Drowning in data: why U.S. advertisers can't trust their own measurement

CIMM and 4As today released a study of 197 marketers showing advertiser measurement confidence lags capability across TV and video, with 43% citing cross-platform gaps.

CIMM and 4As today released a study of 197 marketers showing advertiser measurement confidence lags capability across TV and video, with 43% citing cross-platform gaps.

The Coalition for Innovative Media Measurement (CIMM) and the American Association of Advertising Agencies (4As) today released the findings of a major joint study showing that U.S. advertisers, despite having access to more measurement data than at any previous point, are struggling to trust or act on what that data tells them. The report, titled The Paradox of Plenty: Advertisers' Perspectives on the State of Measurement, was published on March 5, 2026, and is based on a quantitative survey of 197 senior marketers and 16 in-depth executive interviews. It was co-sponsored by Kochava, Nielsen, and TechEdge, and authored by Sarah Mansfield, Alice Sylvester, and Leslie Wood.

The study's central finding is blunt. According to the report, confidence in media and marketing measurement has not advanced at the same pace as measurement capability itself. The sharpest pain point, the authors conclude, is not skepticism about data accuracy. Instead, executives are overwhelmed with the task of prioritizing data inputs, linking disparate data across different sources, and harmonizing definitions across "black box" metrics - leading to a crisis of confidence despite the proliferation of measurement resources.

The full report, which runs to more than 50 pages, is available exclusively to members of CIMM and the 4As. The executive summary is publicly accessible.

The industry, according to the report, has spent the past decade building formidable infrastructure. Advertisers have integrated first-party data with second- and third-party sources, layered in identity graphs, adopted advanced analytics, and invested heavily in measurement solutions spanning performance, attribution, brand impact, attention, and verification. By most external measures, the industry has never been more data-rich.

Yet data richness has not translated into decision confidence. The authors describe an environment in which media fragmentation, platform-specific metrics, incompatible identity systems, and mixed methodologies have become the norm. Advertisers can optimize continuously, the report notes, yet struggle to explain, defend, or unify results with confidence. What they lack is certainty: certainty that the numbers align across systems, certainty that modeled outputs reflect reality, and certainty that they can confidently represent outcomes to internal stakeholders such as finance teams and executive leadership.

One participant, a gaming executive, expressed the problem with particular directness in the qualitative interviews: "We're drowning in dashboards. We don't need another report. We need a single version of reality. Everything is technically measurable, but none of it lines up without a lot of manual reconciliation."

This finding echoes a pattern documented across the industry throughout 2025. A separate TransUnion and EMARKETER study released in October 2025 found that 54.1% of marketing professionals reported no change in measurement confidence year-over-year, while 14.3% said confidence had actually declined - even as tool sophistication increased.

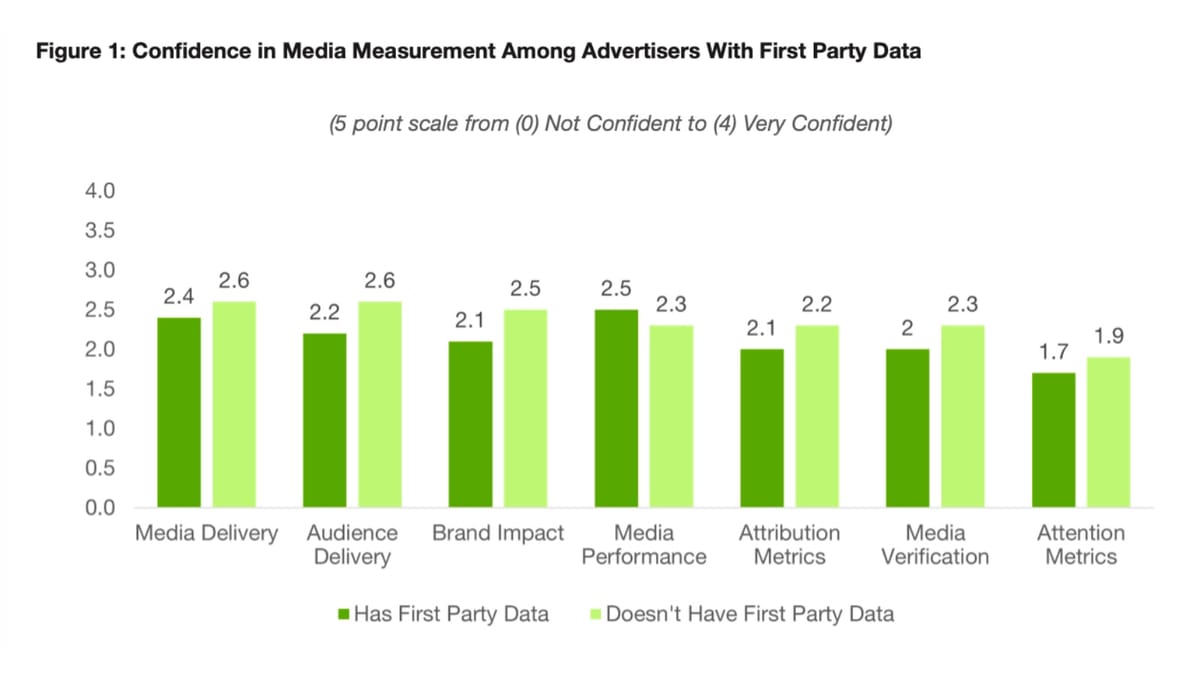

The CIMM/4As study organized the landscape into seven Measurement Domains: Media Delivery, Media Verification, Audience Delivery, Attention Metrics, Brand Impact, Media Performance, and Attribution Metrics. Each domain covers a distinct aspect of campaign evaluation, from basic impressions and reach to multi-touch attribution and marketing mix modeling.

Media Delivery covers the quality and efficiency of placements, encompassing metrics such as impressions, reach, frequency, completion rates, cost per thousand impressions (CPM), and cost per GRP. Media Verification addresses accuracy, compliance, and fraud detection - including invalid traffic (IVT), brand safety compliance, viewability, and geo-targeting accuracy. Audience Delivery validates that the intended demographic is actually being reached, using on-target percentage, average reach and frequency against demographic and advanced audience definitions.

Attention Metrics measure how effectively media captures consumer focus, covering attention time, facial coding, and mental engagement. Brand Impact tracks the effectiveness of media in shifting brand awareness, recall, favorability, and purchase intent. Media Performance - the domain rated most important across the entire sample - measures outcomes such as click-through rate (CTR), cost per lead (CPL), cost per acquisition (CPA), return on ad spend (ROAS), and sales lift percentage. Finally, Attribution Metrics cover the contribution of different media touchpoints to conversions, including multi-touch attribution (MTA), customer journey mapping, and Marketing Mix Models (MMM).

When survey respondents were asked to identify the single most important domain, 39% selected Media Performance. Attribution Metrics ranked second at 20%, followed by Brand Impact at 17%, Audience Delivery at 13%, Media Delivery at 8%, Attention Metrics at 3%, and Media Verification at 2%. The primacy of Media Performance reflects its role as what the report calls the common "boardroom metric" for budget justification.

Confidence, however, follows a different distribution. According to the study, advertisers are most assured when metrics are observable, timely, and widely understood internally. Attention, attribution, and verification are consistently described as "black boxes." Brand impact and audience delivery are better understood in conceptual terms, but remain constrained by speed, comparability, and identity resolution limitations.

The confidence gap, the authors write, is as much human and organizational as it is technical.

Rather than organizing findings purely by sector, the study identifies three distinct measurement orientations that better explain where confidence holds and where it collapses.

Fast Proof Advertisers - primarily in retail and financial services - prioritize speed, causal clarity, and near-real-time optimization. Their confidence is anchored in what can be directly observed: conversions, ROAS, lift tests, and daily optimization signals. These organizations are performance-first by design. A QSR executive interviewed for the study stated: "Everything ladders to ROI and incrementality. If it's not driving incremental transactions, it's not working." Confidence breaks down for this group when signals are slow or contradictory. They tend to operate with clarity inside their own environments while approaching broader ecosystem metrics with greater scrutiny. A technology executive in this cluster noted: "If we're talking about our first party data, our internal data, then I have very high confidence in it. This is a company that prides itself on data and integrity and we have a lot of policies/regulations to govern that."

Comparable Proof Advertisers - spanning CPG, pharma, automotive, and travel - value consistency, rigor, and cross-channel comparability. These sectors operate with indirect sales signals and significant offline outcomes. For CPG, inconsistent data, cross-platform comparability, and signal fragmentation are key concerns. A CPG executive described their current practice: "We do brand awareness studies… quick reads… MMM… clean rooms… and the whole plethora of media metrics." Automotive advertisers face a particular variant of this tension: they are both brand-led and performance-driven while navigating rapid digital acceleration, which creates persistent friction between attribution, brand studies, MMM, and platform-reported data. An auto executive captured it plainly: "Did I get what I paid for and did it move the business? … I can't say that we have done a good job at that." For this group, an auto executive's measurement philosophy is instructive: "We look for consistency. The most important thing is that we can compare channels in the same language."

Future Proof Advertisers - primarily technology and SaaS companies - aspire to both speed and rigor simultaneously. They express the highest expectations of any group and perceive the largest gap between current measurement capabilities and where they believe the industry needs to go. A tech executive quoted in the study stated: "Cross-media measurement where the advertiser, agency, and platforms all come together is really important. The speed needs to accelerate." Another said: "If I can't see the signal in near real-time, I can't optimize against it - so the measurement is incomplete." This orientation reflects a desire for AI-enabled and predictive measurement that does not yet exist at the required scale or reliability. One technology executive went further on the operational ideal: "MMM needs to be daily and used for real-time decision-making."

The quantitative component was conducted by NewtonX and surveyed 197 experienced marketers, each with more than eight years of experience and direct involvement in selecting or using measurement solutions. All respondents were Director-level or above, and the sample was exclusively composed of brand advertisers - not agencies. The research focused on B2C marketers at companies with annual U.S. marketing budgets exceeding $50 million.

Respondent companies were divided into three spending segments: lower ($50-100 million), medium ($100-250 million), and higher (over $250 million). The seven industry sectors covered were Consumer Packaged Goods (n=30), Pharmaceuticals and Healthcare (n=30), Financial Services (n=30), Technology and Telecommunications (n=30), Automotive (n=28), Travel and Leisure (n=30), and Retail (n=30). By seniority, 8% of respondents were C-level, 11% were department or line-of-business heads, 29% were vice presidents, and 52% were senior directors or directors.

With a sample of 197, the margin of error at the 95% confidence level ranges from approximately ±3 percentage points for very small or very large percentages to ±7 percentage points for percentages near 50%. The qualitative component involved 16 one-on-one in-depth interviews with senior executives across the same seven sectors, conducted in confidence. Companies represented in the interviews included Google, T-Mobile, Intuit, Mastercard, Bank of America, Kraft Heinz, Unilever, Sanofi, Toyota, Optum, Wayfair, and Microsoft.

The report makes a counterintuitive observation about advertising spend: it influences measurement priorities, but does not determine measurement philosophy. Roughly one-third of advertisers in the study were using nearly all major channels simultaneously, and more than 80% were using digital video, social media, SEO, broadcast TV, and streaming channels at once. Each channel carries its own delivery systems, metrics, identity frameworks, and reporting standards. As media mixes widen, advertisers are not just managing more channels - they are managing more versions of performance, reach, and impact.

Whether media is managed in-house, by agencies, or through hybrid models does not fundamentally change the challenge. Agencies help manage fragmentation and normalization, but having media capabilities in-house does not eliminate the burden of stitching together inconsistent data sources. In all cases, multiple systems produce competing versions of the truth.

This fragmentation problem has practical consequences well beyond marketing departments. Cross-media measurement has long been identified as a structural challenge, with Bruno Furnari, Chief Product & Technology Officer at AudienceProject, noting that "without cross-media measurement, on the buy-side and on the sell-side, you could be flying blind." The CIMM/4As study puts this in quantitative terms: 43% of advertisers rated cross-platform measurement as a major or severe barrier over the next three to five years, tied with transparency around methodologies as the two largest anticipated obstacles.

The challenge of standardization is structural. CIMM itself has been actively pursuing European cross-media measurement research as of January 2026 to examine how different markets have developed varying measurement infrastructures reflecting local media ownership structures, regulatory environments, and industry relationships. That initiative reflects the same core problem the Paradox of Plenty study surfaces domestically: standards remain fragmented, and fragmentation erodes confidence.

Among emerging technologies, AI-powered measurement stands out as the tool most expected to change the landscape. According to the report, over 80% of advertisers agree that AI solutions will impact measurement in the next three to five years. The appeal is specific: faster interpretation, predictive insight, and relief from the manual reconciliation burden that currently consumes significant organizational resources.

Cross-media measurement ranks second among technology priorities. Privacy-preserving identity solutions, synthetic data, and clean rooms are also cited as future-oriented mechanisms, reflecting an expectation that the next era of measurement will be probabilistic, collaborative, and privacy-safe. A CPG executive described the current gap: "The real holistic measurement of different channels is not there… a unified metric to compare linear TV with digital is missing. We built our own combined qualified reach number."

These expectations are not expressions of technology optimism alone. They reflect a demand for measurement systems that are coherent, interpretable, and usable at the speed of decision-making - not aspirational capabilities that exist in vendor roadmaps but not yet in practice.

Kochava, one of the study's sponsors, has itself been developing tools in this direction. Its MMM Data Validator tool launched in December 2025 to address data quality issues that undermine marketing mix modeling before they propagate through the model. The tool allows marketers to upload CSV files and receive automated reports identifying common errors. The Kochava research published in September 2025 also demonstrated a 35% gap between last-touch attribution and MMM when measuring TikTok's incremental impact, which directly illustrates why the methodology question is not merely academic.

Nielsen, another sponsor, has meanwhile been expanding measurement infrastructure in adjacent areas. The company's August 2025 collaboration with Edison Research to integrate podcast metrics into Nielsen Media Impact created the first platform where advertisers and agencies could plan and compare podcasts, TV, radio, digital, and social in one unified view. The initiative reflected exactly the kind of cross-media interoperability that the Paradox of Plenty study identifies as a priority - though the study makes clear that these efforts remain incomplete at the ecosystem level.

The MRC and IAB finalized attention measurement guidelines in November 2025 after a public comment period, establishing standardized frameworks covering data signals, visual tracking, physiological and neurological observation, and panel-based methodologies. The framework reinforces that attention should not be used as a measure of outcomes for evaluating campaign performance - a nuance the CIMM/4As study reflects when it notes that advertisers value attention metrics conceptually but remain cautious about using them as primary decision inputs.

The study concludes with four priorities for strengthening advertiser confidence. The first is stronger governance through shared definitions and standards: unified definitions, identity standards, and verification norms. The second is greater transparency into methodologies and assumptions, enabling independent review, model logic explanation, and cross-vendor calibration - moving away from what multiple interviewees described as black-box outputs.

The third priority is innovation paired with guardrails. AI-based tools will increase in uptake, according to the study, but confidence in those tools will rise only when they are paired with strong governance that supports experimentation and adoption rather than creating new opacity. The fourth is focused investment in interoperable, future-ready infrastructure - data that can be compared, interpreted, and reconciled across systems. The industry's role, the authors write, is not to push measurement forward, but to make measurement interoperable, intelligible, and fit for decision-making.

Zuber Nosimohomed, President of TechEdge, offered this framing in the report: "The future of measurement isn't about replacing current signals - it's about making them work better together. Hybrid measurement that combines panels and digital data brings clarity to a complex landscape, but its value depends on access, usability, and the ability to turn data into meaningful insights."

Jon Watts, Managing Director of CIMM, addressed the collective challenge in the announcement: "Advertisers are navigating real challenges around comparability and identity in an increasingly fragmented environment. Encouragingly, they don't see those barriers as insurmountable. They're not looking for a single source of truth, but clarity about how different truths relate."

Ashwini Karandikar, 4As EVP of Media, Technology, and Data, framed the demand from the agency side: "To drive real performance, we need more than just innovation - we need accountability. Agencies and their advertiser clients are pushing for a future-ready infrastructure where definitions are unified and methodologies are transparent. By pairing next-gen tools like AI with stronger industry guardrails, we ensure that every dollar is measurable, every assumption is verifiable, and every campaign is optimized against a reconciled, holistic view of the market."

The study closes on a line attributed to an unidentified advertiser that captures the central tension of the entire report: "The data is there. The question is what counts."

Despite inconsistent confidence levels, the majority of advertisers - more than 90%, according to the study - do not anticipate severe measurement barriers emerging over the next three to five years. The challenges are viewed as moderate to major obstacles, but manageable ones. They complicate workflows, slow decision-making, and require reconciliation. But they are not viewed as existential threats. Advertisers have normalized the complexity. As ambitions increase - particularly for attribution, brand insight, and cross-media coherence - the challenges will become more salient. Bridging the confidence gap, the authors conclude, requires not more data or more tools, but systems that help advertisers understand what counts, why results differ, and how to act with assurance in a complex ecosystem.

Who: CIMM (Coalition for Innovative Media Measurement) and the 4As (American Association of Advertising Agencies), with co-sponsorship from Kochava, Nielsen, and TechEdge. The study was authored by Sarah Mansfield (former VP Global Media at Unilever), Alice Sylvester (independent measurement consultant, former Chairman of the Advertising Research Foundation), and Leslie Wood, Ph.D. (advertising analytics leader, formerly of iSpot and NCSolutions). The survey covered 197 senior marketers at Director level or above from seven B2C industry sectors, all at companies with U.S. marketing budgets exceeding $50 million.

What: A joint quantitative and qualitative research study examining how U.S. advertisers prioritize, evaluate, and express confidence in seven major media measurement domains - Media Delivery, Media Verification, Audience Delivery, Attention Metrics, Brand Impact, Media Performance, and Attribution Metrics - across the TV and video ecosystem. The study finds that advertiser confidence has not kept pace with measurement capability, driven not by data scarcity but by the inability to reconcile competing outputs across fragmented platforms and identity systems. Four priorities are identified: stronger governance, greater transparency, innovation with guardrails, and investment in interoperable infrastructure.

When: The study was published today, March 5, 2026. The quantitative survey was conducted by NewtonX. The 16 qualitative interviews were completed in confidence across the same seven industry sectors. The full report is available to CIMM and 4As members; the executive summary is publicly accessible.

Where: The study focuses on the U.S. advertising market. The companies interviewed include major global advertisers headquartered in the United States, with operations across multiple markets. The findings address measurement challenges specific to the U.S. TV and video ecosystem but have implications for any market where media fragmentation and identity resolution challenges are present.

Why: Advertisers have built sophisticated measurement environments over the past decade but face a growing crisis of confidence in interpreting and communicating results. The study identifies that the root cause is not data quality but structural complexity: multiple systems producing competing versions of the truth, black-box methodologies, and the difficulty of reconciling disparate data sources at speed. The research was commissioned to surface where confidence breaks down by category and orientation type, and to identify practical steps the industry can take to restore trust in measurement.