Consumer behavior patterns shifted toward selective spending in August 2025, according to newly released data from Zeta Global's Economic Index. The AI-powered measurement system, which tracks over 245 million consumers, recorded a 0.9% monthly decline in the Economic Index Score to 67.2 on September 2, 2025, marking the fifth consecutive monthly decrease.

According to Zeta Global findings, households demonstrated rebalancing rather than wholesale retreat from spending. The August data reveals consumers maintaining forward-looking intent while reducing non-essential purchases, driven by back-to-school planning across apparel, electronics, and dormitory essentials.

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Subscribe

"Right now, consumer strength isn't about spending more, it's about spending smarter," said David A. Steinberg, Co-Founder, Chairman, and CEO of Zeta Global. The index synthesizes over 20 proprietary signals including spend, browsing, credit, and life-event indicators to reveal intent before it becomes actual spending.

Discretionary spending contracts as credit appetite wanes

Discretionary Spend Propensity dropped 5.7% month-over-month in August, extending summer's downward trend as households trimmed non-essential purchases. Credit Line Expansion Intent fell 22.8% month-over-month, representing its steepest retreat in recent months and signaling consumers are hitting pause on borrowing appetite.

The year-over-year perspective provides additional context. While Credit Line Expansion Intent declined dramatically on a monthly basis, it remained up 9% compared to August 2024, pointing to more resilient underlying trends beneath short-term volatility.

Labor market uncertainty weighs on consumer confidence, with Job Market Sentiment weakening 3.6% month-over-month. Automotive Purchase Intent declined 7.1% month-over-month, amplifying signals of pullback in big-ticket commitments across multiple sectors.

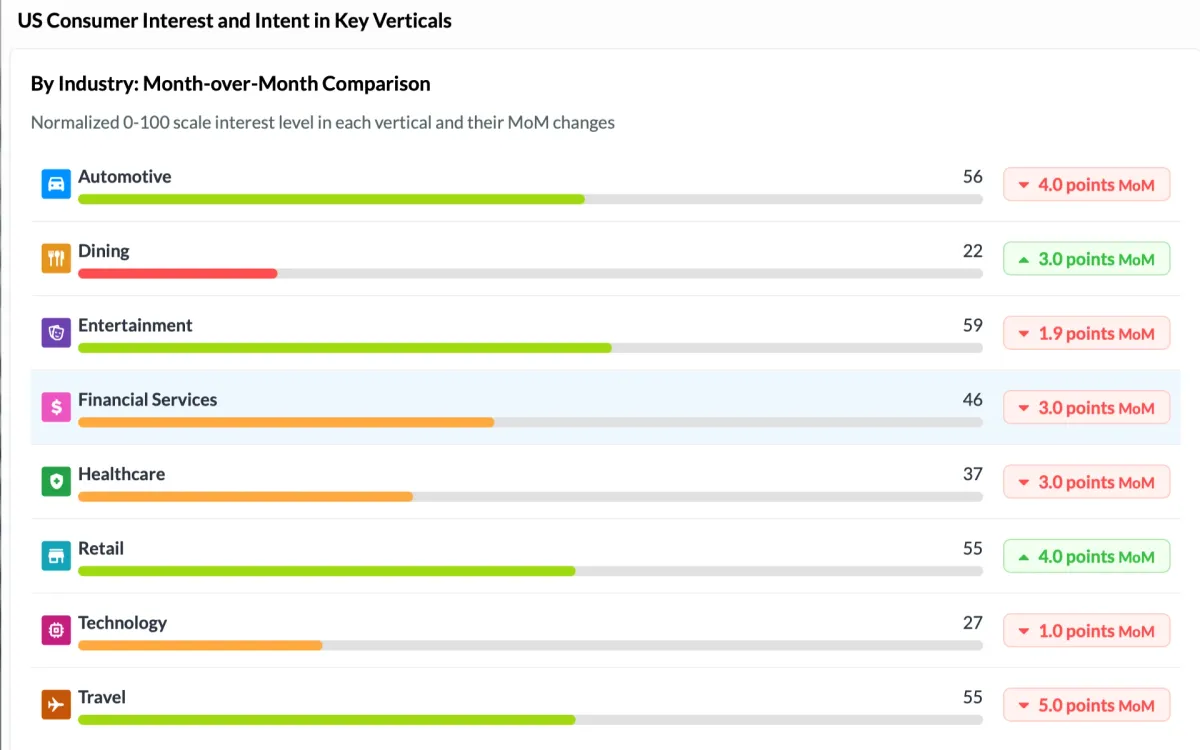

Sector-specific patterns reveal selective behavior

August sector trends demonstrate the pattern of selective consumer behavior across different industries. Retail rose 4.0 points month-over-month as in-store activity increased and consumers shifted from splurge to staple purchases. Back-to-school planning drove a clear mid-August spike in retail engagement.

Travel fell 5.0 points month-over-month, reflecting post-summer cooldown in bookings and mobility patterns. This decline aligns with seasonal expectations as summer vacation periods conclude and consumers return to regular routines.

Automotive slipped 4.0 points month-over-month, with an overall 20-point decline year-over-year as part of the larger pullback in big-ticket categories. This substantial annual decline underscores sustained caution among consumers considering major purchases.

Dining saw a 3.0-point month-over-month lift reflecting seasonal leisure spend, a category that has experienced a 13-point year-over-year increase. This positive trend suggests consumers continue prioritizing experiences and social activities despite broader spending caution.

Financial Services and Healthcare each declined 3.0 points month-over-month, indicating reduced appetite for credit products and elective care. These decreases reflect consumers' strategic postponement of discretionary financial and medical services.

Technology edged down 1.0 point month-over-month after recent bursts of consumer enthusiasm. The modest decline suggests continued interest in technology products with some cooling from peak demand periods.

Forward-looking indicators show resilience

Despite discretionary spending pullbacks, August data revealed positive offsetting trends that suggest underlying consumer stability. Time Browsing Online rose 4.7% month-over-month, consistent with digital planning and pre-holiday engagement patterns.

Out of Home Movement climbed 2.0% month-over-month, suggesting Americans continue spending in the physical world despite tightening budgets. This metric indicates sustained engagement with brick-and-mortar retail environments and service establishments.

Retail Visitation Index inched up 2.2% month-over-month, representing a modest but notable increase given declines in discretionary categories. The uptick demonstrates consumers maintain shopping behaviors while becoming more selective about purchases.

These forward-looking indicators reflect evolving consumer priorities shaped by both immediate needs and longer-term caution. The overarching result presents a consumer who is selective and thoughtful rather than impulsive, reallocating spend instead of reducing activity entirely.

Buy ads on PPC Land. PPC Land has standard and native ad formats via major DSPs and ad platforms like Google Ads. Via an auction CPM, you can reach industry professionals.

Learn more

Economic uncertainty shapes marketing strategies

The Zeta Economic Index data arrives as marketing professionals navigate changing consumer behavior patterns and economic uncertainty affects advertising spending. Previous analysis from PPC Land has documented how retail spending slowdowns impact digital advertising budgets, particularly as retail media has emerged as the fastest-growing advertising segment.

When consumer spending contracts, retailers typically adjust their marketing budgets accordingly, potentially impacting the advertising ecosystem that has benefited from robust e-commerce growth. The selective nature of current consumer behavior suggests marketers must adapt strategies to align with more deliberate purchase patterns.

The timing coincides with broader trends in digital advertising, where performance marketing basics remain challenging despite AI advances. Industry analysis reveals up to 25% of performance media spend being misallocated across digital advertising campaigns, highlighting operational challenges that compound during periods of consumer uncertainty.

Real-time measurement provides competitive advantage

Unlike survey-based gauges or lagging reports, the Zeta Economic Index synthesizes real-time consumer behavior signals to reveal intent before it becomes spending. This capability provides marketers with leading indicators rather than reactive data about completed transactions.

The system's ability to track forward-looking intent becomes particularly valuable during periods of economic uncertainty. While traditional metrics might show declining spending, the index identifies where demand is forming next, enabling marketers to capture growth opportunities while competitors wait on lagging reports.

Recent developments in consumer data collection demonstrate similar real-time capabilities, as NIQ expanded its consumer panel to include 250,000 participants for enhanced market insights. These measurement capabilities reflect industry-wide recognition that traditional survey-based research methods may not provide sufficient speed or granularity for current market conditions.

Consumer trust evolution affects data strategies

The August rebalancing patterns coincide with evolving consumer attitudes toward data collection and privacy. Research from PPC Land revealed that consumer trust crisis hits marketing as AI data use sparks privacy concerns, with 59% of consumers opposing AI training use while demanding clearer data controls.

These privacy concerns create additional complexity for marketers attempting to understand consumer behavior during uncertain economic periods. The Zeta Economic Index approach of synthesizing behavioral signals without relying on individual-level tracking may become increasingly valuable as privacy regulations tighten and consumer resistance to data collection grows.

The intersection of economic uncertainty and privacy concerns suggests successful marketing strategies must balance personalization benefits with user control and transparency requirements. Companies that can demonstrate value exchange for consumer data while respecting privacy preferences may maintain competitive advantages during economic volatility.

Technical infrastructure enables comprehensive tracking

The Zeta Economic Index infrastructure processes signals from over 245 million consumers across multiple touchpoints and channels. This scale enables detection of subtle behavioral shifts that might not appear in smaller data sets or traditional research methodologies.

The system's combination of spend data, browsing patterns, credit indicators, and life-event signals provides multidimensional views of consumer intent. This comprehensive approach addresses limitations in single-source measurement systems that may miss cross-channel behavior patterns or fail to detect early-stage intent formation.

Recent technological developments demonstrate similar comprehensive approaches, as Microsoft Clarity bridges ad gap with AI insights to provide unified views of advertising performance and behavioral analytics. These integrated measurement approaches reflect industry movement toward holistic rather than siloed data analysis.

Implications for marketing budget allocation

The August findings suggest marketing professionals should prepare for continued consumer selectivity rather than widespread spending collapse. The distinction between rebalancing and retreating implies opportunities for brands that can align messaging and targeting with evolving consumer priorities.

Categories showing resilience, such as dining and retail staples, may warrant sustained or increased marketing investment. Conversely, sectors experiencing pullbacks like automotive and financial services may benefit from strategies focused on maintaining brand awareness rather than immediate conversion pressure.

The forward-looking indicators suggesting continued digital engagement and physical world activity point to opportunities across both online and offline channels. However, the emphasis on selective behavior implies creative and targeting strategies must demonstrate clear value propositions rather than relying on impulse-driven messaging.

Methodology and data limitations

The Zeta Economic Index provides real-time consumer behavior insights but should not be considered investment advice or be relied upon to make investment decisions, according to company disclosures. The index represents consumer behavior patterns rather than predictive economic forecasting.

The Economic Stability Index score of 65.3 for Q3 2025, down 0.8% quarter-over-quarter, represents predicted stability for the entire U.S. population regarding their ability to withstand economic downturns. This measurement provides additional context for interpreting monthly behavioral changes within broader economic stability patterns.

The measurement system's reliance on digital signals and consumer touchpoints may not fully capture behavior among demographics with limited digital engagement. Additionally, the system's focus on U.S. consumers limits direct applicability to international markets where different economic conditions and consumer behaviors may prevail.

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Subscribe

Timeline

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Subscribe

PPC Land explains

Understanding the terminology used in consumer behavior analysis and economic measurement provides essential context for interpreting market trends and their implications for marketing strategies.

Consumer Behavior: The study of how individuals and households make decisions about spending their available resources on consumption-related items. In the context of the Zeta Economic Index, consumer behavior encompasses both actual purchase patterns and forward-looking intent signals that precede spending decisions. This comprehensive approach enables marketers to identify emerging trends before they fully materialize in sales data, providing competitive advantages for brands that can adapt quickly to shifting preferences.

Economic Index: A composite measurement tool that synthesizes multiple data points to provide a single score representing overall economic health or consumer activity. The Zeta Economic Index combines over 20 proprietary signals including spend, browsing, credit, and life-event indicators to create a real-time assessment of U.S. consumer behavior. Unlike traditional economic indicators that rely on lagging data, this index reveals intent patterns before they translate into actual transactions.

Discretionary Spending: Consumer expenditures on non-essential goods and services that can be postponed or eliminated during periods of financial uncertainty. The August data showed Discretionary Spend Propensity dropping 5.7% month-over-month, indicating households prioritized necessary purchases while reducing optional spending. This selective approach reflects strategic financial management rather than complete spending cessation, distinguishing current patterns from recessionary behavior.

Month-over-Month (MoM): A comparison metric that measures changes between consecutive months, providing insights into short-term trends and seasonal patterns. The August Economic Index Score declined 0.9% month-over-month, representing the fifth consecutive monthly decrease. This measurement approach enables identification of emerging trends while filtering out longer-term cyclical variations that might obscure immediate market shifts.

Marketing Strategies: Comprehensive plans developed by businesses to reach target audiences and achieve commercial objectives through various channels and tactics. Current economic uncertainty requires marketing strategies that account for selective consumer behavior, emphasizing value propositions and strategic timing. The data suggests successful strategies must balance personalization benefits with transparency requirements while adapting to changing privacy expectations.

Credit Line Expansion Intent: A forward-looking indicator measuring consumer appetite for increased borrowing capacity, reflecting confidence in future financial stability. August data showed a 22.8% month-over-month decline in Credit Line Expansion Intent, representing the steepest retreat in recent months. However, year-over-year growth of 9% suggests underlying resilience beneath short-term caution, indicating consumers remain fundamentally optimistic about longer-term prospects.

Retail Visitation Index: A measurement of consumer traffic to physical retail locations, providing insights into brick-and-mortar engagement patterns. The index increased 2.2% month-over-month in August despite declining discretionary categories, suggesting consumers maintained shopping behaviors while becoming more selective about actual purchases. This metric helps distinguish between browsing intent and conversion likelihood in physical retail environments.

Forward-Looking Indicators: Metrics that predict future consumer behavior based on current intent signals rather than completed transactions. These include Time Browsing Online (up 4.7% month-over-month) and Out of Home Movement (up 2.0% month-over-month). Such indicators provide marketers with early warning systems about changing consumer priorities, enabling proactive strategy adjustments before competitors recognize emerging trends.

Year-over-Year (YoY): A comparison metric that measures changes between the same period in consecutive years, helping identify longer-term trends while accounting for seasonal variations. While many monthly indicators showed declines, several year-over-year measurements remained positive, such as Credit Line Expansion Intent up 9% and dining category up 13 points. This perspective helps distinguish between temporary volatility and fundamental shifts in consumer behavior.

Big-Ticket Categories: High-value consumer purchases that typically require significant financial commitment and careful consideration, such as automotive and major appliances. The data showed sustained pullbacks in these categories, with Automotive Purchase Intent declining 7.1% month-over-month and automotive sector dropping 20 points year-over-year. These patterns reflect consumer caution about major financial commitments during uncertain economic periods, suggesting extended sales cycles and increased emphasis on value demonstration for expensive products.

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Subscribe

Summary

Who: Zeta Global analyzed consumer behavior patterns affecting over 245 million consumers across the United States, with implications for marketing professionals and retailers nationwide.

What: The August 2025 Zeta Economic Index declined 0.9% month-over-month to 67.2, showing consumers rebalancing spending priorities rather than wholesale retreat from purchases. Discretionary spending dropped while forward-looking indicators like online browsing and retail visitation remained stable.

When: Data covers August 2025 consumer behavior, with results announced September 2, 2025. The index shows the fifth consecutive monthly decline, with patterns emerging from July trends continuing into back-to-school season.

Where: Analysis focuses on United States consumer behavior across multiple sectors including retail, automotive, dining, travel, financial services, healthcare, and technology, with data collected nationwide through digital and physical touchpoints.

Why: Economic uncertainty, labor market concerns, and elevated caution around big-ticket purchases drove consumers toward selective spending patterns. Back-to-school needs and seasonal factors provided offsetting positive trends, while ongoing privacy concerns and marketing effectiveness challenges created additional complexity for businesses attempting to understand and respond to changing consumer priorities.

Share this article

The link has been copied!