Credit cards now dominate as shoppers plan record holiday spending

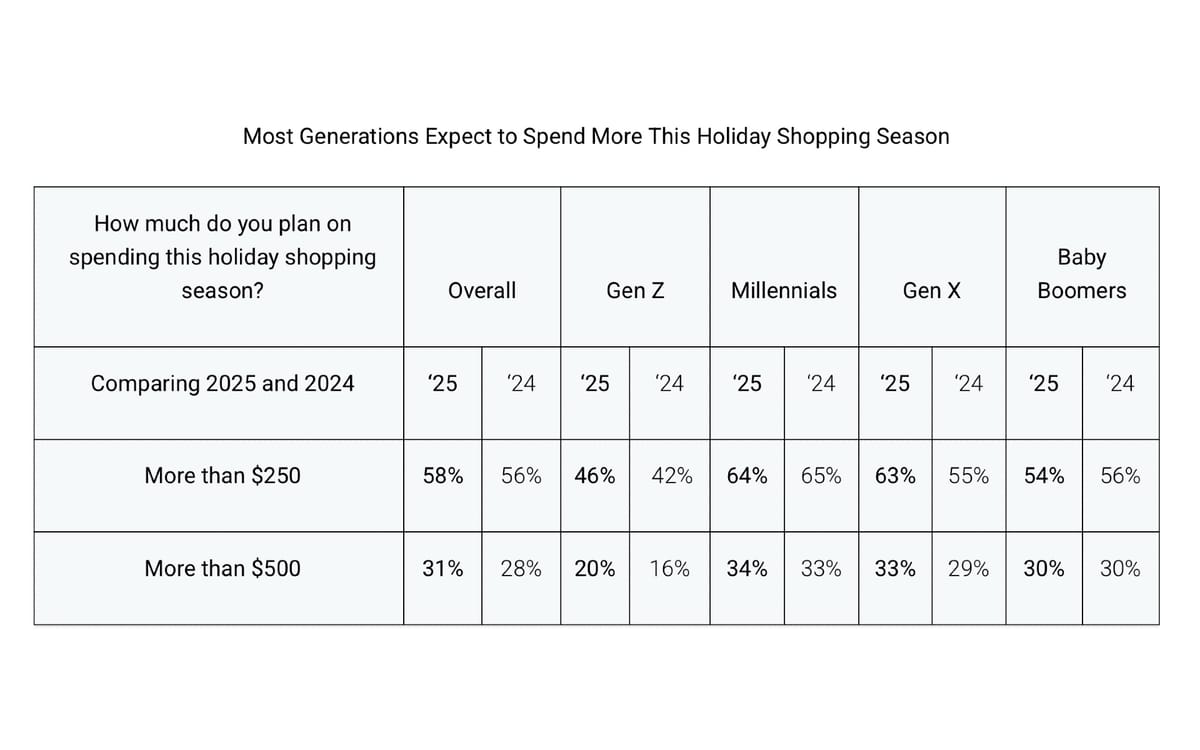

TransUnion Q4 2025 study shows 42% of Americans will rely on credit cards for holiday purchases, up from 38% last year, as 58% plan to spend over $250 despite inflation.

TransUnion Q4 2025 study shows 42% of Americans will rely on credit cards for holiday purchases, up from 38% last year, as 58% plan to spend over $250 despite inflation.

Consumers are turning to credit cards at accelerated rates this holiday season as financial pressures reshape purchasing behavior across the United States. According to TransUnion's Q4 2025 Consumer Pulse Study released on November 20, 2025, 42% of Americans expect to rely on credit cards as their preferred payment method during the holidays, representing a four-percentage-point increase from 38% in 2024.

The study, conducted between October 1 and October 14, 2025, surveyed 3,000 adults and revealed persistent economic anxiety despite strong spending intentions. Nearly six in 10 consumers (58%) expect to spend more than $250 this holiday season, up two percentage points from 56% last year. The findings arrive as retailers prepare for their most critical revenue period amid ongoing concerns about inflation and international trade tariffs.

Subscribe PPC Land newsletter ✉️ for similar stories like this one

Charlie Wise, senior vice president and head of global research and consulting at TransUnion, stated: "As the holiday shopping season kicks off in earnest next weekend, our latest Consumer Pulse study suggests we may see increased spending this year. It's clear that credit cards will be the preferred payment method for many consumers."

The credit card preference marks a significant behavioral shift. Nearly 175 million Americans now hold one or more active credit cards, according to TransUnion, representing steady growth in both cardholders and open accounts. The increase in planned credit card usage coincides with expectations for overall spending levels to remain near record highs, with 31% of consumers planning to spend over $500 compared to 28% in 2024.

Shopping behavior follows traditional patterns despite earlier promotional pushes by retailers. The highest percentage of consumers (41%) plan to shop online between Thanksgiving and Cyber Monday, while 33% intend to shop in person during the Thanksgiving weekend. These figures suggest promotional events during the traditional holiday kickoff period retain their influence on purchase timing.

Overall consumer optimism about household finances declined three percentage points year-over-year. The study found 55% of Americans remain optimistic about their financial situation over the next 12 months, down from 58% in Q4 2024. This represents a continuation of range-bound sentiment that has fluctuated between 54% and 58% since Q1 2023, with a single peak of 60% in Q3 2024.

The decline correlates with moderating income expectations. Just 48% of consumers expect their income to increase in the next year, down from 53% a year ago, while 43% expect income to stay the same, up from 40% in 2024. Despite large corporate layoffs and the federal government shutdown that began October 1, 2025, during the survey period, only 35% cited jobs among their top three financial concerns.

Younger generations maintain significantly higher optimism levels. Gen Z (63%) and Millennials (65%) expressed positive outlooks about their finances, compared to Gen X (50%) and Baby Boomers (45%). High-income households earning $100,000 or more annually reported 63% optimism, though this represents a five-percentage-point decline from the previous year—the largest decrease among all income groups.

"We continue to see a resilient consumer, even as optimism has declined from its peak in recent years," Wise added. "Uncertainty around tariffs and the timing of our research—conducted at the onset of the federal government shutdown—may be contributing factors."

The study revealed stark polarization across income levels regarding financial health. Among households earning $100,000 or more annually, 79% reported their finances were better than or as planned, compared to just 51% of lower-income households earning less than $50,000 annually. Inflation emerged as the key factor driving this divide: 77% of those whose finances were worse than planned reported their incomes were not keeping up with inflation, compared to just 13% of those whose finances were better than expected.

Inflation remains the overwhelming financial concern for American consumers, with 81% citing it among their top three worries affecting household finances over the next six months. This figure holds steady with 80% in Q4 2024. Recession ranks as the second most common concern at 52%, followed by housing prices at 43%.

Groceries (79%) maintained their position as the price increase most concerning to consumers, essentially unchanged from 80% a year ago. Insurance concerns increased from 43% in Q4 2024 to 47% in Q4 2025, while medical care concerns rose from 41% to 45% over the same period.

Tariff anxiety weighs heavily on consumer sentiment. The study found 86% of respondents reported at least some level of concern over the impact of international trade tariffs on their household finances, with 34% saying they are very concerned. This represents a slight increase from 85% in Q3 2025.

High-income households demonstrated greater resilience to inflation pressures. Among households earning $100,000 or more annually, 45% said their incomes kept up with inflation, compared to just 26% of households earning less than $50,000 and 36% of middle-income households earning between $50,000 and $99,999.

Buy ads on PPC Land. PPC Land has standard and native ad formats via major DSPs and ad platforms like Google Ads. Via an auction CPM, you can reach industry professionals.

Personal consumption expenditure rose 0.6% in August 2025, according to the Bureau of Economic Analysis cited in the study. This growth occurred despite persistent economic uncertainty, demonstrating continued consumer resilience. High-income households planned to maintain or increase spending across multiple categories in the next three months: medical services (89%), digital services (83%), retail items like clothing and electronics (69%), discretionary items including dining out and travel (63%), and large purchases like appliances and cars (56%).

Plans to seek new credit or refinance existing credit declined to 30% in Q4 2025, down from 33% in Q3 2025 and 31% a year ago. Demand remained particularly strong among younger generations, with Gen Z (44%) and Millennials (46%) expressing significantly higher intentions to apply for credit compared to Gen X (27%) and Baby Boomers (12%).

Among those planning to apply for credit in the coming year, new credit cards remained the top priority at 55%, unchanged from previous quarters. The fourth most common credit action was increasing available credit on existing credit cards (20%), aligning with the broader trend of consumers using credit cards to manage holiday budgets.

The fastest growing credit action was applying for a new auto loan or lease, with 23% of credit seekers planning this move, up from 19% in Q3 2025. New personal loans (21%), mortgage refinancing (14%), and new home equity lines of credit (12%) rounded out the top credit products consumers planned to pursue.

Two-thirds (66%) of consumers reported having sufficient access to credit and lending products, while 68% said they would be approved if they needed new credit. These figures suggest overall confidence in credit availability despite tightening credit conditions in some segments. Most consumers (88%) consider access to credit important for achieving financial goals, though this varies by generation, with Gen Z (95%) and Millennials (96%) valuing credit access more than Baby Boomers (76%).

Credit history (33%) and income or employment status (29%) emerged as the leading reasons consumers abandoned plans to apply for new credit or refinancing. Cost concerns (24%) and uncertainty about whether changes would sufficiently improve payment situations (24%) also factored heavily in decisions to abandon credit applications.

Margaret Poe, head of consumer credit education at TransUnion, stated: "Building a foundation of sound financial and credit habits and practicing them consistently are the keys to long-term credit health. Consumers who regularly monitor their credit are well on their way to putting themselves in a better position to prepare for today's credit market."

The study found 95% of Americans believe monitoring their credit reports is important, with 60% considering it extremely or very important. Despite this widespread recognition, actual monitoring behavior shows significant variation. Just 54% of consumers reported checking their credit at least monthly, while 11% claimed they never monitor their credit at all.

Younger generations demonstrated the most active credit monitoring habits. Gen Z (65%) and Millennials (64%) reported checking their credit at least monthly, significantly higher than Gen X (54%) and Baby Boomers (45%). Daily monitoring remained relatively rare at just 6% of consumers, while weekly monitoring captured 18% and monthly monitoring 30%.

Among consumers who monitor their credit reports, the top motivations included protecting against fraud (46%), monitoring for accuracy (44%), and improving credit scores (32%). The free nature of credit monitoring services influenced 47% of users, making it the single most cited reason for checking credit reports.

TransUnion launched Credit Essentials earlier in 2025, providing free access to daily credit reports and scores, personalized credit offers, and educational materials. The platform offers alerts about significant changes to credit reports, including late payments, new accounts, and hard inquiries, as well as notifications about credit score shifts.

The service arrives as consumers demonstrate strong interest in understanding their credit standing before opening new accounts. Of the 30% planning to apply for new credit within the next year, 55% intend to seek new credit cards—making pre-application credit checking particularly relevant for this group.

Consumers recognize that alternative data sources could affect their credit scores. When asked how their credit scores would change if businesses used information not on standard credit reports—such as rental payments, short-term loan history, and buy now, pay later loans—45% believed their scores would increase, while 35% thought scores would remain the same and 14% expected decreases.

In Q4 2025, 42% of consumers reported being targeted with email, online, phone call, or text messaging fraud schemes but did not fall victim, representing a three-percentage-point increase from Q4 2024. Another 7% said they were targeted and fell victim, down from 9% a year ago. Just 51% of consumers reported being unaware of any fraud schemes targeting them.

Phishing emerged as the most frequently reported fraud scheme, with 46% of those targeted experiencing fraudulent emails, websites, social posts, or QR codes designed to steal data. Smishing—fraudulent text messages meant to trick recipients into revealing data—affected 45% of fraud targets, while vishing, fraudulent phone calls seeking sensitive information, reached 34%.

Generational differences in fraud exposure were pronounced. Among Gen X and Baby Boomers, 51% reported experiencing phishing attempts, compared to just 30% of Gen Z and 43% of Millennials. This pattern suggests older consumers face higher targeting rates for these traditional fraud-enabling scams, or demonstrate greater awareness of attempted fraud.

Following data breach notifications, consumer response proved inadequate to prevent potential fraud. Among the 30% of Americans notified that details about their identities or online accounts were stolen in the last three months, less than half (46%) checked affected accounts for unauthorized activity and just 41% changed passwords on affected accounts.

Proactive security measures remained limited. Around one-third of data breach victims changed passwords on unaffected accounts (34%) or checked credit reports for unauthorized trades (36%). Just 27% signed up for credit or identity monitoring services, 25% placed freezes on credit, and 18% closed affected accounts.

Broader cybersecurity behaviors showed similar gaps between concern and action. Just over a quarter (27%) of consumers took no action in the last 60 days due to cybersecurity concerns. Among those who did take action, changing passwords (47%) and checking credit reports (44%) were most common—both up two percentage points from 2024. However, only 22% added more secure login options, 13% enrolled in identity monitoring, and 12% initiated credit freezes or purchased identity theft protection.

Among those who took no cybersecurity actions, 49% said they were unsure what steps to take, 17% chose not to invest money in protection, 16% felt overwhelmed by the options, and 15% chose not to invest time in security measures.

More than half (52%) of consumers cut back on discretionary spending like dining out, travel, and entertainment in the last three months, while 30% canceled subscriptions or memberships. These cuts affected all generations, with Baby Boomers (52%), Gen X (56%), and Millennials (52%) reducing discretionary spending at similar rates. Gen Z showed slightly lower reduction rates at 50%.

Digital service changes reflected mixed behavior. While 20% overall canceled or reduced digital services, 11% added or expanded such services, suggesting consumers prioritize different digital offerings based on value perception. Gen Z (19%) and Millennials (18%) were most likely to add new digital services despite economic pressures.

Debt and savings behaviors showed cautious optimism. Nearly a quarter (24%) saved more in emergency funds, while 22% paid down debt faster. However, 17% increased usage of available credit, and 16% saved more for retirement. Just 15% cut back on retirement savings, while 13% used retirement savings to cover current expenses.

Looking ahead three months, consumers planned mixed spending changes across categories. For bills and loans, 40% expected to maintain current spending levels, 45% anticipated keeping spending the same, and 11% planned decreases. Digital services showed 53% expecting stable spending, 25% planning increases, and 18% anticipating cuts.

Discretionary spending plans revealed cautious consumers: 44% expected to decrease such spending, 32% planned to maintain current levels, and 21% intended to increase spending on dining out, travel, and entertainment. Large purchases like appliances and cars showed 35% planning decreases, 31% expecting stable spending, and 18% intending increases.

Medical care and services demonstrated the strongest spending resilience, with 54% planning to maintain current levels, 28% expecting increases, and just 11% anticipating cuts. This pattern reflects the non-discretionary nature of healthcare expenses despite financial pressures.

The TransUnion findings arrived as holiday spending forecasts indicated consumers would spend $890.49 per person, representing the second-highest amount in 23 years of tracking by the National Retail Federation. The correlation between credit card usage intentions and overall spending patterns suggests consumers maintain purchasing power through strategic use of available credit.

Generational divides in financial optimism and spending behavior present distinct opportunities for marketers. Younger consumers drove higher financial optimism and holiday spending intentions despite economic uncertainty, with Millennials and Gen Z demonstrating greater willingness to maintain or increase spending compared to older generations who exercised more caution.

The concentration of shopping activity during specific periods requires coordinated planning across advertising channels. November retail sales rose 4.53% year-over-year, establishing baseline expectations for December performance. The 41% of consumers planning to shop online during Thanksgiving through Cyber Monday, combined with 33% shopping in person during Thanksgiving weekend, demonstrates the continued importance of traditional promotional periods.

Economic concerns affect marketing strategy beyond simple budget allocation. Tariff concerns pushed 34% of shoppers to start holiday buying early, reshaping promotional timing and messaging approaches. The 86% of consumers concerned about tariff impacts requires careful communication about value propositions without explicitly referencing economic pressures.

Polarization across income levels where high-income households at 79% reported better financial positions compared to just 51% of lower-income households requires precision targeting. Retail media networks continue expanding their capabilities to enable sophisticated audience segmentation based on purchase history and financial behaviors, making it possible to deploy targeted approaches meeting consumers at different economic positions.

The fraud and security findings suggest opportunities for financial services marketers to address growing consumer concerns about identity protection. With 49% of fraud targets experiencing phishing attempts and only 54% monitoring credit monthly, educational campaigns about security best practices could build brand trust while addressing genuine consumer needs.

Subscribe PPC Land newsletter ✉️ for similar stories like this one

Subscribe PPC Land newsletter ✉️ for similar stories like this one

Who: TransUnion, a global information and insights company with over 13,000 associates operating in more than 30 countries, conducted the research in partnership with third-party research provider Dynata. The study surveyed 3,000 U.S. adults aged 18 and older across all 50 states, with quotas balancing responses to census statistics on age, gender, household income, race, and region.

What: The Q4 2025 Consumer Pulse Study revealed 42% of Americans plan to rely on credit cards for holiday purchases (up from 38% last year), 58% expect to spend over $250 during holidays (up from 56% last year), 55% remain optimistic about household finances in the next 12 months (down from 58% last year), 48% expect income to increase in the next year (down from 53% last year), and 86% express concern about tariff impacts on household finances.

When: The online survey was conducted October 1-14, 2025, spanning the first two weeks of the U.S. government shutdown. TransUnion released results on November 20, 2025, ahead of the Thanksgiving weekend (November 28-30) and Cyber Monday (December 1) that traditionally mark the start of peak holiday shopping. The findings cover consumer attitudes about current financial conditions and expectations for the next 3-12 months.

Where: The research covered United States resident demographics with representation from all 50 states, examining consumer attitudes and behaviors about household budgets, spending, debt, credit access, fraud protection, and identity monitoring across income levels ($50,000 or less, $50,000-$99,999, $100,000 or more), generational cohorts (Gen Z 18-28, Millennials 29-44, Gen X 45-60, Baby Boomers 61+), and geographic regions.

Why: The study matters for marketing professionals because it demonstrates fundamental shifts in consumer payment preferences driven by financial pressures, with credit card usage accelerating as the preferred holiday payment method. The data reveals polarization across income levels affecting purchasing power and spending intentions, generational differences in financial optimism requiring targeted messaging approaches, persistent inflation and tariff concerns weighing on 81% and 86% of consumers respectively, and gaps between fraud awareness and protective action creating opportunities for financial services marketing. The concentration of 41% of shopping during Thanksgiving through Cyber Monday, combined with 58% planning to spend over $250, makes fourth-quarter advertising effectiveness critical for annual revenue targets across retail and financial services sectors.