November retail sales rise 4.53% as holiday spending meets forecast

CNBC/NRF Retail Monitor shows November retail sales increased 4.53% year-over-year with flat monthly growth as Cyber Monday timing shifts spending patterns.

CNBC/NRF Retail Monitor shows November retail sales increased 4.53% year-over-year with flat monthly growth as Cyber Monday timing shifts spending patterns.

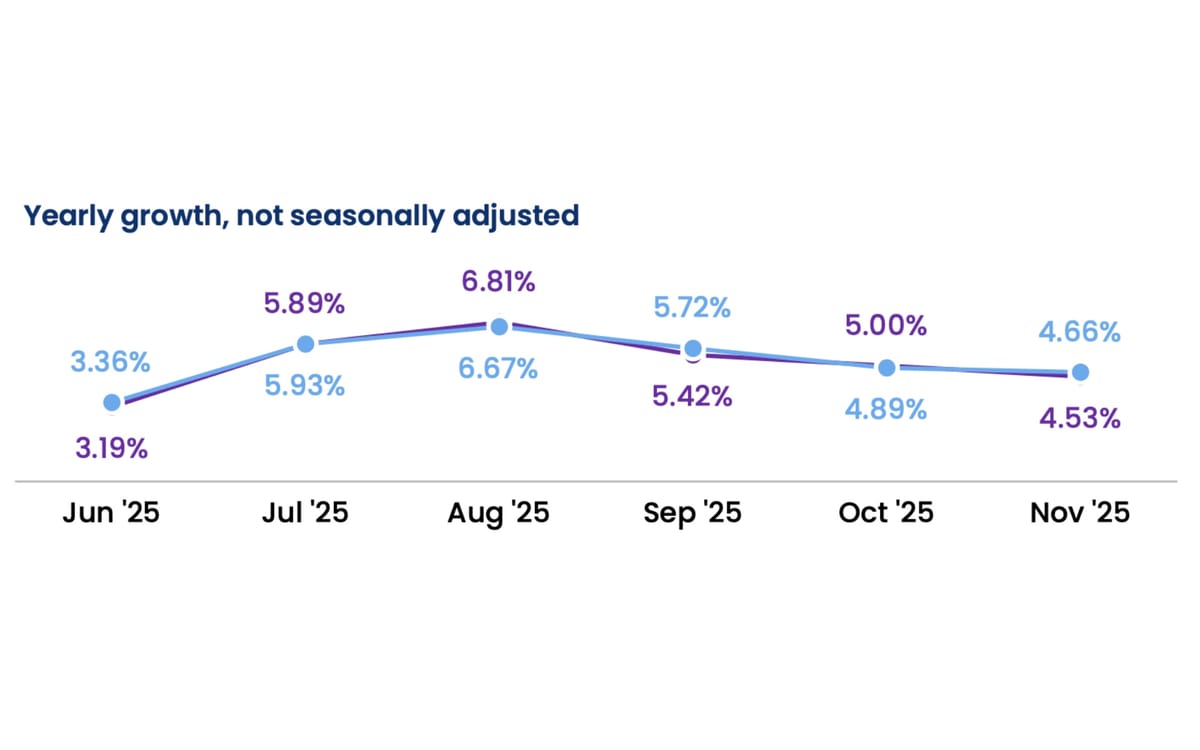

U.S. retail sales demonstrated solid year-over-year expansion in November 2025 while maintaining relatively flat monthly performance, according to data released December 12 by the National Retail Federation. The CNBC/NRF Retail Monitor, powered by Affinity Solutions, showed total retail sales excluding automobile dealers and gasoline stations increased 4.53% compared with November 2024, marking continued momentum in the first half of the holiday shopping season.

Monthly performance registered 0.12% growth on a seasonally adjusted basis. This modest sequential increase contrasts with October's 0.6% month-over-month expansion, suggesting consumers moderated spending ahead of promotional events. Core retail sales, which exclude restaurants in addition to auto dealers and gas stations, declined 0.04% month-over-month but climbed 4.66% year-over-year.

The retail performance data arrives as the National Retail Federation forecasts holiday sales from November 1 through December 31 will increase between 3.7% and 4.2% compared with 2024 levels, reaching just over $1 trillion. NRF projects full-year retail sales will grow between 2.7% and 3.7% over 2024 to as much as $5.48 trillion.

Subscribe PPC Land newsletter ✉️ for similar stories like this one

"Retail sales showed healthy year-over-year gains in November while month-over-month data was largely flat," NRF President and CEO Matthew Shay stated in the announcement, according to the press release. "Shoppers looking for online deals may have held back a bit until Cyber Monday, which landed in December due to a late Thanksgiving, likely shifting some spending. Consumers are focusing on value and spending carefully during the holiday period, and retailers are offering products at competitive prices to fit every budget."

The timing dynamics created by Thanksgiving's late November 28 date affected promotional calendar sequencing. Cyber Monday fell on December 1, potentially delaying digital purchases that would have otherwise registered in November's data. This calendar shift complicates direct comparisons with previous years when Cyber Monday occurred within the November reporting period.

Retail sales grew 5% in October as consumers entered the holiday shopping season, establishing baseline momentum that carried into November. The CNBC/NRF Retail Monitor leverages anonymized credit and debit card purchase data from more than 140 million cards, tracking nearly 9 billion transactions totaling more than $500 billion in annual spending. This methodology distinguishes the measurement system from survey-based approaches employed by the U.S. Census Bureau, eliminating the need for subsequent revisions.

Total retail sales increased 5.06% year-over-year for the first 11 months of 2025, while core sales expanded 5.22% during the same period. These cumulative figures demonstrate sustained consumer spending strength through an extended promotional period that began earlier than traditional holiday calendars.

Digital products led November's category performance with 14.81% year-over-year growth, although the segment experienced a 0.37% monthly decline. The category encompasses electronic books, games, and digital downloads. Sporting goods, hobby, music and bookstores achieved 8.96% annual growth alongside 0.28% monthly expansion. Clothing and accessories stores posted 8.16% year-over-year gains despite a 0.04% monthly decrease.

Grocery and beverage stores demonstrated resilience with 3.89% annual growth and 0.74% monthly expansion, reflecting steady demand for essential purchases. General merchandise retailers grew 3.1% year-over-year but contracted 0.73% month-over-month, suggesting consumers deferred discretionary purchases until deeper promotional events. Health and personal care stores expanded 1.31% annually while declining 0.19% monthly.

Electronics and appliance stores registered modest 1.01% year-over-year growth but experienced a 2.94% monthly decline, the sharpest monthly contraction among measured categories. Furniture and home furnishings retailers achieved 0.53% annual growth with virtually flat 0.01% monthly performance. Building and garden supply stores faced continued headwinds, declining 9.38% year-over-year and 1.74% month-over-month.

The sector-level performance variations reflect shifting consumer priorities during holiday preparation. Early shopping behavior, driven partly by tariff concerns, created demand patterns that diverged from historical norms. Research showed 34% of consumers began holiday shopping in October or earlier, with 71% citing tariff-related price increases as their primary concern heading into peak season.

Consumer spending surveys conducted in mid-October indicated shoppers planned to allocate $890.49 per person on average for holiday gifts, food, decorations and seasonal items—the second-highest amount in the survey's 23-year history. This spending intention data suggested strong demand potential despite widespread economic caution. The actual November sales figures align with these projections, indicating consumers followed through on stated holiday budgets.

The retail measurement infrastructure supporting these insights has gained significance as retail media networks expand toward projected $204 billion in global advertising revenue by 2027. Real-time transaction data provides merchants and advertisers with earlier visibility into consumer behavior shifts compared with traditional government reporting schedules, which require multiple revisions as survey responses arrive.

Display retargeting costs surged 11% year-over-year from September through November according to AdRoll's Q4 2025 State of Digital Advertising Report, reflecting intensified competition for consumer attention during the extended holiday period. The advertising cost increases coincided with the early shopping patterns revealed in retail sales data, suggesting marketers responded to shifting demand timing through increased media investment.

The correlation between Retail Monitor figures and U.S. Census Bureau revised retail sales numbers has established the metric as a reliable forward indicator. Affinity Solutions employs the same seasonalization approach as the Census Bureau, creating methodological consistency while providing approximately one week advance notice compared with official government releases.

Unlike survey-based numbers that undergo monthly and annual revisions, the Retail Monitor produces final figures upon initial release. This stability derives from analyzing actual anonymized credit and debit card transactions rather than projecting from business surveys. The comprehensive dataset encompasses transactions at grocery stores, general merchandise retailers, specialty shops, restaurants, and digital commerce platforms.

Marketing professionals face compressed timelines for fourth-quarter campaigns as holiday shopping extends across multiple months. Google released its Holiday Essentials guide outlining strategic approaches for the 2025 season as consumer behavior shifted toward more deliberate purchasing patterns. The guide revealed 61% of shoppers reported being more selective with spending due to concerns about future economic conditions.

Retail media measurement standardization efforts have intensified as advertising investment concentrates during holiday periods. The Interactive Advertising Bureau and IAB Europe released comprehensive incrementality measurement guidelines in November 2025, establishing frameworks for evaluating causal marketing impact across commerce media campaigns as the sector accelerates toward $100 billion in global spending by 2028.

The concentration of consumer spending during November and December makes fourth-quarter planning critical for retailers and advertisers who must balance inventory availability with marketing investment. Black Friday fell on November 28, 2025, with Cyber Monday following on December 1, creating traditional peaks for shopping activity and advertising revenue that will register in December's retail data.

Wage growth outpacing inflation provides fundamental support for consumer spending despite persistent economic concerns. Employment reports through November showed historically low unemployment rates continuing, supporting household income levels that enable discretionary spending during the holiday season. This macroeconomic backdrop differentiates the current retail environment from previous periods when consumer confidence declined alongside purchasing power.

The November retail sales data confirms that consumers entered peak holiday shopping periods with spending capacity intact, even as behavioral patterns shifted toward value-conscious purchasing and extended research cycles. Retailers adapted promotional strategies to accommodate earlier shopping timelines while maintaining inventory discipline to avoid excess stock accumulation that would pressure margins.

Retail imports forecast showed typical end-of-year slowdown through November and December as most holiday merchandise already reached stores or warehouses. This advance inventory positioning allowed retailers to mitigate potential tariff-related price impacts through strategic planning earlier in the year.

The retail performance metrics carry implications beyond immediate sales figures. Commerce media platforms have expanded measurement capabilities to connect advertising exposure to purchase behavior across both online and offline channels, creating closed-loop attribution systems that leverage the same transaction data underlying retail sales measurements.

European retail media achieved 22.1% growth in 2024, outpacing broader advertising market expansion by nearly four times as brands redirected performance budgets toward commerce media channels. Similar growth trajectories appear across U.S. retail media operators, where fourth-quarter performance typically exceeds annual averages due to concentrated holiday spending.

Food services and drinking places registered 3.86% year-over-year growth, suggesting sustained demand for experiential dining despite overall consumer caution. The restaurant category's performance indicates discretionary spending remained active across multiple retail sectors rather than concentrating exclusively in goods purchases.

Miscellaneous retailers, a category encompassing diverse specialty shops, achieved 5.05% annual growth with 0.04% monthly decline. The segment's steady performance demonstrates consumer willingness to support specialty retail concepts alongside larger format stores, maintaining channel diversity within the retail ecosystem.

Buy ads on PPC Land. PPC Land has standard and native ad formats via major DSPs and ad platforms like Google Ads. Via an auction CPM, you can reach industry professionals.

November's sector performance variations create strategic insights for December forecasting. Categories demonstrating monthly declines despite strong annual comparisons suggest consumers deliberately preserved spending capacity for promotional events concentrated later in the season. Electronics and appliances, furniture, and building supplies all exhibited this pattern, indicating potential demand release during late November and December promotional periods.

The Retail Monitor methodology addresses limitations inherent in traditional retail measurement approaches. Survey-based systems rely on business responses that may lag actual transaction timing, while card transaction data captures purchases in real-time. Seasonal adjustments applied to the raw transaction data align the measurement framework with Census Bureau practices, enabling direct comparison while eliminating revision requirements.

Retailers periodically change how they code card transactions, creating potential data continuity challenges. According to the Retail Monitor documentation, such changes occurred in June, July, and August 2025 compared with 2024 coding practices. While these adjustments did not impact total sales calculations, they affected how sales allocated across individual retail sectors. The measurement team controlled for these coding changes through adjustments to raw sales by category and year-over-year growth percentages.

Marketing platform updates during November reflected industry adaptation to shifting consumer behavior. Google launched four new Demand Gen capabilities on November 17 targeting the holiday shopping season, expanding advertiser control over creative optimization, brand safety parameters, and testing methodologies across YouTube, Discover, and Gmail placements.

The November retail data provides quantitative evidence supporting strategic December planning for retailers and brands. Consumer preservation of spending power during the month, as indicated by flat sequential growth, suggests concentrated demand potential during remaining promotional periods through year-end. Traditional peak shopping days including Green Monday and Free Shipping Day typically drive significant transaction volume in mid-December.

Retail sales measurement has achieved heightened importance as digital advertising platforms integrate commerce data into optimization algorithms. Microsoft and InMobi revealed holiday retail trends across META markets in November 2025, analyzing consumer search and click behavior during the 2024 holiday shopping period to inform 2025 strategies.

The relationship between retail transaction data and advertising performance metrics creates feedback loops where real-time sales information influences media buying decisions, which subsequently affect purchase behavior captured in future transaction data. This dynamic interaction characterizes modern commerce media ecosystems where retail operations and advertising platforms share infrastructure and measurement frameworks.

November's retail performance established baseline expectations for December, which typically represents the single largest revenue month for many retail categories. Gift card purchases accelerate in December, creating revenue recognition patterns that differ from product sales while contributing to reported retail figures. Restaurant spending often peaks during December as holiday parties and celebrations drive dining occasions.

The extended nature of the 2025 holiday season, driven by early shopping behavior and calendar dynamics, created measurement complexity across traditional reporting periods. Transactions that would have concentrated in a compressed late-November through late-December window instead distributed across October through December, affecting year-over-year comparisons and sequential growth calculations.

Consumer behavior demonstrated resilience despite widespread concerns about economic conditions and tariff-related price increases. The 4.53% year-over-year growth in total retail sales exceeded inflation rates, indicating real purchasing volume expansion rather than solely price-driven nominal growth. Core retail sales growth at 4.66% year-over-year further confirmed broad-based demand strength across discretionary and essential categories.

Retailers maintaining competitive pricing strategies throughout November positioned themselves to capture share during peak December periods. The promotional discipline evident in November's relatively modest sequential growth suggests merchants avoided aggressive early discounting that would erode margins while preserving consumer expectations for traditional promotional events later in the season.

Subscribe PPC Land newsletter ✉️ for similar stories like this one

Subscribe PPC Land newsletter ✉️ for similar stories like this one

Who: The National Retail Federation, CNBC, and Affinity Solutions released retail sales measurement data tracking consumer spending across U.S. retail sectors. The measurement system analyzes anonymized credit and debit card transactions from more than 140 million cards.

What: U.S. retail sales excluding automobile dealers and gasoline stations increased 4.53% year-over-year in November 2025 while registering 0.12% month-over-month growth on a seasonally adjusted basis. Core retail sales excluding restaurants grew 4.66% annually but declined 0.04% monthly. Digital products led category performance with 14.81% year-over-year expansion.

When: The CNBC/NRF Retail Monitor November 2025 data was released on December 12, 2025, covering transactions that occurred throughout November. The reporting period captured the first half of the holiday shopping season, with Cyber Monday falling on December 1 due to a late November 28 Thanksgiving.

Where: The retail sales data encompasses transactions at U.S. retail establishments across categories including grocery stores, general merchandise retailers, specialty shops, restaurants, and digital commerce platforms. The measurement excludes automobile dealers and gasoline stations to focus on core retail spending patterns.

Why: The retail sales measurement provides real-time visibility into consumer spending patterns during the critical holiday shopping season, enabling retailers, advertisers, and policymakers to understand demand trends approximately one week before official Census Bureau releases. The data confirmed that consumers maintained spending capacity despite economic concerns and tariff-related price increase worries, validating NRF's forecast for holiday sales to exceed $1 trillion. Marketing professionals use these insights to optimize fourth-quarter advertising strategies and budget allocation across retail media channels projected to reach $204 billion globally by 2027.