AdRoll: retargeting CPMs jump 18% as display prospecting quietly crumbles

AdRoll's Q1 2026 report reveals retargeting CPMs surged 18% while prospecting dropped 11%, marking a structural budget shift toward CTV and DOOH ad channels.

AdRoll's Q1 2026 report reveals retargeting CPMs surged 18% while prospecting dropped 11%, marking a structural budget shift toward CTV and DOOH ad channels.

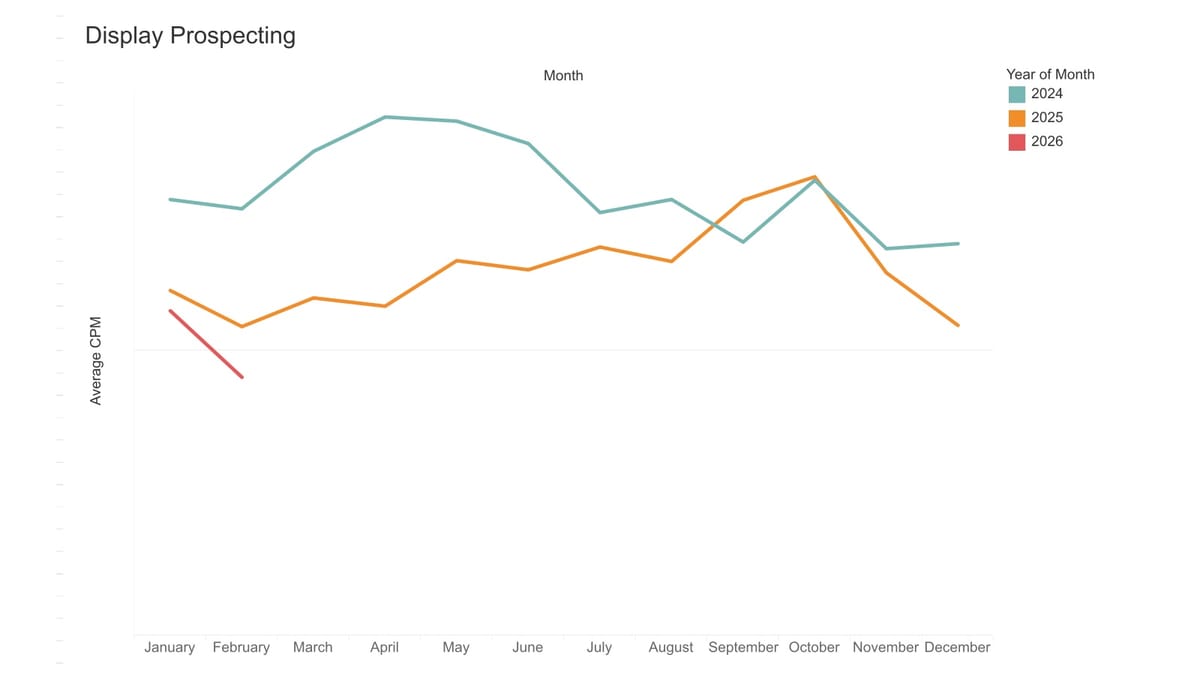

AdRoll today released the Q1 2026 edition of its State of Digital Advertising Report, documenting a deepening split between two segments of display advertising that marketers have long treated as a single category. Display retargeting costs surged 18% in January and February compared with the same period in 2025. Display prospecting CPMs, by contrast, fell 11% over the same interval. The gap between these two figures - wide, and widening - points to a structural reallocation of digital budgets that has been building for several quarters.

The report, published on March 24, 2026, draws on performance data from more than 20,000 online businesses across sectors including finance, beauty and fashion, fitness, technology, and travel. AdRoll, a NextRoll brand, issues the report on a quarterly basis as a barometer of CPM trends in programmatic display.

CPM, or cost per mille, measures the average cost of delivering one thousand ad impressions. It functions similarly to the cost of goods: prices rise when advertiser demand exceeds available publisher supply, and fall when demand softens. The auction-based mechanism that governs most programmatic display buying - handled through supply-side platforms representing publishers and demand-side platforms representing advertisers - makes CPM a sensitive real-time indicator of where marketing budgets are actually flowing.

The 18% retargeting increase recorded in January and February marks an acceleration. Display retargeting CPMs had already surged 11% year-over-year in Q4 2025, driven at that point by an unusually early holiday shopping season and what AdRoll described as K-shaped consumer spending patterns. The Q1 2026 figure arrives without the seasonal tailwind of holiday promotions, suggesting demand for high-intent retargeting inventory has taken on a structural rather than cyclical character.

Prospecting tells the opposite story. The 11% year-over-year decline in January and February extended a downward trend that began in Q4 of last year, when prospecting CPMs had climbed modestly. The reversal indicates that the advertiser appetite for broad web-based awareness campaigns is contracting. Account-based marketing CPMs, measuring the cost of targeting specific high-value business accounts programmatically, fell 8.5% year-over-year during the same period - though the trend has remained relatively stable overall, signaling consistent rather than collapsing demand for B2B programmatic inventory.

The report identifies two interlocking causes behind the divergence, both of which have been developing independently but now reinforce each other.

The first is the collapse of publisher web traffic driven by zero-click search. According to AdRoll's data, zero-click searches - where users receive answers directly within a search results page without visiting any third-party site - now account for more than 60% of Google searches. The rapid adoption of AI answer engines such as ChatGPT is compounding this effect. Publishers have felt the impact acutely. According to Ad Exchange data cited in the report, some publishers saw website traffic decline between 20% and 90% during 2025. PPC Land has documented this erosion extensively, with Ahrefs research showing AI Overviews now correlate with a 58% reduction in click-through rates for top-ranking pages - nearly double the 34.5% decline the same company documented in April 2025.

The consequences for upper-funnel advertising are direct. Prospecting campaigns and brand awareness initiatives require large addressable audience pools spread across many publishers. Fewer site visits mean fewer cookied or identifiable users available in retargeting pools across the open web - and less inventory to bid on for prospecting. The Cloudflare CEO had already warned in May 2025 that content scraping ratios had deteriorated dramatically, with OpenAI systems scraping roughly 1,500 pages per visitor sent to original sources. That dynamic leaves web publishers with diminished traffic and diminished ability to monetize through programmatic display.

Retargeting, by contrast, is less exposed. It relies on comparatively small pools of users who have already visited a brand's own properties - people whose intent is known and whose identity can be matched across devices. Even as the broader publisher ecosystem shrinks, that high-intent segment remains largely intact, and advertisers are competing more fiercely for access to it.

The second structural force is the programmatic transformation of television and out-of-home advertising. Historically, buying time on a television network or space on a billboard required manual negotiations, long-term contracts, and capital that excluded all but the largest brands. As more television screens and outdoor displays become internet-connected, inventory from these environments is increasingly transacted through the same real-time bidding mechanisms used for web display. CTV spending reached over $40 billion in 2025, according to figures cited in a separate AdRoll partnership announcement from October 2025.

AdRoll launched its own CTV product in April 2025. According to the report, advertisers have since expanded beyond traditional web-based channels to include CTV and Digital Out-of-Home (DOOH) in a pattern the company attributes partly to this product introduction. The practical implication is that upper-funnel investment has not evaporated; it has migrated. Programmatic CTV and DOOH offer the large-format, high-impact creative environments historically associated with television and outdoor advertising, while retaining the targeting parameters, performance measurement tools, and budget flexibility that digital advertisers have come to expect.

The Trade Desk's Ventura Ecosystem launch in February 2026 - uniting V's 50 million-device operating system with Nexxen's ad technology in a shared programmatic CTV marketplace - illustrates the speed at which the connected TV supply chain is consolidating. DIRECTV similarly opened its live TV network to programmatic DOOH buying in January 2026, with inventory made accessible through The Trade Desk and Basis among other platforms. JCDecaux, the world's largest outdoor advertising company, reported full-year 2025 results in March 2026 showing DOOH revenue grew 10% organically, with digital screens now accounting for 41.7% of group revenue. Programmatic DOOH revenue through JCDecaux's VIOOH platform reached €180.5 million - real advertiser spend flowing through automated buying infrastructure.

The Q1 2026 report situates its CPM findings against an economic context that is, in the company's framing, relatively stable but not without tension. The U.S. inflation rate has stabilized in the mid-2% range since the government resumed reporting in November 2025, following a gap during which October 2025 data went unpublished due to a government shutdown. Consumer spending held strong in January and February, showing year-over-year growth according to the Bank of America Consumer Checkpoint report. The Consumer Sentiment Index rebounded slightly in January and February but remained significantly below readings from the same period in both 2024 and 2023.

The report explicitly flags the Iran conflict, which began on the last day of February, as a potential disruptive factor whose economic impact is not yet captured in the data. This caveat matters: the CPM figures reflect conditions before that event began to filter through consumer confidence readings or supply chain costs.

The shift toward CTV and DOOH creates genuine technical complications that the report addresses at some length. Different connected-screen environments rely on different targeting frameworks. Traditional web display and social advertising targets individuals on personal devices, using cookies, device identifiers, or first-party data matches. CTV, by contrast, targets households rather than individuals, because streaming devices are typically shared within a home. DOOH targets audiences by geographic proximity to a screen - a fundamentally different unit of analysis from either individual or household.

Reconciling these three targeting paradigms within a single campaign strategy requires marketers to integrate multiple audience datasets. Targeting a customer who first encountered a brand's DOOH creative on a commute, then saw a CTV spot at home, then clicked a retargeting ad on a mobile device - and attributing conversion credit across those touchpoints - is a measurement problem that standard tools were not built to solve.

The report notes that multi-touch attribution (MTA), the conventional method for mapping user journeys across individual touchpoints, becomes less effective precisely for channels like CTV and DOOH, where individual-level tracking may not be possible at all. As a result, marketers are increasingly turning to Marketing Mix Modeling (MMM) and incrementality testing - approaches that rely on statistical modeling and aggregated data rather than deterministic tracking of specific users. Research published by TransUnion and EMARKETER in October 2025 found 46.9% of marketers planned to increase MMM investment over the following 12 months, the highest priority among measurement methodologies. That acceleration is consistent with the scenario AdRoll describes: channels that resist individual-level tracking push advertisers toward aggregate statistical methods.

Separately, the IAB and IAB Europe released an incrementality framework for commerce media in late 2025, providing shared methodology for measuring causal advertising impact. Google reduced its minimum budget for incrementality experiments from thresholds approaching $100,000 to just $5,000 in November 2025, significantly expanding access for smaller advertisers. These developments collectively reflect an industry adapting its measurement infrastructure to environments where the traditional signal - the cookie-tracked individual click - is no longer sufficient.

Vibhor Kapoor, chief executive officer of AdRoll, framed the findings in the company's press release. "The widening gap between retargeting and prospecting costs signals a structural shift in how advertisers build demand," Kapoor said. "Digital advertising is moving beyond the browser and into a multi-screen environment where awareness and performance tactics must work together."

The report recommends that marketers shift from channel-based planning - where separate teams handle display, search, social, and now CTV - toward a full-funnel approach that coordinates messaging across screens. Under this model, a campaign might begin with broad awareness on CTV or DOOH and progress to lower-funnel engagement through retargeting. Executing that kind of sequential cross-screen strategy requires consistent audience data across environments, measurement frameworks capable of spanning individual-level and household-level attribution, and creative assets formatted appropriately for each screen type.

AdRoll has been building toward this integrated model for several quarters. The company unified its brand in August 2025, folding its B2B platform RollWorks into AdRoll ABM and launching an AI Assistant for campaign optimization. In October 2025, 200 brands had activated Experian's syndicated audiences across web and CTV campaigns through AdRoll, accessing more than 3,200 ready-to-use segments. A partnership with Lemonlight, also announced in October 2025, targeted the creative production bottleneck: brands now require three to five times more creative variants than three years ago, and CTV requires video formats that most display-focused teams cannot produce at scale. AdRoll's integration with HUMAN Security in October 2025 added pre-bid fraud detection and viewability measurement across desktop, mobile, in-app, and CTV environments, with invalid traffic detection capable of running within 12 milliseconds of a bid request.

The Q1 2026 report is the fourth consecutive quarterly edition of what was previously called the State of Digital Marketing Report. The Q3 2024 edition had flagged a 47% year-over-year surge in display CPMs, then interpreted as a return to normal after the budget cuts of 2023. The pattern since then - retargeting rising, prospecting falling, CTV expanding - suggests the 2024 recovery was not uniform but rather the beginning of a channel-level bifurcation that has now become visible in the CPM data.

The Q1 2026 findings carry practical implications for budget allocation decisions across marketing teams. A sustained 18% increase in retargeting CPMs, if it persists, raises the cost of reaching bottom-funnel audiences who have already engaged with a brand. Teams that have historically relied on retargeting as a cost-efficient performance driver may find their cost-per-acquisition rising without any change in campaign targeting or creative.

At the same time, the 11% decline in prospecting CPMs presents a buying opportunity - provided the underlying inventory quality has not deteriorated proportionally. If publisher traffic has fallen 20% to 90% for some properties, as the report cites, cheaper prospecting inventory may reflect weaker audience pools rather than genuine bargain pricing. B2B search budget shifts already documented by PPC Land in December 2025 show advertisers redirecting upper-funnel dollars toward paid social, audio, CTV, and DOOH - suggesting that the prospecting CPM decline is being driven partly by demand migrating out of web display entirely rather than simply pulling back.

For marketers currently building their 2026 plans, the structural argument in the AdRoll report is that channel strategy cannot be planned in isolation. CTV targets households; DOOH targets proximity audiences; web display targets individuals. Each channel excels at a different moment in the purchase journey. Coordinating them requires shared taxonomy, consistent audience data, and measurement that spans statistical and deterministic approaches - a standard that most teams have not yet reached. Research from Funnel and Ravn published in December 2025 found that 86% of in-house marketers could not determine the impact of each marketing channel on overall performance, despite unprecedented access to analytics tools.

The 2026 Q1 State of Digital Advertising Report is available at adroll.com/state-of-digital-advertising-report. AdRoll will update the data on a quarterly basis.

Who: AdRoll, a multi-channel advertising platform and NextRoll brand based in San Francisco, released the Q1 2026 edition of its State of Digital Advertising Report. Vibhor Kapoor, chief executive officer of AdRoll, provided analysis. The report analyzes performance data from more than 20,000 online businesses across finance, beauty and fashion, fitness, technology, travel, and other industries.

What: Display retargeting CPMs surged 18% in January and February 2026 compared with the same period in 2025, while display prospecting CPMs fell 11% over the same interval. Account-based marketing CPMs declined 8.5% year-over-year but remained relatively stable in trend terms. The report attributes the divergence to two structural forces: declining publisher web traffic caused by zero-click search and AI answer engines, and the accelerating programmatic availability of CTV and DOOH inventory. AdRoll recommends a shift from channel-based to full-funnel campaign planning.

When: The Q1 2026 State of Digital Advertising Report was released on March 24, 2026. The CPM data covers January and February 2026, compared with the same period in 2025.

Where: The report reflects conditions in the U.S. programmatic display advertising market, drawing on AdRoll's global platform data. Connected TV and DOOH trends have particular relevance to U.S. and international markets where programmatic inventory is expanding rapidly.

Why: The findings matter because they document a measurable reallocation of digital advertising budgets away from web-based upper-funnel campaigns and toward connected-screen environments and lower-funnel performance tactics. Zero-click search is eroding the publisher traffic that makes prospecting display viable at scale, while programmatic infrastructure improvements are lowering the barrier to entry for CTV and DOOH. The CPM data provides marketing teams with a quantitative signal for assessing where competitive pressure and buying opportunity currently sit within the display ecosystem.