Media leaders expect 43% more traffic losses as AI reshapes journalism

Survey of 280 news executives reveals Google Search traffic fell 38% in US, with publishers pivoting to YouTube and AI platforms while questioning industry survival.

Survey of 280 news executives reveals Google Search traffic fell 38% in US, with publishers pivoting to YouTube and AI platforms while questioning industry survival.

The Reuters Institute for the Study of Journalism released its annual technology trends survey on January 12, showing that media leaders anticipate losing nearly half their remaining traffic over the next three years as artificial intelligence continues transforming how audiences consume news. The research, based on responses from 280 industry executives across 51 countries, documents an acceleration of challenges that have already decimated publisher revenues throughout 2024 and 2025.

News publishers have lost half their Google Search traffic in two years, with Web Search declining from 51% to 27% of referrals between 2023 and the fourth quarter of 2025. The Reuters survey confirms this trajectory shows no signs of reversing. Publishers expect an additional 43% decline in search traffic over the next three years, according to the executive responses compiled by Nic Newman.

Chartbeat data tracking more than 2,500 websites revealed global Google Search traffic declined 33% year-over-year comparing November 2024 to November 2025. United States publishers experienced even sharper drops at 38%. Since May 2023, global Google Search referrals have fallen 21%, with US traffic down 22% during the same period.

Google Discover traffic collapsed 21% globally and 29% in the United States year-over-year. The December core update destroyed Discover traffic for news sites, with some publishers reporting complete elimination of impressions within 24 hours. One operator managing four news websites described receiving over 100,000 clicks daily from Discover before December 12, then watching traffic fall to zero.

The survey results demonstrate fundamental shifts in publisher strategy as traditional distribution channels fail. Publishers are deprioritizing activities that drove success for two decades while embracing entirely new approaches to content creation and platform relationships.

YouTube emerged as publishers' highest-priority platform for 2026, recording a net score of +74 when measuring the balance between executives planning to invest more versus less effort. This represents a substantial increase from +52 in the 2025 survey, reflecting recognition that video distribution offers better resistance to AI disruption than text-based content.

The platform paid $70 billion to creators, media companies, and music partners over the past three years through its Partner Program, which now includes 3 million monetized channels. Publishers are attempting to tap into this revenue stream as traditional search traffic evaporates.

CNN announced plans to launch CNN Creators in 2026 with a purpose-built studio in Doha, Qatar. ABC News is preparing to launch ABC News Loop in Australia as a "made-for-social" explainer journalism brand. The Washington Post's Dave Jorgenson left the organization after eight years, demonstrating the pull that independent creator economics exert on talent. After his departure, the Washington Post Universe YouTube channel's views collapsed while his new independent venture overtook the institutional brand's performance.

DMG New Media, which operates the Daily Mail, has hired approximately 60 young creators to build vertical channels. The Independent signed YouTuber Adam Clery as creative director. These organizational changes reflect publisher acceptance that creator-style content production may offer better economic outcomes than traditional editorial models.

The survey found 76% of publishers plan to encourage journalists to behave more like creators. Exactly half plan to partner with creators for distribution, while 31% intend to hire creators directly and 28% are creating joint ventures or creator studios.

Seventy percent of executives expressed concern that creators are taking time and attention from traditional journalism. Thirty-nine percent worried about losing talent to the creator ecosystem. These concerns appear well-founded given the compensation disparities. YouTube Shorts achieved revenue per watch hour parity with traditional video in the United States during the third quarter of 2025, validating short-form content as commercially viable advertising inventory.

Publishers ranked AI platforms including ChatGPT, Gemini, and Perplexity at +61 on the net priority scale, making them the second-highest investment area after YouTube. This prioritization creates tension because current AI platform traffic remains negligible while potential licensing revenue stays uncertain.

ChatGPT accounts for 0.02% of total publisher traffic according to Chartbeat data, growing from essentially zero in July 2024. Perplexity contributes just 0.002% of referrals. Despite these minuscule traffic shares, publishers view licensing agreements with AI companies as critical revenue diversification.

Sixty-nine percent of executives expect at least some revenue from AI licensing within three years. Twenty percent anticipate significant income, while 49% expect minor contributions. Twenty percent expect no AI licensing revenue, and 11% don't know what to expect.

Google partnered with The Associated Press on January 15 to integrate real-time news content into its Gemini application. Neither organization disclosed financial terms. The New York Times has filed lawsuits against OpenAI regarding unauthorized content use, demonstrating the split between litigation and partnership strategies.

Dotdash Meredith reported during first quarter 2025 earnings that licensing revenue increased 30% year-over-year, driven primarily by its OpenAI partnership beginning in May 2024. The company experienced a 3% year-over-year decline in core user sessions partly attributed to AI Overviews appearing on roughly one-third of search results related to its content.

The Financial Times, The Guardian, Der Spiegel, El País, and other major publishers have secured individual deals with Google and OpenAI. Smaller publishers without resources to negotiate individual licensing agreements face traffic declines without compensation mechanisms.

TikTok ranked third in publisher priorities at +56, followed by Instagram at +41 and LinkedIn at +40. These platforms represent opportunities for audience development that don't depend on Google's algorithmic decisions.

Facebook traffic has fallen 43% since May 2023, though the platform showed a 9% year-over-year recovery in the most recent data. X (formerly Twitter) traffic declined 46% since May 2023, with a 15% year-over-year global increase masking a 22% decline in Europe.

Publishers assigned X a net priority score of -52, indicating widespread plans to reduce investment in the platform. This represents one of the sharpest negative scores in the survey. Facebook received -23, suggesting publishers view Meta's flagship social network as a declining asset despite its recovery from 2024 lows.

BlueSky scored -11 on the priority scale. The negative rating for a platform that launched recently indicates skepticism about whether alternative social networks can achieve sufficient scale to justify investment.

Traditional Google SEO scored -25 on the publisher priority index, marking a dramatic reversal for techniques that dominated digital publishing strategy for two decades. The deprioritization stems from recognition that ranking well in search results no longer guarantees traffic when AI Overviews and other features answer queries without requiring clicks.

Research from Ahrefs examining 300,000 keywords found that AI Overviews reduce organic clicks by 34.5% to 54.6% when present in search results. The study compared click-through rates for top positions with and without AI Overviews across identical time periods from March 2024 to March 2025.

Google's December 2025 core update finally wrapped after 18 days, creating ranking volatility that Glenn Gabe, a prominent algorithm analyst, characterized as landing "in a big way" for thousands of previously impacted sites. The Spectator recorded a 64% visibility decline, dropping from 2.4 to 0.9 in SISTRIX tracking. The Telegraph fell 30%, while Reuters decreased 31%.

Google Network advertising revenue, encompassing AdSense, AdMob, and Google Ad Manager, declined 1% to $7.4 billion during the second quarter of 2025. This marked the first year-over-year decline in years, suggesting reduced monetization opportunities as AI features keep users within Google's interface rather than directing them to publisher websites.

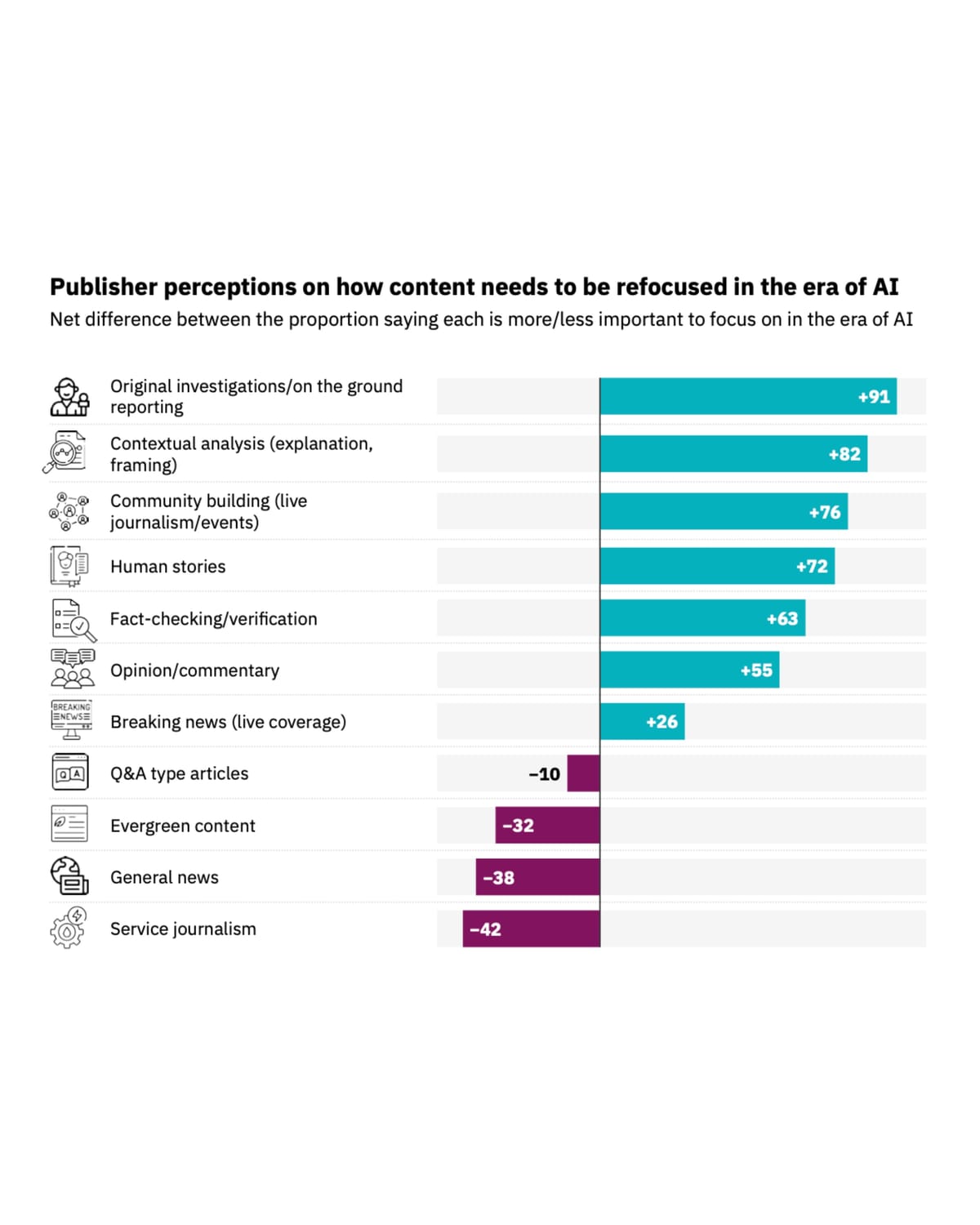

Publishers are making substantial changes to content priorities in response to these distribution challenges. Original investigations and on-ground reporting received the highest net score at +91 when executives rated their importance. Contextual analysis and explanation scored +82, while community building and live events rated +76.

Human stories scored +72, and fact-checking plus verification activities rated +63. These categories share characteristics that make them difficult for AI systems to replicate: original reporting requiring physical presence, nuanced analysis drawing on institutional knowledge, community relationships built over time, and verification expertise.

Service journalism scored -42 on the priority scale, marking it as the content type publishers most aggressively plan to abandon. Evergreen content rated -32, while general news scored -38. These categories face direct competition from AI systems that can answer service questions and provide general news summaries without requiring visits to publisher websites.

The strategic shift reflects acceptance that competing with AI for informational queries represents a losing proposition. Publishers are instead focusing on content types where human judgment, source access, and institutional authority create differentiation that AI cannot easily replicate.

Format priorities demonstrate similar adaptation. Seventy-nine percent of executives said video would become more important, with 41% rating it "much more important." Audio received similar treatment at 71% saying more important. Only 20% of executives rated text as becoming more important, suggesting widespread belief that written journalism faces the harshest AI competition.

Publishers are deploying artificial intelligence internally despite concerns about external AI platforms destroying their business models. Sixty-four percent of executives rated back-end automation including transcription, tagging, and copyediting as "very important" for their AI strategies.

Coding and product development using AI tools scored 44% very important, representing a 16 percentage point increase from the 2025 survey. Commercial applications including propensity models reached 33% very important. Newsgathering uses such as story identification and data interrogation scored 29% very important, as did content creation with oversight.

When asked about results from their AI initiatives, 44% of executives characterized them as "promising," while 42% said "limited." Only 13% described results as "transformational," suggesting most implementations haven't yet delivered breakthrough improvements.

Job impact from AI deployment has been minimal so far. Sixty-seven percent of publishers reported cutting no jobs due to AI, while 16% cut a small number. Nine percent added jobs related to AI implementation, and just 1% cut a significant number of positions.

The New York Times implemented AI to sift through podcasts and videos for investigations. A case involving Charlie Kirk required two weeks instead of what would have been more than a year manually. Helsingin Sanomat deployed HS Watchdog bots to monitor Russian Telegram channels. Reuters introduced FactGenie, a tool that halves the time required for non-corporate alerts used by 150 journalists globally.

Norway's iTromsø created Djinn, a tool that sifts through government documents. The implementation delivered six cover stories in a single week. India's Scroll added a slider bar allowing readers to adjust the depth of explainer content. Norway's VG implemented AI-generated "what's new since last visit" messages personalized to individual readers.

Seventy-five percent of executives expect "large" or "very large" impact from agentic AI over the next three years. These systems include AI browsers such as Atlas and Comet, plus agentic applications like Huxe and Pulse that can autonomously complete tasks rather than simply responding to queries.

Confidence in journalism overall has fallen dramatically. Sixty percent of executives expressed confidence in 2022. That figure dropped to 38% in the current survey, representing a 22 percentage point decline in four years. Eighteen percent now report being not confident in journalism's future, up from 10% previously.

Executives cited multiple reasons for declining confidence: uncertainty about AI adoption paths, loss of visibility in search and social platforms, traditional media losing touch with younger audiences, and political attacks on journalism undermining public trust.

Confidence in respondents' own businesses remained higher at 53%, similar to 2025 levels. This gap between confidence in the overall industry versus individual organizations suggests executives believe their specific companies can navigate challenges even as the broader journalism ecosystem struggles.

Fifty-two percent of executives believe AI-generated content and misinformation will strengthen news media's competitive position, up from 41% in 2025. Twenty-seven percent believe it will weaken their position. The reasoning centers on trusted news brands potentially gaining value as audiences struggle to distinguish reliable information from AI-generated content of uncertain quality.

TikTok has generated more than 1 billion AI videos. Nearly one in 10 of the fastest-growing YouTube channels show only AI-generated content. France documented more than 4,000 fake news sites powered by generative AI. NewsGuard research shows zombie local news sites in the United States now outnumber real local news outlets.

Publishers hope this deluge of low-quality AI content will drive audiences toward established brands with verification processes and editorial standards. Whether this dynamic will offset traffic losses from AI features in search platforms remains uncertain.

Commercial publishers excluding public broadcasters ranked subscription and membership as their top revenue priority at 76%. Display advertising scored 68%, down from 81% in 2020. Native advertising reached 64%, representing a 5 percentage point increase driven primarily by short-form video opportunities.

Events, both physical and online, scored 54%, up 6 percentage points as publishers seek in-person revenue streams resistant to digital disruption. Platform funding including AI licensing scored 37%, representing a 17 percentage point increase over two years.

Philanthropy and foundation funding rated 18%, down 2 percentage points as United States-based funding sources contract. This decline particularly affects nonprofit news organizations that expanded during the previous decade based on expectations of sustained philanthropic support.

The IAB's 2026 Annual Leadership Meeting features zero sessions addressing publisher revenue challenges, according to criticism from Andy Batkin, CEO of Duration Media. The organization, which originally launched exclusively to serve publishers, now dedicates programming to advertiser concerns while publishers face existential threats.

Digital advertising revenue concentration among the top 10 technology companies reached 80.8%, with companies ranked 11 through 20 capturing just 5.9% of total spending. This concentration demonstrates platform power that makes publisher negotiations increasingly asymmetric.

The IAB Europe released technical standards in September 2025 requiring AI platforms to compensate publishers for content ingestion. The framework establishes three mechanisms: content access controls, discovery protocols, and monetization APIs. Implementation remains uncertain as major AI companies have not committed to adopting these standards.

Cloudflare data showed pages crawled to visitors referred ratios deteriorating from 2:1 to 18:1 in June 2025. OpenAI's ratio reached 250:1 and then 1,250:1, indicating the company crawls content at rates vastly exceeding the traffic it sends back to publishers. Unauthorized scraping increased 40% between the third and fourth quarters of 2024.

More than 80 media executives met in New York on July 30, 2025, under the IAB Tech Lab banner to discuss collective responses. Google and Meta sent representatives. OpenAI, Anthropic, and Perplexity notably did not attend, suggesting these AI-native companies see limited benefit in industry coordination that might constrain their access to training data.

Current traffic distribution shows dramatic shifts from historical patterns. Google Discover now accounts for 13% of total referrals to news publishers. Google Search contributes 7.3%, Facebook provides 3.3%, and X delivers 0.3%. ChatGPT and Perplexity combined represent less than 0.03% of traffic.

This distribution creates problems beyond the obvious traffic declines. Google Discover operates through recommendation algorithms that publishers cannot predict or optimize for systematically. Content that receives Discover distribution achieves massive reach, while content excluded receives minimal visibility. Publishers have no reliable method for understanding which articles will receive distribution.

One publisher described this as asymmetric dependency, where content creators must produce material suited to Discover's algorithms while having minimal influence over distribution decisions. This contrasts with traditional search, where optimization practices could improve rankings through established techniques.

The European Commission launched a formal antitrust investigation on December 9, 2025, examining whether Google violated EU competition rules by using publisher content for AI purposes without appropriate compensation or viable opt-out mechanisms. Brussels regulators assessed whether Google imposed unfair terms on publishers while granting itself privileged access to training data that competitors cannot obtain.

Pew Research found that just 1% of users click links when AI Overviews appear in search results. This engagement rate makes AI features functionally equivalent to no-click search for publishers, providing no traffic despite featuring their content.

Marfeel's monitoring research published December 18, 2025, found 51% of Google Discover feed positions in test markets now consist of AI Summaries. Seventy-seven percent of AI Summary exits default to inline YouTube plays rather than publisher links. Publishers receive brand visibility through multi-icon displays but minimal traffic as primary user actions route to Google-owned properties.

Some publishers are exploring revenue-sharing arrangements with platforms. Vox Media secured revenue-share deals with creators for podcasts including Pivot and Hacks on Tap. The Washington Post launched Ripple, offering revenue-share partnerships with independent Substack writers.

Perplexity introduced a revenue-sharing subscription model where the company distributes 80% of user fees to participating publishers based on engagement metrics. This model addresses the zero-click problem by providing compensation without requiring traffic, though adoption remains limited.

Really Simple Licensing (RSL) Collective has organized more than 50 publishers including Penske Media, Ziff Davis, Yahoo, BuzzFeed, USA Today, and Vox Media to negotiate collectively with AI platforms. The collective licensing approach mirrors music rights societies but faces challenges establishing usage measurements and allocation formulas.

WordPress.com partnered with Perplexity AI for content discovery. Google expanded Preferred Sources globally on December 10, 2025, while piloting AI-powered article overviews with major publishers including The Guardian. These partnerships attempt to maintain publisher relationships while deploying AI features that reduce traditional click-through patterns.

The commercial partnerships Google announced included The Guardian, Der Spiegel, El País, Folha de S. Paulo, Infobae, Kompas, The Times of India, The Washington Examiner, and The Washington Post. Google has not disclosed payment amounts. These selective arrangements create two-tier systems where major publishers secure individual deals while independent outlets face traffic declines without compensation mechanisms.

Traffic patterns vary substantially by geography. UK website traffic growth collapsed 86% since Google's AI search rollout, according to Tank research tracking 800 companies across 16 sectors. Average monthly organic traffic growth fell from 26.3% to 3.7%. Hospitality experienced the worst performance at -6.7% growth. Ranking pages declined 11.1%, down from positive 14.1% growth the previous year.

India news sites plummeted during the December update, with SISTRIX tracking showing Hindustantimes.com visibility dropping from above 6 points to below 2 points during the 18-day rollout between December 11 and December 29.

The Reuters survey covered 51 countries, ensuring geographic diversity in responses. Sixty-four editors-in-chief participated alongside 64 CEOs and 51 heads of digital or innovation. This executive-level perspective differs from practitioner surveys, focusing on strategic decisions rather than tactical implementation.

The Reuters findings carry significant implications for digital marketing. Traffic sources that supported programmatic advertising for decades are failing. Publishers implementing paywalls and reducing free content will decrease available advertising inventory. Video and audio formats gaining priority have different advertising characteristics than text-based content.

Creator partnerships offer brands access to audiences but require different relationship models than traditional media buying. YouTube's Partner Program provides standardized creator monetization, potentially simplifying brand collaborations. However, creator content quality and brand safety vary more than traditional publisher inventory.

The shift toward community building and events creates opportunities for experiential marketing but reduces scalable digital advertising placements. Subscription growth limits addressable audiences for advertising-supported campaigns.

AI platform advertising remains nascent. OpenAI explored sponsored content in ChatGPT responses in December, though implementation details remained undisclosed. Google introduced advertising in AI Overviews during May 2025, competing directly with publisher inventory for queries where AI features appear.

Publishers pivoting away from service journalism and evergreen content will reduce advertising inventory for commercial intent queries. Brands previously targeting these content types through contextual advertising must identify alternative placements.

The concentration of advertising revenue among top technology platforms reached 80.8%, limiting publisher negotiating power. Brands seeking diverse media mix options face shrinking independent publisher inventory as consolidation accelerates.

Who: The Reuters Institute for the Study of Journalism surveyed 280 media leaders including 64 editors-in-chief, 64 CEOs, and 51 heads of digital or innovation across 51 countries during November and December 2025. Chartbeat provided traffic data from more than 2,500 websites. NewzDash analyzed 400+ news publishers worldwide.

What: Publishers experienced 33% global Google Search traffic decline year-over-year (38% in US), with Web Search falling from 51% to 27% of Google referrals between 2023 and Q4 2025 while Discover climbed to 68%. Executives expect an additional 43% traffic decline over the next three years. Publishers are shifting priorities toward YouTube (+74 net score), AI platforms (+61), and TikTok (+56) while deprioritizing traditional Google SEO (-25), X (-52), and Facebook (-23). Content strategy emphasizes original investigations (+91), contextual analysis (+82), and video (79% saying more important) while abandoning service journalism (-42) and evergreen content (-32).

When: The Reuters survey occurred November-December 2025 with publication January 12, 2026. Traffic declines began accelerating from the inflection point in late October 2024 when AI Overviews rolled out to 100+ countries. The December 2025 core update between December 11-29 destroyed remaining Discover traffic for many publishers.

Where: Traffic declines affect publishers globally but show regional variations: US publishers experienced 38% year-over-year Search traffic decline versus 33% globally; UK organic traffic growth collapsed 86%; India news sites plummeted during December update. Google Discover now accounts for 13% of total publisher referrals, Google Search 7.3%, Facebook 3.3%, and X 0.3%.

Why: The transformation matters for the marketing community because it represents fundamental shifts in content distribution, with publishers pivoting from search optimization to video, creator partnerships, and AI platform licensing while traditional advertising inventory shrinks. Google Network revenue declined 1% to $7.4 billion in Q2 2025 as AI features keep users within Google's interface. Sixty-nine percent of publishers expect AI licensing revenue within three years, though 52% believe AI-generated content will strengthen rather than weaken news media's competitive position as audiences struggle to distinguish reliable information from low-quality AI content.