European broadcasters face mounting streaming competition

BCG survey shows streaming platforms reach 97% of European viewers, claiming 64% of viewing time as broadcasters struggle with eroding market share.

BCG survey shows streaming platforms reach 97% of European viewers, claiming 64% of viewing time as broadcasters struggle with eroding market share.

A comprehensive survey released on September 16, 2025, reveals streaming platforms have captured 97% of European viewers and account for 64% of weekly viewing time across the UK, France, Germany, and Switzerland. The census-balanced study by Boston Consulting Group and NativeResearch polled 3,500 consumers, documenting how global platforms now dominate four of the top five positions in audiences' streaming preferences.

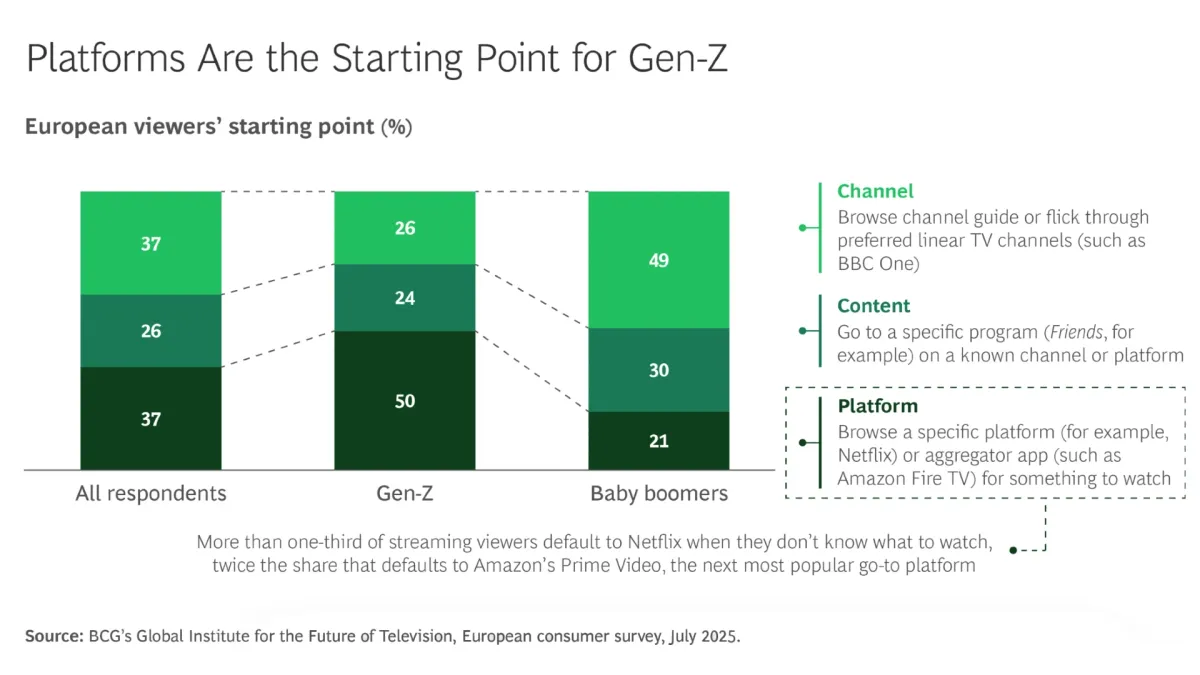

The research demonstrates digital streaming and social video platforms have fundamentally altered viewing patterns. Gen-Z viewers allocate just 16% of their viewing time to linear television, contrasting sharply with baby boomers who dedicate 55% of their time to traditional broadcasts. Algorithmic recommendations have replaced channel surfing as the primary content discovery method for younger audiences—half of Gen-Z viewers begin their viewing experience by browsing streaming platform recommendations.

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Most European consumers maintain four or five streaming subscriptions, with global services claiming at least three slots in every surveyed market. National broadcasters compete for only one or two remaining positions. Global platforms leverage vast content libraries and substantial resources to produce high-profile programming, creating an increasingly unbalanced competitive environment.

YouTube and social video platforms drive additional disruption, collectively representing approximately 20% of total viewing time—exceeding 40% among Gen-Z audiences. YouTube reaches more viewers than Netflix by 10 percentage points within the youngest demographic. The platform's evolution extends beyond user-generated content to encompass live streams, podcasts, and professionally produced programming. One-third of YouTube users now watch television shows or movies through the service, rising to 38% for Gen-Z viewers.

UK broadcasters have responded by developing collaborative advertising solutions, demonstrating adaptation to streaming environments. The viewing shift from television screens to connected devices represents more than format preference—it signals fundamental changes in content consumption patterns and advertising opportunities.

Buy ads on PPC Land. PPC Land has standard and native ad formats via major DSPs and ad platforms like Google Ads. Via an auction CPM, you can reach industry professionals.

In the UK, 41% of YouTube's in-home viewing occurred on television sets during 2024, increasing from 34% the previous year. TikTok and Instagram are developing television-set applications to replicate YouTube's success, expanding competition for living room screens traditionally dominated by broadcasters.

Short-form video platforms introduce different engagement dynamics. Consumers—particularly Gen-Z viewers—report finding short-form content more enjoyable than traditional television programming. The majority of young audiences indicate short-form platforms simplify content discovery compared to conventional services. While 83% of viewers notice advertisements on short-form platforms, only 39% consider ads detrimental to their experience. Baby boomers express more criticism, with nearly half reporting ads negatively impact viewing, contrasting with Gen-Z's relative tolerance.

Spending on streaming services approaches saturation. European households maintain one or two fewer streaming subscriptions than American counterparts, with most consumers reporting proximity to their intended spending limits. This pressure has accelerated hybrid monetization models, combining ad-free and ad-supported options across varied price points.

Streaming platforms have intensified their focus on advertising revenue as subscription growth moderates. Amazon's Prime Video maintains the highest proportion of subscribers on ad-supported tiers. Netflix and Prime Video consistently rank among top platforms for advertisements viewers describe as entertaining and relevant—a critical perception in an increasingly ad-supported marketplace. The Disney+ and Amazon advertising partnership signals broader industry consolidation of advertising capabilities and reach.

Platforms experiment with diverse ad formats extending beyond traditional preroll and midroll positions. Pause ads, interactive overlays, product placements, and shoppable videos represent methods to maximize revenue while minimizing viewer disruptions. Streamers negotiate global advertising deals with agencies and brands, leveraging international scale unavailable to national broadcasters.

European adoption of free ad-supported streaming television (FAST) and fully ad-supported video on demand (AVOD) platforms trails the US by up to 40 percentage points—partially because free-to-air broadcasters fulfill similar roles. Growing awareness and improved local content could drive European viewer adoption closer to American levels, enabling ad-supported platforms to capture larger television advertising shares.

Despite numerous alternatives, 71% of consumers consider national broadcasters relevant—a perspective consistent across regions and generations. Approximately 70% of viewers believe broadcasters fulfill vital roles creating and distributing locally relevant content, including news and live sports. Yet positive sentiment hasn't fully transferred to broadcaster video-on-demand (BVOD) services. While BVOD platforms gain momentum, some remain perceived as catch-up services, continuing to lag global streamers in awareness and reach.

Joyn, the German streaming platform owned by ProSiebenSat.1 Media, reported record quarterly performance with average monthly users increasing 31% year-on-year and viewing time rising 26%. Despite these gains, Joyn ranks outside Germany's top five by user share. France's TF1+ and UK-based ITVX demonstrate rapid growth since launching but, like Joyn, maintain distance from global competitors.

Global streamers steadily expand local content production. The survey data indicates global platforms' share of UK creative and entertainment revenue approximately doubled from 22% in 2014 to 42% in 2024. While this expansion brings UK content to international audiences, it reduces domestic broadcaster market share, potentially limiting reinvestment in local programming. Broadcasters serving smaller, non-English markets face sharper challenges—limited global reach constrains potential returns on content investment.

Sports rights remain contested territory. Streamers collectively project spending exceeding $12 billion on rights during 2025. These acquisitions impact free-to-air and pay-TV broadcasters, eroding traditional positions as primary destinations for major sports competitions in local markets.

Revenue pressures affect all broadcasters, though public entities funded by household license fees face particular exposure. Public sentiment toward broadcasters remains positive, yet opinions about license fees vary—net negative in Germany, more balanced in the UK and Switzerland. In the digital era, license fee funding models encounter increasing challenges, raising questions about public broadcasters' long-term sustainability absent reforms. Younger viewers, despite consuming less public broadcasting, tend to support license fees more strongly—possibly reflecting familiarity with paying for digital content.

The BCG report outlines six strategic imperatives for broadcasters: leveraging national roots, pursuing scale through partnerships and mergers, expanding distribution across digital and social platforms, diversifying revenue sources, embracing artificial intelligence, and partnering with regulators to modernize market rules.

National roots represent broadcasters' sharpest advantage. Deep understanding of local audiences, cultural connections, and relationships with regionally relevant advertisers enable competition where global scale proves insufficient. This requires strategic investment in genres and viewing moments where broadcasters can establish platform dominance while building export potential. Rather than spreading resources through incremental cuts, broadcasters must make decisive choices about concentration and reduction areas.

Scale through aggregation, partnerships, and consolidation can help level the playing field against global competitors. The survey shows 57% of viewers believe too many streaming services exist, with over 60% supporting broadcaster consolidation to better challenge global players. Recent regulatory shifts demonstrate changing momentum—the approved RTL Nederland sale to DPG Media reflects more pragmatic approaches enabling public broadcasters to pool resources while maintaining public service missions. The MediaForEurope takeover of ProSiebenSat.1 predicated on building regional advertising scale and sharing technology costs exemplifies consolidation strategies.

Broadcasters should explore partnerships to scale digital reach, advertising sales, and technology. Freely, a UK public broadcaster joint venture improving free-television distribution, demonstrates collaborative approaches. Channel 4, ITV, and Sky's planned self-service advertising marketplace for small and medium businesses represents another partnership model, simplifying campaign purchases across UK commercial broadcasters.

Distribution expansion requires meeting audiences across platforms. Broadcasters typically reach approximately two-thirds of viewers in home markets. Among missed audiences, over 90% actively use global streaming platforms or YouTube. Marketing approaches must evolve beyond broadcaster-owned channels and isolated clips, designing seamless journeys attracting viewers from TikTok, Instagram, and other platforms. This combines organic content with paid campaigns, creator collaborations, and sustained community building.

Content and distribution partnerships extend reach. Agreements between TF1 and Netflix, France TV and Amazon's Prime Video, and ITV, ZDF with Disney+ demonstrate collaboration potential for audience growth. Without safeguards, broadcasters risk losing control over content, viewer relationships, data, and personalization capabilities. Strategies must balance global platform reach with long-term independence and competitive positioning.

Revenue diversification addresses monetization challenges as traditional models face pressure. Older generations favor free, ad-supported viewing while younger audiences accept payment. Global streaming platforms have scaled ad-supported tiers and deepened engagement, yet broadcasters struggle building robust subscription businesses—majority content often remains available free via broadcast.

Matching global streamers' content output proves unrealistic, but broadcasters can strengthen revenues through ad-free subscription plans bundled with services or tied to exclusive content featuring star talent and franchises. Alternative pay-per-view models could prove effective—TF1 recently announced micropayment plans on its BVOD platform, enabling viewers to avoid advertising on specific programs for under $1.

Generative AI offers broadcasters opportunities for end-to-end transformation. Where personalization and recommendation engines previously required vast resources and global scale, large language models now enable tailored experiences at reduced costs. Most broadcasters pilot GenAI initiatives, typically focusing on individual projects. Connected implementations deliver meaningful results—RTL's GenAI agent generating marketing assets and ITV's experiments with AI-driven ad production illustrate potential when efforts achieve scale and integration.

Responsible AI adoption requires transparency in AI-generated content creation and labeling, intellectual property safeguards, data privacy protection, and bias avoidance in personalization or recommendations. Broadcasters must balance innovation with editorial integrity—using GenAI to enhance creativity and efficiency without compromising truth, fairness, or human connections defining their societal role.

Many European media regulations originated when broadcasters dominated home viewing. Current frameworks can disadvantage them—rules governing advertising, content guidelines, or watershed protections apply unevenly or not at all to global platforms. Broadcasters can collaborate with regulators refreshing rules for on-demand environments. Minimally, broadcasters and global platforms should face equivalent oversight, adapted to different distribution and business models.

Ensuring public broadcaster content discoverability requires acceleration if governments want culturally relevant content production to continue. Rules could extend beyond smart televisions and aggregation applications to include discovery on video-on-demand and social media platforms where audience attention now concentrates.

The report emphasizes challenges facing European broadcasters remain substantial, yet these institutions retain viewer trust and positioning to provide distinct local perspectives, cultural context, and editorial integrity potentially lacking from global platforms. Maintaining prominence requires overcoming regulatory barriers and market complexities that have slowed action—beginning to move at speeds matching global competitors.

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Who: European broadcasters in the UK, France, Germany, and Switzerland; 3,500 surveyed consumers; global streaming platforms including Netflix, Amazon Prime Video, Disney+, and YouTube; Boston Consulting Group and NativeResearch researchers.

What: A census-balanced survey documenting streaming platforms' dominance in European markets, capturing 97% of viewers and 64% of viewing time. The research details shifting consumption patterns, advertising competition, and strategic imperatives for broadcasters facing erosion of traditional market positions.

When: Survey results published September 16, 2025, analyzing current viewing patterns and documenting changes from 2014 to 2024, with projections extending to 2029 when streaming revenue is forecast to overtake linear television in the United States.

Where: United Kingdom, France, Germany, and Switzerland—four major European markets where traditional broadcasters historically dominated home viewing but now face substantial competition from global streaming platforms and social video services.

Why: The research matters for marketing professionals because it quantifies fundamental shifts in audience behavior, advertising opportunities, and media consumption patterns. Understanding these dynamics proves essential for budget allocation decisions, platform selection, and strategic planning as advertising spending migrates from linear television to streaming platforms. The findings demonstrate how cultural content production, local programming investment, and advertising effectiveness increasingly depend on broadcasters' ability to adapt to streaming-dominant environments.