Australian retail media set to triple US growth rates despite global consolidation trends

Australian retail media market projected to reach $3 billion by 2027 while US faces platform fragmentation hurdles.

Australian retail media market projected to reach $3 billion by 2027 while US faces platform fragmentation hurdles.

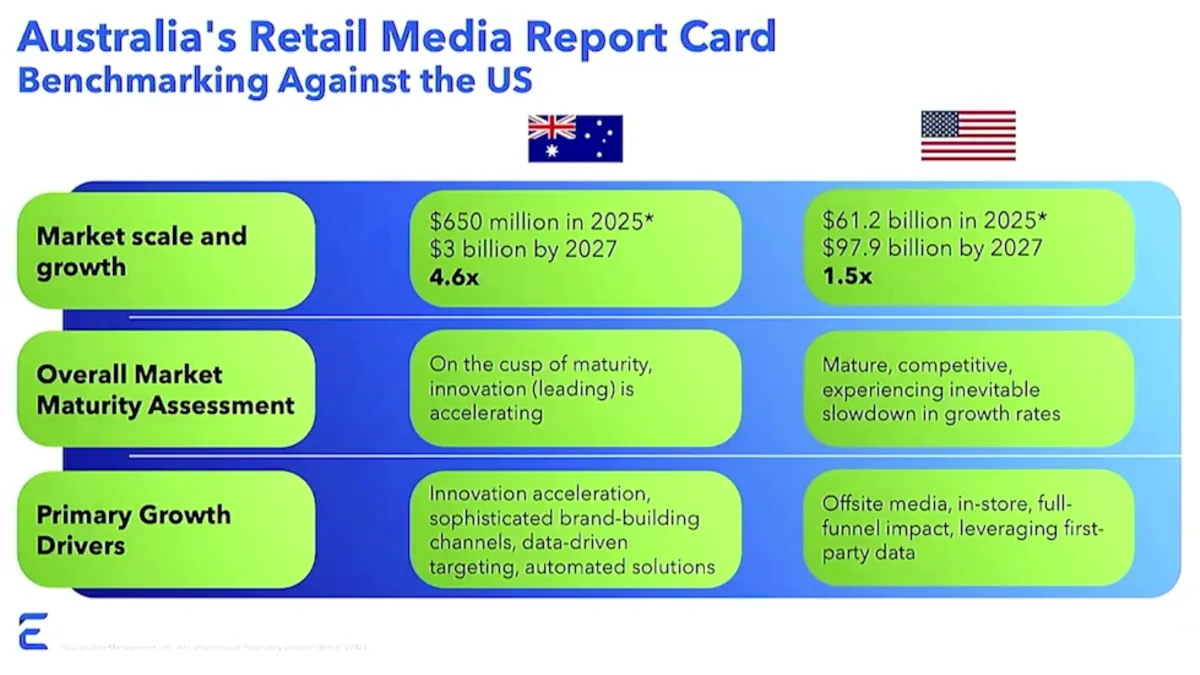

Industry analysis reveals Australia's retail media market will grow at three times the speed of the United States market through 2027, according to eMarketer data presented at the IAB Australia Commerce & Retail Media Summit on July 29, 2025. The presentation highlighted contrasting development patterns between established and emerging retail media ecosystems.

According to the analysis, Australian retail media spending is benchmarked to grow from $650 million USD in 2025 to $3 billion by 2027. This trajectory significantly outpaces the US market, which shows signs of plateauing after sustained growth periods. The presentation identified fragmentation and operational inefficiencies as primary constraints limiting US market expansion.

Subscribe the PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

The US retail media landscape demonstrates high concentration among leading platforms. According to an eMarketer study referenced in the presentation, Amazon captures approximately 77% of total retail media spending, while Walmart accounts for another 7%. This leaves more than 50 retail media networks competing for the remaining 15% of market share, a figure expected to expand to over 70 networks.

"What this is causing is disjointed interfaces, varied standards when it comes to measurement, inconsistent reporting, inability to execute cross retailer strategies and really slow budget reallocation across these RMNs," according to Adam Skinner, MD of Unified Retail Media at Epsilon, who delivered the presentation.

The fragmentation creates multiple operational challenges for advertisers. Manual processes and limited autonomy restrict self-service capabilities that advertisers increasingly expect. Inconsistent reporting standards make cross-network performance comparison difficult, while fragmented reports complicate unified ROAS analysis across retail media investments.

These challenges align with broader industry patterns documented by PPC Land's coverage of retail media standardization efforts. European markets have invested heavily in measurement standards and unified definitions to address similar fragmentation issues.

The presentation outlined advertiser expectations versus current retail media network capabilities. Advertisers seek transparency and consistent measurement, but face inconsistent reporting and user experiences. Self-service capabilities remain limited due to manual processes, while unified ROAS performance analysis encounters fragmentation difficulties.

Data quality issues persist across US retail media networks. Inaccurate, outdated, and siloed first-party data limits targeted advertising effectiveness. Privacy compliance concerns create uncertainty around ethical data usage and second-party data sharing arrangements between retailers and brands.

Australia's retail media development follows different foundational principles compared to US market evolution. The presentation emphasized Australia's strength in physical and in-store media integration, alongside diverse player emergence focused on measurement standards from initial development phases.

"Australia can lead the market globally in providing that as a benchmark, particularly in these Southeast Asian markets where in-store and physical and digital signage is already established," according to the presentation content.

The Australian market demonstrates sophisticated approaches to omni-channel integration. Retailers have developed capabilities bridging physical and digital experiences, incorporating smart shelf tags, digital screens, and mobile advertising formats. This foundation enables comprehensive customer journey optimization across touchpoints.

Australian retail media networks show advantages in data-driven targeting and automated solutions compared to their US counterparts. The presentation highlighted advanced audience-level targeting and measurement standards as key differentiators supporting accelerated growth projections.

Off-site retail media expansion drives growth across both markets, though for different reasons. US retailers shift toward off-site advertising due to inventory saturation constraints. Amazon displays advertisements on 99% of pages, creating supply limitations that prevent revenue growth through additional inventory placement.

The presentation identified that only 20% of shoppers visit retailers' owned and operated e-commerce sites in the US market. On-site traffic plateauing forces retailers to reach the remaining 80% of potential customers through off-site advertising channels. This creates opportunities for re-engaging lapsed shoppers and driving them back to owned properties.

Off-site retail media enables retailers to increase advertising revenue and margin dollars compared to on-site operations alone. The strategy creates flywheel effects including increased in-store visits, higher average order values, and surges in foot traffic to physical brick-and-mortar locations.

Connected television advertising represents another significant trend highlighted in the analysis. CTV adoption accelerates as linear television viewership plateaus and declines. The channel bridges brand awareness objectives with measured performance capabilities, aligning with retail media principles around audience targeting versus broad reach advertising.

Social commerce expansion creates additional opportunities through shoppable experiences on social platforms. This trend intersects with off-site retail media strategies, extending retailer reach into social environments where consumers discover and evaluate products.

The presentation emphasized publishers' mindset adoption among retailers seeking advertising revenue diversification. Successful retail media networks invest in self-service platforms, robust measurement capabilities, and innovative advertising products to attract and retain advertiser partnerships.

Innovation acceleration remains a primary growth driver for Australian retail media, alongside sophisticated brand-building channels and data-driven targeting solutions. The market's maturity trajectory positions it advantageously for sustained expansion compared to more established but operationally constrained markets.

Retailers across both markets face pressure to develop capabilities for data portability as off-site advertising becomes increasingly important. This technical requirement enables effective audience extension beyond owned and operated properties while maintaining targeting precision and measurement accuracy.

Australian retail media's competitive positioning benefits from lessons learned observing US market development. Early investment in standardization, measurement frameworks, and omni-channel integration creates foundations for sustainable growth without encountering fragmentation challenges that constrain more mature markets.

The analysis suggests Australian retail media networks can achieve market leadership through strategic focus on transparency, automated solutions, and comprehensive measurement standards. These capabilities address persistent challenges identified in established markets while supporting advertiser demands for unified campaign management and cross-platform performance analysis.

Subscribe the PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Subscribe the PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Retail Media Networks (RMNs): Advertising platforms operated by retailers that leverage first-party customer data to enable brands to place targeted advertisements across owned digital properties and external channels. These networks have become central to modern digital advertising strategies as they provide access to high-intent shoppers at crucial decision-making moments. The networks generate revenue by monetizing their customer data and digital real estate while offering brands precise targeting capabilities that traditional advertising channels cannot match.

Off-site Advertising: Marketing campaigns that extend beyond retailers' owned and operated websites and applications to reach audiences across third-party platforms using retailer data for targeting. This approach addresses inventory limitations on owned properties while expanding reach to customers who may not regularly visit retailer websites. Off-site strategies have become essential as on-site traffic plateaus and retailers seek to re-engage lapsed customers through display, social, connected television, and digital out-of-home advertising channels.

Fragmentation: The division of retail media spending across numerous independent platforms, each with distinct interfaces, measurement standards, and operational requirements. This market structure creates operational inefficiencies for advertisers managing campaigns across multiple networks, leading to disjointed reporting, inconsistent measurement methodologies, and slow budget reallocation processes. Fragmentation particularly affects markets like the United States, where dozens of retail media networks compete for advertiser attention and spending.

First-party Data: Customer information collected directly by retailers through their owned channels, including purchase history, browsing behavior, demographic details, and engagement patterns. This data forms the foundation of retail media targeting capabilities, enabling precise audience segmentation and personalized advertising experiences. The value of first-party data has increased significantly as third-party cookies phase out, making retailer-owned customer insights increasingly valuable for brands seeking to reach specific consumer segments.

Omni-channel Integration: The seamless connection of advertising experiences across online, mobile, in-store, and other customer touchpoints to create unified brand interactions throughout the purchase journey. Australian retail media networks have particularly excelled in this area, developing sophisticated systems that bridge physical store experiences with digital advertising campaigns. This integration enables retailers to optimize customer experiences across all interaction points while providing comprehensive measurement and attribution capabilities.

Measurement Standards: Unified frameworks for evaluating retail media campaign performance, including standardized metrics for click-through rates, conversion rates, return on advertising spend, and attribution methodologies. The development of consistent measurement approaches addresses industry fragmentation challenges and enables advertisers to compare performance across different retail media networks. Organizations like IAB Europe have invested heavily in creating these standards to facilitate market growth and advertiser confidence.

Sponsored Products: Native advertising formats that promote individual products within retail environments, typically appearing in search results and product pages without requiring additional creative assets. These advertisements automatically pull product images, titles, and details from existing listings, creating seamless integration with organic content. Sponsored Products have emerged as the primary growth driver for retail media spending, particularly in European markets where they contributed to 22.1% sector growth in 2024.

Connected Television (CTV): Streaming television advertising that bridges brand awareness objectives with performance marketing capabilities, enabling retailers to reach audiences through video content while maintaining measurement and targeting precision. CTV adoption accelerates as linear television viewership declines, providing retail media networks with opportunities to extend their reach beyond traditional digital channels. This format aligns with retail media principles by offering audience-based targeting rather than broad demographic approaches.

Programmatic Advertising: Automated buying and selling of advertising inventory through real-time bidding systems that enable dynamic pricing and audience targeting. Recent developments in retail media have introduced programmatic capabilities to sponsored product advertising, addressing operational challenges that previously required manual campaign management. This automation enables better yield optimization for retailers while providing advertisers with flexible, data-driven bidding options that reflect real-time market conditions.

Data Portability: Technical capabilities that enable retailers to extend their first-party data insights across external advertising channels while maintaining targeting effectiveness and measurement accuracy. This functionality becomes crucial as retailers expand into off-site advertising strategies, requiring sophisticated systems to activate audience segments beyond owned properties. Data portability solutions address privacy requirements while enabling retailers to monetize their customer insights across broader advertising ecosystems.

Subscribe the PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Who: Adam Skinner, MD of Unified Retail Media at Epsilon, presented analysis comparing Australian and US retail media markets at the IAB Australia Commerce & Retail Media Summit. The presentation audience included industry professionals from retail media networks, advertisers, and agencies.

What: Analysis revealing Australian retail media market projected to grow three times faster than the US market, reaching $3 billion by 2027 compared to current US plateauing. The presentation highlighted fragmentation challenges constraining US growth versus Australia's strategic advantages in omni-channel integration and measurement standards.

When: The presentation occurred on July 29, 2025, at the IAB Australia Commerce & Retail Media Summit, referencing eMarketer data projecting growth through 2027 and industry trends observed through 2024-2025.

Where: The analysis focused on US and Australian retail media markets, with additional context from European standardization efforts and Southeast Asian market opportunities for Australian networks.

Why: The analysis addresses industry needs for understanding regional retail media development patterns, identifying growth opportunities, and recognizing operational challenges that influence market expansion rates and competitive positioning strategies.