A survey commissioned by AppLovin's Axon platform and conducted by Kantar has found that 71 percent of mobile gamers who purchase a product after seeing a mobile game advertisement do so on the day of exposure - a conversion speed that rivals the fastest-performing channels in digital marketing. The research, published in February 2026 and based on fieldwork completed in January 2026, surveyed 2,500 U.S. adults who had played a mobile game in the previous three months.

The speed finding sits at the center of a broader dataset that challenges long-standing assumptions about who plays mobile games, what they buy, and how receptive they are to advertising while doing so. For the marketing community, the implications touch on channel allocation, audience targeting, and the question of whether mobile gaming warrants a larger share of performance budgets.

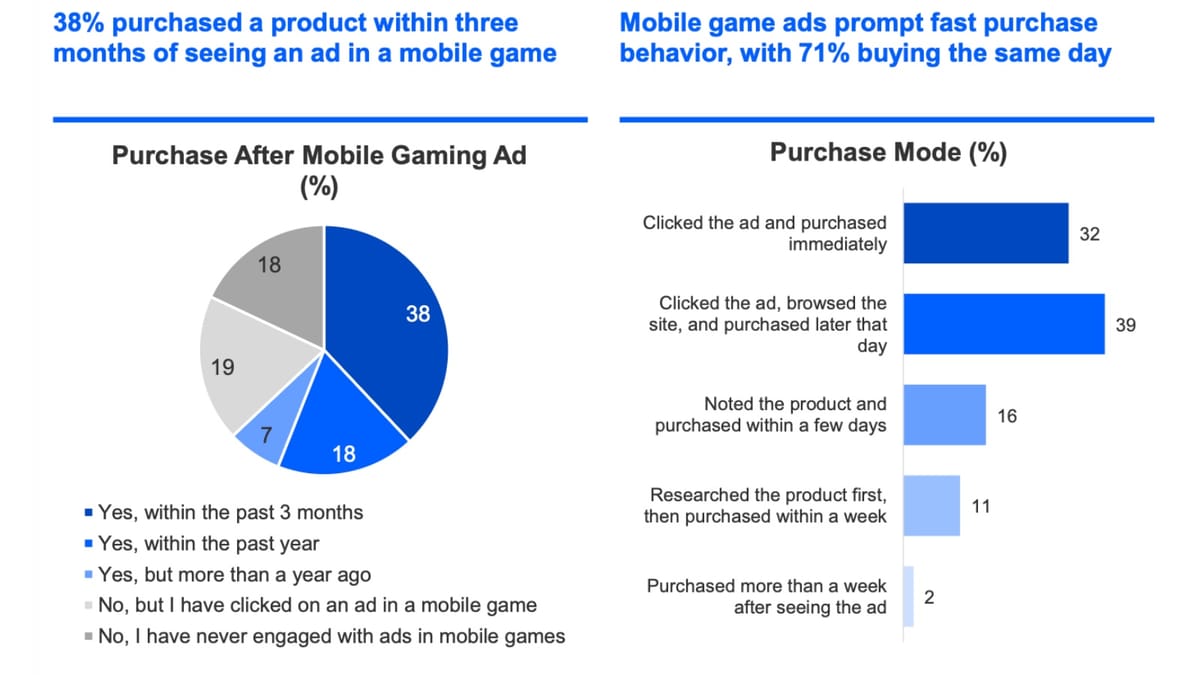

The same-day conversion mechanism

The purchase behavior data is the most commercially concrete element of the study. According to the Kantar report, 38 percent of respondents said they had purchased a product within three months of seeing an advertisement in a mobile game. Among those buyers, 71 percent said the purchase took place the same day. Breaking that down further: 32 percent clicked the ad and purchased immediately, while 39 percent clicked the ad, browsed the site, and completed the purchase later that same day.

Only 2 percent waited more than a week after first seeing the ad.

That pattern - click, browse, buy, all within hours - is structurally similar to the impulse commerce dynamic that has made social feed advertising attractive to direct-to-consumer brands. Yet the channel differs in a significant technical respect: ads in mobile games run within professionally developed applications, not alongside user-generated content. The Kantar report notes this as a brand safety advantage, since adjacency risk is reduced when inventory sits inside a single, known application environment rather than a feed of unpredictable posts.

What drove the purchases? According to the report, 37 percent of buyers said the ad introduced them to a product they had not previously considered - a pure discovery event. Another 47 percent said they had been thinking about buying something similar and the ad reminded them or showed them a specific option. Only 17 percent were already planning to buy that exact product and found the ad simply made the process easier.

The combination matters for how marketers interpret the channel. Discovery accounts for more than a third of conversions. Consideration acceleration accounts for nearly half. Together, they suggest the channel functions across the upper and mid-funnel simultaneously, rather than only closing demand that already existed.

Post-purchase outcomes were also measured. Satisfaction reached 92 percent, with 66 percent describing themselves as very satisfied. Intent to purchase again was 86 percent. These are retention metrics that carry weight in categories with high lifetime value, including consumer electronics, travel, and subscription products.

Who the audience actually is

The persistent image of a mobile gamer as a young man playing combat titles on a console was already becoming outdated before this research. The Kantar data, drawn from a nationally distributed U.S. sample, makes the demographic picture explicit.

Gender split among mobile gamers was 48 percent male and 52 percent female, compared with 49 percent male and 51 percent female in the general population - essentially identical. Age distribution followed a similar pattern: 33 percent of mobile gamers fell in the 25-34 bracket, 21 percent in the 35-44 range, and 19 percent were 55 or older. These figures track closely with general population benchmarks across each band. Full-time employment among mobile gamers stood at 48 percent, compared with 46 percent in the general population. Home ownership reached 63 percent, versus 66 percent nationally.

Regional coverage was broad: 40 percent of respondents came from the Southern U.S., 23 percent from the Northeast, 20 percent from the Midwest, and 17 percent from the West - distributions that roughly parallel the national adult population.

According to the Kantar report, mobile gamers broadly reflect the general consumer population across age, gender, education, geography, and household characteristics, reinforcing mobile gaming as a mass-reach environment rather than a niche channel.

Lifestyle segmentation adds further texture to the audience portrait. Seventy-five percent of mobile gamers in the sample identified as pet owners. Forty-six percent described themselves as food or cooking enthusiasts. Forty-five percent were sports fans. Budget-conscious shoppers made up 41 percent. These are the same consumer identities that direct marketers target across search, social, and email - the difference being that mobile gaming reaches them in a context their peers do not yet saturate with advertising.

Household decision-making and spending authority

Audience scale without purchasing authority is a media planning problem. The Kantar research addressed this directly by asking respondents about household decision-making. Seventy percent of mobile gamers said they make most household purchase decisions themselves. The comparable figure in the general population sample was 60 percent - a statistically significant gap at the 95 percent confidence level, according to the report.

Financial comfort tracked similarly. Seventy percent of mobile gamers described their financial situation as comfortable, either very comfortable or somewhat comfortable. Seventy-one percent shop online at least weekly. Seventy-seven percent spend $100 or more per month on online purchases. Within that group, 23 percent spend between $100 and $199 per month, another 23 percent between $200 and $299, and 16 percent between $300 and $499.

Forward-looking category intent was also measured. Among high-ticket items planned for purchase in the next six months, smartphones and tablets led at 46 percent, followed by travel and vacation at 42 percent, computers and laptops at 37 percent, furniture at 31 percent, and vehicles at 29 percent.

The income segmentation data is particularly relevant for advertisers targeting premium consumers. Among households earning $80,000 to $99,999 annually, 77 percent had purchased a product within three months of seeing a mobile game ad - the highest conversion rate across all income bands tested. Households earning $50,000 to $79,999 converted at 71 percent over the same period. Even at the $200,000-and-above level, 72 percent had converted. Gaming frequency was notably consistent across income levels: among $100,000-plus earners, 70 percent played daily and 96 percent played weekly, figures nearly identical to lower-income brackets.

The Kantar report states that 70 percent of mobile gamers report feeling financially comfortable, and that 71 percent shop online at least weekly, with 77 percent spending $100 or more per month shopping online.

Engagement patterns and emotional context

The report measured not only what mobile gamers buy but when and how they feel while playing. Fifty-eight percent of respondents said they typically play in the evening at home. Fifty-two percent play while watching television. Forty-four percent play before going to sleep, and another 44 percent play on weekends or days off. These are lean-back moments characterized by reduced cognitive load - an environment advertisers associate with higher receptivity in broadcast television research as well.

Mobile gaming is a daily habit for 70 percent of players, according to the Kantar report. Ninety-seven percent play at least weekly. When given 10 hypothetical free minutes, 29 percent of respondents said they would choose to play a mobile game - ahead of watching video or streaming content at 15 percent, messaging at 13 percent, and shopping or browsing products at 5 percent.

Time-use data showed gaming dominates mobile attention relative to other activities. Among participants spending three or more hours per day on their phones, 13 percent spent that time gaming versus 5 percent shopping or browsing and 9 percent messaging.

Emotional state during gameplay was measured against the benchmark of browsing social media. While playing mobile games, 50 percent of respondents reported feeling very positive, compared with 47 percent during social media browsing. The neutral-to-negative proportion was substantially lower during gaming than during social media use. On a combined top-two-box positivity measure, gaming scored 85 versus 80 for social media - a statistically significant difference at the 95 percent confidence level. Seventy-one percent of mobile gamers said they view ads positively while playing.

This emotional dimension carries weight for brand advertising beyond direct response. The Kantar analysis frames gaming as a context that combines attention with positive affect - a pairing that, in media effectiveness research more broadly, is associated with stronger encoding and recall. As Kantar's research on advertising attention published in July 2024 demonstrated, the relationship between attention and brand-building is more complex than raw viewability metrics suggest, with emotional context playing a structuring role.

Methodology and sample design

The survey was conducted using Kantar's KAP Custom Survey Automation methodology. Fieldwork ran in January 2026. Qualification criteria required respondents to be U.S. adults aged 18 or older who had played a mobile game in the previous three months. The final sample of 2,500 respondents was recruited through trusted panel partners operating under ESOMAR data quality principles and a double opt-in registration process.

Kantar applied multiple quality controls at the design and fielding stages. Identity verification used geolocation via IP addresses, browser-based location checks, and a Proxy Score mechanism. Device detection matched respondents to appropriate surveys. Digital fingerprinting identified and eliminated duplicate participants. In-survey quality checks included red herring questions to screen out inattentive respondents and speed traps designed to catch automated or dishonest responses.

The screener design did not disclose the study's purpose before a respondent qualified, preventing gaming of the qualification questions. All survey questions were pre-tested, and soft launch data was reviewed before full deployment. The Kantar report notes that general population comparison data is provided for context only and that the survey sample is not nationally representative in a strict probability sense.

The research was prepared for Axon by AppLovin. That commissioning relationship is relevant context for how the findings should be interpreted. The study was designed to support a commercial argument AppLovin has been developing - that its gaming inventory deserves a larger share of non-gaming advertiser budgets. The data itself comes from a third-party research firm with established methodology, but the framing, presentation, and selection of metrics reflect the client's objectives.

Context for marketing professionals

The report arrives at a specific moment in AppLovin's commercial trajectory. The company has been actively expanding beyond its gaming-advertiser base for roughly 18 months, bringing e-commerce and direct-to-consumer brands onto its Axon platform. AppLovin's Q4 2025 results showed revenue of $1.66 billion, up 66 percent year-over-year, with the self-service Axon Ads Manager - launched on October 1, 2025 - continuing to scale through a referral system. The Axon platform currently reaches over one billion daily active users, primarily adults playing casual mobile games.

For context, AppLovin's CEO addressed transparency concerns in February 2026, following short-seller reports earlier in 2025 that questioned advertising incrementality claims and data collection practices. Those controversies are part of the backdrop against which this Kantar research was published - the data functions partly as third-party validation of the audience quality and commercial effectiveness arguments AppLovin has been making to prospective advertisers.

The gaming advertising ecosystem has attracted broader institutional attention in parallel. The IAB established standard metrics for gaming advertising measurement in June 2025, addressing transparency gaps as the channel has grown. Separately, the AppsFlyer 2025 Performance Index published in December 2025 ranked AppLovin first in the gaming Creative Performance Index and second globally in the power ranking. Research on gaming audiences across international markets has shown consistent patterns: a July 2025 study by IAB Poland found gamers outspend non-gamers across multiple product categories, while LoopMe research from late 2025 found gamers more than three times as likely to be receptive to advertising in gaming environments compared to mobile web.

The Kantar study's specific contribution to this body of evidence is the same-day conversion data. Prior gaming advertising research has generally focused on audience demographics, brand safety perceptions, and engagement time. Granular purchase timing data - how quickly after ad exposure a transaction occurs - is rarer and carries direct relevance for performance budget allocation decisions. The finding that 71 percent of converters act on the same day, with 32 percent clicking and purchasing immediately, positions mobile gaming alongside social commerce formats in speed-of-conversion terms.

Whether individual marketers find this persuasive will depend in part on how they weigh independently commissioned research against the commissioning context - and on their own platform testing results, which vary considerably by category, creative format, and target audience.

Timeline

- January 2026 - Kantar conducts fieldwork for the mobile gaming consumer study, surveying 2,500 U.S. adults aged 18 and older who had played a mobile game in the previous three months.

- February 2026 - Kantar publishes "Mobile Gaming: The New Mainstream Consumer Channel," prepared for Axon by AppLovin, containing the full dataset on demographics, purchasing behavior, and advertising receptivity.

- February 2, 2026 - AppLovin CEO Adam Foroughi publishes a blog post defending the company's business modelfollowing months of short-seller scrutiny.

- February 11, 2026 - AppLovin reports Q4 2025 revenue of $1.66 billion, up 66 percent year-over-year, with the self-service Axon Ads e-commerce platform continuing to scale.

- March 21, 2026 - AppLovin's Axon Growth Ops Team publishes a summary blog post on axon.ai highlighting the Kantar findings and linking to the full report.

Earlier context

Summary

Who: AppLovin's Axon advertising platform commissioned the research. Kantar, the market research firm, designed and executed the study. The subjects were 2,500 U.S. adults aged 18 and older who had played a mobile game within the previous three months.

What: A consumer research report titled "Mobile Gaming: The New Mainstream Consumer Channel," published in February 2026, measuring the demographics, financial profiles, purchasing behavior, and advertising receptivity of U.S. mobile gamers. The headline finding is that 71 percent of mobile gamers who purchase a product after seeing a mobile game ad do so on the day of ad exposure, with 32 percent buying immediately after clicking.

When: Fieldwork was conducted in January 2026. The full Kantar report was published in February 2026. The Axon blog post summarizing the findings was published today, March 21, 2026.

Where: The study covered the United States across all four census regions - Northeast, Midwest, South, and West - and across urban and rural community types. The research was conducted online using Kantar's KAP Custom Survey Automation methodology.

Why: AppLovin has been expanding its Axon advertising platform beyond gaming-specific advertisers into e-commerce and direct-to-consumer categories. The research provides third-party demographic and behavioral data to support the commercial argument that mobile gaming inventory offers performance-oriented advertisers access to a mainstream adult audience with significant purchasing authority - and that the conversion window is substantially faster than the channel's historical reputation suggested.

Share this article

The link has been copied!