Why your podcast ads are missing affluent seniors and burning budget on 25-year-olds

New global study shows advertisers waste spend on narrow demographic while ignoring valuable 55+ audiences. Brand safety filters block engaged listeners across five markets.

Podcast advertisers are leaving billions on the table by concentrating spend on a narrow demographic slice while systematically excluding some of their most valuable audiences, revealing a comprehensive analysis of 50,000 podcasts across five major markets.

The Global Podcast Advertising Compass 2025, released in December 2025 through a collaboration between AdsWizz, Barometer, and NumberEight with review from Sounds Profitable, analyzed advertising patterns across the United States, United Kingdom, France, Germany, and Australia. The findings expose critical inefficiencies in how brands allocate podcast budgets, with consequences extending beyond wasted spend into fundamental questions about measurement, targeting, and suitability frameworks.

PPC Land Newsletter

Subscribe PPC Land newsletter ✉️ for similar stories like this one

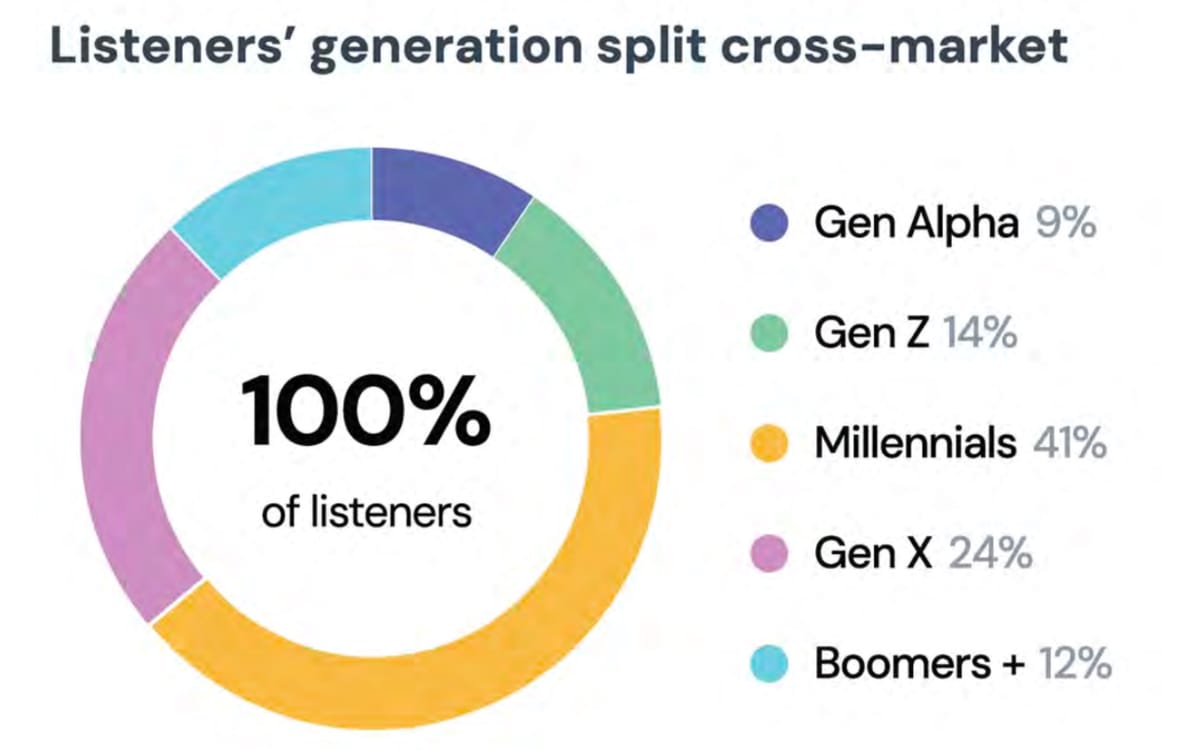

Advertisers directed 43.5% of all age-targeted impressions to the 25-34 demographic during the analysis period, representing more than double the concentration of any other age segment. The 55-64 age group received just 1.9% of targeted impressions, while listeners 65 and older captured only 0.7%, despite these demographics demonstrating strong podcast consumption patterns and commanding significantly higher household incomes than younger cohorts.

Female-targeted campaigns represented 11.4% of total impressions compared to 6.4% for male-targeted campaigns, creating nearly a 2:1 ratio. This gender skew persists despite podcast audiences showing roughly balanced gender distribution globally at 52% female and 48% male, with variations by market.

The concentration becomes more striking when examining spending patterns. The United States captured 86.6% of global podcast advertising spend while representing 80.3% of listeners, demonstrating higher monetization efficiency than other markets. Germany accounted for 4.4% of spend against 7.1% of listeners, the United Kingdom took 2.8% of spend against 4.5% of listeners, and France represented 2.6% of spend against 4.6% of listeners.

Australia demonstrated 3.6% of global listener share, though the measurement infrastructure captured limited spending data for that market. Canada showed 3.6% of advertising spend, but listener data fell outside the study's measurement scope, representing a gap in understanding one of podcasting's mature markets.

Financial Services dominated advertising verticals at 18.5% of total spend, followed by Media & Publishing at 10.1%, Travel at 9.6%, Technology at 7.1%, and Telecommunications at 6.7%. The top 10 verticals collectively represented 76% of all spending, leaving a long tail of 828+ categories fighting for the remaining quarter.

Contextual targeting drove 95.5% of campaigns with declared targeting parameters, while demographic targeting represented just 3.7% and brand suitability targeting fell below 1%. The overwhelming preference for contextual approaches reflects both privacy concerns and the relative maturity of contextual tools compared to demographic or suitability frameworks.

Among contextual targets, Automotive led IAB Tier-1 categories at 18% of targeted impressions, followed by Personal Finance at 15% and Technology & Computing at 10%. Within more granular Tier-2 categories, Insurance captured 3.1%, Banks took 2.7%, Buying and Selling Cars reached 2.4%, and Grocery Stores hit 2.3%.

The research identified significant variations in demographic composition across markets. France showed the strongest female skew at 58% of listeners, followed by the United Kingdom at 54%, while the United States tracked close to the global average. The 25-34 age segment consistently over-indexed across all analyzed markets, though France and the United Kingdom demonstrated particularly strong engagement from 35-44 listeners.

Advertise on ppc land

Buy ads on PPC Land. PPC Land has standard and native ad formats via major DSPs and ad platforms like Google Ads. Via an auction CPM, you can reach industry professionals.

Older demographics varied substantially by geography. The United States emerged as the only market where the 65+ segment significantly over-indexed, while France and the United Kingdom showed notably lower representation from listeners 55 and older. Australia and the United Kingdom recorded higher engagement from listeners under 18 and between 18-24 compared to other markets.

U.S. personas included Holiday & Travel Seniors aged 55-65+ who engage with seasonal travel content, recipes, and homeownership topics. The Multicultural Millennial Connector segment comprised females aged 25-44 from African, Asian, and Hispanic communities. Suburban Family Builders represented males aged 25-44 interested in homebuying, NFL content, and holiday shopping.

German personas featured Affluent Silver Shoppers aged 65+ responsive to holiday retail and value messaging. Gen Z Starters between 18-24 showed signals for automotive purchases, retail, fitness, and pet ownership. Midlife Style & Travel Mavens included females aged 55-64 engaged with fashion, travel, and recipe content.

France developed personas around Midlife Entertainment Enthusiasts aged 55-64 interested in film, festivals, romance television, and Christmas content. Eco-Minded Young Adults between 18-34 demonstrated sustainability concerns, grocery shopping patterns, family planning, and election engagement. Urban Gen Z Trendsetters aged 18-24 focused on fashion, fitness, summer travel, and Pride celebrations.

United Kingdom personas included Mid-life Re-Skillers aged 55-64 pursuing career changes alongside sustainability and technology interests. Family-Stage Strivers between 35-44 navigated parenting, school seasons, Black Friday shopping, and fintech adoption. Silver Pop-Culture Grandad represented males 65+ engaging with events, science fiction, gaming, and pet content.

Australian personas centered on Active Silver Foodies, males 65+ interested in recipes, wellness, seasonal events, and pets. Eco-Minded Midlife Organisers aged 55-64 balanced sustainability concerns with holiday shopping and modern family dynamics. Event & Sports Households spanning ages under 18 through 54 engaged with Boxing Day, multi-sport content, quick-service restaurants, and outdoor cooking.

Common threads emerged across markets. Senior listeners appeared active across all geographies with seasonal shopping, travel, and recipe interests. Sustainability cues repeated throughout UK, German, French, and Australian personas. Family life cycles demonstrated consistency across U.S., UK, Australian, and French audiences.

Genre preferences varied substantially by gender. True Crime over-indexed female listeners globally at 32% compared to baseline, while News and Sports over-indexed male listeners at 33% and 20% respectively. Comedy and Society & Culture provided cross-gender reach opportunities.

Market-specific gender patterns showed France delivering True Crime's highest female concentration at 37%, while News reached 42% male skew in French podcasts, the most news-focused market analyzed. The United Kingdom demonstrated Comedy's strongest female appeal at 31%, while Sports captured 30% male concentration. Germany showed True Crime at 34% female and TV & Film at 36% male, with Fiction reaching 17% male concentration. Australia recorded True Crime at 30% female, Sports at 28% male, and unusually high male engagement with Comedy at 27%.

Age patterns across categories revealed strategic opportunities. Teenagers skewed toward Sports at 35% of that demographic's listening, while Comedy peaked among 25-34 listeners at 31%. Society & Culture increased through middle age, True Crime dominated the 55-64 segment at 59%, and News led among listeners 65+ at 68%.

The United States showed Sports capturing 35% of under-18 listening, Comedy reaching 30% of 25-34 listeners, Education peaking at 28% among 45-54 listeners, True Crime hitting 60% of 55-64 listeners, and News commanding 69% of 65+ engagement.

Germany demonstrated Comedy at 21% among under-18 listeners, Business at 28% for 18-24, Society & Culture at 30% for 35-44, News at 27% for 45-54, and True Crime at 56% for 55-64. France recorded History at 28% for under-18, Sports at 57% for 18-24, News dominating 25-54 at 35-58%, and True Crime at 59-62% for 55-65+.

The United Kingdom showed Sports at 52% for under-18, Comedy at 37-40% for 18-34, Society & Culture at 27% for 35-44, News at 22% for 45-54, and True Crime at 45% for 55-64. Australia recorded Comedy and Sports around 37% for under-18, Comedy at 41% for 18-24, Comedy at 29% for 25-34, True Crime at 32-55% for 45-64, and News at 58% for 65+.

Brand suitability analysis examined 2,271 English-language podcasts, revealing how filtering tools inadvertently exclude valuable audiences. The methodology employed Barometer's four-tier classification system spanning High Risk, Medium Risk, Low Risk, and No Concern categories, combined with NumberEight's audience composition data. Statistical testing at p<0.05 confidence levels identified significant over-indexing and under-indexing patterns against baseline demographics.

Sexually Explicit content, flagged across 167 shows, reached female audiences at 37% versus a 31% baseline, though the difference fell just short of statistical significance at p=0.071. Males under-indexed at 49% versus 57% baseline with statistical significance at p=0.033. The 65+ demographic over-indexed substantially at 12% versus 7% baseline (p=0.005), while 18-24 listeners under-indexed at 13% versus 20% baseline (p=0.015).

Audiences over-indexing on sexually explicit content included Animation Enthusiasts at 60.5% versus 39.1% baseline, Beauty Shoppers at 16.8% versus 6.8%, Dating & Social Singles at 19.2% versus 9.6%, Concert & Festival Enthusiasts at 61.1% versus 39.4%, Romance Lovers at 61.1% versus 39.2%, Streaming Lovers at 68.9% versus 47.8%, and Valentine's Day Vows at 69.5% versus 47.7%, all demonstrating statistical significance below p<0.0001.

Obscenity & Profanity flags, applied to 204 shows, showed males under-indexing at 49% versus 57% baseline (p=0.027). Over-indexed audiences included Action & Adventure Fans at 73% versus 54.7%, Animation Enthusiasts at 70.6% versus 39.1%, Comedy Movie Fans at 70.6% versus 39%, Concert & Festival attendees at 71.1% versus 39.4%, Multicultural Voices at 90.2% versus 77.8%, Music Lovers at 79.9% versus 47%, Pride Party People at 14.2% versus 5%, Recipe Seekers at 25% versus 13.8%, and Streaming Lovers at 79.9% versus 47.8%, all reaching p<0.0001 significance.

Politics and Sensitive Social Issues, flagged in 145 shows, demonstrated 45-54 age under-indexing at 6% versus 12% baseline (p=0.036). Over-indexed audiences comprised AI Influencers & Higher Education Leaders at 31% versus 8.1%, Election Season Engagement at 73.8% versus 37%, Legal Services & Consumer Protection at 21.4% versus 4.9%, and Sustainability & Eco-Conscious consumers at 1.4% versus 0.3%, all exceeding p<0.02 significance thresholds.

Illegal Drugs, Tobacco, and Alcohol flags across 79 shows showed females over-indexing at 42% versus 31% baseline (p=0.033), males under-indexing at 38% versus 57% (p=0.001), and 18-24 under-indexing at 10% versus 20% (p=0.027). Over-indexed audiences included 4th of July Celebrators at 38% versus 25.2%, Foodies at 17.7% versus 2.4%, Grocery Shoppers at 20.3% versus 6.5%, Halloween Haunts at 65.8% versus 48.7%, Holiday Travelers at 19% versus 6.8%, Home Chefs at 34.2% versus 11.9%, Multicultural Voices at 89.9% versus 77.8%, New Year's Resolutions at 43% versus 15.6%, Oktoberfest at 12.7% versus 4.4%, St. Patrick's at 12.7% versus 3.4%, and Valentine's Day at 60.8% versus 47.7%, all demonstrating p<0.04 significance.

Arms & Ammunition flags, appearing in just 25 shows representing a small sample, showed Sci-Fi & Fantasy Fans at 36% versus 12.6% baseline (p=0.00042), Superhero & Comic Fans at 32% versus 8.2%, and Video Game Fans at 32% versus 8.2%, all reaching p<0.0001 significance levels.

Death, Injury, and Military Conflict flags across 113 shows demonstrated 25-34 under-indexing at 17% versus 25% baseline (p=0.047), with 65+ over-indexing at 12% versus 7% (p=0.036). Over-indexed audiences included Election Season Engagement at 58.4% versus 37%, Entry-Level Job Seekers at 9.7% versus 4.1%, and Legal Services at 14.2% versus 4.9%, all exceeding p<0.003 significance.

Crime & Human Rights Violations flags in 127 shows showed 65+ over-indexing at 13% versus 7% baseline (p=0.007). Over-indexed audiences comprised Election Season at 64.6% versus 37%, Female Empowerment at 12.6% versus 6.3%, and Legal Services at 21.3% versus 4.9%, all reaching p<0.004 significance.

Occult flags, appearing in 32 shows with small sample limitations, demonstrated Affluent Consumers at 21.9% versus 7.5% baseline, Sci-Fi & Fantasy at 40.6% versus 12.6%, Superhero & Comic at 31.3% versus 8.2%, Video Game Fans at 31.3% versus 8.2%, Music Lovers at 65.6% versus 47%, Streaming Lovers at 65.6% versus 47.8%, and Halloween Haunts at 65.6% versus 48.7%, all exceeding p<0.04 significance thresholds.

General Election flags across 82 shows showed AI Influencers & Higher Education at 34.2% versus 8.1% baseline, Election Season at 81.7% versus 37%, and Legal Services at 22% versus 4.9%, all reaching p<0.0001 significance levels.

The brand suitability findings carry significant implications for how advertisers approach content adjacency in podcasting. The research demonstrates that broad suitability filters can exclude highly engaged audiences spanning entertainment enthusiasts, culturally engaged communities, seasonal and lifestyle segments, and civically active listeners.

Overuse of categorical filters reduces audience diversity, potentially limiting reach to multicultural communities, LGBTQ+ audiences, and lower-income segments who over-index on content flagged for profanity or social issues. The data suggests brands manage safety through indirect contextual approaches rather than direct suitability blocking, as Politics notably absent from top blocked categories despite concerns about news underinvestment.

The research methodology employed a four-tier classification system applied by Barometer to 2,271 English-language podcasts, with NumberEight providing audience composition analysis. Z-tests at p<0.05 confidence levels identified statistically significant deviations from baseline demographics, which stood at 56.7% male, 30.7% female, and 10.7% gender-neutral designation.

Market-specific spending patterns revealed structural inefficiencies. The United States over-monetizes relative to listener share by approximately 6.3 percentage points, suggesting either premium pricing, higher ad loads, or more sophisticated sales infrastructure compared to other markets. Germany under-monetizes by 2.7 percentage points, the United Kingdom by 1.7 points, and France by 2.0 points against listener representation.

The vertical concentration poses additional concerns. Financial Services' 18.5% share, combined with Media & Publishing's 10.1% and Travel's 9.6%, creates dependency on three sectors representing 38.2% of total spending. Economic downturns affecting these industries could create cascading effects on podcast advertising revenues, while the 828+ long-tail categories each capturing under 0.5% of spend struggle for visibility despite representing diverse business models.

Top podcast concentration mirrors problems facing the music industry. The analysis found top-performing podcasts skew older and more female than platform averages, suggesting advertisers gravitate toward established mass-market shows rather than niche programming. This pattern risks replicating the music industry's imbalance, where monetization concentrates disproportionately among top 100 artists while long-tail creators struggle for sustainable income.

Demand concentration on small sets of premium shows creates pricing pressure, potentially inflating CPMs on popular inventory while leaving mid-tier and emerging shows undervalued. This dynamic disadvantages both advertisers seeking efficiency and creators building audiences, as measurement infrastructure and sales processes favor established players with proven track records.

The demographic concentration raises questions about strategic thinking. Affluent seniors command significantly higher household incomes than 25-34 listeners, demonstrate lower debt burdens, own homes at higher rates, and control substantial investable assets. Yet they receive approximately 1% of age-targeted advertising impressions combined across 55-64 and 65+ segments.

This disconnect between commercial value and advertising allocation suggests several possibilities. Advertisers may prioritize lifetime value calculations favoring younger audiences despite lower immediate purchasing power. Creative and messaging strategies may prove more difficult to execute for older demographics. Measurement infrastructure may provide less granular data on senior listening behaviors. Or the industry may simply operate on outdated assumptions about media consumption patterns that no longer reflect reality.

The gender targeting imbalance presents similar puzzles. Female-targeted campaigns nearly double male-targeted campaigns despite roughly balanced overall listenership. This skew may reflect advertiser preferences for categories where women make purchasing decisions, higher measured engagement rates among female podcast listeners, or creative strategies that prove more effective with female audiences.

Contextual targeting's 95.5% dominance over demographic (3.7%) and suitability (<1%) approaches indicates both technical maturity and strategic preferences. Privacy regulations limiting third-party data access have pushed advertisers toward contextual methods, while category-based targeting aligns with traditional media buying practices familiar to agencies and brands.

The relatively low adoption of demographic targeting, despite its 3.7% share, suggests either technical limitations in podcast demographic data, advertiser skepticism about accuracy, higher costs associated with demographic overlays, or strategic decisions to prioritize context over audience characteristics.

The research identified this as a critical friction point. Pure brand suitability blocking proved too blunt an instrument for podcast content, driving shifts toward contextual and genre-based filtering that provide more appropriate controls. However, this shift leaves gaps in how advertisers manage true brand safety concerns, creating conservative approaches that exclude valuable inventory.

Politics' absence from top 15 blocked categories, despite broader industry concerns about news investment, suggests brands solve for political content through indirect mechanisms. Rather than blocking political discussion directly, advertisers may avoid News categories entirely, select specific shows with editorial perspectives, or rely on contextual targeting to steer clear of partisan content.

This indirect approach creates collateral damage. Podcasts discussing policy implications of technology, healthcare system changes, economic trends, or social movements may get swept into overly broad exclusions despite containing commercially valuable audiences engaged with substantive issues relevant to brand messaging.

The market composition data demonstrates podcasting's global reach while highlighting development disparities. The United States' 80.3% listener share reflects both population scale and market maturity, with podcast consumption embedded in daily routines through commuting, exercise, household tasks, and entertainment.

Germany's 7.1% listener share positions it as Europe's largest podcast market, though monetization efficiency lags U.S. patterns. The United Kingdom's 4.5% and France's 4.6% shares show similar adoption levels with comparable monetization challenges. Australia's 3.6% share demonstrates strong per-capita adoption in a smaller population market.

Canada's presence in spending data (3.6%) without corresponding listener measurement highlights infrastructure gaps. The absence of Canadian listener data from the analysis represents either measurement limitations, partnership scope decisions, or technical challenges in capturing cross-border consumption patterns in a market sharing language and cultural ties with the United States.

The persona development methodology combined demographic data with behavioral and seasonal signals to create actionable audience segments. Unlike traditional demographic buckets, these personas integrate multiple data dimensions spanning age, gender, content preferences, shopping patterns, cultural participation, seasonal behaviors, and purchase intent signals.

This approach acknowledges that a 55-year-old German interested in sustainability behaves differently from a 55-year-old Australian focused on sports, even though traditional age-gender targeting treats them identically. The personas provide advertisers with richer targeting frameworks that move beyond basic demographics toward behavioral and psychographic segmentation.

The sustainability theme repeating across UK, German, French, and Australian personas but absent from U.S. segments reflects both cultural differences and measurement methodologies. European and Australian audiences may demonstrate stronger explicit sustainability signals through consumption, search, and engagement patterns, while U.S. sustainability interest either manifests differently or registers less clearly in available data.

Family life cycle signals appearing across U.S., UK, Australian, and French personas but showing weaker presence in German segments suggests either cultural variations in how family planning affects media consumption or differences in how measurement infrastructure captures these patterns. The consistency across most markets indicates family transitions create identifiable shifts in content preferences and shopping behaviors that advertisers can leverage.

Sports emphasis variations reflect both cultural preferences and content availability. The United States' concentration on American football, Australia's multi-sport engagement tied to Boxing Day and outdoor activities, and Europe's relative de-emphasis of sports in personas compared to entertainment and style content all mirror broader media consumption patterns beyond podcasting.

The findings arrive at a moment of substantial industry growth. Podcast advertising spending increased 26% year-over-year in Q3 2025, with nearly 1,700 brands testing the channel for the first time. However, the persistent gap between consumer engagement and advertiser investment continues expanding.

Consumers dedicate 31% of media time to audio platforms while advertisers allocate only 9% of budgets to audio advertising, creating a 22% engagement gap. This disparity has persisted despite programmatic infrastructure improvements, measurement standardization efforts, and successful case studies demonstrating podcast advertising effectiveness.

The measurement challenges contribute significantly to underinvestment. Media Mix Models historically represent audio with single spend inputs rather than granular performance metrics available for display and video formats. This creates cycles where limited investment reduces data availability, which makes attribution more difficult, which further constrains investment.

Programmatic adoption has accelerated throughout 2025, with platforms expanding automated buying capabilities and standardized transaction mechanisms. SiriusXM reported podcast advertising revenue climbing nearly 50% year-over-year in Q3 2025, while 25% of total U.S. digital audio spending transacted programmatically. These developments address scale limitations that historically kept podcast advertising manual and relationship-dependent.

Video podcast expansion adds complexity to the landscape. Edison Research began incorporating video-only consumption data into podcast rankings in 2025, affecting shows with substantial visual components. Audioboom reported more than 13% of revenue from video content in Q3 2025, with video commanding $40.74 RPM versus lower audio-only rates.

The video dimension creates both opportunities and challenges. Video enables pre-roll ads, mid-roll placements, overlay advertisements, and product placement opportunities unavailable in audio-only formats. However, it also fragments measurement, as platforms must track consumption across audio-only, video-only, and hybrid contexts while maintaining consistent reporting standards.

The contextual targeting dominance at 60% of global dimensions on AdsWizz platforms reflects privacy-first positioning aligned with regulatory evolution. GDPR, CCPA, and emerging frameworks limit third-party data usage, pushing advertisers toward contextual methods that don't rely on persistent identifiers or cross-site tracking.

This shift advantages podcasting relative to display advertising, as audio content provides rich contextual signals through host discussion, category placement, and topic analysis. Episode-level contextual targeting enables advertisers to reach specific topics within individual episodes, exceeding show-level targeting limitations while respecting privacy boundaries.

The technical infrastructure supporting these capabilities has matured substantially. iHeartMedia and Magnite launched an omnichannel audio advertising marketplace in January 2024, bringing together broadcast radio, streaming radio, and podcast assets for programmatic transactions. Identity resolution capabilities enable deduplicated reach and unified frequency control across formats.

Amazon DSP integrated SiriusXM Media inventory in September 2025, providing advertisers with programmatic access to 160 million monthly digital listeners through automated interfaces. These platform partnerships eliminate manual workflows and enable data-driven campaign execution across multiple audio formats simultaneously.

The automation trend extends beyond buying into creative production. Triton Digital launched AI-powered voice cloning in March 2025, enabling scaled host-read advertisements while maintaining creator control. The technology allows hosts to create voice samples that generate personalized advertisements in their own voice, combining programmatic efficiency with host-read authenticity.

The brand suitability challenges identified in the research require industry-wide solutions. Current frameworks borrowed from display and video advertising don't accommodate podcasting's conversational format, where hosts discuss complex topics with nuance that automated scanning tools miss or misinterpret.

Overcorrection through broad blocking excludes valuable audiences and culturally significant content. The finding that Multicultural Voices over-index at 90.2% versus 77.8% baseline on content flagged for obscenity and profanity (p<0.0001) illustrates how categorical exclusions can systematically reduce reach to diverse communities.

Similarly, Pride Party People over-indexing at 14.2% versus 5% baseline (p<0.0001) on profanity-flagged content, and Female Empowerment audiences over-indexing at 12.6% versus 6.3% (p<0.004) on crime and human rights content, demonstrate how suitability tools can inadvertently limit reach to audiences engaged with social issues and cultural movements.

The solution likely involves more sophisticated AI-driven models that interpret tone and topic at both program and episode levels, as suggested by recent platform developments. These systems must balance legitimate brand safety concerns with content nuance, distinguishing between gratuitous profanity and authentic discussion of difficult topics.

The older demographic opportunity represents perhaps the most striking finding. Advertisers leaving 55+ audiences nearly untouched despite strong consumption patterns and superior household economics suggests either systematic measurement failures, outdated strategic assumptions, or creative limitations that prevent effective messaging to senior segments.

The Holiday & Travel Seniors persona in the United States, Affluent Silver Shoppers in Germany, Midlife Entertainment Enthusiasts in France, Silver Pop-Culture Grandad in the United Kingdom, and Active Silver Foodies in Australia all demonstrate engaged, commercially valuable audiences advertisers currently ignore.

These segments control substantial wealth accumulated through decades of career earnings and asset appreciation. They demonstrate lower debt burdens than younger demographics, own homes at higher rates providing collateral for major purchases, and maintain active lifestyles with discretionary income for travel, entertainment, dining, and hobbies.

Yet they receive combined targeting representing roughly 2.6% of age-targeted impressions (1.9% for 55-64, 0.7% for 65+) compared to 43.5% directed at 25-34 alone. This allocation cannot be justified by consumption patterns, purchasing power, or engagement metrics visible in the research data.

The international expansion opportunity extends beyond the five markets analyzed. The study's scope limitations excluding regions like Latin America, Asia, Middle East, and Africa leave substantial podcast markets unmeasured and underserved. Brazil, Mexico, India, China, Japan, South Korea, UAE, and South Africa all demonstrate growing podcast adoption with local-language content ecosystems.

Measurement infrastructure development in these markets lags Western standards, creating chicken-and-egg problems where limited data constrains investment, which limits infrastructure development, which perpetuates data scarcity. Breaking these cycles requires coordinated effort among measurement providers, platforms, publishers, and advertisers to establish baseline standards.

The long-tail activation challenge affects both advertisers and creators. With 828+ verticals each capturing under 0.5% of spend, categories ranging from Recruitment to Arts & Culture to Social Media to Logistics to Non-profits struggle for visibility despite potentially strong audience engagement and commercial relevance.

Programmatic infrastructure theoretically enables long-tail activation through automated discovery and transaction mechanisms. However, the data shows concentration persisting, suggesting structural barriers beyond technology. These may include minimum spend thresholds that exclude smaller categories, agency incentive structures favoring established verticals, measurement gaps making ROI assessment difficult, or simple inertia where buyers stick with familiar categories.

The top-show concentration risk parallels music industry dynamics where top 100 artists capture disproportionate revenue share while mid-tier and emerging artists struggle for sustainable income. This pattern threatens podcasting's creator economy, potentially discouraging new entrants and reducing content diversity if monetization opportunities concentrate too heavily among established shows.

Platform responses have varied. Some emphasize programmatic access to distribute demand more efficiently across inventory. Others focus on measurement standardization to provide comparable metrics across shows. Several have launched creator tools and services designed to professionalize production and sales for mid-tier shows.

The effectiveness of these approaches remains unclear. The research data shows concentration persisting despite infrastructure improvements, suggesting deeper structural issues require addressing. These might include buyer education about long-tail value, creative services helping smaller shows develop advertiser-ready inventory, or alternative business models beyond advertising for creator sustainability.

The research methodology's statistical rigor provides confidence in findings while acknowledging limitations. The 50,000 podcast sample represents a fraction of total podcast universe, with selection processes potentially introducing bias. The five-market geographic scope excludes major regions. The English-language focus for suitability analysis misses non-English content dynamics.

The p<0.05 significance threshold for audience over-indexing and under-indexing provides reasonable confidence while risking false positives in multiple-comparison contexts. The four-tier suitability classification system reflects current industry practice but may not capture all brand safety concerns or content nuance.

These limitations don't invalidate findings but require interpreting results as indicative patterns rather than universal truths. The demographic concentration, market imbalances, and suitability challenges identified likely reflect broader industry dynamics even if specific percentages vary across different sampling methodologies.

The implications extend beyond immediate tactical adjustments. The research suggests podcasting requires fundamentally different frameworks from display and video advertising across measurement, suitability, targeting, and creative development. Attempts to force-fit existing digital advertising paradigms onto conversational audio formats create friction reducing effectiveness and limiting growth.

Building podcast-specific infrastructure requires coordinated industry effort. Measurement providers must develop methodologies capturing audio's unique consumption patterns. Suitability vendors need frameworks interpreting conversational content rather than scanning for keywords. Platforms should enable targeting based on behavioral and contextual signals rather than cookie-dependent approaches.

Advertisers and agencies must educate themselves on podcasting's distinctive characteristics rather than applying display/video mental models. Creative teams need audio-specific storytelling skills. Media planners require understanding of format differences affecting frequency, reach, and attribution.

The research arrives as podcasting transitions from niche to mainstream advertising channel. The 26% year-over-year spending growth in Q3 2025 demonstrates commercial traction. The 1,700 new brands testing the channel indicate expanding advertiser interest. The infrastructure investments by platforms signal industry commitment.

However, the persistent engagement gap, demographic concentration, market imbalances, and suitability challenges revealed in the data suggest podcasting's full commercial potential remains unrealized. Closing these gaps requires addressing both technical infrastructure limitations and strategic mindset barriers among advertisers accustomed to other media formats.

The opportunity spans multiple dimensions. Geography expansion into under-monetized markets like Germany, France, United Kingdom, and Australia. Demographic expansion into affluent seniors and male audiences. Vertical expansion across long-tail categories. Suitability framework refinement enabling brand-aligned content discovery without overcorrection.

Success requires balancing scale with diversity, activating niche alongside mass-market inventory, refining tools to fit the medium, and aligning creative to cultural context per market. The alternative risks replicating music industry's concentration dynamics, where benefits accrue disproportionately to top performers while long-tail creators struggle and mid-tier shows disappear.

The research provides roadmap for action. Measurement providers can prioritize demographic data collection for underserved segments, particularly 55+ audiences. Platforms can develop suitability frameworks interpreting conversational content nuance rather than keyword scanning. Advertisers can test messaging to affluent seniors and other under-targeted segments.

Publishers can package inventory highlighting under-activated audiences. Agencies can educate clients on demographic opportunities beyond 25-34 concentration. Industry associations can establish standards for international measurement and suitability classification.

The findings matter because they expose systemic inefficiencies costing advertisers, publishers, and platforms billions in unrealized value. They matter because overcorrection on suitability reduces reach to culturally engaged communities. They matter because geographic concentration limits podcasting's global potential.

Most importantly, they matter because the current trajectory threatens podcasting's creator economy sustainability. If monetization concentrates too heavily among top shows while long-tail struggles, content diversity suffers. If international markets remain under-monetized, non-English creators face disadvantages. If brand safety overcorrection excludes diverse voices, commercial incentives misalign with cultural value.

The path forward requires acknowledging podcasting as a distinct medium requiring purpose-built infrastructure, measurement, suitability frameworks, and creative approaches. The alternative is forcing the medium into existing digital advertising boxes, limiting effectiveness and growth while perpetuating the identified inefficiencies.

The research demonstrates both podcasting's commercial scale and its unrealized potential. The question facing advertisers, platforms, publishers, and measurement providers is whether the industry builds infrastructure supporting broad-based growth or allows concentration dynamics to narrow podcasting's commercial foundation.

PPC Land Newsletter

Subscribe PPC Land newsletter ✉️ for similar stories like this one

Who: AdsWizz, Barometer, and NumberEight, with review from Sounds Profitable, conducted the analysis. The research examined advertiser behavior, listener demographics, and brand suitability patterns across major podcast markets.

What: The Global Podcast Advertising Compass 2025 analyzed 50,000 podcasts across the United States, United Kingdom, France, Germany, and Australia, revealing that advertisers concentrate 43.5% of age-targeted impressions on 25-34 demographics while directing only 2.6% combined to listeners 55+, despite older audiences demonstrating strong consumption and superior household economics. The study identified market monetization imbalances, with the U.S. capturing 86.6% of spend against 80.3% of listeners while Germany, UK, France, and Australia under-monetize relative to audience share. Brand suitability filters inadvertently exclude valuable audiences including entertainment enthusiasts, multicultural communities, LGBTQ+ listeners, and civically engaged segments.

When: The report was released in December 2025, analyzing data across the analyzed period. The findings arrive as podcast advertising spending increased 26% year-over-year in Q3 2025, with nearly 1,700 brands testing the channel for the first time, while the persistent gap between consumer audio engagement (31% of media time) and advertiser investment (9% of budgets) creates a 22% opportunity.

Where: The research covered five major markets representing different stages of podcast adoption: the United States (86.6% of global spend, 80.3% of listeners), Germany (4.4% spend, 7.1% listeners), United Kingdom (2.8% spend, 4.5% listeners), France (2.6% spend, 4.6% listeners), and Australia (3.6% listener share with limited captured spend data). The study excluded Latin America, Asia, Middle East, and Africa, leaving substantial podcast markets unmeasured.

Why: The research matters because it exposes systemic inefficiencies costing advertisers, publishers, and platforms billions in unrealized value. Demographic concentration on 25-34 audiences ignores affluent seniors controlling substantial wealth. Geographic concentration in the U.S. leaves international markets under-monetized. Brand suitability overcorrection reduces reach to culturally engaged communities including multicultural voices (90.2% vs 77.8% baseline on profanity-flagged content), Pride Party People (14.2% vs 5% baseline), and Female Empowerment audiences (12.6% vs 6.3% baseline on crime/human rights content). The current trajectory threatens podcasting's creator economy sustainability through top-show concentration mirroring music industry imbalances, while the 22% engagement gap between consumer attention and advertiser investment represents untapped commercial potential requiring purpose-built infrastructure, measurement methodologies, and suitability frameworks designed specifically for conversational audio formats rather than borrowed from display and video advertising paradigms.

Share this article

The link has been copied!

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Great! You've successfully signed up.

Great! You've successfully signed up.

Welcome back! You've successfully signed in.

Success! You now have access to additional content.