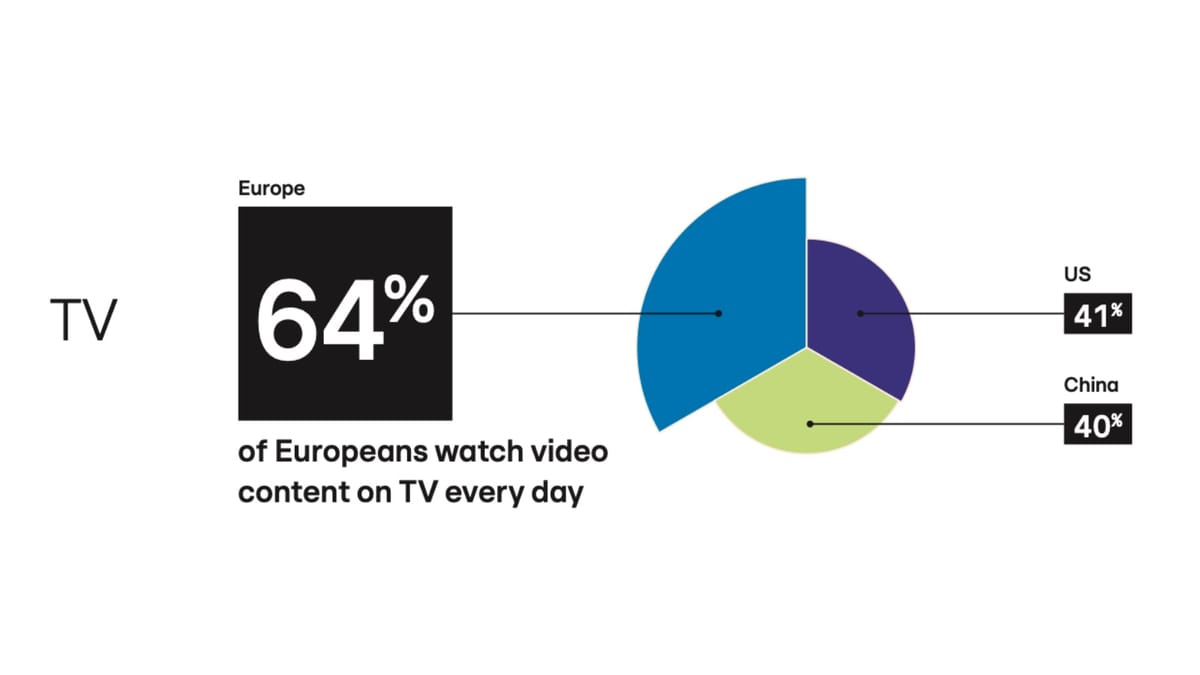

Europe watches TV daily at 64%, yet SVOD daily use collapses to 19%

RTL AdAlliance Living Room Study 2026: 64% of Europeans watch TV daily across 17 markets, but Netflix daily use reaches only 19% despite 53% subscription reach.

RTL AdAlliance Living Room Study 2026: 64% of Europeans watch TV daily across 17 markets, but Netflix daily use reaches only 19% despite 53% subscription reach.

RTL AdAlliance published the fifth edition of its Living Room Study on March 12, 2026, a large-scale survey of video consumption habits across 17 countries. The research, covering nearly 15,000 respondents aged 18 to 64, draws a picture of a European media landscape that is simultaneously more stable and more complicated than the industry narrative of fragmentation suggests. For media planners and advertisers, the numbers contain both reassurance and challenge in roughly equal measure.

The fieldwork ran from January 19 to February 4, 2026, using online questionnaires across three continents. Two markets - China and Hungary - appear for the first time. The remaining 15 are Austria, Belgium, Denmark, Finland, France, Germany, Italy, the Netherlands, Norway, Poland, Spain, Sweden, Switzerland, the UK, and the US. Samples were nationally representative, adjusted for population size, with between 700 and 1,000 respondents per country. The questionnaire covered more than 130 streaming platforms and asked each participant 30 questions, making it one of the more granular multi-market studies of its kind.

The headline finding is straightforward. Sixty-four per cent of Europeans watch video on their television set every day. That figure sits 23 percentage points above the US rate and 24 points above China, according to the study. Ninety per cent of Europeans have at least one television at home, and 86 per cent of those surveyed say the living room is where they watch linear TV most often. The bedroom ranks second, at 22 per cent.

Those numbers have remained broadly stable across the five editions of this study. Marion Ranchet, Founder of Streaming Made Easy and a contributor to the 2026 edition, addresses this directly in the foreword: "For five years now, the Living Room Study has tracked how Europeans watch video content. Every edition has returned the same core finding: the living room is not losing ground in Europe, it is gaining relevance." She adds that 83 per cent of European respondents say they watch video in their living room, compared with 58 per cent in the United States.

The contrast with China is particularly sharp on device choice. European viewers rely primarily on the television set; in China, smartphones lead video consumption, with 81 per cent using them daily for video versus 58 per cent in Europe and 61 per cent in the US. On computers, the gap is smaller but reverses: 34 per cent of Europeans watch video on a computer daily, compared with 32 per cent in China and 26 per cent in the US.

The smart TV homepage is now the dominant gateway to streaming content on the television. Fifty-eight per cent of European viewers use it as their primary entry point. A set-top box follows at 27 per cent, an HDMI stick or key at 21 per cent, screen mirroring at 16 per cent, and a gaming console at 10 per cent. European viewers use an average of 1.3 different devices to access video on their TV - compared with 1.5 in the US and 1.8 in China.

Screen mirroring is noted as a specific tension point. When viewers cast directly from a smartphone or laptop to a television screen, they bypass the TV operating system entirely. That removes the platform's ability to shape content discovery or collect behavioral data. Telecom operators and TV OS providers have been actively attempting to limit this behavior, since it effectively renders their homepage - and its data layer - invisible.

One of the more striking findings is the persistence of shared viewing. Forty-five per cent of Europeans say they often watch broadcaster video-on-demand (BVOD) platforms with another person - a partner, friend, or family member. Co-viewing is highest in Denmark and Norway, both at 55 per cent, and the UK at 53 per cent. Italy sits at 33 per cent and Switzerland at 32 per cent.

The pattern is not driven by older viewers alone. Among 18- to 24-year-olds, 68 per cent say that watching video with others strengthens social bonds. That figure falls to 63 per cent for the 25-to-34 cohort, drops to 40 per cent among 35-to-49-year-olds, and rises again to 54 per cent in the 50-to-64 group. Spain shows the strongest national sentiment on this point: 72 per cent of Spanish respondents agree that watching with other people fosters strong social bonds.

Ranchet frames this in terms that carry direct implications for advertising: "Attention is the word our industry uses most, and understands least. We measure it as an individual metric - one person, one screen, one impression - but European viewing does not follow that model. Here, attention is collective, it compounds." The argument is that co-viewing changes what an advertising impression is worth, and what kind of creative actually registers.

The study also touches on sentiment toward social platforms. According to the report, 73.6 per cent of Europeans say social media has lost its capacity to create real social connections - the highest of any region in the study. The US figure is 72.2 per cent. It is a finding that sits uncomfortably alongside the sustained investment in social advertising, though it does not directly measure ad effectiveness.

When European viewers turn on a TV set, 62 per cent go to Total TV - the combined category of linear and BVOD - first. Linear TV alone accounts for 48 per cent of first destinations, down three percentage points from the 2025 edition. BVOD accounts for 14 per cent, up six points year on year - one of the larger directional shifts in the data. Subscription video-on-demand (SVOD) follows at 29 per cent, flat year on year. Hosting platforms such as YouTube account for 9 per cent, also flat.

When a viewer's favourite programme is available on multiple platforms simultaneously, 69 per cent of European respondents say they would choose Total TV first. Linear alone captures 44 per cent; BVOD takes 25 per cent. In the US, Total TV draws 58 per cent in the same scenario, with YouTube attracting 30 per cent - roughly two-and-a-half times its European rate. That difference reflects a structural one: in the US, streaming emerged partly as an alternative to expensive pay-TV; in Europe, free-to-air television has remained a baseline for most households.

Forty-four per cent of Europeans watch Total TV daily, according to the study. SVOD usage is high but not necessarily habitual: 80 per cent of Europeans watch SVOD at least once a month, and 68 per cent at least once a week. BVOD sits at 61 per cent monthly and 45 per cent weekly. Free ad-supported streaming TV (FAST) channels remain the smallest category, at 11 per cent monthly and 6 per cent weekly.

For many years, BVOD was associated primarily with younger viewers using it for catch-up. The 2026 data complicates that assumption. Weekly BVOD reach is 40 per cent among 18-to-24-year-olds, 46 per cent among 25-to-34-year-olds, 44 per cent among 35-to-49-year-olds, and 52 per cent among the 50-to-64 cohort. The oldest segment now shows the highest weekly reach.

Forty-one per cent of European BVOD users watch live content on their TV through BVOD platforms. That is a meaningful finding given the general assumption that BVOD functions primarily as an on-demand replay service. The live usage share suggests broadcaster platforms are being treated, at least in part, as a more flexible way to watch scheduled television - not as a replacement for it.

Denmark shows the strongest BVOD engagement in the study: 72 per cent of Danish respondents watch BVOD on their TV at least once a week, which is five percentage points higher than SVOD in that market.

Netflix reaches a subscription or access rate of 53 per cent across the European markets in the study. Amazon Prime Video reaches 36 per cent, Disney+ 29 per cent. But daily viewing tells a different story. Only 19 per cent of Europeans watch Netflix every day. Amazon Prime Video reaches 8 per cent for daily viewing; Disney+ just 7 per cent.

The gap between subscription reach and daily engagement is one of the study's more pointed findings for advertisers building media plans around SVOD inventory. As SVOD platforms have expanded their ad-supported tiers aggressively in Europe, with Amazon Prime Video's ad-tier penetration jumping from 26 per cent to 68 per cent between 2025 and 2026 in the study's data, the actual time viewers spend on those platforms does not scale at the same rate as subscriber numbers.

The study notes that Amazon Prime Video's ad tier rose fastest - from 26 per cent in 2025 to 68 per cent in 2026 among those surveyed. Netflix moved from 22 to 35 per cent, and Disney+ from 17 to 40 per cent. Regional variance is wide. Italy shows 87 per cent ad-tier penetration for Amazon Prime Video and 69 per cent for Netflix. Nordic markets, where ad tiers were launched later, show more limited uptake.

Fifty-five per cent of Europeans now subscribe to at least one paid ad-supported tier, whether on BVOD or SVOD. For media buyers, that figure represents a significant shift in inventory availability across premium video environments - one that RTL AdAlliance has sought to address with its AdManager platform since its March 2025 launch.

YouTube occupies a different position in Europe than in the US. Fifty-one per cent of European viewers watch content creators on YouTube, which is 17 percentage points above the US rate. Thirty-eight per cent watch Shorts, 14 points above the US figure. Music videos reach 46 per cent. But on Netflix, Amazon Prime Video, and Disney+, the vast majority of usage - 82 to 85 per cent - is for on-demand movies and series. Live or replay content on those platforms reaches only 10 to 13 per cent of their respective user bases.

The on-demand concentration on SVOD and the creator-driven engagement on YouTube describe two distinct viewing relationships, with different implications for the kind of advertising that can be placed alongside each. Content that attracts passive, scheduled viewing on a broadcaster platform carries different audience attention dynamics from content chosen algorithmically on a hosting platform.

Local content continues to shape broadcaster strength. Fifty-three per cent of Europeans say they often watch local content on linear TV. BVOD reaches 40 per cent for local content viewing. Among SVOD services in Europe, local content viewing sits at 38 per cent. Hungary leads on the importance of local content, with 80 per cent agreeing it matters to have access to local video. Sweden sits lowest among European markets at 60 per cent.

The study contains a section on advertising trust that carries weight for media planning. Linear TV is the most trusted advertising environment in Europe, with 61 per cent of respondents saying they trust an unfamiliar brand after seeing an ad on it. Cinema matches that at 61 per cent. Radio reaches 60 per cent, and magazines and newspapers 58 per cent. BVOD sits at 56 per cent. SVOD reaches 51 per cent, hosting platforms 40 per cent, and social media 33 per cent.

The trust gap between linear TV and social media is 28 percentage points. Between BVOD and social media, it is 23 points. These figures matter because European broadcasters have increasingly positioned themselves as brand-safe alternatives to global platforms in conversations with international advertisers, with RTL AdAlliance among the most active in making that case formally. RTL Group's CEO of RTL AdAlliance, Stéphane Coruble, has stated publicly that 75 to 80 per cent of advertising investment flows to five global platforms, and that European broadcaster alliances represent an alternative route.

On ad irritation, the data points to a specific problem with SVOD. Sixty per cent of Europeans say ads on SVOD platforms annoy them, 14 percentage points higher than the irritation rate for BVOD. The study attributes this primarily to a comprehension gap: 83 per cent of respondents understand why ads appear on linear TV, and 71 per cent understand BVOD's ad model. On SVOD, understanding drops sharply - only 50 per cent say they understand why ads appear there, compared with 75 per cent for hosting platforms. When the purpose of an ad-supported tier is unclear to a viewer who believed they were paying for an ad-free experience, tolerance drops. That structural confusion is a product of how ad tiers were introduced at SVOD platforms - often as opt-in lower-cost alternatives rather than as the default, making the presence of ads feel anomalous rather than expected.

The study lands at a specific moment in European broadcasting. RTL Group cut its 2025 profit outlook in November 2025, reducing full-year adjusted EBITA guidance from approximately €780 million to €650 million, citing weak television advertising markets in Germany and France. RTL subsequently announced 600 job cuts in Germany in December 2025. Against that backdrop, the Living Room Study functions partly as a data-driven argument for broadcaster inventory's continued value - a positioning exercise as much as a research product.

For the advertising community, the more actionable questions are about where viewing time actually goes and what it converts to in terms of ad receptivity. The study's finding that BVOD's weekly reach now exceeds SVOD in Denmark and that trust in broadcaster environments consistently outperforms social platforms and hosting services provides planners with data points for justifying broadcast allocations in media mixes that have been shifting toward programmatic digital. The 16 per cent daily BVOD rate, while still below linear TV's 39 per cent daily reach, is growing.

The six-point year-on-year increase in BVOD as a first destination when turning on a TV set is perhaps the number most likely to matter to connected TV buyers and broadcaster sales teams in the near term. Whether it reflects a durable behavioral shift or a base effect from platforms launching in new markets - BVOD ad tiers were not available in some Nordic countries in 2025 - is a question the annual cadence of this study will be positioned to answer.

Who: RTL AdAlliance, the international advertising sales house of RTL Group, together with contributor Marion Ranchet of Streaming Made Easy, and research partner Norstat.

What: The fifth edition of the annual Living Room Study, covering video consumption habits across 17 countries with approximately 15,000 respondents aged 18-64, surveying more than 130 streaming platforms. Key findings include 64 per cent daily TV viewing in Europe, a 6-point year-on-year increase in BVOD as a first destination on the TV set, a 28-percentage-point trust gap between linear TV and social media for advertising, and a structural gap between SVOD subscription reach and daily engagement rates.

When: Fieldwork ran from January 19 to February 4, 2026. The study was published on March 12, 2026.

Where: Fifteen European countries - Austria, Belgium, Denmark, Finland, France, Germany, Hungary, Italy, the Netherlands, Norway, Poland, Spain, Sweden, Switzerland, and the UK - plus China and the United States. Two markets, China and Hungary, appear for the first time in this edition.

Why: The study tracks how viewing habits across living rooms shape the environment for video advertising in Europe. For media buyers, the data on BVOD growth, SVOD engagement gaps, ad-tier irritation, and trust levels by media type informs planning decisions around broadcast, streaming, and digital video allocations. The research also provides context for broader industry debates about the relative value of European broadcaster inventory versus global platform reach.