Paramount climbs to third despite losing ground year-over-year

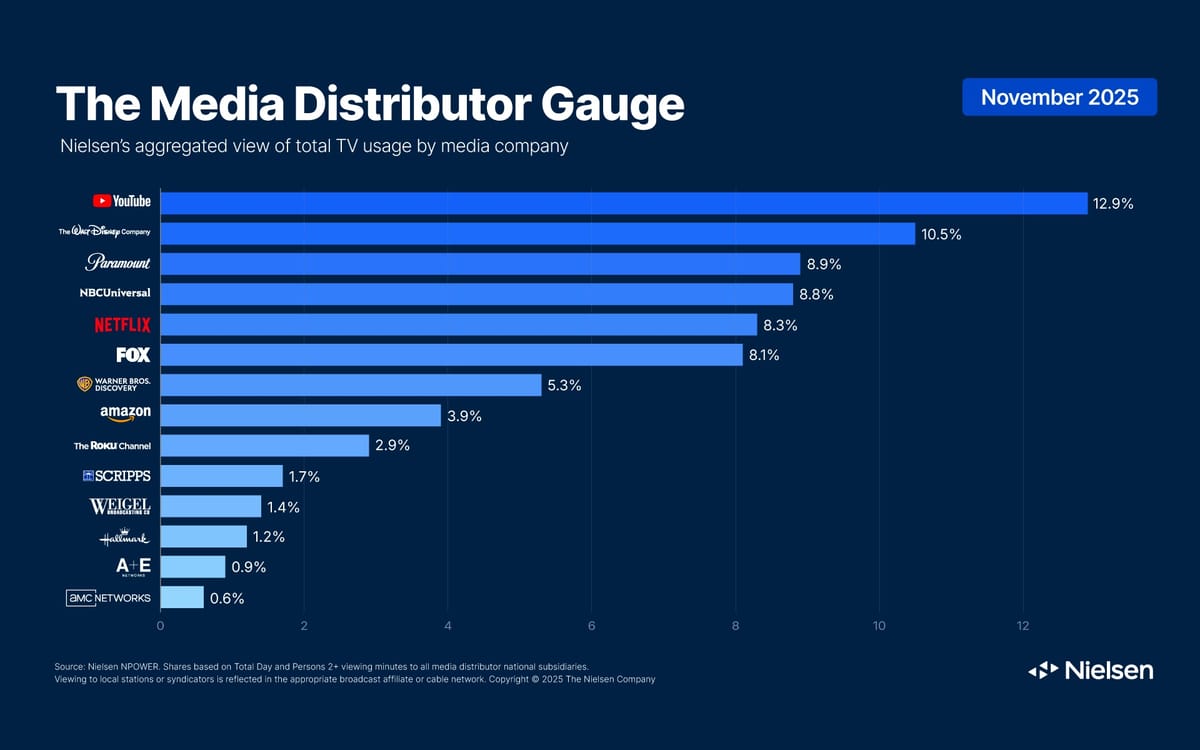

Paramount captured 8.9% of TV in November 2025 with strong monthly gains, though down from 9.3% in 2024. Netflix grew to 8.3% while YouTube leads at 12.9% share.

Paramount captured 8.9% of TV in November 2025 with strong monthly gains, though down from 9.3% in 2024. Netflix grew to 8.3% while YouTube leads at 12.9% share.

Nielsen released its November 2025 Media Distributor Gauge on December 22, revealing a television landscape where monthly momentum masks underlying year-over-year shifts. Paramount climbed to third position among all media distributors during November despite declining 0.4 share points compared to the same period in 2024, while Netflix expanded its presence and YouTube solidified dominance at the top.

Paramount captured 8.9% of total television watch-time in November 2025, posting a 14% increase over October through combined strength across broadcast and streaming properties. CBS affiliates drove half of this growth with an 18% viewing surge, contributing 0.5 share points, while Paramount+ streaming service added 0.2 share points with its own 18% monthly increase. The 0.7 share point gain represented the largest monthly increase among all distributors measured, positioning Paramount at its strongest performance since April 2025.

The measurement interval spanned five weeks from October 27 through November 30, following Nielsen's broadcast calendar where weekly intervals begin on Monday. This period encompassed Thanksgiving Day programming and substantial live sports coverage that influenced viewing patterns across multiple platforms.

Subscribe PPC Land newsletter ✉️ for similar stories like this one

However, year-over-year data shows Paramount declining from 9.3% in November 2024 to 8.9% in November 2025, a 0.4 share point drop despite the strong month-over-month performance. This contradiction illustrates how seasonal fluctuations and programming strategies can create divergent trends when examining different time horizons.

Netflix achieved 8.3% of total television usage in November 2025, adding 0.3 share points through a 10% monthly viewing increase. The return of Stranger Things generated nearly 12 billion viewing minutes alone, while new original series The Beast in Me and Guillermo del Toro's Frankenstein film combined for approximately 7 billion viewing minutes across the month. Year-over-year, Netflix expanded from 7.7% in November 2024 to 8.3% in November 2025, demonstrating consistent growth trajectory.

YouTube maintained first position with 12.9% of television viewing in November 2025, holding steady month-over-month. This represents significant year-over-year growth from 10.8% in November 2024, adding 2.1 share points to cement its position as the dominant media distributor measured by Nielsen.

Disney dropped to second position with 10.5% share, declining 0.9 share points versus October 2025. Year-over-year comparisons show Disney falling from its November 2024 leadership position of 11.1%, losing 0.6 share points. The decline stemmed primarily from ABC affiliates and ESPN decreases attributable to the carriage interruption from the YouTube TV dispute that affected live sports programming access.

NBCUniversal posted 7% overall viewing growth to capture 8.8% of TV (+0.2 points), marking its largest total since October 2024. Peacock streaming drove NBCU's gains with a 22% surge fueled by NFL Sunday Night Football coverage and Thanksgiving Day programming. The platform achieved a non-Olympic monthly record of 1.9% television share in November. Compared to November 2024 when NBCUniversal held 8.7%, the distributor gained 0.1 share points year-over-year.

FOX finished November 2025 with 8.1% of TV viewing after gaining 2.4% in total usage but ceding 0.3 share points due to the 5.5% increase in overall TV usage. FOX broadcast affiliates surged 22% versus October, led by the Thanksgiving Day NFL matchup between Green Bay and Detroit plus World Series Games 4 through 7. The final World Series game ranked as the sixth most-viewed telecast of the month. FOX recorded 8.6% in November 2024, meaning the network declined 0.5 share points year-over-year despite monthly gains.

Hallmark produced the highest percentage viewing increase during November 2025 with a 28% gain, reaching 1.2% of total TV watch-time. The network benefited from its signature slate of holiday movies alongside original series Mistletoe Murders. Year-over-year data shows Hallmark declining from 1.4% in November 2024 to 1.2% in November 2025, a 0.2 share point drop despite recording even stronger percentage growth in 2025 (28%) than 2024 (24%).

Total TV usage increased 5.5% in November 2025 compared to October 2025, with overall viewing patterns reflecting the combined impact of live sports, holiday programming, and the five-week measurement interval. This growth rate exceeded typical month-over-month fluctuations, demonstrating how seasonal factors and major events can substantially shift aggregate viewing levels.

The November 2025 data arrives as Nielsen has expanded measurement capabilities across multiple markets, providing advertisers with increasingly granular insights into cross-platform viewing behaviors. The company's measurement infrastructure incorporates person-level data from panels exceeding 100,000 people across 42,000 homes nationwide, complemented by big data resources that capture television viewing at the device level across cable, satellite, and streaming platforms.

CBS affiliates benefited from extensive sports coverage including NFL games and college football programming that attracted audiences seeking live event viewing. The broadcast network's strong performance aligns with broader NFL-driven gains observed in previous months, where Sunday programming created dramatic category shifts across the television landscape.

Paramount's streaming service reached audiences through both subscription and ad-supported tiers, with the platform having integrated measurement partnerships covering broadcast, cable and streaming properties. This multi-year agreement provides comprehensive audience insights across Paramount's diverse media portfolio, addressing advertisers' needs for unified measurement in fragmented viewing environments.

Netflix's performance in November reflects the platform's dual strategy of tentpole content releases combined with depth of catalog offerings. While Stranger Things dominated viewing minutes, the breadth of available content including original films and series enabled the platform to capture sustained attention throughout the measurement period. The streaming service operates both ad-supported and ad-free subscription tiers, with the ad-supported option creating inventory for advertisers while maintaining subscription revenue streams.

Buy ads on PPC Land. PPC Land has standard and native ad formats via major DSPs and ad platforms like Google Ads. Via an auction CPM, you can reach industry professionals.

Peacock's 1.9% share in November 2025 marked significant progress for NBCUniversal's streaming efforts, demonstrating how NFL programming drives platform adoption and sustained viewing. The service has increasingly focused on live sports as a differentiation strategy, with NFL Sunday Night Football providing exclusive streaming access alongside traditional broadcast distribution.

The YouTube TV carriage dispute that affected Disney properties illustrates ongoing tensions between traditional media companies and digital distributors over content licensing terms and revenue sharing arrangements. Such disputes periodically disrupt viewer access to live programming, particularly impacting sports coverage where alternative viewing options remain limited. ABC and ESPN properties experienced viewing declines during November as subscribers lost access through YouTube TV, the largest internet-based TV service measured in Nielsen data.

Holiday programming demonstrated continued relevance for advertisers seeking to reach audiences during the November-December period. Hallmark's 28% viewing gain in November 2025 compared to 24% in November 2024 reflects specialized content strategies that capitalize on seasonal viewer preferences, providing advertisers with concentrated audience delivery during specific calendar periods. However, the year-over-year share decline from 1.4% to 1.2% illustrates how overall television usage growth can erode individual distributor positions despite strong percentage performance.

The five-week measurement interval for November 2025 created longer observation periods compared to typical four-week monthly reports, potentially amplifying viewing changes and share point shifts. November 2024's measurement spanned four weeks from October 28 through November 24, while November 2025 covered five weeks from October 27 through November 30, complicating direct month-over-month and year-over-year comparisons.

Streaming platforms collectively maintained dominant positions in the Media Distributor Gauge, with YouTube, Netflix, Paramount+, Peacock, and other services combining to represent substantial portions of total television viewing. This distribution reflects the continuing evolution of streaming's market share, which has progressively increased since Nielsen began publishing comprehensive cross-platform measurement data.

Advertiser implications extend across multiple dimensions as viewing fragmentation continues. Brands seeking mass reach must increasingly allocate budgets across multiple distributors rather than concentrating spending on dominant broadcast networks. The rise of streaming platforms with both subscription and advertising models creates new inventory sources while simultaneously fragmenting audience delivery.

Live sports programming remains among the few content categories capable of generating simultaneous mass audiences across both broadcast and streaming distribution. The NFL's Thanksgiving Day games, World Series coverage, and regular season matchups drove viewership spikes for CBS, FOX, Peacock, and Paramount+ during November 2025. This pattern reinforces sports rights' value for both traditional broadcasters and streaming platforms competing for advertising revenue.

Paramount's November 2025 performance demonstrates the complexity of television measurement in the current environment. The company achieved the largest monthly viewing gain among all distributors while simultaneously declining year-over-year, illustrating how strategic programming decisions, seasonal content deployment, and overall market dynamics interact to produce divergent trends across different measurement horizons.

The year-over-year declines for Paramount, FOX, Hallmark, and Disney contrast with growth for YouTube, Netflix, and NBCUniversal, suggesting structural shifts in how audiences allocate attention across distributors. YouTube's 2.1 share point gain year-over-year represents the most substantial increase, reinforcing the platform's trajectory as the leading television distributor despite not operating traditional broadcast or cable networks.

Measurement methodology differences affect interpretations of both month-over-month and year-over-year comparisons. Nielsen implemented Big Data + Panel measurement during 2025, combining traditional panel data with device-level information from 45 million households. This enhanced methodology provides more comprehensive viewing capture than previous panel-only approaches, though direct comparisons with November 2024 data measured under the legacy system require careful interpretation.

Content investment strategies revealed in the November data demonstrate different approaches across distributors. Netflix maintains extensive catalog depth with continuous original content releases, while networks like Hallmark concentrate resources on seasonal programming designed to capture specific audience segments during limited timeframes. Both models demonstrated effectiveness in November 2025, though with divergent year-over-year trajectories.

Platform-level viewing data provides advertisers with insights into where audiences allocate attention, informing media planning decisions across increasingly complex campaign strategies. The shift from three major broadcast networks to dozens of distributors each commanding meaningful audience shares requires sophisticated optimization approaches that balance reach, frequency, and cost efficiency across multiple platforms.

Disney's year-over-year decline from 11.1% to 10.5% despite maintaining second position highlights competitive pressures facing established media companies. The temporary loss of YouTube TV distribution affected millions of subscribers during a period when live sports programming traditionally attracts premium audiences. Such disruptions create revenue implications for both advertising-supported and subscription-based business models.

The November measurement period preceded major fourth-quarter advertising spending typically associated with December holiday shopping and year-end campaigns. Results from this interval provide baseline data for evaluating seasonal advertising effectiveness across platforms, with particular relevance for retailers and consumer brands planning Connected TV campaigns.

Warner Bros. Discovery captured 5.3% share in November 2025, declining from 6.1% in November 2024, representing a 0.8 share point year-over-year drop. Amazon held 3.9% in November 2025 compared to 3.7% in November 2024, gaining 0.2 share points year-over-year. These smaller distributors face intensifying competition as larger platforms consolidate audience attention.

The Roku Channel expanded to 2.9% in November 2025 from 1.9% in November 2024, marking substantial year-over-year growth of 1.0 share points. This performance demonstrates free ad-supported streaming television's continued expansion, with Roku benefiting from both platform reach and content depth. Scripps declined to 1.7% from 2.0%, while A+E dropped to 0.9% from 1.1%, and AMC Networks fell to 0.6% from 0.8%, illustrating pressure on traditional cable-focused distributors.

Cross-platform measurement remains challenging despite technological advances, as viewers increasingly shift between devices and platforms throughout individual viewing sessions. A single household might watch NFL pregame coverage on broadcast television, stream the actual game on a mobile device, and view post-game highlights through a connected TV app. Capturing this fragmented behavior requires sophisticated attribution methodologies.

November 2025's results demonstrate television's continued ability to aggregate mass audiences despite increasing platform fragmentation. The 5.5% growth in total TV usage versus October indicates that competition among distributors for viewer attention may be expanding overall engagement rather than simply redistributing existing viewership. This pattern suggests that streaming platforms and traditional broadcasters collectively generate incremental viewing occasions.

The data release timing on December 22 provides the advertising industry with final November insights before year-end planning cycles conclude. Fourth-quarter performance evaluations typically incorporate both November and December data to assess full holiday period effectiveness, making timely measurement reporting essential for campaign optimization and annual budget allocation processes.

Subscribe PPC Land newsletter ✉️ for similar stories like this one

Subscribe PPC Land newsletter ✉️ for similar stories like this one

Who: Nielsen measured viewing across media distributors including YouTube (12.9%), Disney (10.5%), Paramount (8.9%), NBCUniversal (8.8%), Netflix (8.3%), FOX (8.1%), and Hallmark (1.2%). The data represents viewing from Nielsen's 42,000-home panel covering more than 100,000 people nationwide using Big Data + Panel methodology combining traditional panel data with device-level information from 45 million households.

What: YouTube maintained first position with 12.9% share (+2.1 points year-over-year from 10.8% in November 2024). Paramount recorded the largest monthly gain of 0.7 share points through 14% viewing increase to reach 8.9%, though this represents a year-over-year decline from 9.3% in November 2024. Netflix grew from 7.7% to 8.3% year-over-year (+0.6 points). Disney dropped from first position at 11.1% in November 2024 to second at 10.5% in November 2025 (-0.6 points). FOX declined from 8.6% to 8.1% year-over-year despite monthly gains.

When: The November 2025 measurement interval spanned five weeks from October 27 through November 30, 2025, compared to four weeks in November 2024 (October 28 through November 24). Nielsen released the Media Distributor Gauge results on December 22, 2025.

Where: The measurements cover United States television viewing across broadcast, cable, streaming, and other distribution platforms accessed through television screens. Data excludes mobile device and computer consumption. Nielsen's Big Data + Panel methodology incorporates viewing data from cable, satellite set-top boxes, smart TVs, and streaming devices across 45 million households combined with traditional panel measurement.

Why: Live sports programming including NFL games and World Series coverage, strategic streaming content releases including Netflix's Stranger Things return, and Thanksgiving holiday programming drove monthly viewing gains. However, year-over-year comparisons reveal structural shifts favoring YouTube and Netflix at the expense of traditional media conglomerates. The YouTube TV carriage dispute affecting Disney properties created offsetting declines for ABC and ESPN. Overall TV usage growth of 5.5% month-over-month diluted share for distributors that grew slower than the category average, explaining why Paramount's 14% monthly gain translated to year-over-year decline when compared against November 2024's 9.3% baseline.