European advertisers struggle with trust gaps despite digital growth forecasts

IAB Europe's first comprehensive digital advertising report reveals 70% frustration with performance measurement while CTV investment momentum builds across continent.

IAB Europe's first comprehensive digital advertising report reveals 70% frustration with performance measurement while CTV investment momentum builds across continent.

IAB Europe today published its inaugural Attitudes to Digital Advertising Report, mapping an ecosystem where investment continues expanding while fundamental measurement and operational challenges threaten to constrain the pace of growth. The organization surveyed over 170 advertising professionals between October and November 2025, capturing perspectives from advertisers, agencies, publishers, and ad tech companies across 27 European markets.

More than two-thirds of respondents anticipate increased digital advertising investment or revenue over the next 12 months, most commonly within the 1-25% range. The projection signals steady rather than explosive expansion, according to the report findings. Agencies expressed the strongest confidence, with nearly two-thirds expecting growth and zero respondents forecasting declines. Ad tech companies projected healthy expansion, while publishers demonstrated the most cautious outlook and advertisers presented polarized sentiment reflecting sector-specific pressures.

Performance and efficiency dominate investment decisions. The report identified 61% of respondents citing outcomes as their top driver, followed by operational efficiencies at 56% and cost optimization at 54%. Stakeholder priorities diverged significantly, with advertisers emphasizing cost controls at 70%—by far the highest among any group. Agencies prioritized performance at 60% alongside transparency at 50%, reflecting responsibility for demonstrating clear client value. Publishers focused on operational effectiveness at 71%, while ad tech companies leaned most heavily into performance drivers at 72%.

"This report shows an industry that continues to grow, but where fragmentation is holding progress back," IAB Europe Industry Development & Insights Director Marie-Clare Puffett stated. "As investment increases and new channels scale, clearer measurement and more unified approaches will be essential."

The survey documented significant maturity gaps in programmatic adoption across channels. Display advertising achieved the strongest penetration, with 30% of respondents reporting full programmatic operations. Video reached 28% full adoption, though the format recorded higher "Don't know" responses suggesting execution clarity issues. Connected TV adoption remained fragmented at 22% fully programmatic, with 18% indicating uncertainty. Audio lagged substantially—while 26% reported full programmatic penetration, 25% responded "Don't know," highlighting both slower adoption and limited visibility.

Cross-channel activation proved particularly limited. Only 17% of respondents reported that 81-100% of their campaigns activated across multiple formats. Advertisers demonstrated the most siloed operations, with 56% reporting just 1-20% cross-channel activation. Agencies led integration efforts, with 40% reporting 61-80% of campaigns spanning channels.

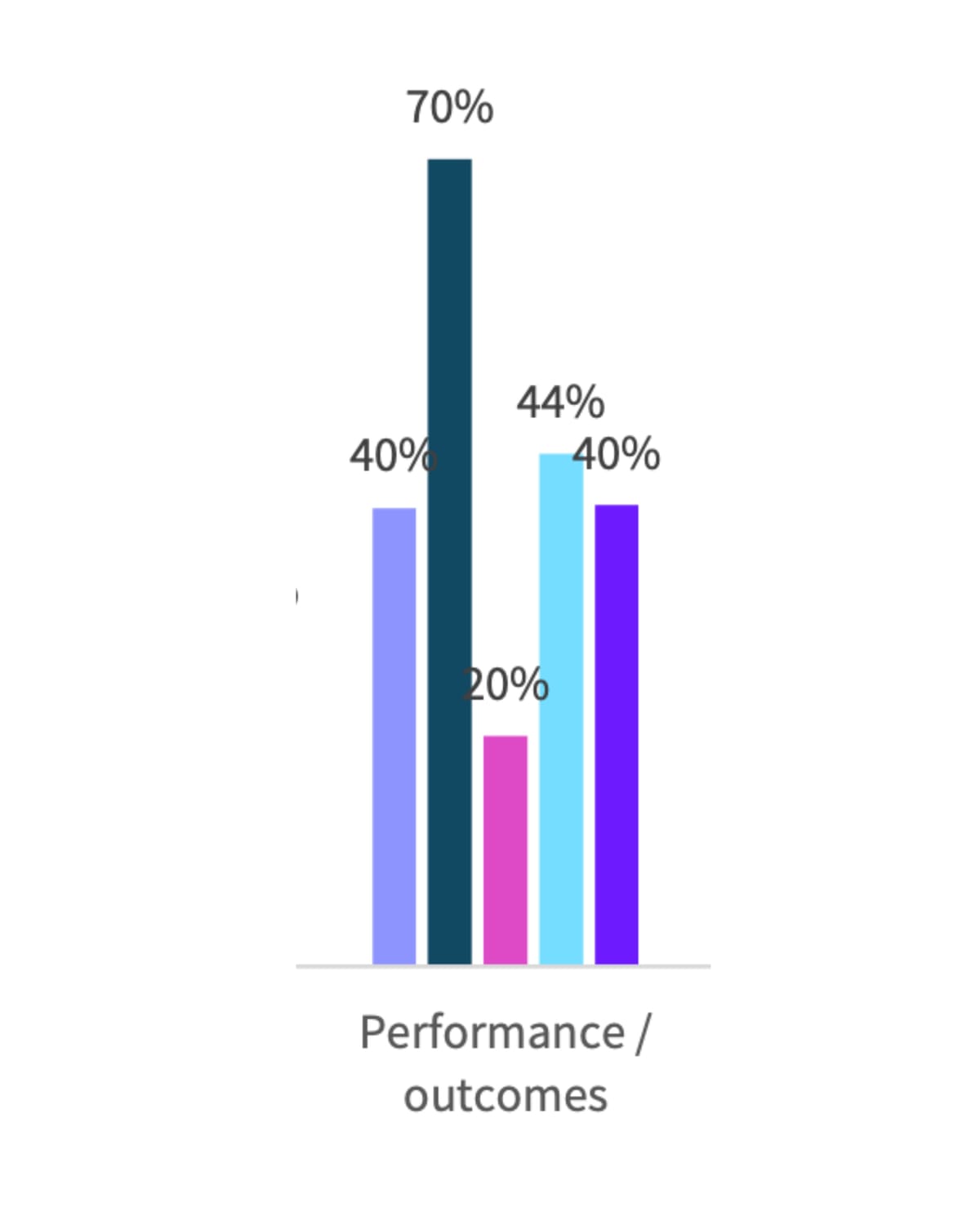

Media quality issues emerged as the most widely cited obstacle to growth. Over half of respondents—52%—identified fraud, brand safety, viewability, and transparency concerns as major barriers. Operational complexity followed closely at 51%, encompassing measurement, performance management, data usage, and creative execution challenges. External pressures including political and economic uncertainty constrained 45% of respondents, while talent shortages affected 42%.

Advertisers stood apart in their acute frustration with performance measurement. A striking 70% cited outcomes as their primary barrier—significantly higher than any other stakeholder group. Publishers and ad tech companies felt operational and macro-economic pressures more intensely, with publishers reporting 61% concern for both operational elements and the broader economic climate.

Measurement practices varied dramatically by channel, revealing how stakeholders evaluate success differently across formats. CTV attracts evaluation primarily through brand and audience metrics, reinforcing the format's role as a premium, upper-funnel environment. Brand metrics reached 36% importance for CTV, with audience metrics at 31% and attention metrics at 27%. Display remained the most performance-driven channel, with interaction metrics at 50%, sales metrics at 52%, and media efficiency metrics at 43%. Video blended brand and performance expectations, with quality metrics particularly important at 48%—reflecting publisher and ad tech emphasis on viewability, fraud prevention, and brand safety. Audio continued as the least measured channel, suggesting limited maturity or strategic focus.

The disconnect between channel measurement approaches reflects broader standardization challenges. Cross-media measurement efforts are now targeting European standards fragmentation, with IAB Europe announcing a comprehensive strategic review examining initiatives across European markets.

Data strategy preferences showed clear directional shifts toward privacy-centric approaches. First-party data already underpins 81% of current strategies, with future adoption projected to reach 76%—despite the percentage appearing lower, this reflects consolidation as organizations refine their data infrastructure. Third-party data remains widely used at 50% currently, but stakeholders signaled more selective future deployment at 57%. Second-party data gained traction, rising from 42% current usage to 33% planned adoption, reflecting retail media network growth, clean-room collaborations, and publisher alliances.

A notable 25% of respondents operate without any audience data, and this proportion barely shifts in future plans—highlighting persistent maturity gaps particularly among advertisers and publishers where structural barriers or contextual targeting reliance may limit progress.

Curated marketplaces demonstrated inconsistent adoption and often poor understanding across the ecosystem. While 8% reported 81-100% investment in curated environments, 23% responded "Don't know"—the highest uncertainty rate for any transaction type examined. Agencies and ad tech providers drove adoption, using curated environments to improve quality, transparency, and supply-path efficiency. Advertisers and publishers showed lower engagement and higher uncertainty, suggesting curated marketplaces remain a technical backend optimization rather than a clearly communicated strategic choice.

Connected TV emerged as the standout growth area for the next 12 months. Nearly 70% of respondents identified CTV as a top opportunity, with agencies and ad tech especially confident in continued expansion. The format's momentum builds on infrastructure developments including standardized ad formats and improved measurement capabilities.

AI ranked as the second-strongest driver at 37% overall, led by advertisers at 60% who see significant potential in automation, optimization, and predictive modeling. Retail and Commerce Media continues gaining momentum particularly among advertisers and publishers, reflecting the appeal of first-party data and closed-loop measurement. Digital out-of-home showed polarized expectations—strongly backed by ad tech at 50% but not yet embraced by advertisers at 0% or publishers at 0%.

Wayne Tassie, Chair of IAB Europe's Advertising & Media Committee, emphasized the report's strategic timing. "Building on more than a decade of programmatic research, this expanded study captures the realities of today's market, from growing investment in CTV and Retail Media to the accelerating impact of AI," Tassie stated. "By bringing together perspectives from across the ecosystem, it offers a clear and balanced view of where the industry stands."

The methodology encompassed C-suite and Director-level leaders accounting for a majority of participants, complemented by substantial mid-management representation. Stakeholder groups included 14% advertisers, 21% agencies, 36% ad tech providers, and 29% publishers. Geographic coverage spanned pan-European and global-with-European-remit roles alongside respondents from more than 25 individual markets.

The findings arrive as European digital advertising reached €118.9 billion in 2024 with 16% year-over-year growth, crossing the €100 billion threshold for the first time. Retail media spending achieved 22.1% growth, outpacing the broader market by nearly four times.

The report signals that while digital advertising investment trajectories remain positive, the industry's ability to fully capitalize on opportunities depends on addressing persistent quality, measurement, and operational consistency challenges. Investment flows toward channels demonstrating clear attribution and measurable outcomes, with performance accountability increasingly non-negotiable for budget allocation decisions.

Who: IAB Europe surveyed over 170 advertising professionals including advertisers (14%), agencies (21%), ad tech providers (36%), and publishers (29%) from C-suite, Director, and mid-management levels across 27 European markets.

What: The inaugural Attitudes to Digital Advertising Report documents steady investment growth expectations (67% anticipating increases), identifies performance measurement as the primary barrier for 70% of advertisers, reveals programmatic adoption gaps particularly in CTV and audio, and positions Connected TV as the dominant growth opportunity for the next 12 months.

When: The survey ran between October and November 2025, with results published on January 15, 2026, representing the organization's evolution from a decade of programmatic-focused research to comprehensive digital advertising ecosystem analysis.

Where: The report covers pan-European perspectives alongside 25+ individual European markets, documenting an ecosystem that reached €118.9 billion in 2024 with retail media achieving 22.1% growth outpacing the broader 6.1% advertising market expansion.

Why: The research addresses critical industry needs for standardized measurement frameworks, unified cross-channel approaches, and clear benchmarking as European digital advertising transitions from fragmented adoption patterns to mature strategic infrastructure requiring accountability, transparency, and operational consistency for continued growth.