Google Network advertising revenue declines 1% as AI features reduce publisher traffic

Alphabet Q2 2025 results show Network revenue pressure while Search and YouTube advertising grow amid fundamental changes in user search behavior.

Alphabet Q2 2025 results show Network revenue pressure while Search and YouTube advertising grow amid fundamental changes in user search behavior.

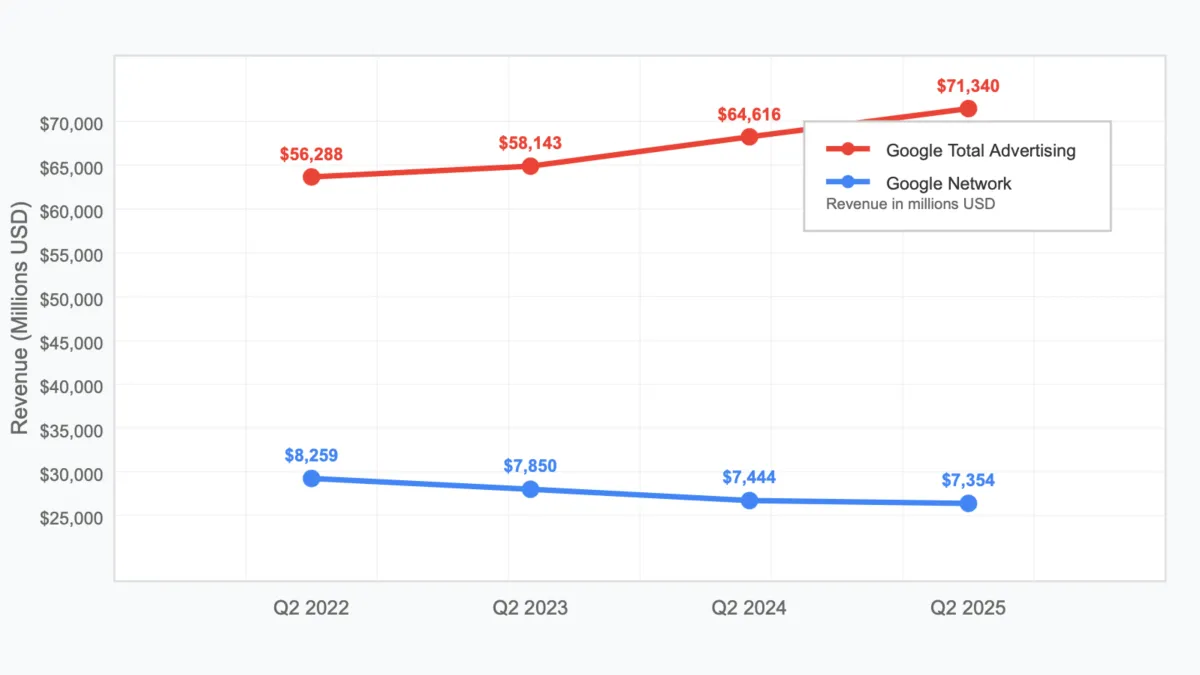

Google Network advertising revenues declined 1% year-over-year to $7.4 billion during the second quarter of 2025, marking a concerning trend for publishers as artificial intelligence features increasingly answer user queries without directing traffic to external websites. According to Alphabet Inc.'s earnings announcement on July 23, 2025, the Network revenue decline contrasts sharply with growth in Google's owned properties, suggesting a fundamental shift in how search traffic flows through the digital advertising ecosystem.

Subscribe the PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

The Mountain View-based technology company reported total advertising revenues of $71.3 billion in Q2 2025, representing 10% year-over-year growth, but the distribution of that growth reveals strategic changes that significantly impact third-party publishers. While Google advertising chief Philipp Schindler stated the company achieved 'robust growth across the company,' the Network segment faces headwinds as AI-powered search experiences retain users within Google's ecosystem rather than sending them to publisher websites.

Google Services, which encompasses advertising alongside subscriptions and devices, achieved revenues of $82.5 billion in Q2 2025, up 12% year-over-year. However, the Network advertising decline within this broader growth indicates that publishers participating in Google's advertising programs are experiencing reduced monetization opportunities as search behavior fundamentally changes.

The Google Network, which includes AdSense, AdMob, and Google Ad Manager, traditionally served as a crucial revenue source for millions of websites worldwide by placing contextual advertisements alongside publisher content. The 1% revenue decline to $7.4 billion suggests that reduced traffic from Google Search is beginning to impact publisher monetization capabilities significantly.

During the earnings call, Schindler provided minimal commentary on Network revenue performance, acknowledging the decline without detailed explanation. This approach suggests the revenue reduction represents expected outcomes from strategic platform changes rather than temporary market conditions or competitive pressures.

The Network revenue decline aligns with fundamental changes in search result presentation that increasingly provide answers directly within Google's interface. AI Overviews, which now serve over 2 billion monthly users according to CEO Sundar Pichai, often satisfy user intent without requiring clicks to external websites. "We know how popular AI Overviews are because they are now driving over 10% more queries globally for the types of queries that show them," Pichai stated during the earnings call, but this query increase doesn't translate proportionally to publisher traffic.

AI Overviews and AI Mode are the final nails to the coffin for traditional publisher traffic models, with industry observers noting that Google is effectively diverting all our traffic through direct answer provision.

Google's emphasis on Demand Gen campaigns represents a deliberate strategic shift that impacts Network revenue distribution. Rather than directing advertiser spending toward third-party publisher websites through traditional Display campaigns, Demand Gen routes investment toward YouTube, Discover, and other Google-owned surfaces.

This strategic reorientation reflects Google's preference for higher-margin advertising inventory where the company controls both the user experience and revenue capture. While Network advertising requires revenue sharing with publishers, owned inventory allows Google to retain entire advertising proceeds while maintaining complete control over ad placement and user experience.

The Demand Gen emphasis aligns with broader industry trends toward walled garden advertising environments. Previous PPC Land analysis indicated that Google's transition away from traditional Network campaigns reflects strategic priorities favoring controlled advertising environments over distributed publisher inventory.

During the earnings call, Schindler emphasized Performance Max and Demand Gen capabilities without addressing Network advertising opportunities, suggesting these automated campaign types increasingly direct spending toward Google's owned properties rather than external publisher websites.

YouTube advertising revenues reached $9.8 billion in Q2 2025, representing 13% year-over-year growth that contrasts dramatically with Network advertising decline. The YouTube performance illustrates Google's strategic preference for owned inventory where the company controls both content and advertising experience.

"YouTube saw similar performance across verticals. Its 13% growth in advertising revenues was driven by direct response, followed by brand," Schindler reported during the earnings call. The YouTube growth occurs within an environment where Google maintains complete control over content recommendation, user engagement, and advertising placement without relying on external publisher cooperation.

Connected TV advertising within YouTube showed particularly strong momentum. "In the past 12 months, YouTube ads viewed on CTV screens drove over one billion conversions," Schindler stated. "We saw strong growth in retail thanks to CTV shopping ads, which allows viewers to shop directly via QR codes, helping us leverage direct marketing opportunities."

The Connected TV success demonstrates how controlled environments enable innovative advertising formats that would be difficult to implement across distributed publisher networks. QR code integration, direct shopping capabilities, and seamless conversion tracking require the technical control that YouTube provides but Network advertising cannot match.

YouTube Shorts achieved significant monetization improvements during the quarter, with important implications for publisher competition. "In the U.S., Shorts now earn as much revenue per watch hour as traditional in-stream on YouTube. And in some countries, it now even exceeds in-stream's rate," Pichai announced. This monetization success occurs entirely within Google's ecosystem while potentially drawing audience attention away from publisher websites where Network advertising operates.

According to Nielsen data referenced during the earnings call, "YouTube has led U.S. streaming watch time for over two years" while achieving "a record high of 12.8% of total TV viewing in June 2025." This viewing leadership provides YouTube with significant advantages over traditional publishers who must compete for audience attention in an increasingly fragmented content landscape.

Google Search and other revenues reached $54.2 billion during the quarter, marking 12% growth that demonstrates continued advertiser confidence in search marketing despite fundamental changes in result presentation. However, this growth occurs alongside features that reduce traditional website visits, creating a disconnect between search advertising success and publisher revenue opportunities.

"Search and other revenues delivered growth across all verticals with the largest contributions coming from retail and financial services," CFO Anat Ashkenazi reported during the earnings call. The vertical growth indicates that advertisers continue investing in search campaigns even as AI features alter traffic distribution patterns.

The search advertising growth benefits from increased query volume driven by AI features. "Our new AI experiences significantly contributed to this increase in usage," Pichai explained. "We are also seeing that our AI features cause users to search more as they learn that Search can meet more of their needs. That's especially true for younger users."

However, the increased search usage doesn't proportionally benefit publishers participating in Network advertising programs. AI Overviews often provide sufficient information to satisfy user intent without requiring external website visits, while traditional organic search results compete for reduced attention in AI-enhanced result layouts.

Visual search capabilities through Lens demonstrate this traffic retention dynamic clearly. "The majority of Lens searches are incremental and we are seeing healthy growth with shopping queries using Lens," Schindler reported. While these shopping queries might traditionally drive traffic to e-commerce websites, Google's integration of product information and purchasing capabilities directly within search results reduces external website dependencies.

Google's artificial intelligence capabilities increasingly influence advertising campaign performance through automated optimization tools that prioritize platform-controlled inventory over external publisher websites. These tools systematically redirect advertiser spending toward Google's owned properties while reducing investment in Network advertising opportunities.

AI Max in Search, introduced during the quarter, provides advertisers with automated optimization features within search campaigns. "Advertisers that activate AI Max in Search campaigns typically see 14% more conversions," Schindler reported. However, these conversion improvements often result from directing users to advertiser websites directly from search results rather than through intermediate publisher content that generates Network advertising revenue.

Smart Bidding Exploration, described as "the biggest update to bidding strategy in a decade," enables automated campaign optimization that systematically favors higher-performing inventory. "Campaigns using Smart Bidding Exploration see a 19% increase in conversions on average," according to Schindler. This optimization inherently directs spending toward Google's owned properties where conversion tracking and optimization capabilities exceed those available through third-party publisher websites.

Performance Max campaigns, which Google increasingly positions as the default campaign type, operate through automated inventory selection that prioritizes YouTube, Shopping, and other owned surfaces over Network placements. While these campaigns can include Network inventory, the algorithmic optimization naturally favors platforms where Google maintains greater control over user experience and conversion attribution.

The Network advertising revenue decline represents only the direct impact of reduced traffic on publisher monetization. Secondary effects include reduced audience engagement, decreased content production capabilities, and diminished competitive positioning relative to platform-controlled content sources.

Publishers traditionally relied on Google Search traffic to build audience relationships that extended beyond individual page visits through newsletter subscriptions, social media follows, and direct website bookmarks. As AI features satisfy user intent without requiring website visits, publishers lose opportunities to establish these ongoing audience connections.

The reduced traffic also impacts publisher ability to gather first-party data about audience preferences and behaviors. This data traditionally supported advertising targeting, content optimization, and business development decisions. Without sufficient traffic volume, publishers struggle to maintain the data collection necessary for competitive digital advertising operations.

Content production economics face particular pressure as reduced traffic undermines the revenue models that support journalism, specialized technical content, and other information resources. Industry discussions documented by PPC Land indicate that many publishers report "dramatic drops in organic visibility and earnings" that threaten content production sustainability.

The advertising performance distribution across Google's properties reveals deliberate strategic choices that prioritize platform control over ecosystem distribution. Marketers increasingly recognize that Google's AI features serve platform objectives that may conflict with traditional publisher revenue models.

Recent analysis from PPC Land suggests that "AI agents replace traditional web browsing patterns" while "search engines experience fundamental changes" that systematically favor platform-controlled experiences over distributed website ecosystems.

The emergence of AI-powered search alternatives creates additional pressure on traditional publisher business models. While Google maintains dominant market position, the competitive landscape increasingly features AI-first search experiences that prioritize direct answer provision over website traffic generation.

Enterprise advertising adoption shows particular momentum in platform-controlled environments where conversion tracking and audience targeting capabilities exceed those available through distributed publisher networks. The democratization of sophisticated advertising tools primarily benefits campaigns that operate within Google's owned inventory rather than external publisher websites.

Google's investment priorities indicate continued emphasis on AI capabilities that retain users within platform-controlled experiences rather than directing traffic to external websites. The company's increased capital expenditure guidance to $85 billion reflects infrastructure development that supports AI feature expansion rather than traditional search traffic distribution.

"We expect 2026 to be the year in which people kind of use agentic experiences more broadly," Pichai stated during the earnings call when discussing AI agent development. These agentic experiences operate autonomously within Google's ecosystem, suggesting further traffic retention that could impact Network advertising revenue.

The company's approach to AI Mode monetization indicates future advertising integration that occurs entirely within Google's interface. "Just like we are doing with AI Overviews and with AI Mode over time, we'll be able to bring very good commercial experiences there as well," Pichai explained. This monetization strategy provides no revenue opportunities for external publishers while potentially reducing traditional search traffic further.

Network Advertising: Google's distributed advertising program encompassing AdSense, AdMob, and Google Ad Manager that places advertisements on third-party publisher websites and mobile applications. This revenue stream declined 1% to $7.4 billion in Q2 2025, representing a fundamental shift away from traditional publisher monetization models. Network advertising traditionally provided crucial revenue for millions of websites worldwide by enabling contextual advertisement placement alongside publisher content, but AI-powered search features increasingly retain users within Google's ecosystem rather than directing traffic to external sites where Network ads generate revenue.

AI Overviews: Google's artificial intelligence-powered feature that provides comprehensive responses directly within search results, now serving over 2 billion monthly users across more than 200 countries and territories. Powered by Gemini 2.5 models, AI Overviews drive 10% more queries globally for applicable search types while often satisfying user intent without requiring clicks to external websites. This functionality represents a fundamental challenge to traditional publisher business models that depend on search traffic, as users obtain complete answers within Google's interface rather than visiting websites where they might encounter advertising or engage with publisher content.

Publisher Traffic: The flow of users from Google Search to external websites, which forms the foundation of Network advertising revenue and traditional digital publishing economics. AI features increasingly reduce this traffic by providing answers directly within search results, creating significant challenges for publishers who depend on website visits for advertising revenue, audience development, and content monetization. The systematic reduction in publisher traffic affects not only immediate advertising revenue but also long-term audience relationship building, first-party data collection, and content production sustainability across the digital publishing ecosystem.

YouTube Advertising: Google's video advertising platform that generated $9.8 billion in Q2 2025, representing 13% year-over-year growth within a controlled environment where Google maintains complete oversight of content, user experience, and advertising placement. YouTube's success demonstrates the advantages of owned inventory over distributed Network advertising, with Connected TV advertising showing particular strength and Shorts achieving monetization parity with traditional video formats. The platform's growth contrasts sharply with Network advertising decline, illustrating Google's strategic preference for controlled advertising environments over external publisher revenue sharing arrangements.

Search Advertising: Google's core advertising business that generated $54.2 billion in Q2 2025 with 12% year-over-year growth, encompassing advertisements displayed alongside search results and within Google's search interface. While search advertising continues growing, the integration of AI features fundamentally alters how users interact with search results, often providing complete answers without requiring website visits that traditionally supported publisher monetization. The search advertising growth masks significant challenges for external publishers as AI-enhanced results reduce traditional click-through patterns while maintaining advertiser investment in Google's platform.

Demand Gen Campaigns: Google's advertising campaign type that prioritizes YouTube, Discover, and other Google-owned surfaces rather than directing advertiser spending toward third-party publisher websites through traditional Display campaigns. This strategic emphasis reflects Google's preference for higher-margin advertising inventory where the company controls both user experience and revenue capture without requiring revenue sharing with external publishers. Demand Gen represents a deliberate shift toward walled garden advertising environments that systematically redirect marketing investment away from distributed publisher networks toward platform-controlled inventory.

AI Mode: Google's experimental end-to-end artificial intelligence search experience that achieved over 100 million monthly active users in the United States and India, designed specifically for "longer and more complex questions" that traditional search methods handle less effectively. AI Mode operates entirely within Google's interface, providing comprehensive conversational search experiences that eliminate the need for external website visits. This feature represents the future direction of search interaction, where users engage in extended information-seeking sessions within Google's ecosystem rather than browsing multiple websites, further reducing traffic opportunities for publishers participating in Network advertising programs.

Connected TV Advertising: YouTube's television-based advertising format that drove over one billion conversions in the past 12 months, demonstrating the platform's effectiveness in premium video advertising environments. Connected TV advertising enables innovative formats like QR code shopping integration and direct conversion tracking that would be difficult to implement across distributed publisher networks, showcasing the technical advantages of controlled advertising environments. This advertising category represents YouTube's competitive strength against traditional television broadcasters while providing advertisers with digital precision targeting combined with television-scale reach, capabilities that external publishers cannot match through Network advertising programs.

Visual Search: Google's image-based query capabilities through Lens and Circle to Search that grew 70% year-over-year, enabling users to search by selecting visual elements rather than typing text queries. Visual search increasingly includes shopping functionality and product information directly within Google's interface, reducing the need for external e-commerce website visits that traditionally generated Network advertising revenue. The rapid growth of visual search capabilities demonstrates changing consumer behavior patterns, particularly among younger demographics, while creating additional traffic retention mechanisms that keep users within Google's ecosystem rather than directing them to publisher websites.

Platform-Controlled Inventory: Advertising placements within Google's owned properties like YouTube, Search, and Discover where the company maintains complete control over user experience, content presentation, and revenue capture without requiring external publisher cooperation. This inventory type provides superior conversion tracking, audience targeting, and creative format flexibility compared to distributed Network advertising placements on third-party websites. Google's strategic emphasis on platform-controlled inventory reflects broader industry trends toward walled garden advertising environments that prioritize predictable user experiences and comprehensive data collection over the distributed, less controllable nature of traditional publisher networks.

Subscribe the PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Who: Google Network advertising segment, representing millions of publishers worldwide using AdSense, AdMob, and Google Ad Manager, experienced revenue decline while Google's owned properties grew under advertising chief Philipp Schindler's strategic direction.

What: Network advertising revenues declined 1% to $7.4 billion in Q2 2025, contrasting with Search advertising growth to $54.2 billion (12% increase) and YouTube advertising growth to $9.8 billion (13% increase), as AI features increasingly retain users within Google's ecosystem rather than directing traffic to external publisher websites.

When: Performance covers the quarter ended June 30, 2025, announced during the July 23, 2025 earnings call, representing continued pressure on publisher revenue models amid expanding AI feature deployment throughout the first half of 2025.

Where: Global Network advertising decline affects publishers across all markets, while YouTube demonstrates particular strength in Connected TV advertising and Google Search maintains growth across retail and financial services verticals through AI-enhanced experiences.

Why: AI Overviews, AI Mode, Lens search, and other platform features increasingly satisfy user intent without requiring external website visits, systematically reducing the traffic that generates Network advertising revenue while Google prioritizes owned inventory through Demand Gen campaigns and automated optimization tools that favor platform-controlled experiences over distributed publisher ecosystem participation.