Microsoft on June 30, 2026 published its first country-by-country tax report under an EU transparency directive, showing the company generated 47.1 billion dollars in pretax profit in Ireland against 661 million dollars in Germany, Europe's largest economy, in the fiscal year ending June 2025.

The filing, required under Chapter 10a of Directive 2013/34/EU, breaks down Microsoft's revenue, profit, income tax and headcount across 27 European Union member states plus five additional jurisdictions, including Panama and Turkey. It is the kind of granular, country-level financial disclosure that companies have previously shared only with tax authorities, not the public. Microsoft appears to be among the first major American technology companies to publish such a report following the rollout of the EU's country-by-country reporting directive, according to reporting in The New York Times.

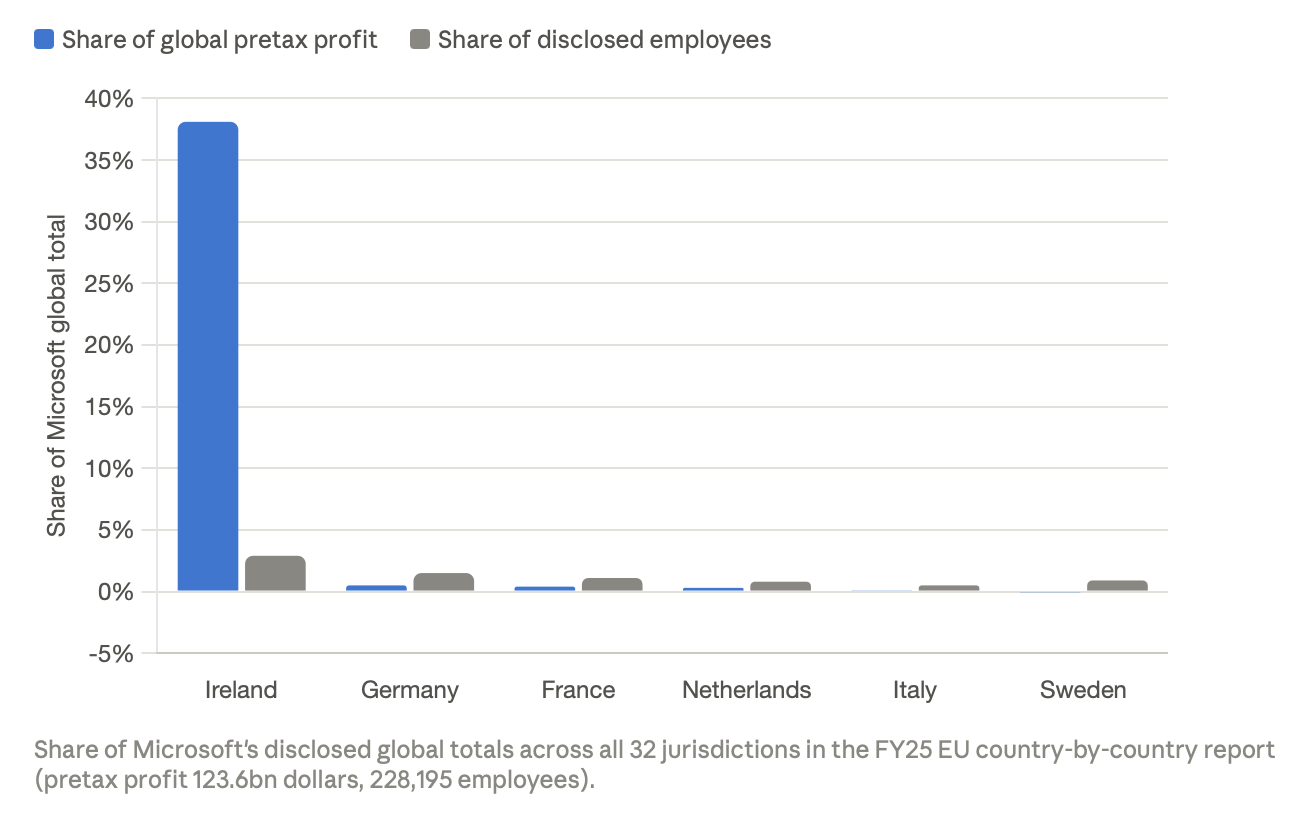

Ireland dominates the numbers. According to the report filed under the directive, Microsoft generated 196 billion dollars in revenue and 47.08 billion dollars in profit before income tax in Ireland during the twelve months to June 30, 2025, while employing 6,654 people there. That single country accounted for roughly 38 percent of Microsoft's entire worldwide pretax profit, a total that includes every other country the company operates in, the United States among them, folded into the filing's aggregated "rest of world" line, even though Ireland's share of the disclosed workforce came to under 3 percent. Germany, by contrast, generated 11.7 billion dollars in revenue but only 661 million dollars in profit before tax, despite employing 3,471 people, roughly half of Ireland's headcount.

Jeff Bullwinkel, Vice President and Deputy General Counsel for Microsoft EMEA, published the disclosure alongside a company blog post the same day, framing the release as a proactive step ahead of scrutiny the numbers might otherwise invite. "We have provided this kind of information directly to tax authorities for several years under the Organization for Economic Cooperation and Development (OECD) framework," Bullwinkel wrote. "It is now published to support transparency commitments, and we believe it is important to proactively address any questions these disclosures may raise, recognizing that numbers on a spreadsheet rarely tell the full story."

What the report actually discloses

Section 2 of the filing lists, for each tax jurisdiction, five figures: revenue, profit or loss before income tax, income tax paid on a cash basis, income tax accrued for the current year, and accumulated earnings, alongside the number of employees. Thirty-one lines appear individually, covering the 27 EU member states along with Panama, the Russian Federation, Trinidad and Tobago, Turkey and Vietnam. A thirty-second line aggregates "all other tax jurisdictions" worldwide, reporting 279.2 billion dollars in revenue and 74.6 billion dollars in profit before tax across 198,843 employees, a figure that includes the United States and therefore dwarfs any single European country in the table.

Section 3 lists the underlying corporate entities behind each jurisdiction's figures. Ireland alone accounts for more than twenty separate Microsoft-affiliated legal entities, including Microsoft Ireland Operations Limited, which the filing identifies as covering manufacturing, sales, marketing, distribution, purchasing and services to unrelated parties, a broader functional scope than most of the sales-and-distribution-only entities listed for other EU countries. Germany's entities, including Microsoft Deutschland GmbH and LinkedIn Germany GmbH, are described mainly under sales, marketing and distribution, along with several research and development units tied to gaming studios acquired through Activision Blizzard and ZeniMax.

The filing separates two tax measures that are often conflated: income tax paid on a cash basis and income tax accrued for the year. Bullwinkel's blog post explained the difference directly. "Accrued tax is what you owe for the year. Tax paid is the amount actually paid during the year," he wrote, adding that the two figures "can differ because the timing of owing tax and paying tax doesn't match exactly." France illustrates the gap. The country-by-country table shows negative 96.4 million dollars in cash tax paid for France in the reporting year, a result Bullwinkel attributed to a one-time refund of tax the company had overpaid in an earlier year. "Microsoft paid 374 million dollars in tax in France over the prior three years," he wrote, arguing that the single-year cash figure should not be read as representative on its own.

Ireland's outsized share, by the numbers

The scale of the Ireland-Germany gap becomes clearer against the totals across all thirty-two lines in the filing. Summing every jurisdiction disclosed, Microsoft reported approximately 123.6 billion dollars in worldwide pretax profit and 228,195 employees across the categories covered by the report. Against that total, Ireland's 47.08 billion dollars represents close to 38 percent of profit while carrying under 3 percent of the disclosed workforce. Germany's 661 million dollars comes to roughly half of one percent of the same profit total, despite the country holding about 1.5 percent of the workforce, a figure similar to Ireland's own headcount share. According to the New York Times, excluding Ireland altogether, Microsoft generated less than 2 percent of its worldwide pretax earnings across the rest of Europe combined, a figure that lines up closely with a recalculation from the raw filing, which puts Europe excluding Ireland at roughly 1.5 percent of the same global total.

Income tax figures follow a similar pattern to profit, though not identically. Ireland's income tax accrued for the year came to 6.65 billion dollars, and its cash tax paid came to 5.58 billion dollars, a difference of more than a billion dollars between the two measures within a single jurisdiction. Sweden presents an unusual case in the opposite direction: the country reported an 81.4 million dollar pretax loss for the year, yet still recorded 143.7 million dollars in income tax accrued and 288.8 million dollars in cash tax paid, driven by accumulated earnings the filing lists at negative 983.8 million dollars, reflecting historical results rather than the single reporting year.

Company-wide context beyond the country tables

Bullwinkel's blog post placed the country-level figures inside a broader account of Microsoft's tax position and investment activity. Companywide, he wrote, Microsoft ranks second globally in corporate income taxes paid over the past year, according to S&P, with a total of 28.7 billion dollars, a figure covering all jurisdictions worldwide rather than the European set disclosed in the country-by-country filing. Within the EU specifically, Bullwinkel wrote that the company paid 6.3 billion dollars in income tax for fiscal year 2025, a figure that lines up closely with a recalculation of cash tax paid across the 27 EU member states listed in the report, and one that Bullwinkel noted excludes payroll tax, value added tax, property tax and other categories paid in addition.

The blog post also detailed capital investment figures unconnected to the tax filing itself. Microsoft's total capital expenditure reached 176 billion dollars over the three years ending June 30, 2025, according to the post, alongside 89.2 billion dollars spent on research and development in the markets where the company operates over the same period. Bullwinkel cited a 2024 study by IDC on partner profitability, stating that for every dollar of Microsoft revenue, partners providing services generate 8.45 dollars, and partners developing software generate 10.93 dollars, though he noted these multipliers vary by country and partner segment.

Microsoft's European history, as described in the blog post, dates to 1982, when the company opened its first European office in the United Kingdom, followed by France and Germany in 1983, and then Denmark, Ireland, Italy, Norway, Spain and Sweden in 1985. The post describes Ireland as the company's largest hub in the region. Microsoft states it is now present in all 27 EU member states.

The disclosure's regulatory backdrop

The country-by-country reporting directive under which Microsoft filed traces to Chapter 10a of Directive 2013/34/EU, a measure requiring large multinational companies operating in the EU to publish, on a country-specific rather than consolidated basis, the kind of financial detail previously shared only with tax authorities under OECD information-exchange rules. According to the New York Times, other American companies will soon need to produce comparable reports as the same directive takes effect more broadly, meaning Microsoft's filing functions as an early test case for how such disclosures will be read and interpreted once they become commonplace across large multinationals with European operations.

The filing itself states, in Section 1, that the information was not prepared according to the tax-purpose reporting instructions under Section III, Parts B and C of Annex III to Directive 2011/16/EU, distinguishing the EU public disclosure format from the separate confidential reporting Microsoft has made to tax authorities for years under the OECD's base erosion and profit shifting framework. Section 4 of the filing states that no information was omitted for the financial year covered, and none was omitted in a previous year that required disclosure in the current filing.

Beyond the two source documents at the center of this report, PPC Land has tracked a wider pattern of European regulatory pressure on major US technology and advertising companies through 2026, spanning data protection, platform design and cross-border data flows. The European Commission found Meta and Instagram in preliminary breach of Digital Services Act obligations tied to addictive design features, exposing the company to a fine of up to 6 percent of global turnover. Separately, noyb chair Max Schrems called on the European Commission to begin an orderly withdrawalfrom the EU-US Data Privacy Framework adequacy decision, after a US Supreme Court ruling undermined the independence of the Federal Trade Commission, a body the Commission's own adequacy decision cites more than 250 times. Both cases illustrate a regulatory environment in which large American technology and platform companies operating in Europe face increasingly granular disclosure and compliance obligations across multiple legal frameworks simultaneously, of which the tax transparency directive under which Microsoft filed is one strand among several.

Why this matters for marketers and advertisers

For a trade audience focused on paid media, programmatic infrastructure and platform economics, a corporate tax filing might seem several steps removed from campaign management. It is not. Microsoft Advertising, LinkedIn and Microsoft's cloud and AI infrastructure businesses all sit inside the same corporate structure whose profit allocation this filing describes, and the entities named in Section 3, including LinkedIn Ireland Unlimited Company and Microsoft Ireland Operations Limited, are directly connected to the commercial infrastructure that advertisers and publishers already transact through. Ireland's Data Protection Commission, the lead EU regulator for most major American technology companies including Microsoft, has separately faced scrutiny over enforcement consistency, a dynamic PPC Land has covered in the context of stalled GDPR appeals. A jurisdiction that already carries outsized regulatory significance for data protection purposes now also emerges, through this filing, as the jurisdiction carrying an outsized share of one major advertising and cloud platform's disclosed profit.

The wider pattern of EU transparency rules extending into new corners of corporate disclosure, seen already in DSA advertising transparency obligations, AI Act labeling requirements and now country-by-country tax reporting, means that marketing and advertising professionals working with major platform vendors are likely to see more, not fewer, granular public disclosures about how those vendors structure their European operations going forward. Understanding where a vendor's profit, tax and legal entities sit is not directly actionable for day-to-day campaign work, but it does inform how advertisers evaluate the durability, jurisdictional exposure and regulatory risk profile of the platforms carrying an increasing share of global media spend.

Timeline

- 1982 - Microsoft opens its first European office, in the United Kingdom.

- 1983 - Microsoft expands into France and Germany.

- 1985 - Microsoft expands into Denmark, Ireland, Italy, Norway, Spain and Sweden; Ireland becomes the company's largest regional hub.

- July 1, 2024 - Start of the fiscal year covered by Microsoft's country-by-country report.

- June 30, 2025 - End of the fiscal year covered by the report.

- June 30, 2026 - Microsoft publishes its first Public Country-by-Country Report and an accompanying blog post from Jeff Bullwinkel.

- July 3, 2026 - The New York Times publishes an analysis of the disclosure, describing it as a rare look into corporate profit-shifting practices.

Related PPC Land coverage

- Meta faces 6% turnover fine as EU finds Instagram breach addictive design - Covers a separate EU enforcement track under the Digital Services Act, illustrating the wider regulatory pressure facing large American technology platforms operating in Europe.

- Supreme Court FTC ruling sinks EU-US data deal, noyb says - Details a parallel legal challenge to the EU-US data transfer framework, including reference to Ireland's Data Protection Commission as lead regulator for major American technology companies.

- Microsoft Monetize fuses LinkedIn profile data into CTV via three DSPs - Provides background on the LinkedIn and Microsoft Monetize commercial entities named in the tax filing's list of European subsidiaries.

Summary

Who: Microsoft Corporation, through Jeff Bullwinkel, Vice President and Deputy General Counsel for Microsoft EMEA, published the disclosure. The New York Times, through reporters Jesse Drucker and Karen Weise, subsequently analyzed the filing.

What: Microsoft published its first Public Country-by-Country Report under Chapter 10a of Directive 2013/34/EU, disclosing revenue, profit before tax, income tax paid and accrued, and employee counts across 27 EU member states and five other jurisdictions. The filing showed Ireland generating approximately 38 percent of disclosed global pretax profit with under 3 percent of the disclosed workforce, compared with Germany's roughly half of one percent of profit despite a larger local headcount than Ireland's.

When: The report covers the fiscal year from July 1, 2024, to June 30, 2025. Microsoft published the report and blog post on June 30, 2026. The New York Times published its analysis on July 3, 2026.

Where: The disclosure covers Microsoft's operations across all 27 European Union member states, plus Panama, the Russian Federation, Trinidad and Tobago, Turkey and Vietnam, with additional context describing Microsoft's presence in the region dating to its first European office in the United Kingdom in 1982.

Why: The filing is required under a relatively new EU transparency directive that compels large multinational companies to disclose country-level financial detail publicly rather than only to tax authorities. Microsoft's report is among the earliest such disclosures by a major American technology company, positioning it as an early reference point for how the public, journalists and regulators interpret this category of information as more companies become subject to the same requirement.

Discussion