FAST (Free Ad-Supported Streaming TV) channels have reached 27% household adoption across Europe, according to a pan-European consumer study published on March 24, 2026, by CTV ad-tech company ShowHeroes and Omnicom Media Netherlands. The findings, drawn from 4,377 respondents aged 18 to 65 across six markets - the UK, Germany, France, Italy, Spain, and the Netherlands - paint a picture of a subscription economy that has hit a structural ceiling, with free, ad-supported alternatives filling the gap.

The study, titled "The Rise of FAST: Consumer Preferences in Connected TV," arrives as the streaming industry confronts a fundamental tension: audiences want more content but are unwilling to pay for it. European households now maintain an average of two to three paid streaming subscriptions, according to the research, and 59% say they want to lower those costs. Perhaps more striking, 37% say they would cancel a paid service outright if advertising were introduced without meaningful price reductions.

That dynamic - consumers walking away from platforms that add ads without cutting the bill - sits at the heart of what the study calls a structural rebalancing. The market is not contracting. It is redirecting.

Subscription fatigue is the phrase that anchors the report's framing. Ilhan Zengin, CEO at ShowHeroes Group, described it plainly: "Subscription fatigue is not cyclical; it is structural. The European streaming market has reached economic equilibrium. FAST represents the next phase of Connected TV, where scale, engagement and ad acceptance converge."

The numbers market by market

Country-level data reveals meaningful variation. The UK and Italy jointly lead at 37% adoption, while Spain has experienced rapid monthly reach growth landing between 31% and 35% - a trajectory the study describes as making it a frontrunner among major European markets. Germany sits at 26%, France at 23%, and the Netherlands at 16%, though the Dutch market is characterized as traditionally subscription-heavy with an average of three to four paid subscriptions per household.

These are not marginal figures. FAST channels surged 42% globally between mid-2023 and early 2025 according to Gracenote data, underscoring that the European numbers reported by ShowHeroes and Omnicom track with a broader international pattern.

The growth potential is further evidenced by intent data in the study. More than 35% of non-users across the six markets say they plan to try FAST channels within the next three months. In Italy, 43% of non-users expressed readiness to try - the highest latent demand figure across any surveyed country.

Not casual viewing: prime-time habits

One of the most consequential findings for advertisers is that FAST viewing is not relegated to secondary or incidental use. Among current FAST users, 62% watch in the evening - during conventional prime time - and 57% tune in several times per week. Satisfaction is high: 66% report being "highly satisfied" with the experience.

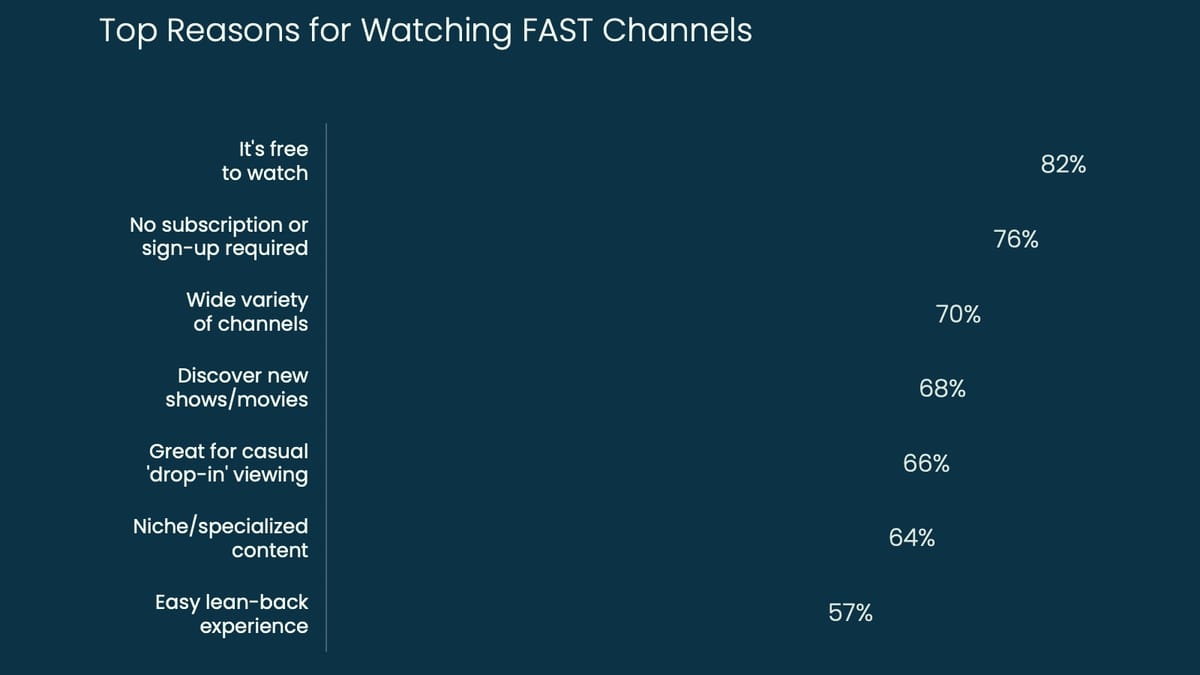

What drives people to FAST in the first place? Cost is the dominant factor: 82% of FAST users cite the fact that it is free as their primary reason, and 76% value the absence of any subscription or sign-up requirement. A wide variety of channels follows at 70%, then content discovery at 68%, and casual "drop-in" viewing at 66%.

The study also recorded a notable behavioral shift: 44% of respondents say they have replaced some of their social media or gaming time with Open CTV viewing. News consumption on FAST is also growing within the data - in the Netherlands, news viewership on FAST channels climbed from 27% to 36%, while in Germany it moved from 27% to 39%.

Content preferences vary by country. In the Netherlands, sport (46%), action (41%), and documentaries (40%) lead. German viewers favor comedy (51%), action (49%), and crime (41%). In the UK, drama (51%) and documentaries (49%) dominate alongside sport (49%). Spain leans toward comedy (62%) and documentaries (61%). These granular preferences matter for advertisers developing contextual targeting strategies across European markets, a challenge explored in recent industry work around CTV's contextual gap.

The incremental reach argument

Perhaps the most commercially significant data in the study involves audience exclusivity. In France, 56% of FAST channel users do not use any SAVOD platform. In the Netherlands, that figure is 54%. The UK stands at 41%, Germany at 40%, Italy at 33%, and Spain at 27%.

For advertisers, this is not duplicated reach. These are audiences that cannot be accessed through subscription-based advertising tiers - effectively invisible to campaigns that run exclusively on platforms like Netflix's ad tier or Amazon Prime's ad-supported layer.

Sarah Lewis, Global Vice President CTV at ShowHeroes, framed this plainly: "Our research shows Open CTV, particularly FAST channels, is unlocking incremental reach by attracting viewers who refuse to pay more but still demand premium entertainment. In this environment, advertising is not an interruption, it is part of a transparent exchange."

Marit van Zon, Insights Consultant at Omnicom Media Netherlands, described the broader shift as consumer-driven: "Audiences are making rational decisions about value, and they are responding positively to environments where that value exchange is clear. FAST combines high engagement with high receptivity."

This audience composition also skews demographically valuable. Indexed against the total population, FAST viewers over-index significantly on the 25-34 age group (index 135), households of four (index 143), and middle-to-high income brackets (index 118). These are not fringe audiences; they are sought-after segments for consumer brands.

Ad acceptance and the four-minute rule

The question of whether audiences tolerate advertising on free platforms is often treated as uncertain in media planning circles. The study addresses it directly. Across all six markets, ad acceptance is measurably higher on FAST channels than on SAVOD platforms. When asked whether advertising felt fair given the service they received, UK FAST users answered yes at 69%, compared to 65% for SAVOD. In Germany, the gap is even wider: 65% for FAST versus 39% for SAVOD. The Netherlands shows a similar pattern at 68% versus 42%.

The key variables driving acceptance are consistent. Viewers tolerate advertising when content is free, when ad breaks are concise, when ads are relevant to them or to the content they are watching, and when overall content quality is high. The study identifies approximately four minutes of advertising per hour as the threshold viewers consider acceptable - a number with direct implications for inventory planning and yield management.

The 30-second format continues to deliver the highest recall in CTV environments, consistent with findings from ShowHeroes' own 2024 CTV study that established ad-supported CTV as mainstream, with 77% of viewers reporting they see ads on CTV.

Smart TV penetration as a distribution backbone

The study provides smart TV ownership data that contextualizes why Open CTV - the broader category that encompasses FAST channels and AVOD alongside SAVOD - has distribution reach at scale. Spain leads at 94%, followed by Italy at 93%, the Netherlands at 90%, the UK at 88%, Germany at 86%, and France at 80%. These figures approach saturation in several markets, meaning the home screen of the smart TV is fast becoming the primary content discovery interface for a large majority of households.

The home screen implication is significant. Research documented by PPC Land has previously noted that 40% of CTV viewers rely on the TV home screen for content guidance, making it a critical touchpoint for advertisers seeking to connect with audiences during discovery moments rather than mid-content.

LG Ad Solutions data cited at PPC Land showed that in the US, viewers spend approximately 100 minutes per session using FAST apps on LG TVs - 23% longer than on subscription services. While not directly comparable to the European data in this study, the directional signal is consistent: once audiences engage with FAST, they stay.

Market-specific advertising implications

The Netherlands presents a particular case. The Dutch market is traditionally resistant to advertising, and 44% of Dutch consumers say they would cancel a subscription if ads were added. Yet the study finds that FAST ad acceptance ratings are significantly higher than SAVOD in the market - a contradiction that resolves when content is understood as free. The "fairness" of advertising is perceived very differently depending on whether the viewer is paying for the service.

In Germany, 47% of viewers are unreachable through SAVOD advertising channels entirely. That is not a marginal planning consideration - it is a major audience gap. ShowHeroes' recent acquisition of Munich-based Traffective positions the company to address exactly this kind of publisher-side fragmentation, with the combined entity reaching close to 2,000 publisher partners and generating more than 25 billion ad impressions.

Spain shows particularly strong receptivity to targeted advertising within FAST environments. The study finds 42% of Spanish FAST viewers find personalized ads interesting, and 36% prefer contextually linked ads. That aligns with the broader industry trend toward contextual targeting in CTV, where Viant's integration with Wurl enabled scene-level targeting across FAST inventory in August 2025 - a technical development designed precisely to improve ad relevance at the content level.

The measurement dimension

The study's findings land at a moment when European CTV measurement infrastructure is maturing rapidly. IAB Europe's CTV Working Group published its analysis of attribution challenges in March 2026, noting that cross-device attribution and fragmented identifiers still block CTV's full transition to a performance channel. FAST channels, with their linear-style scheduling and ad pod structures, present measurement challenges that differ from SVOD environments. The absence of login walls - a feature, not a bug, for consumers - also means identity resolution relies on household-level signals rather than deterministic user IDs.

For marketers who have been warned against treating CTV like display campaigns, the FAST environment requires additional care. Open-market buys across FAST channels can expose advertisers to vast supply volumes without adequate contextual control, and the study's finding that relevance drives acceptance puts the onus squarely on targeting precision. Private marketplace deals or programmatic guaranteed arrangements with specific FAST publishers offer a route to the contextual specificity the data suggests audiences want.

Why this matters to advertisers

The research carries several concrete implications for media planners and advertisers operating in European markets. First, reach planning that excludes FAST channels is now effectively excluding significant audience segments - particularly in France and the Netherlands, where the majority of FAST users have no overlap with SAVOD platforms. Second, the ad acceptance data suggests FAST inventory may carry structurally better brand reception than ad-supported subscription tiers, where advertising is perceived as an unwelcome intrusion by paying customers. Third, the audience profile - younger, higher income, larger households - aligns with demographic targets that performance and brand advertisers typically prioritize.

The study also points to a content migration that carries audience implications. Sports and news, both traditionally the domain of linear television, are moving toward ad-supported digital streaming. That migration is already visible in the data - news consumption on FAST channels is rising in Germany and the Netherlands, and the study notes that sports live rights are increasingly going to CTV-native publishers.

Retail media and CTV are already converging per IAB Europe analysis from late 2025, with retail media spend on connected television projected to grow three times faster than retail media search. The FAST environment, with its lean-back audience and high ad acceptance, sits naturally within that convergence as a channel for mid-funnel brand campaigns supported by first-party retail data.

Timeline

- 2016 - ShowHeroes founded in Berlin by Ilhan Zengin, Mario Tiedemann, and Dennis Kirschner

- 2020 - ShowHeroes Group launched, expanding into international markets

- 2024 - ShowHeroes and Omnicom Media Netherlands conduct their first joint CTV consumer study; findings establish 86% CTV viewing rate and 77% ad exposure rate among viewers

- June 2024 - GumGum and ShowHeroes announce global partnership for contextual video advertising

- April 2025 - LG Ad Solutions' Big Shift 2025 report documents 36% of US viewers dropping paid subscriptions, 24% planning to add FAST services

- July 2025 - ODMedia launches FAST channels on Titan OS, expanding Netherlands CTV reach

- August 2025 - FAST channels globally surge 42% as programmers expand beyond nostalgic content, per Gracenote analysis

- November 2025 - Industry expert warns advertisers against treating CTV like display campaigns

- November 2025 - Retail media and CTV convergence analysis published by IAB Europe

- December 2025 - Lionsgate hands FreeWheel exclusive control of its 30 US FAST channels

- March 6, 2026 - ShowHeroes acquires Munich-based Traffective, creating one of Europe's largest independent publisher monetisation platforms

- March 11, 2026 - IAB Europe CTV Working Group publishes analysis of attribution gaps and performance measurement challenges

- March 24, 2026 - ShowHeroes and Omnicom Media Netherlands publish "The Rise of FAST: Consumer Preferences in Connected TV," based on 4,377 respondents across six European markets

Summary

Who - ShowHeroes, a Berlin-based CTV and digital video advertising company founded in 2016, and Omnicom Media Netherlands, part of the international Omnicom Group, jointly conducted and published the study. Key figures include Ilhan Zengin (CEO, ShowHeroes Group), Sarah Lewis (Global VP CTV, ShowHeroes), and Marit van Zon (Insights Consultant, Omnicom Media Netherlands).

What - A pan-European consumer research study, "The Rise of FAST: Consumer Preferences in Connected TV," surveying 4,377 respondents aged 18 to 65 across the UK, Germany, France, Italy, Spain, and the Netherlands on their attitudes toward FAST channels, subscription services, and advertising in streaming environments.

When - Published on March 24, 2026. The underlying survey builds on a prior study from 2024, allowing for year-on-year behavioral comparisons.

Where - Research conducted across six European markets via online questionnaire, adapted to each local language. The findings were announced from London.

Why - The study was commissioned to understand how European consumers are responding to the proliferation of streaming options and rising subscription costs, and to map the structural shift from subscription-led growth to ad-supported free streaming as the primary driver of incremental CTV reach. For the advertising industry, the data provides a basis for evaluating how FAST channels should be weighted within European media plans, given the audience exclusivity, demographic quality, and ad acceptance rates documented in the research.

Share this article

The link has been copied!