AppsFlyer index shows AppLovin, TikTok closing gap with market leaders

AppsFlyer's 2025 Performance Index analyzed 16.2 billion installs across 88 media sources, revealing tighter competition as iOS ad spend rises significantly.

AppsFlyer's 2025 Performance Index analyzed 16.2 billion installs across 88 media sources, revealing tighter competition as iOS ad spend rises significantly.

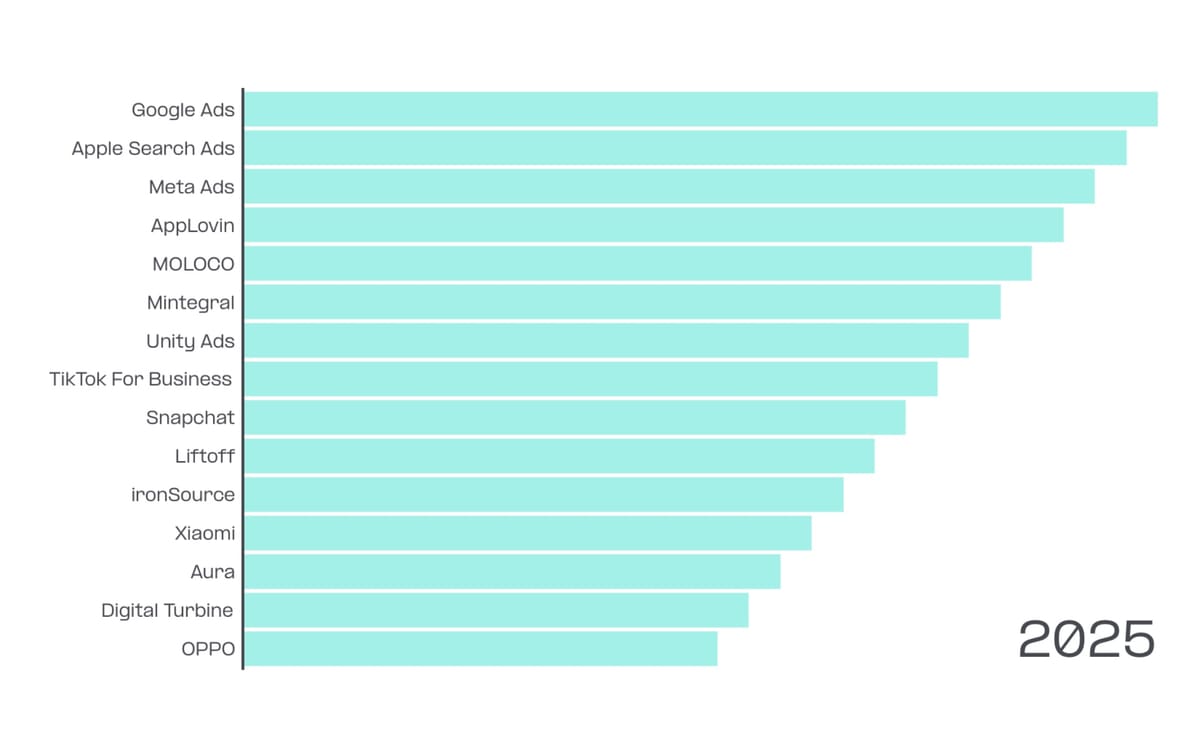

AppsFlyer released its 2025 Performance Index on December 3, 2025, revealing a mobile advertising landscape defined by intensifying competition and rising investment. The report analyzed 16.2 billion non-organic installs from 39,000 apps across 88 media sources, marking the index's tenth anniversary since establishing itself as the industry standard for mobile media performance rankings in 2015.

The data shows Google Ads and Apple Ads maintained their leadership positions, but their advantages narrowed considerably as AppLovin, Mintegral, Meta Ads, and TikTok for Business gained ground across both gaming and non-gaming categories. Overall ad spend increased in 2025, driven primarily by significant iOS gains rather than Android investments.

Subscribe PPC Land newsletter ✉️ for similar stories like this one

Budget concentration patterns emerged clearly across ranking tiers. Among the top five media sources, 60% saw year-over-year ad spend increases, according to the report. That figure climbed to 80% for sources ranked sixth through tenth before dropping sharply to just 30% among ranks 11 through 20. Most top five Android platforms gained spend, while iOS demonstrated steadier growth across middle-tier sources, reflecting more balanced investment strategies among multiple media networks.

The index introduced its first Creative Performance Index this year, analyzing which media sources delivered the strongest results across video formats including user-generated content and gameplay footage. The rankings incorporated AppsFlyer's AI-powered Creative Optimization solution, which tags gameplay mechanics and scene dynamics while identifying emotional triggers and motivations that drive engagement.

Apple Ads held the number one global power ranking for iOS gaming, but its advantage over competitors shrank substantially. The power ranking score gap between Apple and AppLovin compressed from 43% to 28% compared to the previous index. Apple ranked first in all genres except Hypercasual and Tabletop, where it placed second, with particular strength in Midcore games.

Geographically, Apple led in Greater China, the Indian Subcontinent, Japan & Korea, Latin America, the Middle East, and Southeast Asia. However, it fell to second place in both Europe and North America. Apple Ads continues to deliver the highest quality among the top five networks in the category.

AppLovin held second in the global power ranking while advancing from third to second in the volume ranking. The gap with Apple narrowed, though AppLovin still trailed significantly in quality metrics. It ranked first in Hypercasual and second in Action, Casino, Casual, Match, and Simulation genres.

AppLovin's strong Q3 2025 performance demonstrated the company's momentum, with 68% revenue growth driven by gaming advertising model improvements. AppLovin dominated Western tier-one markets, claiming first place in both power and volume rankings across North America and Europe.

Google Ads stayed at third in the power ranking, though its gap from AppLovin widened compared to the previous index. It climbed one position to fourth in the volume ranking. By genre, Google ranked third in Midcore and Action games, while regionally it placed third in North America and fourth in Southeast Asia.

Moloco maintained its fourth global power ranking, supported by strong retention scores. It ranked second in RPG and third in Casino, with regional strengths highlighted by a fourth spot in Japan & Korea and fifth in North America and Eastern Europe.

Mintegral rose three positions to fifth in the power ranking, led by a first ranking in Tabletop and third rankings in Simulation and Hypercasual. It also performed strongly in the Middle East and the Indian Subcontinent, where it ranked third overall.

Among other notable movements, adjoe surged eight spots to sixth in the power ranking, reflecting the rising strength of rewarded platforms. It posted a top-tier quality score alongside third rankings in Casual games and in Japan & Korea. Meta enhanced its AI optimization for app campaigns in November 2025, demonstrating 29% higher return on ad spend compared to volume optimization. The company gained three spots to reach seventh in the power ranking, driven by an improved retention score.

TikTok for Business advanced two spots to ninth in the power ranking thanks to a jump of three spots in the volume ranking to fifth and strong genre results in Midcore and Sports & Racing.

Buy ads on PPC Land. PPC Land has standard and native ad formats via major DSPs and ad platforms like Google Ads. Via an auction CPM, you can reach industry professionals.

Google retained its dominance across Android gaming, ranking first in the global power and volume rankings across nearly every genre and region, with only a few exceptions. While its unrivaled scale continues to drive performance, the search giant also showed solid quality, particularly in Casino, Tabletop, Puzzle, Racing, and Action games.

AppLovin came in second in the power ranking, closing the gap with Google. While still significant, the power score difference narrowed considerably thanks to a 10% improvement in its quality retention score and a rise in the number of clients. The ad network ranked second in Match, Puzzle, RPG, Sports, and Tabletop with strong quality metrics. It also claimed the first spot in Match games in Eastern Europe, posting its highest average power scores in Australia & New Zealand, Latin America, Eastern Europe, and Western Europe.

Mintegral jumped two positions to land at third in the global power ranking, driven by second positions in Action, Hypercasual, Racing, and Simulation. The network also ranked first in Eastern Europe across Action, Hypercasual, and Simulation, and secured the first Hypercasual ranking in Western Europe.

Unity Ads dropped one spot to fourth in the global power ranking, with genre positions of third in Puzzle and fourth across Action, Hypercasual, Match, Shooting, Simulation, Strategy, and Tabletop. Its strongest results came from Eastern and Western Europe, with second positions in Shooting and Casino, alongside a top-three showing in Shooting games in North America.

Meta Ads saw increased scale, rising two spots in the volume ranking to fourth, though it slipped one slot to fifth in the power ranking. The network delivered strong quality with second positions in Casino, Shooting, and Strategy, while performing particularly well in India, Southeast Asia, and Latin America.

TikTok for Business surged, climbing five spots in the power ranking to hit seventh, and one spot in the volume ranking to sixth. Rewarded platforms also gained ground, with exmox, Gamelight, Mistplay, and Freecash all improving. But adjoe shined, rising six spots in the power ranking and one in the volume ranking, to hit 12th and 10th, respectively.

Chinese OEM networks saw declines in the power ranking: Vivo dropped five positions, Oppo fell four, and Xiaomi decreased seven, largely due to lower quality scores.

Apple Ads maintained its first position in both the global power ranking and volume ranking for iOS non-gaming, leveraging unrivaled scale and solid quality. It secured the top spot across all categories and regions, with the sole exception of Australia & New Zealand, where it ranked second.

Meta Ads held the global second position in both the power ranking and volume ranking, while narrowing its power score gap with Apple. This was fueled by a significant increase in scale and strong results in Life & Culture and especially eCommerce, where it ranked second. Regionally, Meta placed second in the Indian Subcontinent and Latin America, and third in North America and Western Europe.

Google's enhanced iOS measurement tools launched in May 2025, providing streamlined App Attribution Partner integrations. TikTok for Business climbed one position to third in both the power ranking and the volume ranking, thanks to a stronger retention score and an increase in install scale. Its success was driven by a second power ranking in Finance, and third placements in Life & Culture and the Utility group.

Google Ads advanced three spots to reach fourth in the power ranking but slipped one slot to fourth in the volume ranking, as other networks grew faster despite Google's own scale increases. Its gains were driven by a two-spot climb in both Finance and eCommerce, placing it third in power within the broader Life & Culture grouping.

Snapchat rose one position to fifth in the power ranking, propelled by an improved retention score and stronger category performance. It climbed two positions in Life & Culture, and reached a second power ranking in Western Europe.

For Android non-gaming, Google Ads held the global first position in both the power ranking and volume ranking, leading across all regions and categories with just one exception: eCommerce in Eastern Europe, where it placed second. Google maintained its power score gap over its closest competitor, underscoring its unmatched scale and quality in the non-gaming space.

Meta Ads ranked second globally in both the power ranking and volume ranking, following closely across nearly every category and region. It achieved a first ranking in eCommerce in Eastern Europe and placed second in most other areas.

TikTok for Business climbed one position to third in the global power ranking and held steady at third in the volume ranking, boosted by an improved retention score and increased install scale. Meta's Q5 guidance released in October 2025 partnered with AppsFlyer for market analysis, highlighting the platforms' collaborative relationship in mobile advertising intelligence.

Google Marketing Platform, comprising DV360 and CM360, surged eight spots to fourth in the power ranking, fueled by a substantial lift in quality now among the best in class and a rise in its share of installs. Snapchat also jumped eight spots, landing at fifth in the global power ranking thanks to a significant improvement in retention quality.

In the inaugural Creative Performance Index, AppLovin took the first spot for gaming, driven by a first-place finish in gameplay as well as in creatives combining animated and real-life footage. It also ranked first in casual gaming across all four creative types, with particularly strong results in North America and Western Europe.

Moloco followed at second, powered by a first-place finish in animated creatives for midcore gaming and consistent second rankings in casual gaming across animated, animated-and-real-life, and gameplay formats. TikTok for Business came in third overall, placing third in both UGC and animated-and-real-life categories, while leading regionally with first in LATAM, second in Eastern Europe, and first in North America for UGC creatives.

Among non-gaming apps, Google Ads, mainly YouTube, led the chart at first, driven by top performance in UGC creatives. Meta Ads ranked second, with leading results in gameplay-based content, while TikTok for Business secured the third spot, excelling in creatives that combine animated and real-life footage.

Remarketing continued to expand in 2025, with a 20% year-over-year increase in both conversions and the number of apps running remarketing campaigns, according to the index. Google and Meta maintained their dominant leadership, ranking first and second in both power and volume rankings, commanding even greater market share than in user acquisition.

Non-gaming remarketing operates at a massive scale and is the main reason driving overall growth, while gaming is much smaller and remains steady. On Android non-gaming, Google Ads remained unrivaled, holding the first power ranking across nearly every category and region except Food & Drink in LATAM, where it placed third.

Meta Ads secured the second spot globally, propelled by strong results in Shopping, the largest remarketing category, and consistent second power and volume rankings across all regions. TikTok for Business climbed to third with impressive gains in Finance and Food & Drink, while holding second in Travel and Utility.

On iOS non-gaming, Meta overtook Google for the first time, leading in Shopping and ranking first in North America, APAC, and LATAM, while Google held strong in Europe and Middle East & Africa.

For gaming remarketing, Adikteev surged three spots to claim first globally on Android, driven by top rankings in Casual and Casino, and regional first in North America and second in Europe. Google Ads led iOS gaming, holding first in all regions except LATAM. RevX reached second overall, powered by first in Casino and strong results in APAC.

The 2025 index marks a decade of mobile marketing measurement since AppsFlyer launched the report in 2015. The ten-year perspective reveals how fraud protection, privacy changes including iOS 14.5, economic cycles, and the COVID-19 pandemic shaped platform performance and advertiser behavior.

AppsFlyer's November 2025 product launches introduced eight new capabilities spanning AI agents, incrementality measurement, cross-platform tracking, and data collaboration. The timing aligns with the company's positioning as a "Modern Marketing Cloud" rather than just a mobile attribution provider.

The creative performance data provides marketers with new guidance on media source selection based on specific content formats. Gaming advertising measurement standards established by IAB in June 2025 addressed transparency gaps as 80% of U.S. internet users identify as gamers, creating standardized baseline metrics across gaming environments.

Mobile app marketers face increased complexity navigating multiple attribution methodologies across platforms. The index data suggests success requires platform-specific optimization strategies rather than uniform approaches, particularly given the diverging performance patterns between iOS and Android ecosystems.

Research on NFL betting and fantasy apps conducted by AppsFlyer and Sensor Tower in November 2025 demonstrated the company's expanded role in category-specific performance analysis beyond general platform rankings.

The narrowing gaps between leading platforms and challengers indicate maturing competition that benefits advertisers through improved performance and more favorable pricing. However, the budget concentration patterns suggest smaller platforms face mounting challenges attracting investment from top-tier advertisers.

Subscribe PPC Land newsletter ✉️ for similar stories like this one

Subscribe PPC Land newsletter ✉️ for similar stories like this one

Who: AppsFlyer released the index analyzing 88 media sources including Google Ads, Apple Ads, Meta Ads, TikTok for Business, AppLovin, Mintegral, Unity Ads, Moloco, Snapchat, and numerous other platforms serving mobile app marketers across gaming and non-gaming categories.

What: The 2025 Performance Index analyzed 16.2 billion non-organic installs from 39,000 apps, introducing the first Creative Performance Index while revealing tightening competition as Google and Apple maintained leadership but AppLovin, Mintegral, Meta, and TikTok closed gaps across power and volume rankings in both iOS and Android ecosystems.

When: AppsFlyer released the report on December 3, 2025, marking the tenth anniversary of the Performance Index first launched in 2015, with data reflecting 2025 performance patterns showing 20% year-over-year remarketing growth and significant iOS ad spend increases.

Where: The index covered 11 regions including North America, Western Europe, Eastern Europe, Greater China, the Indian Subcontinent, Japan & Korea, Latin America, the Middle East, Southeast Asia, Australia & New Zealand, and Africa across up to 22 app categories spanning gaming genres and non-gaming verticals.

Why: The report matters for mobile marketers because narrowing performance gaps between platforms create more competitive pricing and improved targeting capabilities, while the Creative Index introduction provides unprecedented guidance on media source selection based on specific content formats, and budget concentration patterns reveal strategic implications for platform selection and investment allocation across the increasingly fragmented mobile advertising ecosystem.