investment. This fragmentation manifests across measurement methodologies, creative specifications, audience definitions, and reporting frameworks, forcing advertisers to navigate disparate systems when managing campaigns across multiple retail networks.

The technical infrastructure supporting retail media continues evolving toward greater interoperability. Criteo became the first onsite retail media partner for Google Search Ads 360 in September 2025, enabling advertisers to create campaigns across retail media inventory through unified interfaces. Similarly, retail media networks embraced real-time bidding for sponsored products through partnerships like Pentaleap and Teads, delivering programmatic solutions across multiple retail networks.

The Trade Desk enabled programmatic retail media buying through Koddi partnership, announced on October 9, 2025, with Gopuff serving as the initial launch partner. This integration addresses fragmentation by providing advertisers access to sponsored product ads and onsite retail placements through unified platforms, eliminating the need for separate campaign management across multiple retail media networks.

European market dynamics differ from global patterns while sharing common growth drivers. Retail media is projected to capture 20% of global advertising revenue by 2030, representing approximately $300 billion in spending according to Omdia research. This worldwide expansion reflects how retailers recognize the monetization potential of their customer data and digital real estate beyond traditional commerce activities.

Geographic expansion continues across European markets. MediaMarktSaturn launched its first offsite retail media program in September 2025, partnering with Unlimitail to extend advertising capabilities beyond owned digital properties. The rollout began in October 2025 across Germany, Spain, Italy, Netherlands, and Belgium, with Turkey, Poland, Austria, Switzerland, Luxembourg, and Hungary receiving access in early 2026.

Technology partnerships facilitate access to previously difficult-to-reach markets. Topsort partnered with Skai to deliver the first API integration providing access to retail media networks across 40 countries through unified global platforms. This collaboration enables advertisers to manage campaigns spanning international retailers and marketplaces including Poshmark, DoorDash, JustEatTakeaway, Cencosud, and LG Electronics through single interfaces.

Platform providers have introduced specialized capabilities addressing retail media requirements. Innovid unveiled retail media tools in July 2025, featuring platform integrations, self-service tools, shopping-oriented creative formats, and incrementality analytics designed to streamline execution across onsite and offsite campaigns. These capabilities respond to Mediaocean research indicating more than one-third of marketers plan to increase retail media network advertising spending.

Buy ads on PPC Land. PPC Land has standard and native ad formats via major DSPs and ad platforms like Google Ads. Via an auction CPM, you can reach industry professionals.

Non-traditional players have entered the market, expanding retail media beyond conventional retail boundaries. Mastercard launched its commerce media network on October 1, 2025, leveraging permissioned transaction data from more than 160 billion annual payments. The platform operates with 25,000 advertisers and reaches 500 million enrolled consumers across owned channels, bank outlets, and publishing partners worldwide.

Regional market data demonstrates widespread adoption patterns. UK retail media spending drives digital advertising growth, with online retail media hitting £1.5 billion in the first half of 2025 according to IAB UK's September 22, 2025 report. The forecast shows UK digital advertising expenditure reaching £45 billion by 2026, with retail media cementing its status as one of the sector's fastest-growing channels.

The marketing community faces both opportunities and operational challenges as retail media matures. Access to first-party data provides unprecedented targeting precision, while point-of-sale consumer reach enables advertising at critical decision moments. However, measurement fragmentation persists despite industry growth, with disparate methodologies making cross-platform performance comparison challenging for advertisers managing campaigns across multiple networks.

Industry responses to standardization gaps include IAB Europe's release of updated retail media definitions addressing buyer concerns. The organization's Retail & Commerce Media Committee has compiled guidelines targeting the 70% of buyers who cite lack of retail media standards as investment barriers. These efforts aim to establish common frameworks for measurement, creative specifications, and reporting that facilitate scaled adoption across European markets.

Organizational evolution accompanies budget expansion. Buy-side stakeholders maintaining retailer partnerships for more than one year increased from 50% to 63%, according to IAB Europe's Attitudes to Retail Media research. This longevity indicates retail media's transition from experimental tactics to strategic infrastructure requiring sustained investment and dedicated operational resources.

Investment patterns reveal growing sophistication in retail media strategies. While onsite retail media maintains dominance with over 90% of buyers allocating at least 41% of budgets to onsite formats, offsite investment demonstrated remarkable growth. The proportion of buyers allocating more than 41% of digital spending to offsite retail media jumped from 30% to 46%, primarily driven by display and social advertising formats.

Display advertisements lead offsite investment activity at 58% of buy-side spending, with social media maintaining 55% share. Connected television advertising captured 31% of offsite retail media budgets, highlighting the growing importance of video formats in retail media strategies. However, gaps exist between buy-side demand and sell-side availability, with only 19% of retailers currently enabling CTV placements despite 31% of buyers allocating offsite budgets to connected television advertising.

The European retail media expansion occurs amid broader digital advertising transformation. Privacy regulations, third-party cookie deprecation, and demand for transparent measurement have created favorable conditions for retail media platforms that leverage first-party data within privacy-compliant frameworks. These structural factors suggest sustained growth beyond current forecasts as advertisers seek alternatives to traditional targeting mechanisms.

Technical infrastructure supporting retail media continues evolving toward greater sophistication. Auction-based display technology, programmatic sponsored product solutions, and unified measurement frameworks represent recent innovations addressing advertiser requirements for efficiency and transparency. These developments enable retail media platforms to compete effectively with established digital advertising channels for budget allocation.

The sector's trajectory reflects fundamental changes in how advertisers approach digital marketing strategies. Rather than viewing retail media as supplementary to search, display, and social advertising, brands increasingly position retail media as core infrastructure for reaching consumers throughout the purchase journey. This strategic shift explains why retail media growth substantially outpaces broader market expansion, with budgets flowing from traditional channels toward retail environments.

For marketing professionals, the data underscores retail media's evolution from emerging trend to essential channel. The combination of first-party data access, point-of-sale reach, and measurable outcomes addresses persistent challenges in digital advertising, particularly as privacy regulations limit traditional targeting approaches. However, standardization gaps remain the primary obstacle to accelerated adoption, requiring industry collaboration to establish common frameworks enabling scaled investment across multiple retail networks.

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Timeline

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Who: IAB Europe, led by Chief Economist Daniel Knapp, compiled retail media statistics covering advertisers, agencies, and retail media networks across 31 European markets, with survey respondents representing organizations managing advertising budgets of €1 million or above.

What: European retail media advertising reached €13.7 billion in 2024, representing 21.1% growth and now accounting for one-fifth of total digital advertising expenditure, with forecasts projecting the market to reach €28.8 billion by 2028 despite standardization challenges cited by 53% of buyers.

When: IAB Europe released the retail media statistics infographic on October 7, 2025, documenting 2024 performance data and providing forecasts through 2028, following the organization's July 2025 Attitudes to Retail Media Report that surveyed 180 respondents between April and June 2025.

Where: The data covers European retail media markets, with 31 countries represented in the research, showing retail media now captures 20% of digital advertising spending, with budget shifts primarily coming from display advertising at 55%, linear television at 45%, and programmatic advertising at 39%.

Why: Retail media growth significantly outpaces broader advertising market expansion because 85% of buyers cite access to retailer first-party data as the key opportunity, enabling precise targeting and attribution measurement as third-party cookie limitations expand, though lack of standardization remains the primary barrier for 53% of buyers limiting further investment acceleration.