SparkToro and Datos yesterday published a landmark study examining where desktop search actually happens across the internet - and the results challenge some of the most widely repeated assumptions in the marketing industry. Published on March 2, 2026 by Rand Fishkin, the research analyzed 41 domains spanningtraditional search engines, e-commerce platforms, social networks, AI tools, and other major verticals, using Datos' panel of millions of desktop devices across the United States and 27 EU member countries plus the United Kingdom throughout all four quarters of 2025.

The headline figure is striking. According to the report, Google alone was responsible for 73.7% of all desktop searches across the 41 domains analyzed in the US in Q4 2025. That number is lower than the 90%+ share Google is typically assigned by methodologies such as Statcounter - which only count traditional search engines - but substantially higher than figures Google has tried to use in its antitrust defense. The gap matters enormously for how marketers allocate budget and attention.

What the data actually covers

The methodology here is the most expansive of its kind. Datos' 2025 desktop panel covers millions of devices in the United States, the 27 EU member states, and the United Kingdom, broken down by month and quarter. The 41 domains were selected editorially by Fishkin from the most visited 250 domains in Datos' panel, narrowed to those with relevant search behavior. Instagram was included; USPS.com was not. The study explicitly excludes adult content sites and domains where search activity exists but was deemed not sufficiently relevant. Mobile browsers and apps were not included, which the researchers flag as a significant caveat.

All searches and prompt sessions were treated equally. According to the report, "AI prompt sessions with multiple back-and-forths were counted as a single 'search' just as Google searches with dozens of clicks were treated the same as those with zero clicks." That methodological choice compresses some of ChatGPT's relative importance - long multi-turn research sessions count as a single unit, just like a two-second Google lookup.

The 41 domains were further grouped into five top-level categories: traditional search engines (Google, Yahoo, Bing, Yandex, DuckDuckGo, AOL, Baidu), commerce platforms (Amazon, Walmart, eBay, Etsy, HomeDepot, AliExpress, Temu, Booking, AirBnB), social networks (YouTube, Reddit, Facebook, Instagram, Twitter/X, TikTok, LinkedIn, Pinterest, Threads, Tumblr, DeviantArt, Snapchat, Bluesky), AI tools (ChatGPT, Claude, Deepseek), and other verticals(Wikipedia, Apple, Steam, IMDB, NYTimes, Twitch, Indeed, Archive.org, Patreon, Craigslist).

When expressed as a share of all desktop search activity across those five categories, the picture is clear. According to the report, approximately 80% of searches still occur on traditional search engines. Commerce platforms account for roughly 10%. Social networks come third at approximately 5.5%. And AI tools represent only 3.2%.

That 3.2% figure for AI tools deserves particular attention given the volume of industry coverage devoted to the subject. As Fishkin notes in the report, "Most AI Search and AI Answers happen on Google. Even if you combine every prompt on ChatGPT, Claude, Deepseek, and the rest and assume every prompt is a search-equivalent, Google dwarfs them." The approximately 16% of Google search results pages that show AI Overviews make Google itself the dominant AI-assisted search experience, while the fraction of users clicking through to Google's AI Mode remains below 0.1%.

Within the AI tools category specifically, the data from Datos' panel shows ChatGPT reached 40.47% of US desktop devices in Q4 2025, followed at a distance by Yahoo at 23.57%, Bing at 18.86%, Deepseek at 4.20%, Claude at 3.99%, Yandex at 3.35%, and DuckDuckGo at 3.17%. In EU/UK markets, Google reached 93.36% of desktop devices, ChatGPT reached 48.77%, and Bing came in at 26.42%.

For search market share rather than mere device reach, the Q4 2025 figures for the US show Google at 73.7%, Amazon at 7.83%, Bing at 4.31%, YouTube at 3.65%, and ChatGPT at 2.86%. DuckDuckGo held 1.26%, eBay 1.06%, and Yahoo 0.92%. Claude registered 0.18% and Deepseek 0.15%.

Perhaps the most operationally relevant finding for search marketers is the ranking of platforms below Google. According to the report, Amazon, Bing, and YouTube each receive more desktop search activity than ChatGPT. Amazon's 7.83% share made it the clear second-largest search destination in the US by Q4 2025 - a figure that grew from 7.16% in Q1. YouTube climbed from 2.61% to 3.65% over the same period. Bing rose from 3.90% to 4.31%.

ChatGPT, by contrast, moved from 1.75% in Q1 to 2.58% in Q4. That is meaningful growth. But it still trails three platforms that search marketing budgets have historically underweighted relative to Google. As Fishkin puts it in the report: "Three domains where search marketers historically have put limited effort compared to the onslaught of dollars flooding the 'we need to rank in ChatGPT!' space."

The trend data for the full year amplifies this point. Google lost 3.5 points of search share between Q1 and Q4 2025 in the US - falling from 77.14% to 73.74% across the top-7 platforms analyzed. That is, according to Fishkin, a loss without precedent in Google's history as a measurable metric. But the beneficiaries were Amazon, Bing, YouTube, and the 34 smaller sites in the study - not primarily ChatGPT, which also shrank slightly in share terms despite growing its absolute volume.

As PPC Land has tracked, the Datos and SparkToro Q4 2025 State of Search report released in January 2026 had already documented traditional search holding around 10% of total desktop activity, with AI tools remaining under 1% of total desktop events when measured against all activity rather than just search queries. The new March 2026 report zooms out further, counting searches directly rather than overall desktop events, which produces the more familiar-looking 80% figure for traditional search.

The EU/UK picture

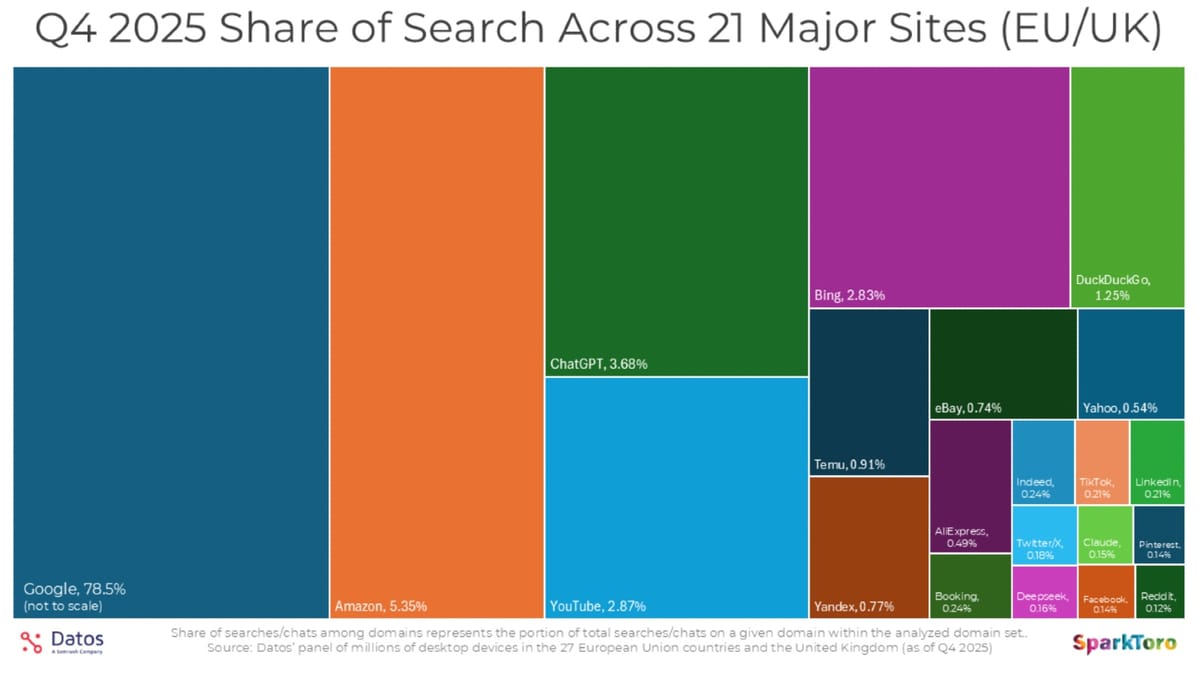

European markets show a slightly different distribution. Google's share in the EU/UK reached 78.5% in Q4 2025 - about 5 points higher than the US figure. Amazon's EU/UK share stood at 5.35%, somewhat lower than its US counterpart, while ChatGPT reached 3.68% - modestly higher than its 2.86% US share. Bing held 2.83% and YouTube 2.87%.

According to the research, in the EU/UK "Google is more dominant (with an additional 5% of all searches vs. the US), while Amazon, YouTube, and Bing hold smaller shares of the search pie." ChatGPT's slightly elevated EU/UK figure is consistent with Europe's "slightly faster/more aggressive adoption of AI tools overall," the report states. AliExpress featured notably in EU/UK e-commerce, reaching 25.34% of EU/UK desktop devices in Q4, compared to its smaller US footprint.

Wikipedia's desktop decline - visible in both the US and EU/UK - is another standout observation. The research points to reduced Google traffic referrals to Wikipedia as a plausible explanation, a dynamic previously explored on PPC Land, where zero-click behavior and on-SERP answers have reshaped the distribution of attention across the web.

Visits vs. searches: a critical distinction

One of the more technically important findings concerns the relationship between visiting a platform and actually searching on it. The research asked Datos to report the percentage of monthly visitors to each domain who performed at least one search or prompt during their visit. The 12-month averages reveal wide variation.

Google leads at 97% - nearly every visitor searches. DuckDuckGo came in at 91%, Bing at 84%, Craigslist at 75%, and Amazon at 73%. Then the numbers drop sharply. Only about 56% of ChatGPT visitors actually prompt the system. eBay came in similarly at 56%. For social platforms, the numbers fall further: YouTube at 23%, LinkedIn at 13%, TikTok at 11%, Twitter/X at 10%, Reddit at 8%, and Facebook at 7%.

The low ChatGPT conversion from visit to prompt has a specific explanation. According to Eli Goodman, CEO of Datos, many ChatGPT visitors arrive only to view conversations others have shared - they are not entering their own prompts. This distinction has a direct consequence for anyone using raw traffic or visit-based data to estimate how much search activity ChatGPT handles. PPC Land has previously reported how ChatGPT's click-through rate to external websites stands at approximately 1.3%, compared to Google's 29.2% - a 96% gap that partly reflects this same visit-versus-engagement dynamic.

SparkToro acknowledged in the report that it had itself fallen into this trap. Upon receiving the new data, Fishkin wrote that he immediately emailed co-founder Casey Henry, and "as of today, we've updated our Search and AI Tool usage graphs to be search-focused rather than visit-centric."

Searches per searcher

A further layer of analysis tracks how many searches each active user performed per month on average. Google users averaged between 92 and 104 searches per month across the year, making it by far the most intensively used platform. DuckDuckGo users averaged 50-56 searches per month, and Bing users averaged 32-38.

ChatGPT users, while falling in the 10+ searches-per-user group, showed considerably lower intensity - ranging from 6.08 prompt sessions per month in January 2025 to around 11-12 by year-end. The low January figure reflects ChatGPT's "slow start" to the year, after which intensity stabilized without dramatic spikes. This data suggests ChatGPT's user base, while growing in breadth, has not yet developed the same habitual daily-use patterns that define Google's core audience.

Threads showed notable growth in searches per searcher, climbing from roughly 2 to nearly 4 over the year, consistent with the platform surpassing Twitter/X's daily user count on mobile in January 2026. Pinterest also featured as a standout, with growing searches per user that Fishkin had highlighted in an earlier State of Search report.

What this means for marketing strategy

The research carries concrete implications for how marketers allocate visibility efforts. As PPC Land has covered, Fishkin has long argued that SEO should be redefined as "Search Everywhere Optimization" - a framework that takes seriously the search activity occurring on Amazon, YouTube, TikTok, Pinterest, and Reddit alongside traditional engines and AI tools.

The new data gives that argument its most rigorous empirical grounding yet. Of the 41 sites analyzed, 23 had more than 0.1% market share of search. Assuming Google conducted 5 trillion searches in 2025 - the same volume as 2024 - that 0.1% threshold is equivalent to 5 billion searches per year on a single platform. Most of those platforms are receiving little to no optimization attention from search marketing teams.

Amazon's advertising growth to $21.3 billion in revenue in Q4 2025 is directly connected to its role as a search destination. The platform's 7.83% share of US desktop searches in Q4 makes it the largest search destination after Google - and one where brands compete through sponsored products and sponsored brands rather than organic link building. The AI tools stabilization data published by Datos and SparkToro in November 2025 similarly pointed to parallel growth rather than substitution between AI and traditional search - a conclusion this new report reinforces at greater scale and resolution.

One methodological note worth flagging: the study does not filter out non-search-relevant AI prompts. A ChatGPT session used entirely for code generation or image creation counts as a search. A Google navigational query for Gmail counts too. The researchers flag this explicitly and note that the diversity of intent underlying what gets counted as a "search" is "important to keep in mind when drawing conclusions." That caveat applies particularly to comparisons between AI platforms, whose prompt mix skews more heavily toward non-informational tasks, and traditional search engines, where informational and navigational intent dominates.

Timeline

- January 2025 - December 2025: Datos' desktop clickstream panel collects data across US, EU, and UK markets covering the 41 analyzed domains

- Q1 2025: Google holds 77.14% of the top-7 search platforms' share in the US; ChatGPT holds 1.75%; Amazon at 7.16%

- Q4 2025: Google's US share among the top 7 declines to 73.74%; Amazon grows to 7.83%; YouTube to 3.65%; ChatGPT reaches 2.58%

- Q4 2025: AI tools reach 3.2% of all desktop search activity across the 41 sites, while traditional search holds 80.76% and commerce 9.76%

- January 28, 2026: Datos and SparkToro publish their Q4 2025 State of Search report, showing traditional search holding ~10% of all desktop activity with AI tools under 1% of total desktop events

- February 11, 2026: Ahrefs publishes analysis showing ChatGPT sends 190 times less traffic to websites than Google despite handling approximately 12% of Google's search volume

- March 2, 2026: Rand Fishkin publishes "Search Happens Everywhere: An Analysis of 41 Websites with Significant Search Activity" via SparkToro, based on Datos' 2025 desktop panel across the US and EU/UK

Summary

Who: Rand Fishkin, co-founder of SparkToro, published the research in partnership with Datos (a Semrush company). The analysis was supported by Datos team members Belinda Conde, Stanislav Pugach, Teresa Lee, and Eli Goodman, with proofreading from Amanda Natividad.

What: A comprehensive analysis of desktop search activity across 41 major websites in the US and EU/UK throughout 2025, measuring search volume, market share, visits-to-searches conversion, and searches per user across traditional search engines, commerce platforms, social networks, AI tools, and other verticals. The research found Google responsible for 73.7% of US desktop searches in Q4 2025, AI tools collectively accounting for 3.2%, and Amazon, Bing, and YouTube each outranking ChatGPT as search destinations.

When: The research was published on March 2, 2026, drawing on Datos' 2025 desktop panel covering the full period January 1, 2025 to December 31, 2025.

Where: The study covers desktop devices in the United States and 27 EU member countries plus the United Kingdom, using Datos' multi-million device clickstream panel. Mobile browsers and apps were excluded.

Why: The research addresses a significant gap in how search market share is typically measured - standard methodologies count only traditional search engines, producing Google market share figures of 90%+, while this study expands the denominator to include commerce, social, AI, and other platforms where people actively conduct information and product queries. The result is a more complete picture of where search behavior actually occurs, with direct implications for how marketing professionals should allocate visibility efforts across platforms.

Share this article

The link has been copied!