Display retargeting CPMs surge 11% as early holiday shopping intensifies

AdRoll reports retargeting costs jumped 11% year-over-year in Q4 2025 as brands competed for early holiday demand amid economic uncertainty and K-shaped spending patterns.

AdRoll reports retargeting costs jumped 11% year-over-year in Q4 2025 as brands competed for early holiday demand amid economic uncertainty and K-shaped spending patterns.

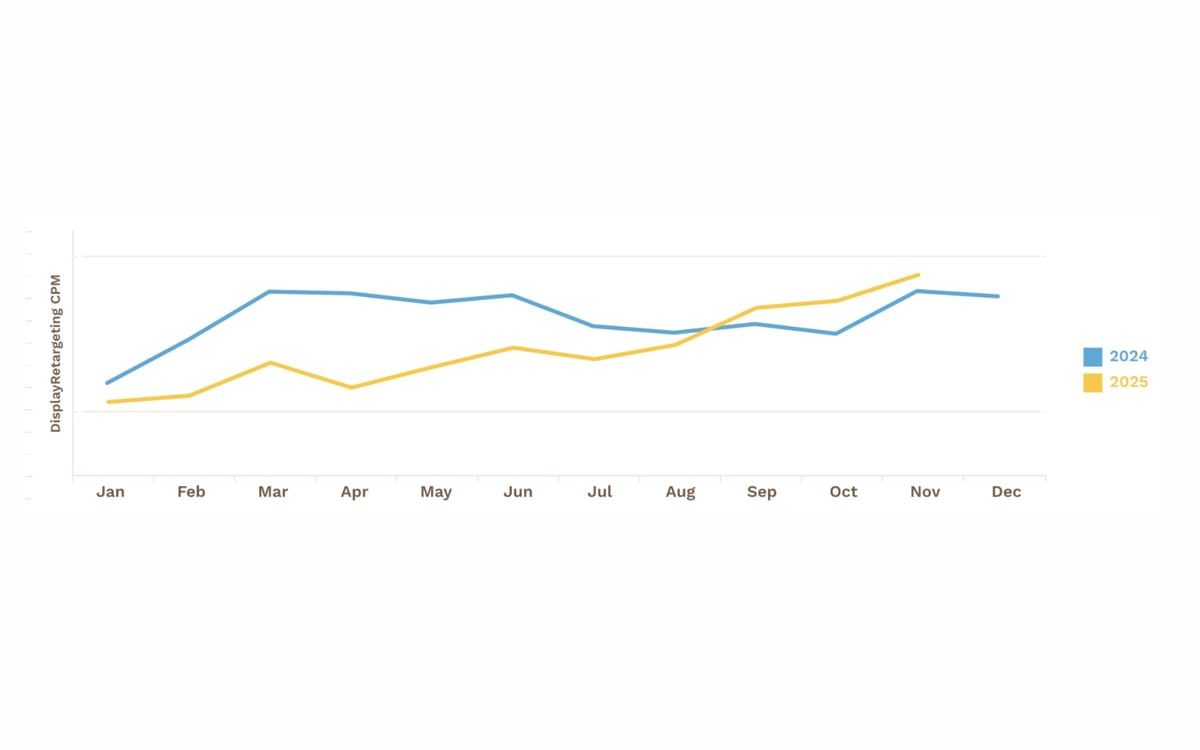

AdRoll released its Q4 2025 State of Digital Advertising Report on December 3, revealing display retargeting cost per mille surged 11% year-over-year from September through November as an unusually early holiday shopping season and widening economic inequality intensified competition across digital channels.

The report, based on data from more than 20,000 online businesses, showed both display retargeting and prospecting costs climbed sharply during the three-month period. Display prospecting CPMs increased 2% on average compared to last year, while account-based marketing campaign CPMs rebounded, narrowing their year-over-year decline to just 10% in November after hitting a 23% drop in August.

Subscribe PPC Land newsletter ✉️ for similar stories like this one

According to the company, much of the spike can be traced to a holiday season that began nearly two months ahead of schedule. Brands pulled promotions forward to hedge against an uncertain economic outlook, while shoppers moved early to secure deals and spread out spending as inflation worsened. This concentrated ad spend pushed CPMs sharply upward, especially across high-intent retargeting inventory.

"Marketers are entering one of the most complex holiday seasons we've seen in years," said Vibhor Kapoor, chief business officer at AdRoll. "When demand pulls forward and AI reshapes discovery paths, brands can no longer rely on last-minute spend or single-channel strategies. Success now depends on full-funnel visibility, experimentation, and tight orchestration across every team influencing the customer journey."

The aggressive surge in CPMs across display retargeting and prospecting channels in September and October was driven by fundamental shifts in market behavior and underlying economic realities. Display retargeting costs experienced a sharp turnaround in early Q4. After narrowing the year-over-year gap through the summer, CPMs surged significantly from September to November, surpassing last year's level by an average 11%. This aggressive upward trend confirmed intense demand for retargeting inventory, driven by the early and highly competitive start to the holiday spending season.

Display prospecting followed suit. After months of narrowing the year-over-year gap, prospecting CPMs surged in September and October, surpassing last year's level by 6%. This marked a strong recovery and signaled that advertisers were aggressively building top-of-funnel audiences early, driving up acquisition costs as they vied for consumer attention. Then, as brands allocated budgets toward retargeting in November, prospecting CPMs dropped.

Account-based marketing CPMs also saw a strong recovery, narrowing the year-over-year decline to just 10% in November from 23% in August. This rebound suggested that B2B marketers, after a typical summer slowdown, were investing again to fill pipelines and capture year-end budget cycles.

Economic polarization further amplified the surge. With higher-income households driving a disproportionate share of spending and lower-income households pulling back, advertisers concentrated budgets on smaller, more affluent segments. That shift intensified competition for limited premium inventory, with higher-income verticals seeing the steepest CPM increases.

The K-shaped economy in the United States, where consumer spending is primarily driven by higher-income households while lower-income households pull back, increased competition among advertisers. Businesses are increasingly targeting a smaller, more affluent group of high earners who have more disposable income to spend. This focus on a premium, highly desirable demographic increased competition due to limited advertising inventory, which pushed CPMs higher.

AdRoll examined CPM data across verticals and noticed diverse trends in certain verticals. Verticals that are geared toward higher income households and are less sensitive to economic outlook, such as Pets Services, saw a strong increase in average CPM in September and October. On the other hand, verticals with a wider customer base that are more sensitive to economic downturns, such as Hobbies & Interests, saw their average CPM stagnant or in decline.

U.S. inflation reached its highest level of 2025 in September, hitting 3%. Consumer sentiment fell to a three-year low during the prolonged federal government shutdown, with the consumer sentiment index dropping to its lowest level in more than three years in November, only slightly above its worst level on record. Yet consumer spending remained resilient through September and October according to Bank of America Consumer Checkpoint report, creating a market defined by volatility rather than clarity and requiring marketers to plan for agility as much as performance.

Early holiday shopping data from Adobe and Salesforce showed the growth trend was likely to continue into November and December. As predicted by BazaarVoice, this year's holiday shopping season started early—almost two months earlier than usual—amid ongoing economic concerns.

This early start was fueled by a dual push from both businesses and consumers. Businesses accelerated holiday promotions in effort to capture consumer spending before potential downturns or budgeting freezes. Consumers also began shopping earlier to take advantage of deals and spread out their spending to offset anticipated price hikes caused by worsening inflation. This condensed and accelerated spending cycle intensified competition in September and October, driving CPMs above last year's levels.

Google launched four new Demand Gen features on November 17 targeting the holiday shopping season. The product update, branded as the November "Drop," expanded advertiser control over creative optimization, brand safety parameters, and testing methodologies across YouTube, Discover, and Gmail placements. Research showed 61% of shoppers reported being more selective with spending due to concerns about future economic conditions.

Consumer spending patterns demonstrated significant changes entering the 2025 holiday period. Research showed 34% of consumers began holiday shopping in October or earlier, with 71% citing tariff concerns as their top worry heading into peak season. This early shopping behavior created challenges for marketers attempting to optimize campaign timing and budget allocation across promotional periods that now span multiple months.

Looking ahead to 2026, AdRoll identified three forces that will shape marketing strategies: persistent economic uncertainty that requires nimble budget allocation; AI agents that will increasingly mediate product discovery, comparison, and recommendations; and the growing necessity of coordinated cross-functional teams to deliver efficient, full-funnel performance.

The economic volatility seen in 2025 driven by trade policy uncertainty, inflation fears and job growth worries, suggested that cost-conscious consumer behaviors will persist. Successful marketers need to be agile, focused on campaign efficiency, and ready to pivot strategies faster than ever to manage fluid consumer confidence and economic forecasts.

The adoption of generative AI continues to grow, and in 2026, AI agents, not search engines or social feeds, will increasingly handle product discovery, comparison, and recommendations for consumers and business buyers. This inserts a new layer between brands and their customers, obscuring traditional conversion paths.

Buy ads on PPC Land. PPC Land has standard and native ad formats via major DSPs and ad platforms like Google Ads. Via an auction CPM, you can reach industry professionals.

Marketing success will require full-funnel awareness. The report recommended investing in brand awareness channels like connected television, podcasts, and premium display ads to ensure brand awareness and affinity among target customers. Particularly for B2B marketers, full-funnel account-based marketing means going beyond acquisition to cover retention and upsell strategies.

AI optimization—including AI Experience Optimization and Generative Engine Optimization—will become critical. Monitoring how various AI platforms interpret brand information and how often they recommend it becomes essential. Adapting content and product data to be easily digested, indexed, and cited by generative AI models will determine visibility.

In a complex, multi-channel world defined by AI and changing consumer behavior, siloed teams are destined to fail. Marketing success takes a village. Achieving optimal return on ad spend and return on investment will require deep coordination across all channels—web, mobile, social, connected television—and teams including marketing, sales, and product.

Marketers must break down organizational silos to ensure coordinated targeting with a unified view of the customer across all platforms. Budget synchronization requires bidding and budget allocation optimized dynamically across the organization's entire media portfolio. Account-based marketing campaigns must be perfectly synchronized with B2B sales outreach to deliver a consistent narrative to target audiences.

The advertising industry has seen significant investment in agentic AI capabilities throughout 2025. Multiple platforms launched autonomous systems designed to handle campaign management, targeting recommendations, and analytics workflows. Amazon introduced Ads Agent on November 11, enabling natural language campaign creation and audience segment recommendations. Google deployed autonomous shopping capabilities on November 13, including agentic checkout that autonomously purchases tracked items when prices drop.

McKinsey analysis published in July 2025 identified agentic AI as the most significant emerging trend for marketing organizations, with $1.1 billion in equity investment flowing into the technology during 2024. The shift represents a transition from chatbot interactions to virtual coworkers that can independently manage complex workflows.

The concentration of consumer spending during holiday periods makes fourth-quarter planning critical for retailers and advertisers. Retail media networks are projected to capture approximately 20% of total global advertising revenue by 2030, exceeding $300 billion according to previous research. Digital advertising platforms have responded to holiday shopping patterns with enhanced capabilities, with Amazon's advertising revenue reaching $17.7 billion in third quarter 2025, growing 22% year-over-year.

Platform dynamics continued shifting throughout the holiday season, with Amazon expanding bot restrictions on November 24 while simultaneously deploying aggressive autonomous shopping capabilities through its Rufus AI assistant. The contradiction revealed strategic positioning around walled product data while deploying proprietary AI agents that complete purchases without human oversight.

The AdRoll State of Digital Advertising Report offers marketers insights into business and advertising trends. The report is based on AdRoll's performance statistics of more than 20,000 online businesses across finance, beauty and fashion, fitness, technology, travel, and other industries. The information in the report is updated on a quarterly basis, providing average CPM trends for display retargeting, display prospecting, and account-based marketing.

CPM, or cost per mille, is an advertising metric that measures the average cost of showing an ad one thousand times. CPM, similar to the cost of goods, is determined by supply and demand. In the digital advertising world, publishers serve as the suppliers; the websites or mobile apps that host and deliver ads to advertisers' target audiences.

The selling and buying of digital ads on the web is typically conducted in an auction format that can be handled programmatically by two types of platforms: the supply-side platform, representing the publishers, and the demand-side platform, representing the advertisers. Since the amount of advertising space offered by the publishers doesn't typically fluctuate, changes in CPM are mostly driven by advertisers' demand for ads.

Subscribe PPC Land newsletter ✉️ for similar stories like this one

Who: AdRoll, an AI-powered connected advertising platform, analyzed data from more than 20,000 online businesses across finance, beauty and fashion, fitness, technology, travel, and other industries. Vibhor Kapoor, chief business officer at AdRoll, provided analysis.

What: Display retargeting CPMs surged 11% year-over-year from September through November, while display prospecting CPMs increased 2% on average. Account-based marketing campaign CPMs rebounded, narrowing their year-over-year decline to 10% in November from 23% in August. The report identified two primary drivers: an unusually early holiday shopping season starting nearly two months ahead of schedule, and a K-shaped economy where higher-income households drove disproportionate spending while lower-income households pulled back.

When: The CPM surge occurred from September through November 2025, with the Q4 2025 State of Digital Advertising Report released on December 3, 2025. U.S. inflation reached 3% in September 2025, the highest level of 2025, while consumer sentiment dropped to a three-year low in November during the prolonged federal government shutdown.

Where: The analysis covered digital advertising costs across the United States market, examining display retargeting, display prospecting, and account-based marketing campaigns across multiple industries including finance, beauty and fashion, fitness, technology, and travel sectors.

Why: The CPM increases resulted from businesses accelerating holiday promotions to capture consumer spending before potential economic downturns, while consumers began shopping earlier to secure deals and spread out spending as inflation worsened. Economic polarization created a K-shaped economy where advertisers concentrated budgets on smaller, more affluent segments, intensifying competition for limited premium inventory and pushing costs higher. The report projected three forces will shape 2026 marketing strategies: persistent economic uncertainty requiring nimble budget allocation, AI agents increasingly mediating product discovery and recommendations, and growing necessity of coordinated cross-functional teams.