Semrush posts 20% revenue growth as AI products accelerate adoption

Q2 2025 results show $108.9 million revenue with enterprise customers paying $50,000+ annually surging 83% year-over-year.

Q2 2025 results show $108.9 million revenue with enterprise customers paying $50,000+ annually surging 83% year-over-year.

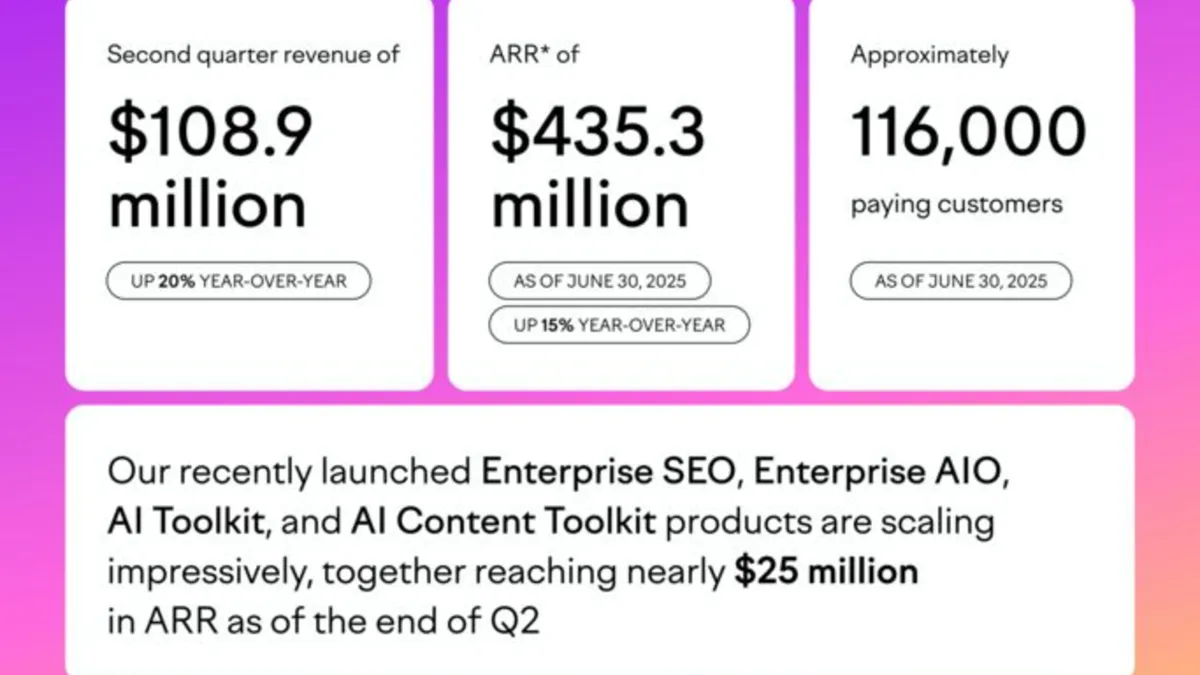

Semrush Holdings Inc. (NYSE: SEMR) reported second quarter 2025 revenue of $108.9 million, marking a 20% increase from the same period last year, according to financial results announced August 4, 2025. The online visibility management platform company demonstrated strong growth in its artificial intelligence and enterprise product segments while confronting challenges in lower-tier customer acquisition.

The Boston-based SaaS company achieved annual recurring revenue (ARR) of $435.3 million as of June 30, 2025, representing 15% year-over-year growth. Customers paying more than $50,000 annually increased 83% year-over-year, signaling robust adoption among enterprise clients. According to company executives, Enterprise SEO has become the single largest contributor to both revenue and ARR growth within just one year of general availability.

"We posted strong revenue growth in the second quarter and were especially pleased by the accelerated adoption of our AI and Enterprise products," said Bill Wagner, CEO. The company achieved approximately 116,000 paying customers as of June 30, 2025, while dollar-based net revenue retention reached 105%.

Subscribe the PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

The company's Enterprise SEO solution expanded to 260 customers with average ARR of approximately $60,000 per customer. This represents significant momentum for a product launched just over a year ago. Enterprise customers now demonstrate dollar-based net revenue retention consistently above 120%, highlighting the platform's ability to expand within existing accounts.

Average ARR per paying customer increased to $3,756, representing growth of more than 15% compared to the same quarter last year. This metric reflects Semrush's successful cross-selling strategy and movement toward higher-value customer segments. According to CFO Brian Mulroy, the company expects ARR from Enterprise and AI products to approach $50 million by the end of 2025.

"Notably, our Enterprise SEO product is gaining traction in the market with new deals such as Digital Ocean, HSBC, and the Royal Bank of Canada," according to previous company statements. The enterprise segment's growth aligns with marketing industry trends toward AI-powered search optimization as businesses adapt to changing search landscapes.

Semrush introduced AI Optimization (AIO) as an Enterprise Solution during the second quarter, providing businesses with tools to track, control, and optimize brand presence across AI-powered search platforms. Within several weeks of launch, over 30 enterprise customers purchased this new AI product for total ARR of nearly $1 million.

The company's AI Toolkit became the fastest-growing product in company history, expanding from zero to $3 million in ARR within months of its late Q1 2025 launch. According to Wagner, usage data shows customers who purchase AI Toolkit experience a 20% increase in their activity within Semrush's SEO Toolkit, demonstrating complementary product adoption.

"We believe we are approaching a time when every SEO expert will need to add AI Search capabilities," Wagner stated during the earnings call. The company introduced several AI-powered enhancements, including SearchGPT integration within Position Tracking tools and an AI Traffic dashboard enabling businesses to monitor brand visibility across platforms like ChatGPT, Copilot, Gemini, and Perplexity.

Industry analysis indicates AI search optimization is fundamentally changing SEO practices, with Google's AI Overviews now operating in 200 countries and 40 languages as of May 2025. This technological shift creates new opportunities for platforms like Semrush that provide comprehensive AI search optimization tools.

The company encountered continued softness in its lower-tier customer segment, including freelancers and less sophisticated users who historically demonstrate higher churn rates. This customer segment faced additional pressure from dramatic increases in paid-search cost-per-click during the quarter, elevating customer acquisition costs.

According to Wagner, the company made strategic decisions not to increase marketing spend pursuing volume and near-term revenue at the expense of long-term value. Instead, Semrush directed marketing and engineering resources toward high-growth, high-retention segments, specifically Enterprise and AI search products where customer demand and returns prove more compelling.

Cash flow from operations reached $0.7 million in the second quarter, representing a cash flow margin of 0.6%. Free cash flow was negative $3.6 million, primarily due to timing of cash tax payments, collections, and prepaid expenses. The company maintains expectations for 12% free cash flow margin for full-year 2025.

Semrush revised its full-year 2025 revenue guidance to $443.0 million to $446.0 million, representing approximately 18% growth at the midpoint. This represents a reduction from previous guidance of $448.0 million to $453.0 million, reflecting near-term revenue headwinds from strategic resource shifts toward higher-value segments.

For the third quarter 2025, the company expects revenue between $111.1 million to $112.1 million, representing approximately 15% year-over-year growth at the midpoint. Third quarter non-GAAP operating margin is expected at approximately 11.5%.

The company maintains full-year expectations of 12% for both non-GAAP operating margin and free cash flow margin, despite reduced revenue outlook and foreign exchange headwinds from a weaker U.S. dollar. Non-GAAP operating margin reached 11.0% in the second quarter, compared to 13.4% in the prior year period.

Forrester named Semrush as a Leader in SEO Solutions, recognizing the company's competitive intelligence, robust analytics, and vision for SEO as the "engine of digital discoverability." This recognition comes as the SEO industry adapts to AI search disruption, with traditional optimization practices evolving to address artificial intelligence-powered search environments.

The company announced a $150 million share repurchase program, demonstrating confidence in business fundamentals and commitment to shareholder value. According to Mulroy, "Our share repurchase program demonstrates our strong conviction in the business, reflects the strength of our balance sheet and free cash flow generation."

Semrush ended the quarter with cash, cash equivalents, and short-term investments of $258.5 million, increasing $27.0 million from the prior year period. This financial position provides flexibility for continued investment in AI and enterprise product development.

The company's results occur amid significant changes in digital marketing practices. According to Wagner, ChatGPT and Google's AI Mode are increasing overall search opportunity size rather than simply redistributing existing search volume. Company data shows positive correlation between ChatGPT usage and Semrush product utilization.

"The big difference is that the number of sources has grown by an order of magnitude," Wagner explained. Marketers must understand prompts used to find their products, optimize content for those prompts, and ensure message visibility across websites, YouTube videos, local reviews, and platforms like Reddit and Quora.

This expanded search ecosystem creates opportunities for comprehensive platforms like Semrush that provide tools for optimization across multiple touchpoints. Recent industry frameworks identify four distinct optimization categories: Answer Engine Optimization, Generative Engine Optimization, AI Integration Optimization, and Search Experience Optimization.

Semrush's Q2 2025 performance compares favorably to historical results and demonstrates accelerating growth in key segments. Second quarter 2024 revenue reached $91.0 million with 22% year-over-year growth, while Q2 2023 achieved $74.7 million with 19% growth. The current 20% growth rate reflects sustained momentum despite market headwinds.

ARR growth patterns show evolution from $302.4 million in Q2 2023 (20% growth) to $377.7 million in Q2 2024 (25% growth) to current $435.3 million (15% growth). While ARR growth rate has moderated, average revenue per customer continues expanding, indicating successful customer value optimization.

Dollar-based net revenue retention has varied across periods, reaching 112% in Q2 2023, 107% in Q2 2024, and 105% currently. Company leadership expects this metric to strengthen as enterprise customer mix increases and lower-retention segments represent smaller portions of the business.

The evolution demonstrates Semrush's strategic transition from volume-focused growth to value-focused expansion, prioritizing higher-quality customer relationships and sustainable unit economics over absolute customer count increases.

The earnings announcement reflects leadership changes implemented over the past year. Bill Wagner assumed the CEO role from co-founder Oleg Shchegolev, bringing experience in enterprise software and AI product development. CFO Brian Mulroy continues guiding financial strategy and resource allocation decisions.

This leadership team emphasizes disciplined growth approaches, balancing immediate revenue opportunities with long-term value creation. The strategic focus on enterprise and AI segments reflects management conviction about sustainable competitive advantages in these higher-value market segments.

Company guidance and resource allocation decisions demonstrate commitment to this strategic direction, even when it creates near-term revenue pressure from reduced investment in lower-value customer acquisition activities.

Subscribe the PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

The following terms represent the most frequently mentioned concepts throughout Semrush's Q2 2025 earnings analysis, reflecting the evolving digital marketing landscape and the company's strategic positioning.

Annual Recurring Revenue (ARR) represents the predictable revenue stream from subscription customers normalized to a yearly basis. For Semrush, ARR reached $435.3 million in Q2 2025, growing 15% year-over-year. This metric provides investors and management with clear visibility into business momentum and customer retention patterns. ARR calculations exclude one-time payments and variable usage fees, focusing on the reliable subscription foundation that drives SaaS company valuations. Strong ARR growth indicates successful customer acquisition and retention strategies, while ARR composition analysis reveals shifts toward higher-value customer segments.

Artificial Intelligence (AI) encompasses machine learning technologies integrated throughout Semrush's product portfolio to enhance marketing capabilities. The company's AI products include AI Optimization, AI Toolkit, and AI Traffic dashboard, collectively approaching $50 million in ARR by year-end 2025. These solutions address the fundamental shift in search behavior as users increasingly interact with AI-powered platforms like ChatGPT, Copilot, and Gemini. AI integration enables automated content optimization, predictive analytics, and intelligent workflow management that traditional marketing tools cannot provide. For Semrush, AI represents both a product category and a competitive differentiator in the evolving search ecosystem.

Enterprise customers represent Semrush's highest-value client segment, typically characterized by annual spending above $50,000 and complex organizational marketing needs. This segment increased 83% year-over-year in Q2 2025, demonstrating successful upmarket expansion. Enterprise customers exhibit significantly higher retention rates, with dollar-based net revenue retention consistently above 120% compared to the company average of 105%. These clients require sophisticated platform capabilities, dedicated support resources, and integration with existing enterprise software systems. The enterprise focus reflects Semrush's strategic evolution from serving individual marketers toward becoming mission-critical infrastructure for large organizations.

Search Engine Optimization (SEO) represents the practice of improving website visibility in search engine results through technical enhancements, content optimization, and authority building. Semrush's Enterprise SEO platform became the single largest contributor to company growth within one year of general availability, securing clients like Digital Ocean, HSBC, and Royal Bank of Canada. SEO encompasses traditional ranking factors while adapting to AI-powered search environments that synthesize information rather than simply ranking pages. The discipline requires continuous evolution as search algorithms advance and user behavior shifts toward conversational and voice-based queries.

Revenue growth measures the year-over-year increase in total company income, reaching 20% for Semrush in Q2 2025 with $108.9 million quarterly revenue. This growth rate reflects successful execution of cross-selling strategies, enterprise market penetration, and new product adoption. Revenue composition analysis reveals increasing contributions from higher-margin enterprise and AI products, while lower-tier segments face acquisition challenges due to elevated customer costs. Sustainable revenue growth requires balancing immediate opportunity capture with long-term customer value optimization, particularly as market dynamics shift toward AI-driven search behaviors.

Customer acquisition describes the process of attracting and converting prospects into paying subscribers, presenting increasing challenges in Semrush's lower-tier segments due to dramatic paid-search cost increases. The company strategically reduced marketing spend in segments with declining unit economics, redirecting resources toward enterprise and AI products with superior returns. Effective customer acquisition requires understanding total customer lifetime value relative to acquisition costs, channel effectiveness analysis, and segment-specific conversion optimization. For SaaS companies like Semrush, acquisition strategy must balance immediate revenue generation with sustainable unit economics.

Dollar-based net revenue retention measures the revenue expansion from existing customers over time, accounting for upgrades, downgrades, and churn within the customer base. Semrush achieved 105% retention in Q2 2025, indicating customers increased their platform spending despite some account losses. This metric provides insight into product stickiness, customer satisfaction, and expansion revenue potential. Values above 100% demonstrate organic growth from existing relationships, reducing dependence on new customer acquisition. Enterprise segments typically exhibit higher retention rates due to deeper platform integration and switching costs.

Operating margin represents the percentage of revenue remaining after deducting operating expenses, providing insight into business efficiency and profitability. Semrush achieved 11.0% non-GAAP operating margin in Q2 2025, down from 13.4% in the prior year due to strategic investments and foreign exchange impacts. Operating margin analysis reveals the balance between growth investments and immediate profitability, with higher margins indicating mature business operations. For growing SaaS companies, margin trends reflect strategic choices about market expansion, product development, and competitive positioning investments.

Free cash flow measures actual cash generation after accounting for capital expenditures and working capital changes, providing insight into business sustainability beyond accounting profits. Semrush expects 12% free cash flow margin for full-year 2025 despite negative $3.6 million in Q2 due to timing factors including tax payments and prepaid expenses. Free cash flow enables dividend payments, share repurchases, and growth investments without external financing. Strong cash generation supports Semrush's $150 million share repurchase program while maintaining flexibility for strategic acquisitions and product development.

Market positioning describes Semrush's competitive standing within the digital marketing tools landscape, strengthened by Forrester's recognition as a Leader in SEO Solutions. The company's position benefits from comprehensive platform capabilities, proprietary data assets, and early AI search optimization tools. Effective positioning requires differentiation from competitors like Ahrefs, Moz, and BrightEdge through unique value propositions and market segment focus. Semrush's enterprise and AI emphasis creates competitive moats through integration complexity and switching costs that protect customer relationships and enable premium pricing strategies.

Subscribe the PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Who: Semrush Holdings Inc. (NYSE: SEMR), CEO Bill Wagner, CFO Brian Mulroy, and approximately 116,000 paying customers globally

What: Q2 2025 financial results showing $108.9 million revenue (20% YoY growth), $435.3 million ARR (15% YoY growth), and 83% increase in customers paying $50,000+ annually, with strong adoption of AI and Enterprise products including AI Optimization and AI Toolkit

When: Results announced August 4, 2025, covering quarter ended June 30, 2025, with conference call held August 5, 2025

Where: Boston-based company with global operations across Austin, Dallas, Amsterdam, Barcelona, Belgrade, Berlin, Munich, Limassol, Prague, Warsaw, and Yerevan serving 116,000 customers worldwide

Why: Results reflect successful strategic pivot toward higher-value enterprise and AI product segments amid changing search landscape driven by artificial intelligence adoption, while facing customer acquisition challenges in lower-tier segments due to increased paid-search costs and market dynamics