Six months after Amazon's entry into the ad-supported streaming market, cost per thousand (CPM) rates have declined significantly across major streaming platforms, according to industry data. The shift began in January 2024 when Amazon defaulted all Prime Video subscriptions to include advertisements, marking a strategic move that has reshaped the streaming advertising landscape.

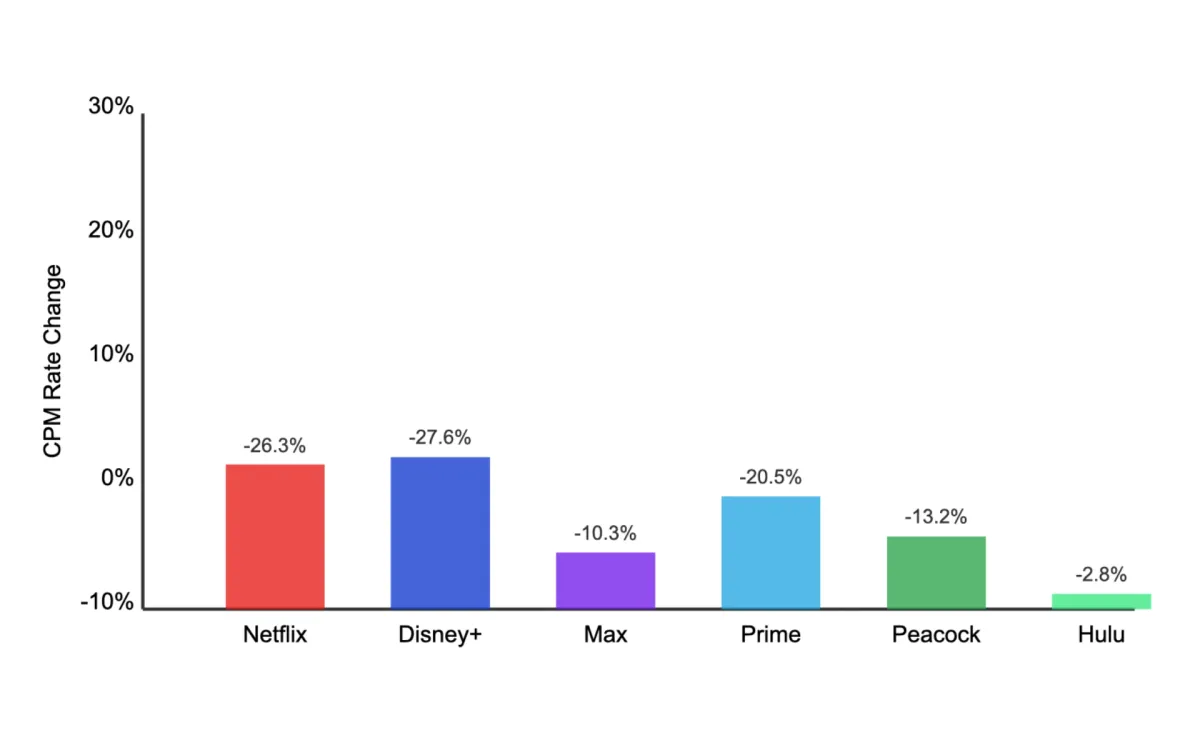

According to EMARKETER data released on December 9, 2024, Netflix and Disney+ experienced the most substantial CPM decreases at 26.3% and 27.6% respectively. Max witnessed a 10.3% reduction, while Prime Video and Peacock saw their rates decline by 20.5% and 13.2%. Hulu maintained relative stability with a modest 2.8% decrease.

The market transformation began when Amazon introduced its ad-supported tier at CPM rates between $30 and $35, significantly lower than competitors' rates. According to the Wall Street Journal, this forced Netflix to adjust its CPM rates from a previous range of $39 to $45 down to approximately $29 to $35.

Mark Douglas, CEO at MNTN, an ad tech company specializing in connected TV (CTV), explained the dynamics at play during the Cannes Lions advertising industry event in June. "Amazon knows how to gain market share and they know how to use price to gain market share," Douglas said. "They can monetize the content way better and bring down the price. That is the main dynamic at work right now."

The impact extends beyond pricing. MoffettNathanson estimates indicate Prime Video could contribute over 50 billion impressions to the connected TV market this year, "an amount that is likely to dwarf a lot of the smaller players in the space."

Amazon's competitive advantage stems from its extensive reach through Prime delivery services and its ability to maintain customers within its ecosystem. Rita Ferro, Disney's president of global advertising, acknowledged the market changes at Cannes Lions: "There's no question it has created an excess of supply in the marketplace."

The transformation of Prime Video subscriptions occurred when Amazon defaulted all subscriptions to the ad-supported tier at monthly rates of $14.99 for Prime delivery members and $8.99 for non-Prime members. Subscribers seeking an ad-free experience must now pay an additional $3 monthly.

Industry analysts project this downward pressure on CPM rates to continue into early 2025, though the rate of decline is expected to moderate. By the second quarter of 2025, EMARKETER forecasts that Netflix and Max will be the only streaming services maintaining average CPMs above $30.

The broader implications for advertisers and the industry are significant. The decrease in streaming ad costs provides an opportunity for marketers to offset rising social media advertising expenses. Additionally, as linear TV viewership continues to decline, ad prices in traditional television are also falling after years of growth.

Connected TV ad spending is projected to reach $33.35 billion in 2025, according to EMARKETER's November forecast. This growth comes as streaming services compete not only on pricing but also through enhanced targeting capabilities and improved ad formats.

The current market dynamics represent a significant shift in the streaming industry's monetization strategies. As competition intensifies with players like Fubo, Tubi, and Paramount+ entering the space, prices may continue to face downward pressure. This trend benefits advertisers but raises questions about maintaining user experience quality amid potential increases in ad frequency and duration.

For advertisers, the evolving landscape presents both opportunities and challenges. While lower CPMs make streaming advertising more accessible, the fragmented nature of the market requires sophisticated strategies to effectively reach target audiences across multiple platforms.

As the streaming advertising market continues to mature, industry observers anticipate further evolution in how services compete for ad dollars, potentially leading to innovations in ad delivery, measurement capabilities, and viewer experience optimization.

Share this article

The link has been copied!