UK travel marketers bet on bigger budgets despite economic clouds

UK travel & tourism marketers predict revenue growth and budget increases for 2026, as AI search boosts organic traffic and influencer marketing remains dominant strategy.

UK travel & tourism marketers predict revenue growth and budget increases for 2026, as AI search boosts organic traffic and influencer marketing remains dominant strategy.

Impression today released its Travel & Tourism Marketing Landscape 2026 report, revealing that nearly 80% of UK travel and tourism marketers expect revenue growth in the year ahead - a striking figure given the backdrop of persistent inflation, geopolitical instability, and a search landscape reshaped by artificial intelligence.

The research, published on March 30, 2026, draws on responses from 1,000 UK marketing professionals spanning roles from middle management to C-suite, at companies generating revenue from under £1 million to over £500 million. The industries covered include airlines, hotels and accommodation, travel agencies, car rental and rail transport, destination marketing organisations, attractions, luxury travel, and cruises. Survey data was collected in October 2025. Impression, a certified B Corp performance marketing agency with offices in Nottingham, London, Manchester, and New York, is the report's author.

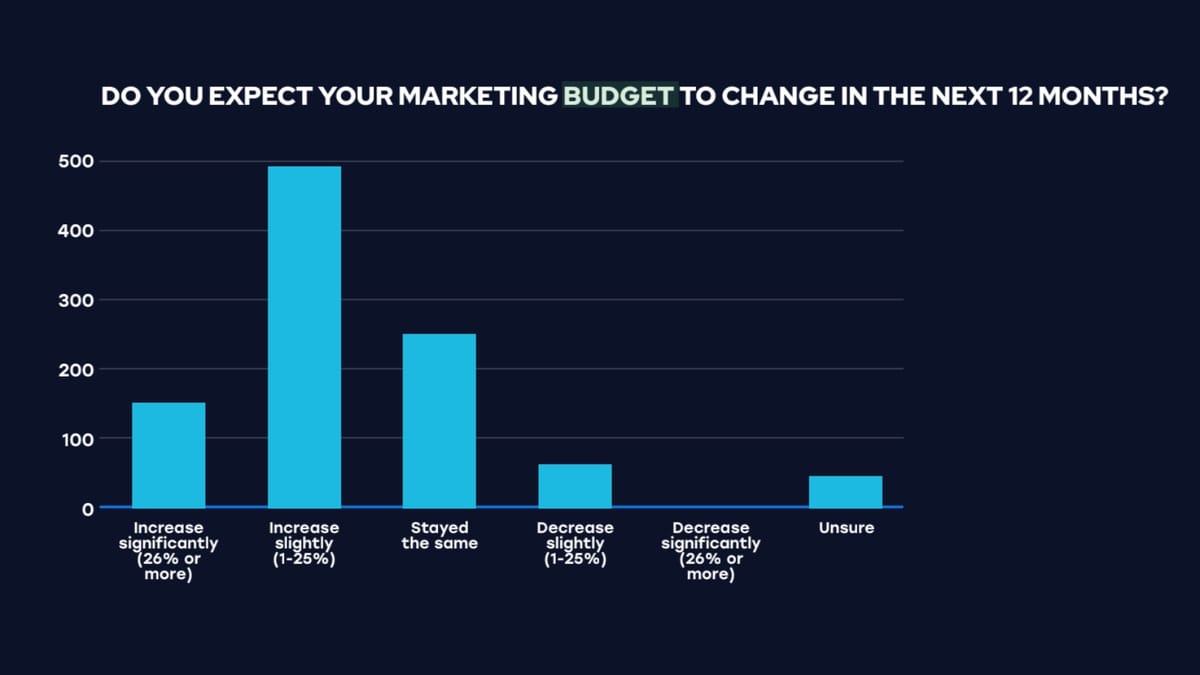

The headline finding is straightforward: 78% of respondents expect their organisation's annual revenue to increase over the next 12 months. Of those, 61% anticipate a slight increase of between 1% and 25%, while only 17% forecast a significant increase of 26% or more. Separately, 64% expect to raise their marketing budgets over the same period. Half of all respondents - 49% - said they expect marketing budgets to increase slightly (1-25%), while 25% expect budgets to remain flat. Larger businesses are more likely to see significant budget increases; smaller companies tend to be uncertain.

"Tough economic conditions and ongoing global conflicts have had a significant impact on travel patterns around the world," said Mikey Emery, Chief Commercial Officer at Impression. "Nonetheless, the travel market remains resilient, adapting to these rapidly developing circumstances."

The picture is nuanced. Marketers are optimistic, but the report cautions that optimism is not guarantee of results. Emery described high growth expectations as characteristic of the profession. "While growth is certainly on the table for the coming years, it won't be universally achieved," he noted.

Asked to identify the two biggest challenges their business faced in 2025, the majority of respondents cited economic uncertainty and inflation, closely followed by increased competition. Larger businesses showed particular susceptibility to shifts in consumer booking behaviour, while businesses of all sizes ranked economic instability and competitive pressure at the top. When asked specifically about the challenges of planning and executing marketing activity, budget constraints ranked first by a wide margin - followed by difficulty finding the right talent or skills.

That talent tension runs throughout the report. Finding the right people was the second biggest concern for Travel and Tourism marketers in 2026. It is also striking that despite growing AI adoption, 64% of travel and tourism brands still intend to expand their internal marketing teams over the next 12 months. Only 7.2% expect their teams to shrink. This is not a story of AI replacing workers; it is, according to the data, a story of AI expanding demand for skilled people.

"AI might have become a core part of how marketers work, but brands clearly recognise the ongoing importance of having a talented team to harness this technology," Emery said. "Where AI drives efficiency and scale, humans elevate creativity and effectiveness."

The report notes that 29% of respondents identified growing their teams as a key priority for success over the next 12 months. That figure stands alongside 53% who cited having a clear marketing plan as their primary success factor, and 28% who prioritised securing a larger marketing budget.

One of the report's clearer technical findings concerns booking channels. The data shows that own-website/app and online travel agencies (OTAs) dominate conversion activity across all business sizes. First-party websites - such as those operated by individual airlines or hotel chains - and platforms like Booking.com collectively account for the majority of sales. Phone and call centres, in-person branches, and third-party affiliates trail significantly.

A companion data point reinforces this: 54% of customers prefer to book via a company's own website. For marketing departments, this provides a direct justification for continued investment in mobile-first experiences, price transparency tools, and speed optimisation. Those who still book in person, the report notes, tend to have complex needs requiring high-touch service - a reminder that not all customer journeys are digital.

Perhaps the most counterintuitive finding concerns AI-powered search. Despite substantial industry concern over the impact of AI Overviews and large language models on organic traffic - a concern with documented basis in multiple studies tracking UK website traffic collapses following Google's AI search rollout - the travel sector appears to have had a different experience. According to the report, 67% of Travel and Tourism businesses say they have seen a positive impacton organic search traffic from AI search. A further 48% reported a slight increase in overall traffic.

This is a meaningful divergence from broader industry findings. Research published in February 2026 documented that Google's AI Overviews correlate with a 58% reduction in click-through rates for top-ranking pages, nearly doubling the decline documented in earlier studies from April 2025. Separate research from Ahrefs found a 34.5% reduction in organic clicks when AI Overviews appear in search results, examining 300,000 keywords. The travel sector's positive experience may reflect a specific content dynamic: travel queries tend to be experience-led and destination-specific, which LLMs and AI Overviews may surface more readily than generic informational content.

Charlie Norledge, Head of SEO Performance at Impression, contextualised the broader shift in a quote included in the report. "AI Overviews and other LLM-powered search experiences mark one of the most significant shifts in organic search in recent years. It's not all positive, as we've seen noticeable click declines for businesses that rely heavily on informational content." However, he argued that fundamentals still apply: building a strong brand, creating audience-relevant content, addressing gaps in coverage, and maintaining fast and accessible websites.

The growing importance of generative engine optimisation (GEO) - optimising content for visibility in ChatGPT, Perplexity, and other LLMs - is reflected in the channel investment data. According to the report, 27% of travel marketers outsource or plan to outsource GEO work, matching the percentage planning to outsource traditional SEO. The distinction between these two disciplines was formalised in technical guidance from Microsoft Advertising in January 2026, which detailed how AEO focuses on real-time data accuracy while GEO targets authoritative citation visibility in generative systems.

Social media retains its position as the primary engagement channel across all revenue brackets. When asked about platforms where audiences are most active, respondents placed Instagram first at 26.6%, followed by Facebook at 21.4%, TikTok at 19.3%, and YouTube at 12.3%. LinkedIn and Snapchat trail considerably. Meta's combined Instagram and Facebook presence accounts for nearly half - 48% - of all platform activity cited. TikTok's 19.3% share makes it the second-largest non-Meta platform, particularly important for reaching younger travellers.

Amy Stamper, Head of Paid Social at Impression, noted in the report that Meta's dominance reflects algorithmic advantage more than audience size alone. "Their strength isn't just audience size. Although precise targeting is harder - Meta's sophisticated algorithm rewards brands that produce diversified creative at scale." She also flagged a potential structural shift: Meta's stated pivot toward "agentic commerce," integrating AI-powered agents directly into WhatsApp and Messenger for business, could close the loop between discovery on Instagram and Facebook and conversion via chat.

Influencer marketing commands a near-majority position. According to the report, 62.5% of brands are already deploying influencer marketing as part of their strategy. A further 20% of brands not currently using influencer marketing plan to begin within the next 12 months. Only 11.6% said they tried it and found it did not work. When looking ahead, the report found that 59% of marketers plan to build or retain customer loyalty through social media, while 27% identify organic social as their primary revenue driver. Influencer marketing is expected to drive revenue for 21% of respondents.

Hannah Craig, Director, Head of PR & Social at Impression, framed the challenge in precise terms. "Travel marketing is often driven by enticing consumers with imagery that inspires. But when it comes to social media, engaging visuals won't be enough. Brands must remember that they're up against algorithms that reward unique, diversified content at scale, not just on social platforms, but increasingly within AI-powered search and discovery too."

The growth of influencer marketing as a structural channel is consistent with trends documented across European markets. Spain's digital advertising market data from early 2026 showed influencer marketing reaching €158.4 million in 2025 - a cumulative 100% increase since 2023 - with forecasts of 20% to 40% further growth projected for 2026.

The report provides a detailed breakdown of planned channel investment increases. Among the top-ranked channels for increased spending are email, SMS and app push; organic social media; content marketing; influencer marketing; and social media advertising. SEO and GEO also feature prominently in planned increases. Paid search and shopping appears comparatively lower in planned investment priorities - a pattern consistent with broader budget signals documented by PPC Land in December 2025, which noted search dollars flowing towards paid social, audio, CTV, and DOOH.

Creative investment is rising sharply. According to the report, 61.2% of respondents said investment in creative assets for performance marketing channels is increasing. Only 26.2% said it was staying the same. Immy Fox, Head of Creative at Impression, made the case for diversity: "We know that the major platforms, particularly across Social, need variety and diversity of content to perform against platform metrics; but brands still need to maintain consistency to drive those behavioural responses beyond what the platforms deliver."

The brand-versus-performance split reveals something about marketer uncertainty. Asked about their budget allocation between brand-building and performance marketing, the largest clusters of responses fell at a 40:50 or 50:50 split. The theoretical optimal - roughly 60% brand-building and 40% performance activation, as advocated in Binet and Field's "The Long and the Short of It" - was less common. The report suggests this ambiguity may reflect uncertainty about which approach is most appropriate rather than a deliberate strategic choice. Claire Elsworth, Strategy Director, was direct: "The 60:40 split isn't a rule; it's a reference point. The right balance should reflect your commercial model, purchase cycle, and category dynamics."

The technology priorities signal a sector investing in infrastructure. Asked which technologies their teams most needed to achieve goals over the next 12 months, 29% of respondents identified Customer Data Platforms (CDPs), followed by marketing automation platforms at 26%, better CRM systems at 21%, and attribution software also at 21%.

On measurement, Customer Lifetime Value (CLV) analysis, Marketing Mix Modelling (MMM), and incrementality testing emerged as the leading effectiveness measurement tools in use. Incrementality testing is growing because it allows marketers to isolate the causal impact of a channel - useful when budgets are under pressure and proving ROI is the second biggest internal challenge cited in the survey. AI and automation are planned for use in data analysis by 18.2% of respondents, content creation by 14%, marketing campaign optimisation by 12.7%, and personalisation by 12.6%.

Regarding outsourcing, the report found that travel and tourism is bucking a broader trend toward in-house consolidation - instead recognising the value of agencies. Some 43.8% of respondents plan to use a combination of agency, in-house, and freelance support to deliver marketing activity. A pure agency model was selected by 30.1%, with in-house teams at 18.9% and freelancers at 7.2%. The channels most frequently outsourced or planned for outsourcing are email, SMS and app push (30%), organic social media (25%), SEO (27%), and GEO (27%).

For performance marketers tracking the travel sector, the Impression report is a useful benchmark. The resilience of budget intentions despite economic headwinds suggests that travel brands regard marketing investment as non-discretionary - consistent with research showing how cuts compound faster than they appear to. The positive AI search sentiment among travel marketers is particularly worth noting, given how negative the picture looks in aggregate data. Travel content - destination guides, reviews, experience narratives - may be one of the few categories where LLM-powered discovery actively amplifies reach rather than suppressing it.

The finding that 64% of teams plan to grow despite AI adoption challenges assumptions that automation erodes headcount. The report positions AI as a productivity multiplier for skilled marketers rather than a replacement mechanism, a framing consistent with how Impression's own executives describe the dynamic.

Who: Impression, a 130+ employee performance marketing agency, surveyed 1,000 UK Travel & Tourism marketing professionals spanning middle management to C-suite, at companies ranging in size from under £1 million to over £500 million in annual revenue. Sectors covered include airlines, hotels, travel agencies, transport, luxury travel, cruises, and destination marketing organisations.

What: The Travel & Tourism Marketing Landscape 2026 report reveals that 78% of UK travel marketers expect revenue growth and 64% expect marketing budget increases, despite economic and geopolitical uncertainty. The report also finds that 67% have seen a positive impact on organic search traffic from AI search, 62.5% use influencer marketing, 64% plan to grow their internal teams, and that email/SMS, organic social, content, and influencer channels are the top investment priorities for the year ahead.

When: The survey was conducted in October 2025 with results published on March 30, 2026.

Where: The research covers UK-based travel and tourism businesses. Impression is headquartered in Nottingham with offices in London, Manchester, and New York.

Why: The report matters because it provides a sector-specific benchmark at a moment when broader digital marketing data - particularly around AI search - is predominantly negative for organic traffic. Travel and tourism marketers are maintaining budget confidence and hiring intentions while adapting to AI-driven discovery, influencer-led channels, and a booking landscape dominated by first-party websites and OTAs. For performance marketers and media planners, the data offers a counterpoint to generalised pessimism about the AI search impact and a signal that human talent demand is not being eroded by automation in the near term.