New York Times adds 460,000 subscribers in Q3 2025 earnings

Publisher reaches 12.33 million total subscribers with 14% digital subscription revenue growth. Digital advertising surges 20.3% while operating profit climbs 36.6%.

Publisher reaches 12.33 million total subscribers with 14% digital subscription revenue growth. Digital advertising surges 20.3% while operating profit climbs 36.6%.

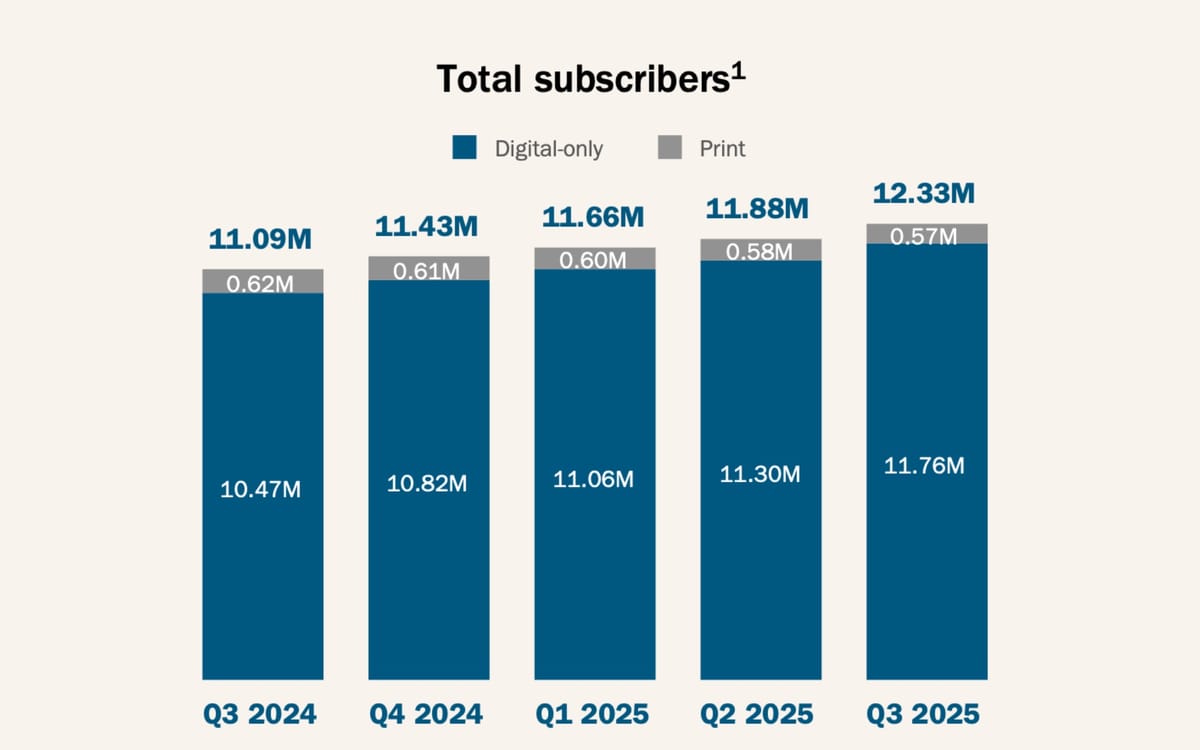

The New York Times Company added approximately 460,000 net digital-only subscribers during the third quarter of 2025, bringing its total subscriber base to 12.33 million, according to financial results announced on November 5, 2025. Digital advertising revenues surged 20.3 percent compared to the same period in 2024, demonstrating the publisher's continued ability to monetize both readership and advertiser demand.

Total digital-only average revenue per user increased 3.6 percent year-over-year to $9.79, driven primarily by subscribers transitioning from promotional pricing to higher rates and price increases implemented for certain tenured subscribers, according to the earnings release. The combination of subscriber growth and ARPU expansion pushed digital-only subscription revenues up 14.0 percent to $367.4 million for the quarter.

Digital advertising revenues reached $98.1 million in the third quarter, marking a 20.3 percent increase from $81.6 million in the same period of 2024. The company attributed this performance to strong marketer demand and new advertising supply, according to chief financial officer Will Bardeen during the November 5 earnings call. Total advertising revenues climbed 11.8 percent to $132.3 million, partially offset by a 7.1 percent decline in print advertising to $34.2 million.

Your go-to source for digital marketing news.

No spam. Unsubscribe anytime.

The subscriber additions came across multiple products in the company's portfolio. Bundle and multiproduct subscribers now comprise 51 percent of the total digital-only subscriber base, reaching approximately 6.27 million. News-only subscribers totaled approximately 1.56 million, while other single-product subscribers reached approximately 3.92 million as of September 30, 2025.

"Q3 was another great quarter across the board at The Times and our results demonstrate that our strategy is working as designed," stated Meredith Kopit Levien, president and chief executive officer, in the earnings release. "We saw strong revenue growth and we are generating significant free cash flow."

Operating profit increased 36.6 percent year-over-year to $104.8 million, while adjusted operating profit climbed 26.1 percent to $131.4 million. Operating profit margin for the quarter reached 15.0 percent, representing a year-over-year increase of approximately 300 basis points. Adjusted operating profit margin expanded to 18.7 percent, up approximately 240 basis points from the prior year period.

Total revenues grew 9.5 percent to $700.8 million in the third quarter. Subscription revenues increased 9.1 percent to $494.6 million, with digital-only products driving growth while print subscription revenues decreased 3.0 percent to $127.2 million. The decline in print subscriptions reflected lower domestic home-delivery and single-copy revenues, according to the company's financial statements.

Affiliate, licensing and other revenues increased 7.9 percent to $73.9 million, primarily driven by higher licensing revenues. Digital affiliate, licensing and other revenues totaled $49.2 million for the quarter, according to footnotes in the company's financial statements.

Operating costs rose 5.8 percent to $596.0 million, with adjusted operating costs increasing 6.2 percent to $569.4 million. Cost of revenue climbed 5.2 percent to $349.1 million, driven mainly by higher journalism costs, subscriber servicing expenses, and advertising servicing costs. Sales and marketing costs jumped 15.1 percent to $79.6 million, while product development costs increased 9.8 percent to $67.0 million.

The company invested heavily in video journalism during the quarter, transforming award-winning podcasts into video shows and introducing a new Watch tab in its flagship Times app. Games product development continued with the launch of Pips, a new logic puzzle. The publisher also expanded its use of artificial intelligence for automated voice features, personalization, targeting, and monetization across customer journeys and advertising products, according to prepared remarks from the earnings call.

Diluted earnings per share reached $0.50 for the quarter, an $0.11 increase year-over-year. Adjusted diluted earnings per share totaled $0.59, up $0.14 from the third quarter of 2024. The company generated $420.3 million in net cash from operating activities during the first nine months of 2025, compared to $258.8 million in the same period of 2024. Free cash flow reached $392.9 million for the nine-month period, up from $237.7 million in the prior year.

Cash and marketable securities totaled $1.1 billion as of September 30, 2025, an increase of $184.9 million from year-end 2024. The company maintained a $400 million unsecured revolving line of credit with no outstanding borrowings as of quarter-end. During the third quarter, the publisher repurchased 482,833 shares of Class A Common Stock for approximately $27.3 million, with approximately $393.0 million remaining authorized for repurchases as of October 31, 2025.

Third-quarter results included $2.4 million in litigation-related costs connected to the company's lawsuit against Microsoft Corporation and OpenAI Inc. alleging unauthorized use of journalism and content for generative artificial intelligence product development. The quarter also included a $3.5 million charge related to impairment of a non-marketable equity investment.

For the fourth quarter of 2025, the company projects digital-only subscription revenues will increase 13 to 16 percent year-over-year, with total subscription revenues expected to grow 8 to 10 percent. Digital advertising revenues are forecast to increase mid-to-high-teens, while total advertising revenues should climb high-single-to-low-double-digits. Affiliate, licensing and other revenues are expected to increase mid-single-digits, with adjusted operating costs projected to rise 6 to 7 percent.

The performance reflects broader trends in digital media monetization, where subscription models combined with diversified advertising revenue streams provide publishers with multiple pathways to financial sustainability. The company's digital advertising growth outpaced many competitors during a period when programmatic advertising platforms reported varied performance across different market segments.

Bundle and multiproduct ARPU reached $12.84 in the third quarter, up from $12.35 in the same period of 2024. News-only ARPU climbed to $12.67 from $11.48 year-over-year, while other single-product ARPU remained relatively stable at $3.51. The variations in ARPU across product categories reflect different pricing strategies and value propositions, similar to patterns observed across social media platforms with diverse monetization approaches.

Buy ads on PPC Land. PPC Land has standard and native ad formats via major DSPs and ad platforms like Google Ads. Via an auction CPM, you can reach industry professionals.

Capital expenditures totaled approximately $8 million in the third quarter, compared to approximately $6 million in the prior year period. For full-year 2025, the company expects capital expenditures of approximately $35 million, depreciation and amortization of approximately $85 million including approximately $28 million of acquired intangible assets amortization, and interest income and other net of approximately $40 million on a pre-tax basis.

The company's advertising performance came despite ongoing industry challenges around measurement and attribution, with digital advertising infrastructure facing scrutiny over targeting accuracy and transparency. The New York Times attributed its advertising strength to a portfolio of compelling products in spaces with broad marketer appeal including sports, games, and shopping, combined with a large engaged audience that marketers can target effectively.

Media expenses, representing costs to promote the subscription business, increased 18.0 percent to $41.3 million from $35.0 million in the third quarter of 2024, primarily driven by higher brand marketing expenses. This investment in subscriber acquisition occurred as the company maintained confidence in its ability to widen the number of people who use and engage deeply with its content across multiple platforms.

Subscribe PPC Land newsletter ✉️ for similar stories like this one

Subscribe PPC Land newsletter ✉️ for similar stories like this one

Who: The New York Times Company (NYSE: NYT), a publicly traded media organization led by president and CEO Meredith Kopit Levien and CFO Will Bardeen, serving more than 12 million subscribers across print and digital products including news, games, sports, cooking, and shopping content.

What: Third-quarter 2025 financial results showing 460,000 net digital-only subscriber additions, 14.0% digital subscription revenue growth to $367.4 million, 20.3% digital advertising revenue increase to $98.1 million, 9.5% total revenue growth to $700.8 million, 36.6% operating profit increase to $104.8 million, and expanded operating margins reaching 15.0%.

When: Results announced November 5, 2025, covering the quarter ended September 30, 2025, with earnings conference call held at 8:00 a.m. Eastern Time that morning and financial guidance provided for fourth quarter 2025 and full-year expectations.

Where: Global operations headquartered in New York with digital products reaching subscribers worldwide, investor communications distributed through company website investors.nytco.com, and services delivered across web platforms, mobile applications, connected television, and traditional print distribution channels.

Why: Results demonstrate successful execution of subscription-first strategy combining world-class journalism with lifestyle products in large addressable markets, multiple revenue stream diversification through advertising and licensing growth, strategic investments in video and AI technology to enhance user engagement, and operational discipline enabling margin expansion while maintaining product development spending across news and emerging formats.