US out-of-home ad spend hits $4B in 2026 - but digital screens face a slowdown

US out-of-home ad spend reaches $4 billion in 2026, up 4.1% YoY. DOOH grows 14.5% but decelerates as traditional formats lag at 1.5% growth.

US out-of-home ad spend reaches $4 billion in 2026, up 4.1% YoY. DOOH grows 14.5% but decelerates as traditional formats lag at 1.5% growth.

US out-of-home advertising spend is projected to reach $4 billion in 2026, rising 4.1% year-over-year, according to new data published this month by Guideline, the media intelligence platform that captures $110 billion in annual ad spend directly from holding companies and independent agencies. The forecast arrives as the DOOH segment posts double-digit growth but shows unmistakable signs of deceleration - a dynamic that has significant implications for media planners allocating budgets across an increasingly fragmented advertising landscape.

The headline number masks a widening split within the OOH category itself. Traditional out-of-home formats are forecast to grow just 1.5% in 2026, while digital out-of-home is projected to expand by 14.5%, according to the Guideline report. That differential - nearly a ten-to-one ratio - reflects the structural shift that has been reshaping outdoor advertising since at least 2017, when digital formats accounted for only 7% of total US OOH ad spend.

The data tells a clear story of gradual displacement. In 2017, traditional OOH held a 93% share of total US outdoor advertising spend. By 2025, that figure had fallen to 80%, with digital climbing from 7% to 20% over the same period. That 2-percentage-point rise from 18% in 2024 to 20% in 2025 may look modest, but it translates into real dollars at scale. According to Guideline, 55% of total US OOH ad revenue growth between 2024 and 2025 came directly from DOOH.

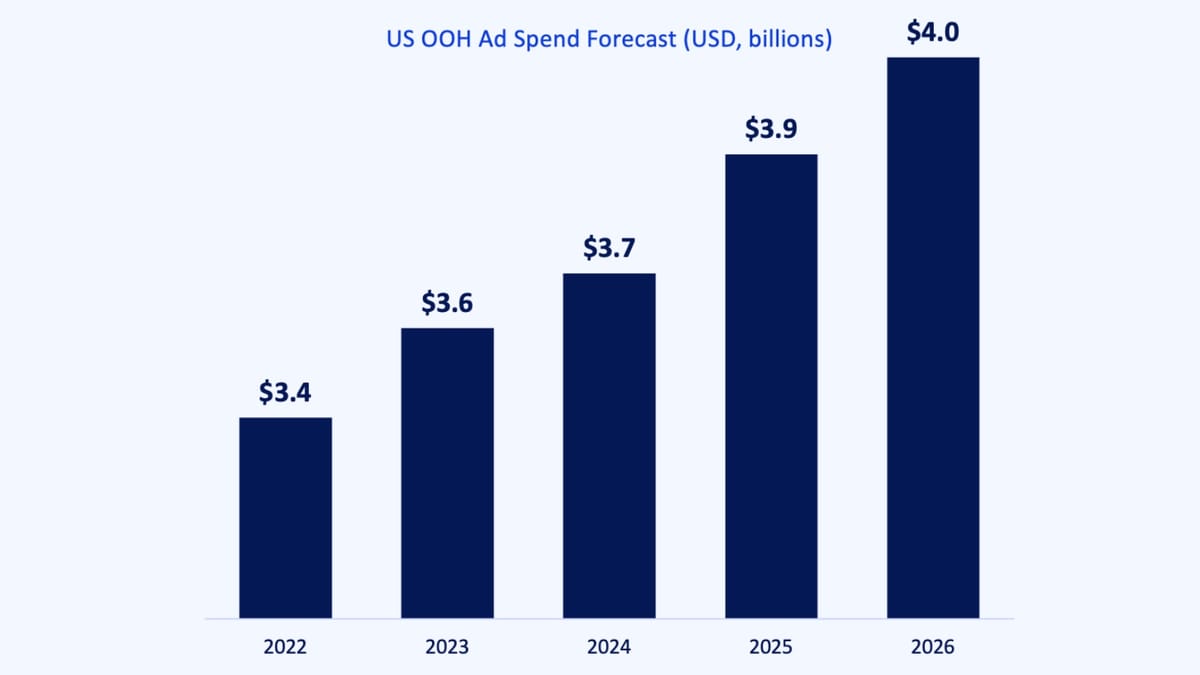

The absolute spend numbers track this trajectory closely. US OOH ad spend was $3.4 billion in 2022, rising to $3.6 billion in 2023, $3.7 billion in 2024, and $3.9 billion in 2025 before reaching the $4.0 billion projected figure for 2026. Growth has been consistent, averaging around 4% annually since 2022, according to Guideline's US data. But consistent growth at the category level has not translated into a growing share of total US media spend. OOH represented 3.1% of all US media expenditure in 2022 and had slipped to 2.7% by 2025 - a loss of 40 basis points of market share over three years despite absolute spending increases every single year.

The market-share paradox is one of the most striking findings in the Guideline report. According to the data, OOH lost $500 million in market share since 2022 and $1.3 billion since 2017, even as the category posted year-on-year revenue gains throughout that period. The reason is straightforward: the rest of the advertising market has grown faster. Performance digital formats - search, social, streaming audio, CTV, programmatic, and retail media networks - are collectively projected to expand 6.7% in 2026, according to Guideline's global ad spend forecast. Traditional formats such as radio, print, and linear television are forecast to contract 3.5% over the same period. OOH sits in the middle, growing at 4.1% and holding the unusual distinction of being the only non-pure-digital format forecast to expand at all.

That positioning matters for media buyers. PPC Land has tracked the accelerating convergence of digital and outdoor advertising as research increasingly demonstrates OOH's return on investment credentials. Research from Keen Decision Systems released in October 2025 found that out-of-home advertising achieves a marginal ROI of $7.58 per incremental dollar invested, compared with an average media type marginal ROI of $5.52 across channels.

Guideline's source-of-volume analysis identifies the specific budget flows feeding OOH growth between 2024 and 2025. Starting from a 2024 base of $3,664.64 million, digital performance channels contributed a net decrease of $104.84 million to OOH's budget pool, while television added $248.25 million, remaining channels contributed $27.02 million, and CTV added $19.40 million. A further $4.83 million came from other shifts, bringing the 2025 total to $3,859.30 million. According to Guideline, airlines, banking, and software were among the specific industry verticals that shifted budgets into OOH during this period.

The category dynamics analysis points to several sectors as both high-total-spend and high-OOH-spend growth areas. Non-health insurance, discount stores, banking, and pet food are identified as categories where OOH spend is increasing even as their overall ad spend trajectories vary. Guideline estimates that capturing fair-share of category budgets from these verticals would drive $1.3 billion in incremental OOH revenue. Broken down by opportunity, non-health insurance represents $107 million in potential incremental spend, pet food and care accounts for $41 million, and discount stores add $31 million.

The macro-economic outlook for 2026 introduces caution into some of these projections. Guideline's category risk index - which uses data science forecasting methods incorporating industry-specific economic headwinds and tailwinds - places toys and games, consumer electronics, QSR, apparel, and finance as categories forecast to grow their ad spend. Auto, insurance, non-alcoholic beverages, media, telco, and pharma are placed on the other end of the risk scale, forecast to cut spend. The report notes that without one-off tentpole events such as the World Cup or the Olympics, the overall US advertising market is forecast to grow just 2% in 2026.

The 14.5% growth forecast for digital out-of-home in 2026 is the highest segment growth rate in the OOH category, but it represents a meaningful slowdown from recent years. Guideline's data frames this explicitly: "digital's growth healthy but decelerating." The report identifies limited DOOH inventory as a structural constraint slowing market adoption. This supply-side bottleneck sits alongside a demand-side problem: retaining existing OOH budgets. According to Guideline's source-of-loss analysis for traditional OOH, competitive share shift during 2025 showed that social captured 25% of budget defections from traditional outdoor, programmatic took 23%, search drew 18%, other digital (including retail media, shortform, CTV, and digital audio) accounted for 11%, and DOOH itself captured just 1% of redirected traditional OOH budgets.

That last figure is especially telling. Only 1% of traditional OOH budgets that left the category were reinvested into digital out-of-home. DOOH's growth is coming almost entirely from incremental budgets - new money entering outdoor advertising rather than internal migration from static formats. The programmatic infrastructure buildout that has characterized the DOOH market throughout 2025 has been extensive. Broadsign acquired Place Exchange in November 2025, expanding its programmatically transactable inventory network to 1.8 million screens globally. Place Exchange subsequently launched programmatic guaranteed for DOOH within Google's Display & Video 360 in December 2025. VIOOH announced a partnership with Dolphin OOH in January 2026 providing programmatic access to more than 5,000 digital screens. Despite this infrastructure expansion, Guideline's data suggests inventory constraints continue to limit how quickly the market can absorb advertiser demand.

A separate dimension of the Guideline report examines the United States' position within global OOH markets. According to Guideline's global OOH spend data, the US accounts for 70% of the platform's global ad spend pool but only 39% of global OOH advertising. The US share of global OOH spend has hovered around approximately 40% since 2017, while the global OOH market grew from $9 billion in 2022 to $10 billion in 2025. Over that period, 60% of global markets have outpaced US OOH growth.

The country-level breakdown illustrates the dynamic. In 2022, the US represented 41% of global OOH spend in Guideline's data pool, the UK 13%, Switzerland 16%, and the remaining markets (including Canada, New Zealand, Italy, Chile, Germany, Denmark, Spain, France, and Mexico) 30%. By 2025, the US share had slipped to 39%, the UK rose to 15%, Switzerland fell to 13%, and remaining markets increased to 33%. The gradual erosion of the US share, even against a backdrop of absolute growth, points to faster OOH adoption in other markets - particularly in contexts where programmatic digital out-of-home infrastructure has expanded more rapidly relative to existing inventory.

Understanding the data's scope matters for interpreting the forecasts. According to Guideline, $110 billion in annual ad spend is captured directly from leading holding companies and independent agencies. The data contributors include major holding company networks alongside independent agencies such as Horizon, WPP Media, Dentsu, Publicis Groupe, IPG Mediabrands, Icon Media Direct, Havas Media, Assembly, OMG, Canvas Worldwide, Evergreen Trading, and RPA. Guideline positions itself as having unified three industry platforms - SQAD (now Guideline MediaTools and Guideline MediaCosts), Standard Media Index (now Guideline SMI), and a third component now operating as Guideline Lumina - into a single platform for media sellers.

The company's data collection approach, drawing directly from agency billing rather than survey-based estimation, gives its figures a different character from forecasting methodologies relying on self-reported spend or extrapolation. For the OOH category specifically, this means the 4.1% growth projection for 2026 is grounded in observed 2024-2025 spend patterns from verified agency sources rather than modeled projections built on historical trends alone. The US ad market overall is forecast to grow 4.0% in 2026 within Guideline's data pool, meaning OOH is projected to grow at roughly the same rate as total US advertising - a meaningful improvement from 2025, when OOH's 2.7% share of media spend represented erosion relative to the 3.1% share it held in 2022.

For marketing professionals constructing 2026 media plans, the Guideline data presents several specific structural considerations. OOH is the only non-pure-digital format forecast to grow in 2026, positioning it as a defensive allocation within a total media mix facing significant pressure in traditional channels. The category's demonstrated ability to attract television and CTV budgets - $248.25 million and $19.40 million respectively in 2024-to-2025 budget flow - suggests that the competitive argument for OOH is increasingly being made against video formats, not just other outdoor alternatives.

PPC Land has followed the acceleration of DOOH infrastructure throughout 2025 and into 2026, with supply-side platforms racing to connect buyers to fragmented inventory across retail, transit, and place-based environments. The Guideline forecast implies this infrastructure expansion still has to overcome the inventory constraint and budget retention challenges that the report identifies as structural headwinds. How quickly those constraints are resolved will likely determine whether DOOH's 14.5% projected growth rate in 2026 proves conservative or optimistic.

The category outlook section of the Guideline report flags macro-economic softening as a risk factor shaping category spend expectations. Several high-OOH categories - including finance and travel - are forecast to grow overall ad spend, which in theory creates upside for outdoor allocation. Others, such as auto and insurance, face headwinds. The net effect, according to Guideline's risk-indexed forecast, is a category that grows but does so against a mixed backdrop of advertiser confidence across the sectors that have historically supported OOH investment.

Who: Guideline, a media intelligence platform that unifies data from SQAD, Standard Media Index, and Lumina, capturing $110 billion in annual ad spend from holding companies and independent agencies including WPP Media, Dentsu, Publicis Groupe, Havas Media, and others.

What: Guideline published a report titled "Winning in the Digital Age: Shifting Digital Budgets, an Opportunity for DOOH," projecting US out-of-home ad spend will reach $4 billion in 2026, a 4.1% increase year-over-year. The report details DOOH growth of 14.5%, traditional OOH growth of 1.5%, a US market-share loss from 3.1% to 2.7% of total media spend since 2022, and budget flow analysis showing television channels contributed the largest share of incremental OOH investment between 2024 and 2025.

When: The data was published and shared on March 9, 2026. The underlying spend data covers calendar years 2017 through 2025, with forecasts running through 2026.

Where: The analysis covers the United States as its primary market, with a supplementary global section comparing US OOH share against the UK, Switzerland, and a group of additional markets including Canada, New Zealand, Italy, Chile, Germany, Denmark, Spain, France, and Mexico.

Why: The report addresses a structural tension in the OOH market - consistent absolute growth combined with persistent market-share erosion - and frames DOOH as the mechanism most likely to help the category compete for digital advertising budgets shifting away from performance channels. The context is a 2026 US ad market expected to grow 4.0% overall, with traditional formats declining 3.5% and digital performance formats growing 6.7%, leaving OOH as the sole non-pure-digital channel forecast to grow at all.