Social media reaches 68.7% of global population as AI use surpasses 1 billion

Digital 2026 report reveals 5.66 billion social media users with 259 million new identities added. AI adoption exceeds 1 billion monthly users while ad spend climbs.

Digital 2026 report reveals 5.66 billion social media users with 259 million new identities added. AI adoption exceeds 1 billion monthly users while ad spend climbs.

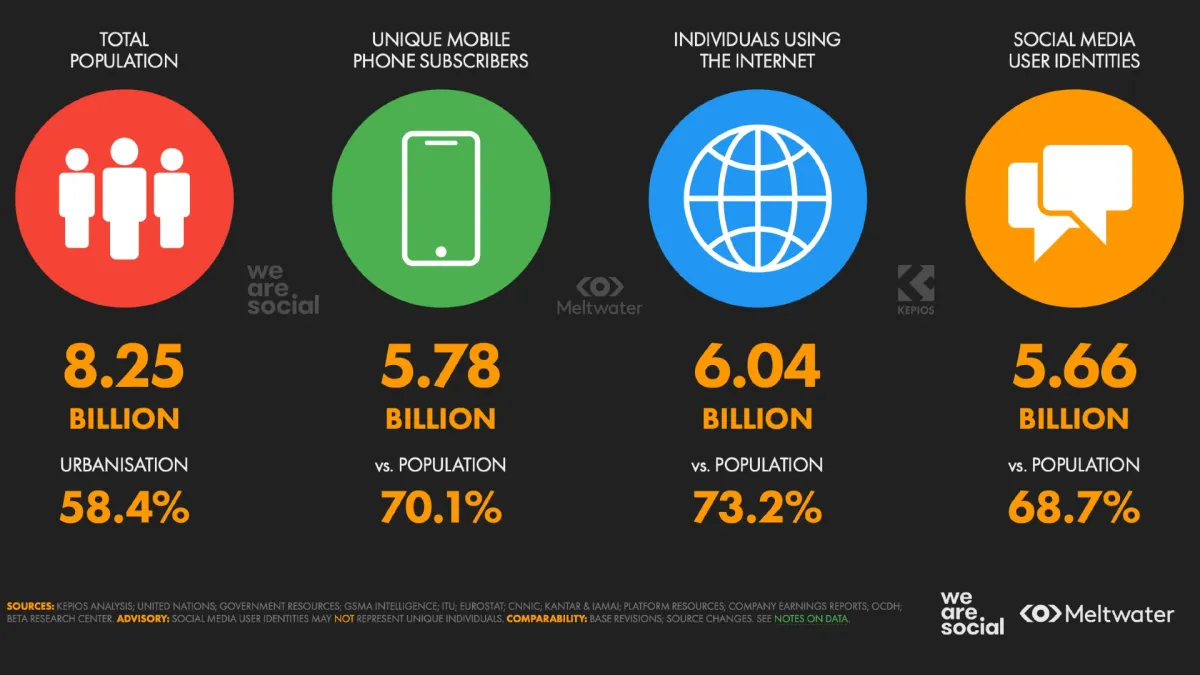

Meltwater and We Are Social released their Digital 2026 report on October 15, 2025, documenting substantial shifts in how individuals interact with digital platforms. Global social media user identities now stand at 5.66 billion, representing 68.7 percent of the world's total population. This figure marks what researchers describe as a 'supermajority', with social media users outnumbering non-users two to one.

The global total increased by 4.8 percent over the past year, adding 259 million new user identities, according to Digital 2026. This growth pattern demonstrates continued expansion despite market maturation in developed regions. The report encompasses 700 pages of data covering the entire online ecosystem, from advertising expenditure to platform-specific engagement metrics.

Internet penetration has crossed another milestone. More than 6 billion people now access the internet globally. This marks the first time internet users have exceeded this threshold, expanding the potential audience for digital communications and commerce.

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Time allocation on digital platforms reveals changing user priorities. The typical internet user spends more than 2.5 hours per day on social and video platforms. 'Filling spare time' now ranks as the second-biggest motivation for using social media, trailing only 'keeping in touch with friends and family', according to Digital 2026.

Similarweb data shows YouTube commands the largest number of active app users. The platform holds almost 50 percent more users than fifth-placed TikTok. However, engagement duration tells a different story. The typical TikTok user spends an average of 1 hour and 37 minutes per day using the platform's Android app, significantly exceeding any other social platform.

These figures underscore the distinction between reach and engagement. While YouTube attracts more total users, TikTok captures substantially more time per user. This gap has implications for advertisers seeking either broad awareness or deep engagement with specific audiences.

Women aged 16 to 24 demonstrate the highest social media consumption, spending an average of 3 hours and 40 minutes per day on social and video platforms. This represents the most intensive usage of any demographic group measured in the research. The typical social media user now engages with an average of 6.75 different platforms each month, indicating a fragmented attention landscape.

Digital 2026 highlights fundamental differences in how different generations discover brands. Social media ads now dominate as the primary discovery channel for younger consumers. For internet users aged 16 to 34, social media advertisements serve as the number one source of brand discovery.

The report finds that 34.2 percent of 16 to 24-year-olds use social media ads to learn about new products and services. Among 25 to 34-year-olds, the figure stands at 32.1 percent. This represents a clear departure from traditional discovery mechanisms.

Social media ads also rank as a strong second behind search engines for those aged 35 to 44. This positioning underlines a generational divide where older audiences continue relying on more traditional channels. The shift holds significant implications for marketing budget allocation across different target demographics.

For marketing professionals, this trend has reshaped how brands approach audience development. Traditional advertising channels continue losing ground as younger consumers increasingly depend on social platforms for product information. The data suggests this pattern will likely intensify as Generation Alpha enters peak consumption years.

Digital 2026 provides evidence that more than 1 billion people now use standalone generative AI tools every month. OpenAI's CEO reported that ChatGPT alone reached 800 million weekly users in early October 2025. This rapid adoption reshapes online behaviors, particularly in search.

GWI data shows a steady decline in the number of people who use a conventional search engine each month. Only 80 percent of online adults now use one, down from previous measurements. This erosion of traditional search usage coincides with the rise of AI-powered alternatives.

The shift toward AI tools appears to be accelerating. Nearly half of the world's online adults indicate they are excited about artificial intelligence's potential. This enthusiasm suggests adoption rates may continue climbing as capabilities expand and user interfaces improve.

AI adoption patterns vary significantly across regions and demographics, with younger, more educated populations leading usage. The technology's integration into daily workflows continues expanding beyond early adopter segments into mainstream consumer behavior.

Buy ads on PPC Land. PPC Land has standard and native ad formats via major DSPs and ad platforms like Google Ads. Via an auction CPM, you can reach industry professionals.

Marketers are on track to spend $1.16 trillion on advertising in 2025, with digital channels accounting for nearly three-quarters of that total at 74.4 percent. This represents continued growth in digital advertising's share of overall marketing budgets.

Social media advertising continues enjoying strong expansion. Global spend is projected to increase by 13.6 percent year-on-year to reach $277 billion in 2025, according to Digital 2026. This growth rate exceeds many other advertising categories.

Online retail advertising demonstrates particularly robust momentum. Marketers are on track to spend a combined $204 billion on ads on these platforms in 2025. This surge reflects the continued integration of commerce and media across digital environments.

Global advertising markets face varying growth trajectories, with economic conditions and platform innovation driving differential performance across regions. Pure-play digital advertising maintains a commanding position in overall spending patterns.

There are 5.78 billion unique mobile users globally, equating to 70.1 percent of the world's population. This mobile penetration rate underscores why mobile-optimized advertising formats have become essential for reaching contemporary audiences.

Streaming platforms now account for more than half of all time spent watching television content globally, representing 50.4 percent. This milestone marks the first time streaming has surpassed combined traditional television viewing on a worldwide basis.

Connected television advertising formats have expanded their reach significantly. Globally, YouTube's advertising formats on connected televisions now reach more than four in ten of its users each month. This represents substantial audience access for advertisers targeting living room viewing contexts.

The transition from linear to streaming television continues accelerating across most markets. Connected TV advertising has become a priority channel for brands seeking to maintain television presence while adapting to evolving consumption patterns.

"We're seeing a profound shift in how people discover brands, with more people turning to social media and AI platforms than ever before," said Alexandra Bjertnæs, Chief Strategy Officer at Meltwater. "Among younger audiences, social media ads now carry more weight than traditional search in shaping awareness and perception, while the rise of GenAI, now used by more than a billion people each month, is transforming how people find and trust information."

Bjertnæs added that "for marketers and communicators, this is an exciting opportunity to build strategies that connect with audiences in new ways and meet them where they are today."

Toby Southgate, Global Group CEO at We Are Social, emphasized the competitive landscape: "This year's report confirms the game keeps changing, creating both huge opportunities and a new challenge for marketers. A 'supermajority' of the world is now active on social media - this is where brands win or lose."

Southgate continued, "That means we have moved from a race for reach to a battle for relevance. Success in this new landscape will be defined by a deep, cultural understanding of platforms and behaviours, and the ability to earn attention with ideas that are truly worth talking about."

The data reveals advertisers must navigate increasingly complex platform ecosystems while audiences fragment across multiple services. Platform-specific strategies have become essential as users demonstrate distinct behavioral patterns across different environments.

Content authenticity concerns continue rising among users. Brand safety and content adjacency have become critical considerations for advertisers deploying campaigns across social media environments where user-generated content dominates.

The report documents continued mobile dominance in digital access. With 5.78 billion unique mobile users, smartphones serve as the primary gateway to digital services for the majority of the global population. Desktop computing retains importance for specific tasks but represents a minority of overall digital engagement.

Platform-specific behaviors differ substantially between mobile and desktop contexts. Video consumption, social media engagement, and instant messaging all show pronounced mobile preferences. Work-related activities and complex research tasks continue favoring desktop environments.

These usage patterns create challenges for advertisers seeking to maintain consistent messaging across devices. Creative formats optimized for mobile viewing often fail to translate effectively to desktop contexts, requiring platform-specific adaptations.

While global figures demonstrate substantial digital penetration, regional disparities remain significant. Developed markets show near-universal internet and social media adoption, while developing regions continue experiencing rapid growth from lower baseline levels.

Infrastructure limitations constrain adoption in some territories. Access to reliable high-speed internet remains inconsistent in regions with developing telecommunications networks. Mobile-first strategies dominate in markets where desktop computing never achieved mass adoption.

Economic factors also influence platform selection and usage patterns. Premium streaming services achieve higher penetration in wealthy markets, while advertising-supported platforms command larger audiences in regions with lower disposable incomes.

The research reveals distinct content preferences across different demographic segments. Sports content drives engagement among certain groups, while entertainment and lifestyle content attracts others. These preferences influence which platforms gain traction in specific markets.

User-generated content continues gaining ground against professionally produced material. Authenticity and relatability often prove more engaging than production quality for younger audiences evaluating content choices.

Short-form video has emerged as a dominant format across platforms. The success of TikTok has prompted competing services to emphasize similar content structures. This convergence creates challenges for platforms seeking to maintain distinct identities.

Growing awareness of data collection practices influences user behavior on social platforms. Younger users demonstrate more comfort with data sharing in exchange for personalized experiences, while older demographics express greater caution.

Regulatory frameworks continue evolving to address privacy concerns. Platform operators must navigate varying requirements across different jurisdictions, complicating global service delivery. These constraints affect targeting capabilities available to advertisers.

Transparency requirements have increased across major platforms. Users now receive more information about why specific advertisements appear in their feeds. This disclosure helps build trust but may reduce some targeting effectiveness.

Audio advertising experienced growth reaching $331 million, representing 4.7 percent of total general display advertising. Podcast consumption drives much of this expansion, with audiences demonstrating strong engagement with spoken-word content.

Music streaming services command substantial listener attention. These platforms offer advertisers access to users during moments when visual content cannot compete, such as commutes or exercise sessions.

Voice-activated devices continue their gradual integration into household environments. These systems create new touchpoints for audio advertising, though adoption rates vary significantly across markets.

The trajectory documented in Digital 2026 indicates digital channels will continue capturing larger shares of consumer attention and advertising budgets. Platform innovation shows no signs of slowing, with new services and features constantly emerging.

AI integration across digital platforms appears poised to accelerate. Tools that seemed experimental months ago are rapidly becoming standard features. This pace of change demands adaptive strategies from both platforms and advertisers.

The social media supermajority will likely grow further as remaining non-users in developing markets gain internet access. This expansion creates opportunities for platforms that successfully serve diverse global audiences with varying needs and preferences.

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Who: Meltwater, a global leader in media intelligence, and We Are Social, a socially-led creative agency, released the comprehensive Digital 2026 report analyzing global digital trends. The research examines behavior patterns of 5.66 billion social media users, 6 billion internet users, and more than 1 billion AI tool users worldwide.

What: The Digital 2026 report documents that social media users have reached a 'supermajority' representing 68.7 percent of global population, with 259 million new user identities added over the past year. The report reveals AI adoption has surpassed 1 billion monthly users, digital advertising expenditure will reach $1.16 trillion in 2025, and social media ads have become the primary brand discovery channel for consumers aged 16 to 34.

When: The Digital 2026 report was released on October 15, 2025. The data covers the 12-month period through mid-2025, with advertising projections extending through the end of 2025.

Where: The research covers global digital trends with data from 700 pages analyzing the worldwide digital ecosystem. Specific regional variations are documented across developed and developing markets, with particular attention to generational differences in platform usage and brand discovery methods across all territories with internet access.

Why: The report matters for the marketing community because it documents fundamental shifts in consumer behavior affecting advertising strategy. Social media ads now outrank traditional search for brand discovery among younger demographics, AI tools are eroding conventional search engine usage, and streaming platforms have captured the majority of television viewing time. These trends require marketers to reallocate budgets, adapt creative strategies, and develop new approaches to reaching audiences across increasingly fragmented digital environments. The data provides benchmarks for evaluating campaign performance and strategic planning in 2026.