Australian retail media spending shows steady growth amid measurement challenges

Brands increase investment in retail networks by 79% while reporting transparency remains industry priority.

Brands increase investment in retail networks by 79% while reporting transparency remains industry priority.

Australian brands and agencies are significantly increasing their retail media investments, with 79% of companies already operating in the space planning to expand their spending, according to IAB Australia's Wave 3 Retail Media State of the Nation research released on July 29, 2025.

The comprehensive study surveyed industry professionals across brands, agencies, and retail media networks, revealing that proximity to point-of-purchase transactions remains the primary driver for retail media investment for the second consecutive year. Point-of-purchase positioning held the top spot in both the previous wave and current research, demonstrating sustained advertiser confidence in commerce-adjacent advertising opportunities.

Subscribe the PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

First-party data access, previously the leading investment driver, dropped to third position after ranking second in the prior year. This shift reflects evolving industry expectations as practitioners gain more experience with retail media platform capabilities and data availability realities.

The research indicates a substantial increase in the number of retail media networks that Australian advertisers are utilizing. Brands are diversifying their partnerships, though the total number of networks remains lower than markets including the United States and Europe, where hundreds of retail media networks operate. Despite this more modest ecosystem compared to international markets, Australian advertisers are demonstrating increased sophistication in their multi-platform strategies.

Investment sources reveal a mixed funding approach, with 19% of respondents reporting access to completely new budgets for retail media activities. Traditional non-digital advertising represents the largest source of reallocated spending, alongside performance marketing budgets and trade spending. The reallocation patterns vary significantly depending on existing client strategies and agency structures.

Supermarkets continue to dominate retailer types used in retail media strategies, maintaining their early-mover advantage in the sector. These grocery retailers established comprehensive first-party data operations and developed substantial media businesses within their organizations. However, the research identifies emerging expansion into different retailer categories and sizes as the commerce media definition continues to evolve.

Platform integration with broader media planning approaches shows encouraging development. Retail media is increasingly considered within holistic marketing strategies rather than in isolation, with advertisers examining its contribution alongside above-the-line activities. This integrated approach represents maturation in how practitioners evaluate retail media performance relative to other channels.

Performance metrics emerged as the top priority when evaluating retail media partners, followed closely by reporting and measurement capabilities. The prominence of reporting and measurement as a key differentiator indicates an industry still developing its infrastructure and transparency standards. According to the research, this emphasis on measurement represents a sign of continued sector development, whereas established advertising channels typically view reporting capabilities as table stakes rather than competitive advantages.

Product preference analysis shows on-site search and sponsored listings maintain their position as the most popular retail media format, with continued growth year-over-year. Off-site extension products are gaining traction as advertisers become more comfortable utilizing retail data to expand reach beyond owned properties. The expanding product array creates diverse opportunities while introducing measurement complexity across different advertising formats including audio and out-of-home placements.

Primary campaign objectives center on bottom-of-funnel performance metrics, contrasting with video and out-of-home advertising where brand metrics typically rank highest. Sales-focused objectives dominate retail media applications, though industry stakeholders express growing interest in measuring brand impact from retail media activities. This performance orientation aligns with retail media's inherent proximity to purchase transactions.

Return on ad spend and incrementality measurement represent the most important performance indicators for evaluating retail media investments. Incrementality analysis has gained particular prominence across the advertising industry, focusing on isolating the specific contribution of individual media investments. The research indicates IAB Australia is developing guidance on incrementality measurement for upcoming publication.

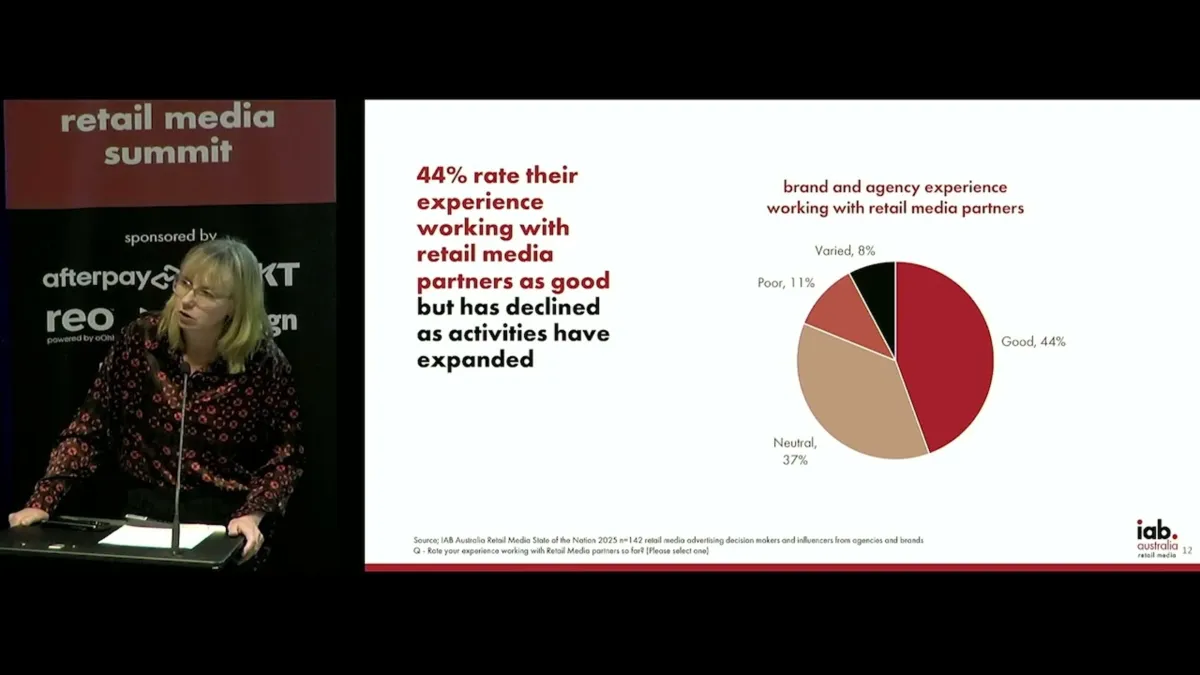

Satisfaction levels with current retail media activities show 44% of respondents rating their experiences as good. The research suggests this moderate satisfaction reflects the challenges of setting appropriate expectations in a rapidly evolving sector. Industry confusion about performance benchmarks and comparison standards contributes to uncertainty about what constitutes successful retail media outcomes.

Further investment drivers focus heavily on measurement and reporting improvements, with both agency and brand stakeholders prioritizing operational efficiency. Agency-side responses emphasize smooth client relationship management, while brand-side priorities center on demonstrating clear value from retail media spending. This alignment between buy-side needs and sell-side development priorities suggests potential for addressing current industry challenges.

Retailer development plans show measurement offering enhancements as the top priority, creating alignment between advertiser demands and supplier roadmaps. Product offering expansion ranks as another key retailer focus, indicating continued investment in platform capabilities and advertising format diversity.

Privacy considerations remain top-of-mind as regulatory frameworks continue evolving. Organizations with established first-party data strategies maintain advantages due to their existing focus on customer data relationships and governance. However, potential additional privacy regulations may impact retailer partnerships and data utilization practices, particularly concerning data sharing arrangements.

Budget sources demonstrate mixed funding approaches with traditional advertising spend, performance marketing budgets, and trade spending all contributing to retail media investment. The 19% of respondents reporting entirely new budgets may reflect agency involvement in expanding client retail media access or represent genuine budget increases in recognition of retail media's strategic value.

Industry standardization efforts focus on measurement alignment, performance outcome definitions, and language harmonization across traditionally separate retail, trade, and media stakeholder groups. Transparency in data usage and consumer governance represents another priority as the industry demonstrates responsible data stewardship to maintain consumer trust.

The research emphasizes the continued need for case studies and best practice sharing to advance industry knowledge. Practitioners consistently request examples of successful implementations and lessons learned from both effective and unsuccessful retail media campaigns.

According to the research findings, Australian retail media maintains healthy growth trajectory characteristics. Retailers are actively advancing their platform offerings while point-of-purchase proximity remains the primary strategic advantage. Integration with complete media and marketing perspectives is increasing, though sales objectives continue dominating campaign goals over brand-focused metrics.

The study concludes that industry development requirements mirror established advertising sector playbooks: measurement standardization, performance outcome alignment, transparency enhancement, education initiatives, and language harmonization. Clear data usage guidelines and governance frameworks will support consumer trust and regulatory compliance as the sector continues expanding.

Subscribe the PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Subscribe the PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Who: IAB Australia conducted research surveying brands, agencies, and retail media networks across Australian markets to assess retail media adoption and investment patterns.

What: Wave 3 Retail Media State of the Nation research revealing 79% of existing retail media advertisers plan to increase spending, with point-of-purchase proximity maintaining its position as the primary investment driver while measurement challenges persist industry-wide.

When: The research findings were announced on July 29, 2025, representing the third wave of IAB Australia's ongoing retail media industry assessment.

Where: The study focused on Australian retail media markets, examining advertiser behavior across supermarket-dominated networks and emerging retailer categories while comparing adoption patterns to more developed international markets.

Why: The research addresses industry needs for benchmarking retail media maturation, understanding investment sources and barriers, measuring ecosystem development, and identifying growth opportunities as the sector transitions from experimental tactics to strategic advertising infrastructure.