IAB lowers 2025 US ad spend forecast as tariff concerns mount

IAB reduced its 2025 US advertising spend projection to 5.7% growth from 7.3% as buyers grapple with tariff impacts on automotive, retail, and consumer electronics sectors.

IAB reduced its 2025 US advertising spend projection to 5.7% growth from 7.3% as buyers grapple with tariff impacts on automotive, retail, and consumer electronics sectors.

The Interactive Advertising Bureau announced on September 25, 2025, a downward revision of its full-year US advertising spend forecast, lowering projections by 1.6 percentage points to 5.7% growth. The adjustment reflects mounting concerns among advertisers about tariff impacts and macroeconomic pressures that have reshaped spending expectations for the second half of 2025.

The revision stems from findings in IAB's 2025 Outlook Study September Update, which surveyed over 200 buyers at brands and agencies between July 29 and August 28, 2025. While first-half spending held steady with IAB's original forecast at 7.0% growth, second-half projections dropped to 5.0%, driving the lower annual outlook.

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Tariff concerns dominate the conversation among advertising buyers. A substantial 91% of buyers express concern about how tariffs will affect media spending, with particular anxiety centered on sectors heavily dependent on imported products and parts. The automotive, retail, and consumer electronics categories face the most pressure, with 62% to 69% of buyers expecting these industries to be hit hardest by tariff-related costs.

Major automotive manufacturers have reported significant tariff-related expenses this year. General Motors cited $1.1 billion in tariff costs, Ford reported $800 million in a single quarter, and Stellantis faced $350 million in impacts. Consumer electronics and retail brands encountered similar challenges, with Apple reporting $1.1 billion in quarterly tariff costs, Nike facing $1 billion, and Adidas experiencing $218 million in second-half impacts.

These financial pressures have prompted widespread price increases across affected sectors. Companies ranging from AutoZone and Volkswagen to Best Buy, Macy's, Shein, Target, Temu, and Walmart have raised or expect to raise prices. Consumer electronics manufacturers Canon, Nikon, and Nintendo have implemented similar adjustments.

David Cohen, CEO of IAB, characterized the current environment as one of significant uncertainty. "The marketplace reacts poorly to uncertainty," Cohen stated. "With tariff impacts starting to roll through the supply chain, there is a lot of hesitance as to where the economy and consumer sentiment will go over the coming months. Marketers are laser-focused on maintaining the utmost flexibility while driving short-term performance that delivers on their business goals."

The survey identified macroeconomic headwinds as the top challenge for media investments, cited by 41% of buyers, followed closely by changing consumer habits at 40%. Additional pain points include demonstrating incrementality of media investments (36%) and executing cross-channel media measurement (36%).In response to buyers' concerns, 42% plan to focus more on performance campaigns, while 39% intend to shift spending toward channels with better measurement capabilities. These adjustments represent increases from February 2025, when concern about tariffs first emerged. At that time, 35% prioritized performance campaigns and 29% emphasized measurement-focused channels.

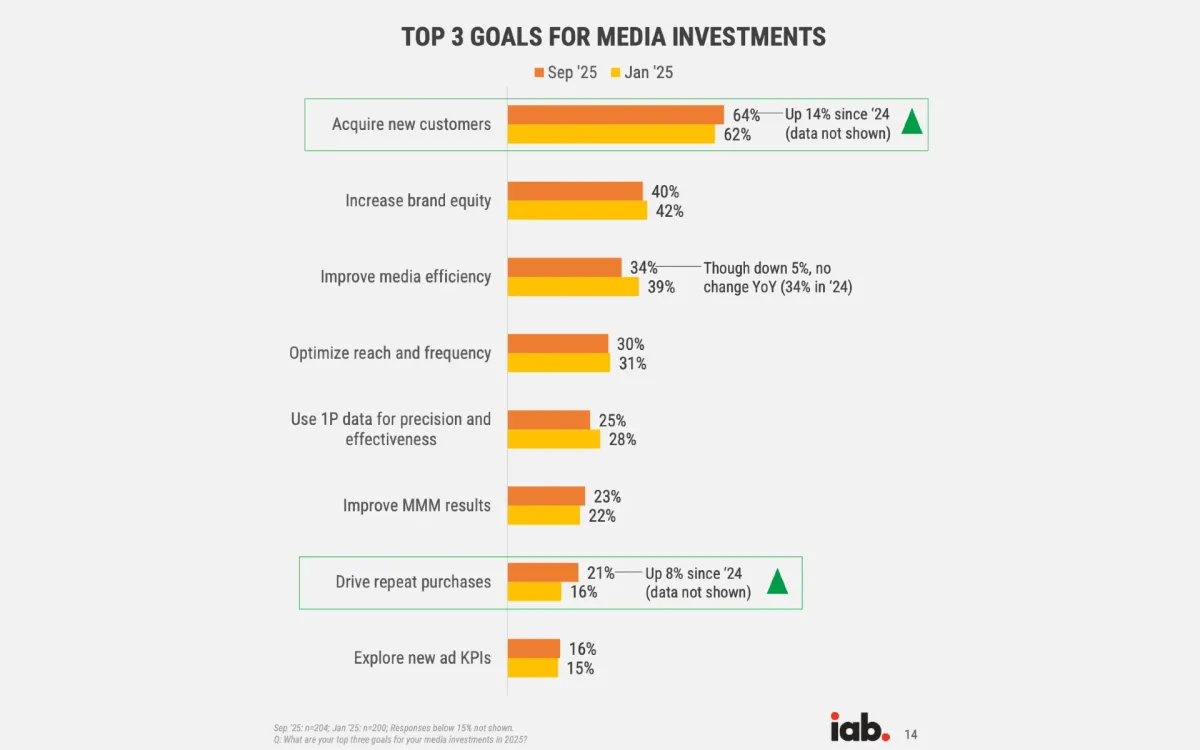

Customer acquisition dominates advertiser objectives, with 64% identifying it as a top goal, marking a 14-percentage-point increase compared to 2024. Driving repeat purchases gained eight percentage points since 2024, now representing 21% of buyer priorities. Chris Bruderle, Vice President of Industry Insights & Content Strategy at IAB, characterized the shift as a response to economic pressures. "In our January report, we saw real concerns about the economy, and a shift toward performance-driven media," Bruderle explained. "Now that shift is accelerating. If consumers are pulling back, that means every single dollar of ad spend has to earn a return—and that's more important than ever for auto, retail, and consumer electronics advertisers."

Despite the overall downward revision, several digital channels remain on track for double-digit growth. Social media advertising is projected to grow 14.3% in 2025, up from January's 11.9% forecast. Retail media maintains 13.2% projected growth, down from 15.6% in January, while connected television advertising is expected to expand 11.4%, compared to January's 13.8% projection.

Traditional media faces steeper declines than previously anticipated. Linear television advertising will contract 14.4%, worse than January's projection of 12.7% decline. Other traditional media categories including radio, print, out-of-home, and direct mail will fall 3.4%, double January's forecasted 1.5% decline.

The budget share allocated to digital video including connected television is expected to hold at 22.3% in 2025, down slightly from January's 23.2% projection. Social media's budget share increased to 18.0% from 17.2%, while linear television's share dropped to 10.2% from 13.7%.

Commerce media, driven primarily by consumer packaged goods and beauty categories, continues growing at double-digit rates but faces deceleration. The channel maintained 13.2% projected growth for 2025, down from January's 15.6% forecast and representing nearly half of 2024's 25.1% expansion. Ecosystem fragmentation, limited measurement capabilities, and difficulties proving incrementality continue dampening broader adoption.

Among buyers concerned about tariff impacts, 45% have reduced or plan to reduce overall spending. This percentage matches February 2025 levels despite the shift from extreme to moderate concern among most respondents. The proportion reporting extreme concern dropped from 57% in February to 25% in September, while those somewhat concerned increased from 37% to 66%.

Flexibility emerged as a priority response, with 36% of concerned buyers negotiating increased flexibility or cancellation options, up from 21% in February. Delaying or pausing ad buys increased from 17% to 22%, while shortening campaign lifespans held steady at 20%.

Cohen emphasized the industry's resilience despite the challenges. "The silver lining in all of this is that the overall attitude of buyers remains positive," Cohen stated. "Budgets may tighten somewhat, but they're confident that digital media can deliver the measurable results they need. This update to our projections should help the industry make the most of the remainder of 2025 while keeping an eye on 2026."

The survey drew responses from 204 advertising investment decision-makers at brands and agencies between July 29 and August 28, 2025. Brands represented 52% of respondents, agencies 42%, and other marketing communications entities 6%. C-level executives and presidents comprised 27% of participants, with senior vice presidents, vice presidents, and directors accounting for 44%, and managers and planners making up 29%.

WPP previously revised its global advertising forecast in June 2025, cutting projections to 6% growth from 7.7%, citing trade disruptions and deglobalization pressures. That analysis showed digital advertising maintaining 73.2% of global ad revenue in 2025, rising to 81.6% when including digital extensions like streaming television and digital out-of-home.

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Who: The Interactive Advertising Bureau surveyed over 200 advertising buyers at brands and agencies to assess spending patterns and concerns.

What: IAB lowered its 2025 US advertising spend growth forecast from 7.3% to 5.7%, a 1.6-percentage-point reduction, while maintaining double-digit growth projections for social media (14.3%), retail media (13.2%), and connected television (11.4%).

When: The announcement came on September 25, 2025, based on survey data collected between July 29 and August 28, 2025, reflecting conditions through the first half of 2025 and expectations for the second half.

Where: The forecast applies to United States advertising markets, with particular impact on sectors including automotive, retail, and consumer electronics that depend heavily on imported products or parts.

Why: Tariff concerns affected 91% of buyers, driving budget reductions and shifts toward performance-driven, measurable advertising channels as macroeconomic headwinds and changing consumer behavior emerged as top challenges for the remainder of 2025.