Trade Desk shares plummet 27% despite strong Q2 performance

Trade Desk delivered robust quarterly results but faces investor skepticism over future growth trajectory and competitive pressures in programmatic advertising sector.

Trade Desk delivered robust quarterly results but faces investor skepticism over future growth trajectory and competitive pressures in programmatic advertising sector.

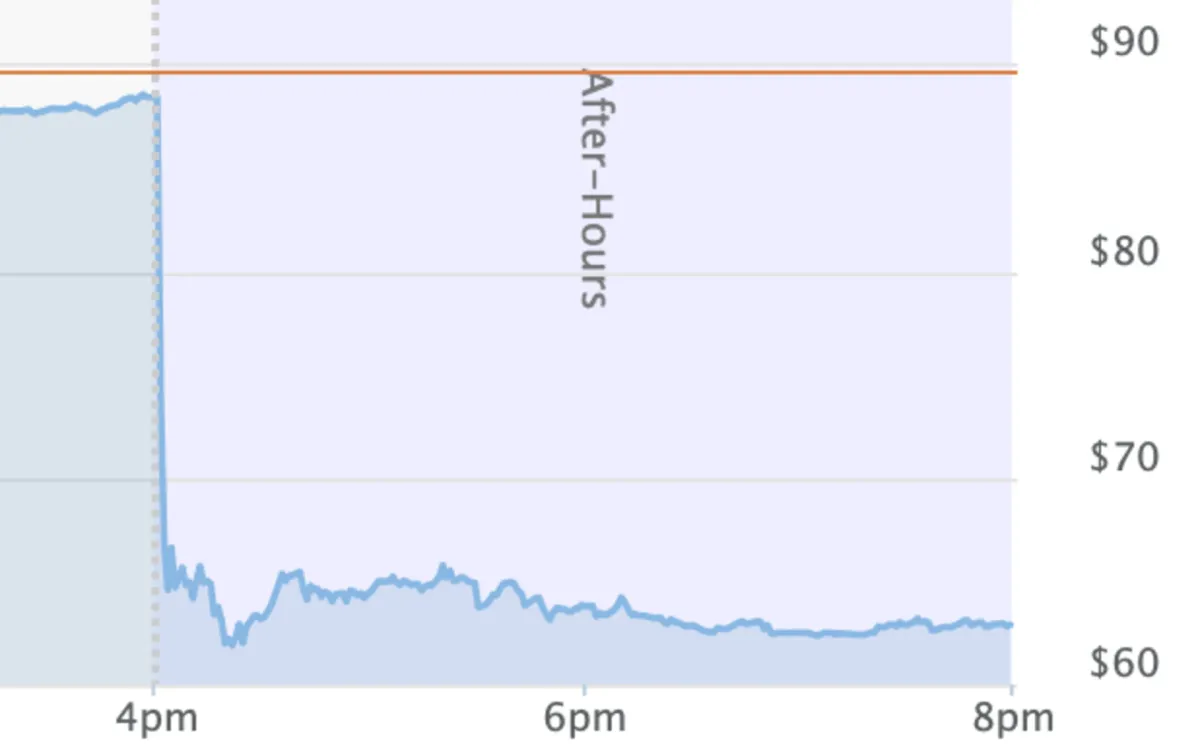

The Trade Desk reported Q2 2025 revenue of $694 million on August 7, 2025, marking 19% year-over-year growth while announcing significant leadership changes. Despite exceeding analyst expectations with earnings of $0.41 per share versus $0.34 estimates, shares plummeted 27% in after-hours trading to $64.17.

According to CEO Jeff Green, the quarter demonstrated continued momentum across key growth initiatives, particularly connected television advertising and the company's artificial intelligence-powered Kokai platform. "We again posted strong growth in the second quarter," Green stated. "Our revenue grew about 19% compared with Q2 last year, and we continue to outpace the digital advertising market."

Subscribe the PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

The company delivered adjusted EBITDA of $271 million, representing a 39% margin, while maintaining customer retention above 95% for the 11th consecutive year. Connected television remains the fastest-growing channel segment, with CTV-led video accounting for a high-40s percentage share of overall business in Q2 2025.

"CTV continues to be our fastest-growing channel with no signs of slowing down," Green emphasized during the earnings call. Notable partnerships with Disney, NBCU, Walmart, Roku, LG, Netflix expanded during the quarter as streaming platforms increasingly adopt programmatic advertising models.

According to the company's financial disclosure, operating expenses reached $448 million in Q2 2025, up 23% year-over-year, primarily driven by platform investments and team expansion. Free cash flow totaled $117 million while the company maintained $1.7 billion in cash, cash equivalents, and short-term investments.

CFO Laura Schenkein, who will transition from her role on August 21, noted geographic expansion momentum with international markets outpacing North American growth. "North America represented about 86% of spend, and international represented about 14% of spend for the quarter," Schenkein reported.

Green addressed growing investor concerns about Amazon's advertising efforts during the quarterly call, positioning The Trade Desk's independent platform as fundamentally different from walled garden approaches. "Our strategy has not changed," Green stated. "We give marketers the power and the tools to own and control their own future."

The CEO argued that Amazon's bias toward its own Prime Video inventory creates conflicts that prevent objective media buying across the open internet. "They push sponsored listings most and Prime Video after that. Neither of those compete with us," Green explained.

According to Green, Amazon's position as both advertiser competitor and cloud services provider to major brands creates additional trust complications. "Amazon already competes with many of the world's biggest advertisers in categories like retail, CPG, and cloud," he noted. "Which makes it difficult for those brands to fully trust them as a partner."

Green characterized Amazon more as a potential partner than long-term competitor, suggesting Amazon should open Prime Video to external demand sources. "If Amazon opens Prime Video to external demand, which I believe they should, we believe we'd be an amazing partner to drive demand to them," he stated.

The differentiation strategy emphasizes The Trade Desk's focus on transparency and objectivity versus closed platform approaches. "We don't have any media. And we don't grade our own homework," Green emphasized, contrasting with competitors that measure their own platform performance.

The company's AI-powered Kokai platform achieved significant milestones during Q2 2025, with over 70% of client spend now flowing through the upgraded system. Kokai integrates artificial intelligence capabilities across campaign forecasting, supply path optimization, and predictive clearing to enhance advertising effectiveness.

According to Green, early Kokai adopters demonstrated substantial performance improvements. Samsung achieved a 43% improvement in reaching target audiences for omnichannel campaigns in Europe, while Cash Rewards saw a 73% improvement in cost per acquisition for Asia campaigns. "In the aggregate, we are seeing more than a 20% improvement across key KPIs for campaigns running in Kokai," Green reported.

The platform's advanced capabilities enable clients to increase their overall Trade Desk spending more than 20% faster compared to those not using Kokai. "This is precisely what we believed was possible when we launched Kokai," Green noted. "Advertisers are getting meaningfully better returns on their ad dollars."

The company expects complete client migration to Kokai by the end of 2025. DealDesk, currently in beta testing, represents a major component of the Kokai ecosystem, leveraging AI forecasting to optimize deals between advertisers and publishers. Disney has emerged as an early DealDesk adopter, supporting the company's goal to shift 75% of ad revenue to biddable programmatic by 2027.

OpenPath, The Trade Desk's direct publisher integration system, continued expanding during Q2 2025, enabling publishers to connect directly with the platform for more transparent programmatic transactions. "A material amount of spend on our platform is now flowing through OpenPath," Green reported.

Publishers adopting OpenPath have demonstrated significant revenue improvements. The New York Post saw a 97% boost in programmatic display revenue, while Hearst Newspapers achieved a 4x improvement in fill rates since deployment.

"The New York Post is always striving for ways to simplify our connection to advertisers to help fill our ad spots more efficiently and transparently," said Amanda Gomez, SVP of revenue operations and ad technology at the New York Post. "We partnered with The Trade Desk to test OpenPath, to help achieve this goal with great success over the past year."

The company's January 2025 acquisition of Sincera strengthened supply chain transparency efforts through OpenSincera, launched in Q2 2025. The free platform provides advertising industry participants with metadata about publisher quality, enabling better decision-making across the ecosystem.

Despite strong overall performance, The Trade Desk acknowledged pressures facing major enterprise clients due to tariff policies and related economic uncertainty. "The impact of tariffs and related policies on these businesses are very real," Green stated, specifically referencing major brands in automotive and consumer packaged goods sectors.

The company's focus on large global advertisers creates exposure to these macro pressures, distinguishing Trade Desk from competitors serving primarily small and medium businesses. "This fact that we concentrate on the large ones is not generally a negative. It is almost always a positive. But just in this moment, it's negative because of how uniquely they're being affected by the tariffs and related policies," Green explained.

However, Green expressed confidence that volatile environments historically accelerate programmatic adoption due to its control, agility, and performance characteristics. "In volatile environments, these things have historically accelerated the move programmatic precisely because it comes with control, agility, and performance," he noted.

The company's Q3 2025 guidance projects revenue of at least $717 million, representing 14% year-over-year growth. Excluding benefits from U.S. political advertising in 2024, the estimated growth rate would be approximately 18% year-over-year. Adjusted EBITDA guidance for Q3 2025 is approximately $277 million.

Subscribe the PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Alex Kayyal will join as Chief Financial Officer effective August 21, 2025, replacing Laura Schenkein who served in the role for more than a decade. Kayyal brings extensive experience from Salesforce Ventures and Lightspeed Venture Partners, along with previous investment experience with The Trade Desk dating to 2014.

"Alex has been on our board, but his relationship with this company spans over a decade," Green noted. "He's also been a leader in the digital space for more than two decades." Kayyal's appointment comes as the company pursues larger enterprise opportunities and international expansion.

The leadership transition occurs during a critical period for platform adoption and market share expansion. The company recently joined the S&P 500 in July 2025, marking a historic milestone for the independent advertising technology sector.

Vivek Kundra joined as Chief Operating Officer in March 2025, while Omar Tawakil was appointed to the board of directors. "Over the years, Omar has been one of the real innovators in ad tech, whether it was founding Bluekai in 2007 or more recently founding Rembrandt," Green stated.

The dramatic stock decline despite beating earnings expectations reflects broader investor concerns about digital advertising sector dynamics. Growth deceleration from historical rates above 25% to current 19% levels signals potential maturation in programmatic advertising adoption among enterprise clients.

Privacy regulation pressures, measurement accuracy scrutiny, and intensifying competition from major technology companies create additional uncertainty about long-term growth sustainability. The timing of leadership transitions amid these challenges potentially amplified investor concerns about operational continuity.

However, the company's expanded AI creative marketplace and strategic partnerships with Netflix demonstrate continued innovation momentum despite market pressures.

The company maintains focus on return of capital through share repurchases, using $261 million in Q2 2025 with $375 million available for future repurchases. International expansion opportunities remain significant, with 88% of current spend concentrated in North America despite 60% of global advertising dollars spent outside the region.

Subscribe the PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Subscribe the PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Programmatic Advertising: An automated method of buying and selling digital advertising inventory in real-time through algorithmic bidding systems. The Trade Desk operates as a demand-side platform that enables advertisers to purchase ad space across websites, apps, and streaming services without manual negotiations. This technology-driven approach allows for precise targeting, real-time optimization, and efficient budget allocation across multiple advertising channels simultaneously, which explains why The Trade Desk achieved 19% revenue growth even amid sector challenges.

Connected TV (CTV): Television content delivered through internet-connected devices including smart TVs, streaming sticks, and gaming consoles rather than traditional cable or broadcast signals. For The Trade Desk, CTV represents the largest and fastest-growing revenue segment, reaching over 90 million households and accounting for a high-40s percentage share of business in Q2 2025. This channel enables advertisers to combine the visual impact of traditional television with the targeting precision of digital advertising, creating opportunities for more effective campaign measurement and optimization that traditional linear TV cannot provide.

Kokai Platform: The Trade Desk's artificial intelligence-powered advertising platform that integrates machine learning across all aspects of media buying, launched to replace the previous Solimar system. Kokai processes over 13 million advertising impressions per second while applying predictive algorithms for bid optimization, audience targeting, and campaign performance measurement. The platform delivered over 20% improvement across key performance indicators for campaigns, with over 70% of client spend now flowing through the system as of Q2 2025.

Walled Gardens: Closed digital advertising ecosystems controlled by major technology companies like Google, Amazon, and Meta, where these platforms own both the advertising technology and the media inventory being sold. Unlike The Trade Desk's open approach, walled gardens create potential conflicts of interest because they measure their own performance and prioritize their owned media properties. CEO Jeff Green emphasized this distinction when addressing Amazon competition, noting that walled gardens "have a vested interest in guiding spend to their owned and operated media" rather than providing objective access to the entire internet.

Supply Chain Optimization: The process of improving efficiency and transparency in digital advertising transactions between advertisers, platforms, and publishers to reduce costs and increase campaign effectiveness. The Trade Desk's OpenPath initiative and Deal Desk platform aim to reduce intermediary fees while increasing campaign performance visibility, helping advertisers achieve better return on investment. According to the earnings results, publishers adopting OpenPath saw significant improvements, with The New York Post achieving a 97% boost in programmatic display revenue.

Adjusted EBITDA: Earnings Before Interest, Taxes, Depreciation, and Amortization, excluding stock-based compensation and other non-cash expenses that don't reflect actual cash flow generation. The Trade Desk's 39% adjusted EBITDA margin in Q2 2025 demonstrates strong operational efficiency and the scalability of its software-based business model. This metric provides insight into the company's operational profitability by removing accounting items that vary significantly between companies and time periods.

Revenue Growth: The percentage increase in company sales compared to the same period in the previous year, which serves as a key indicator of business expansion and market share gains. The Trade Desk's 19% year-over-year revenue growth to $694 million demonstrates continued market share capture in the competitive digital advertising sector, though this rate represents a deceleration from historical peaks above 25% that contributed to the negative market reaction despite beating earnings expectations.

Customer Retention: The percentage of existing customers who continue using a company's services over a specific period, indicating client satisfaction and platform effectiveness. The Trade Desk's maintenance of 95%+ customer retention for 11 consecutive years demonstrates strong client satisfaction and platform value, which typically correlates with recurring revenue predictability and organic growth opportunities through increased customer spending rather than costly new customer acquisition.

Deal Desk: An AI-enabled tool currently in beta that manages and optimizes advertising deals between advertisers and publishers, providing transparency into deal performance, pacing analysis, and access to alternative inventory when deals underperform. Disney has emerged as an early adopter of Deal Desk, supporting their goal to shift 75% of ad revenue to biddable programmatic by 2027. This innovation addresses persistent inefficiencies in programmatic advertising deals that often underperform due to limited visibility into impression quality and delivery schedules.

Market Capitalization: The total dollar market value of a company's outstanding shares, calculated by multiplying share price by the number of shares outstanding. The Trade Desk's market cap of approximately $43 billion reflects investor valuation of the company's future cash flow potential, though this declined significantly following the 27% after-hours stock drop despite strong earnings results. The dramatic market reaction demonstrates how investor sentiment can diverge from fundamental performance when growth expectations aren't met.

Subscribe the PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Who: The Trade Desk Inc. (NASDAQ: TTD), a programmatic advertising platform, with CEO Jeff Green and incoming CFO Alex Kayyal replacing Laura Schenkein

What: Second quarter 2025 financial results showing $694 million revenue (19% year-over-year growth) and announcement of new Chief Financial Officer appointment, accompanied by 27% stock decline despite beating earnings expectations

When: Results announced August 7, 2025, for quarter ended June 30, 2025, with CFO transition effective August 21, 2025

Where: Headquartered in Ventura, California, with global operations across North America, Europe, and Asia Pacific markets serving international advertisers

Why: Revenue growth reflects continued adoption of programmatic advertising and connected TV expansion, while stock decline indicates investor concerns about growth deceleration, competitive pressures from Amazon, and broader sector uncertainty amid privacy regulation and measurement accuracy scrutiny