France's digital marketing sector generated 14.4 billion euros in direct revenue during 2024 while supporting 310,000 jobs across the economy, according to a comprehensive impact study released by Alliance Digitale and EY on December 4, 2025. The research reveals an industry expanding five times faster than French GDP growth, with value creation concentrated among advertising technology firms and platform operators.

The second edition of the macroeconomic impact assessment demonstrates digital marketing's progression from experimental channel to economic infrastructure. More than 18,000 companies now operate within the sector, representing a 41% expansion since 2022 compared to 16% growth across France's broader economy during the same period.

Subscribe PPC Land newsletter ✉️ for similar stories like this one

Subscribe

Technology platforms and content distribution networks captured 36% of total industry revenue, generating 5.2 billion euros through search engines, social networks, and marketplace advertising placements. Marketing technology providers contributed 5 billion euros representing 35% of sector turnover, while consulting and creative agencies accounted for 4.2 billion euros at 29% of the total.

The concentration of digital advertising spending among major platforms reflects broader European patterns, where France ranks second in the continent with digital advertising expenditure reaching 11.2 billion euros in 2024. Platform dominance continues intensifying as social networks and search engines capture approximately 70% of digital advertising revenues.

Research and development investments distinguish the sector from traditional industries. Companies allocated 1.6 billion euros to innovation activities in 2024, representing 11.5% of revenue compared to 3% among automotive manufacturers. AdTech and MarTech firms demonstrated the highest innovation intensity at 16% of turnover.

"Companies we surveyed continue investing heavily in R&D despite difficult macroeconomic conditions," explained Yannick Cabrol, Director at EY Consulting. The commitment reflects competitive pressure to develop artificial intelligence capabilities and measurement systems as regulatory frameworks restrict traditional targeting methods.

Employment growth outpaces comparable industries

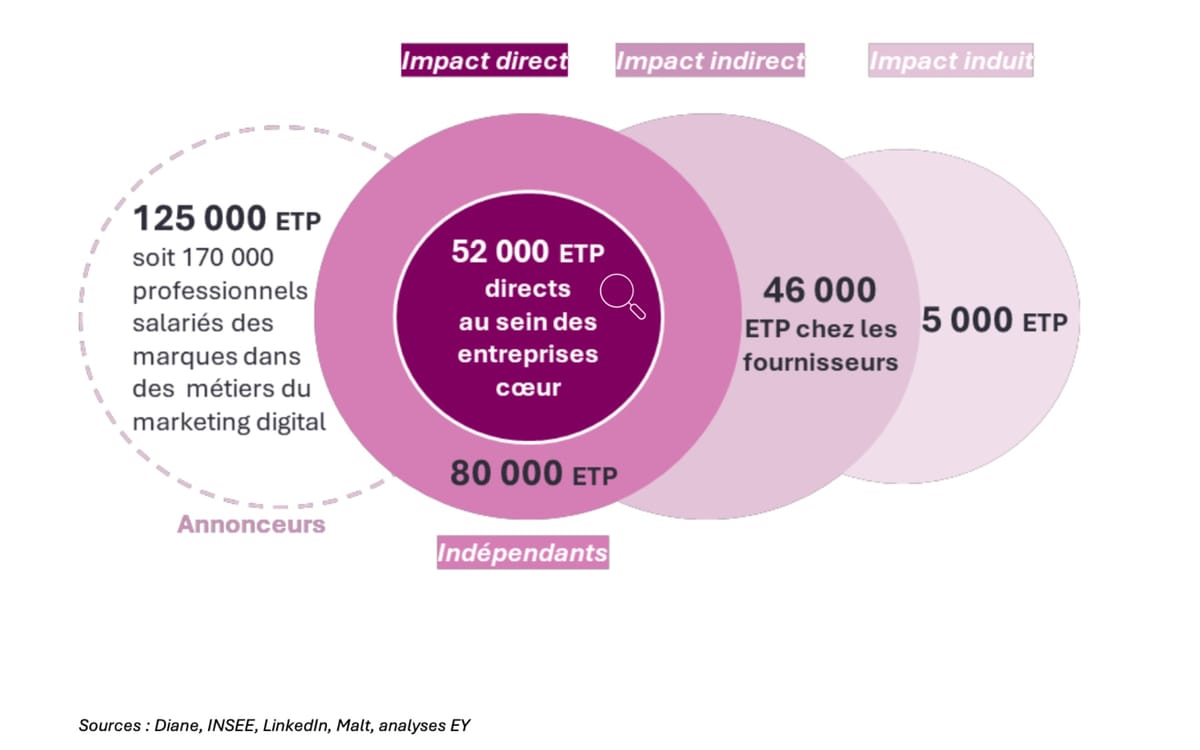

Direct employment reached 51,846 full-time equivalents within core digital marketing companies, with additional indirect positions created among suppliers and independent contractors. The study identified 80,000 freelance professionals operating in marketing disciplines, while 170,000 salaried positions exist within advertiser organizations managing digital campaigns.

Geographic distribution reveals significant development outside Paris, with 49% of positions located beyond Île-de-France region. Lyon, Marseille, Bordeaux, Montpellier, and Nantes emerged as secondary employment centers hosting specialized agencies and technology providers.

Compensation data indicates average monthly salaries reaching 3,522 euros, approximately 29% above private sector averages. Technology platforms and search providers reported highest wage levels at 3,761 euros monthly, reflecting competition for technical expertise in data engineering and algorithm development.

Gender representation remains below economy-wide participation rates, with women occupying 40% of digital marketing positions compared to 44% across all private employment. The disparity appears most pronounced within technology development roles at 35% female participation versus 46% in consulting and creative functions.

Economic multiplier effects extend across sectors

Indirect economic impacts generated 8.9 billion euros in supplier revenue plus 1 billion euros through employee consumption patterns. Total economic output reached 24.3 billion euros when combining direct, indirect, and induced effects across the French economy.

Each euro of direct value creation produced 1.26 euros in additional economic activity, exceeding multiplier effects observed in cinema (0.84 euros) and pharmaceutical manufacturing (0.91 euros). The elevated impact stems from extensive service procurement including legal advisory, technical infrastructure, content production, and analytics platforms.

The expansion of retail media networks created additional demand for marketing services, with e-commerce platforms developing advertising inventory that agencies and technology providers must integrate into campaign planning systems. This infrastructure development sustained employment among third-party service organizations.

Innovation spending concentrates in technology firms

Software publishers and measurement platforms allocated 40% of sector research budgets, totaling approximately 640 million euros for platform development and algorithm refinement. Agencies invested more conservatively at 5% of revenue, focusing resources on client service delivery rather than proprietary technology development.

Innovation priorities centered on artificial intelligence integration across campaign automation, content generation, and performance optimization. Survey responses indicated 82% of executives anticipate generative AI transforming industry operations during coming years, despite the sector's established experience with algorithmic systems.

The technology development cadence reflects competitive positioning requirements. Companies must demonstrate advanced capabilities to compete for advertiser budgets as marketing procurement teams demand measurable return on investment amid economic uncertainty.

Buy ads on PPC Land. PPC Land has standard and native ad formats via major DSPs and ad platforms like Google Ads. Via an auction CPM, you can reach industry professionals.

Learn more

Regulatory complexity emerges as operational constraint

Survey participants identified regulatory compliance as the second-most significant business challenge, with 74% expressing concern about evolving data protection requirements. The General Data Protection Regulation and ePrivacy Directive implementations created operational burdens while reducing targeting precision compared to less-regulated markets.

Nicolas Rieul, President of Alliance Digitale, noted the paradoxical effect: "Regulation destroys value short-term but recreates it medium-term. This explains the strong innovation capacity of French agencies, often more creative than European counterparts due to a more constraining framework."

Compliance costs disproportionately affect smaller organizations lacking dedicated legal resources. However, regulatory constraints have stimulated development of consent management platforms and first-party data infrastructure, creating new technology categories within the marketing ecosystem.

Concentration of advertising inventory among major technology platforms emerged as the primary strategic concern, with 79% of surveyed executives worried about limited diversification opportunities. Major platforms reportedly control approximately 70% of digital advertising distribution, creating dependency relationships that constrain negotiating leverage.

The market structure influences pricing power and service terms, with smaller publishers and agencies accepting unfavorable commercial conditions to maintain platform access. This asymmetry extends to data access, where platform operators retain comprehensive user information while restricting advertiser visibility into underlying audience composition.

Agency executives reported increasing difficulty demonstrating campaign effectiveness as measurement systems evolve. Attribution complexity intensifies as users engage across multiple devices and platforms, while privacy regulations restrict cross-site tracking mechanisms that previously enabled performance assessment.

Budget pressure intensified during 2024, with 68% of survey respondents noting advertiser focus on immediate return metrics rather than brand-building objectives. This shift toward performance-oriented spending advantages direct response channels including search and social platforms over display advertising formats.

The emphasis on measurable outcomes created operational challenges for agencies accustomed to creative development and strategic planning. Many organizations now compete directly with automated bidding systems and self-service platforms that promise superior efficiency through algorithmic optimization.

EssenceMediacom France demonstrated attention-based bidding strategies achieving 7% cost efficiency improvements through Display & Video 360 custom algorithms. Such technical implementations require data science capabilities beyond traditional agency competencies, forcing organizational restructuring and talent acquisition.

International expansion drives growth strategies

Export revenue reached 2.3 billion euros representing 17% of sector turnover, with technology platforms demonstrating highest internationalization at 19% of revenue. Agencies recorded 14% export share, constrained by service delivery requirements and local market knowledge necessary for effective campaign execution.

Geographic expansion targets primarily European markets, with 69% of surveyed companies planning international development initiatives. However, only 20% intend establishing foreign offices, preferring partnership models and remote service delivery to reduce capital requirements.

Technology firms demonstrated greater international ambition, leveraging software distribution economics that enable global reach without proportional cost increases. Platforms and measurement providers serve multiple markets from centralized development operations, achieving scale economies unavailable to service-oriented agencies.

Workforce planning emphasizes commercial talent

Recruitment priorities centered on commercial roles and technical specialists capable of implementing artificial intelligence systems. Half of surveyed companies reported hiring difficulties, citing talent shortages at 47% and competitive pressure at 42%.

Salary inflation reached 8.5% between 2022 and 2023 within the sector, exceeding economy-wide wage growth of 5.6%. This premium reflects competition for specialized skills in programmatic advertising, data engineering, and performance analytics as companies expand automated campaign capabilities.

Offshore outsourcing emerged as cost management strategy, with 41% of organizations utilizing or planning international service delivery for routine functions including reporting, optimization, and administrative tasks. The practice concentrates among agencies facing margin pressure from advertiser procurement demands.

Environmental commitments diverge from market priorities

While 71% of companies reported increased environmental engagement compared to three years prior, executives noted weakening advertiser interest in sustainability initiatives. Economic uncertainty shifted procurement priorities toward immediate performance metrics rather than environmental impact considerations.

Decarbonization strategies reached 73% adoption among surveyed organizations, with 86% of implementing companies reporting progress meeting established targets. Energy consumption reduction emerged as the most common priority at 54%, followed by supply chain decarbonization at 49%.

The digital sector contributes approximately 4% of France's carbon footprint, comparable to heavy freight transport according to ADEME and ARCEP estimates. Generative AI deployment threatens increasing this share as training and inference operations consume substantial computational resources.

Methodology integrates quantitative and qualitative research

EY teams conducted the analysis between July and October 2025, combining statistical modeling with 40 executive surveys and 16 in-depth interviews. Companies surveyed represent more than 50% of sector revenue, providing representative coverage across agency, technology, and platform segments.

The statistical scope differs from the 2023 edition due to Alliance Digitale's merger with DMA France, expanding coverage to include data marketing and customer relationship management specialists. Updated methodology incorporated revised industry classification codes and enhanced company identification through keyword analysis.

Impact calculations employed input-output modeling based on INSEE national accounts data, tracking economic effects through supplier relationships and household consumption patterns. The approach enables comparison with previous editions while accommodating scope adjustments from organizational consolidation.

Subscribe PPC Land newsletter ✉️ for similar stories like this one

Subscribe

Timeline

- December 2022: First Alliance Digitale economic impact study establishes baseline methodology

- May 2025: IAB Europe reports European digital advertising reaching €118.9 billion with France at €11.2 billion

- July-October 2025: EY conducts surveys and interviews with French digital marketing executives

- September 2025: IAB Europe AI study reveals 85% adoption across European advertising

- December 4, 2025: Alliance Digitale and EY release second economic impact assessment at Forum Alliance Digitale

Subscribe PPC Land newsletter ✉️ for similar stories like this one

Subscribe

Summary

Who: Alliance Digitale and EY Consulting examined 18,387 French companies operating in digital marketing, employing 51,846 full-time equivalents plus 80,000 freelance professionals and 170,000 in-house marketing specialists at advertiser organizations.

What: The digital marketing sector generated 14.4 billion euros in direct revenue and 5.6 billion euros in value creation during 2024, investing 1.6 billion euros in research and development while supporting 310,000 jobs across direct, indirect, and induced employment.

When: The study analyzed 2024 economic data with research conducted between July and October 2025, releasing findings on December 4, 2025, at the annual Alliance Digitale forum in Paris.

Where: Operations concentrate in Île-de-France capturing 51% of employment, with significant presence in Lyon, Marseille, Bordeaux, Montpellier, and Nantes, while 17% of revenue originates from international markets across Europe and North America.

Why: The assessment demonstrates digital marketing's economic contribution amid regulatory evolution, platform concentration, and artificial intelligence integration transforming advertising operations while French companies maintain innovation leadership despite competitive pressure from global technology platforms.

Share this article

The link has been copied!