Most Valentine's shoppers keep budgets under $100 despite price pressures

Only 11% plan spending over $100 for Valentine's Day 2026 as thoughtfulness tops price concerns, with 61% undeterred by inflation, InMarket survey finds.

Only 11% plan spending over $100 for Valentine's Day 2026 as thoughtfulness tops price concerns, with 61% undeterred by inflation, InMarket survey finds.

Thoughtfulness emerged as the dominant purchasing criterion for Valentine's Day 2026, outranking price considerations despite persistent inflation pressures affecting consumer spending across retail categories. InMarket's survey of 4,844 U.S. adults conducted in January 2026 revealed that 55% of consumers prioritize recipient interests and needs when making purchase decisions, while only 11% of celebrators plan to spend more than $100 on the holiday.

The spending distribution presents a stark contrast to aggregate industry projections. While Valentine's Day spending reached a record $29.1 billion earlier this year, the majority of individual consumers maintain modest budgets. Thirty percent of respondents indicated planned spending below $25, while 33% allocated $25 to $50 for Valentine's purchases. An additional 26% positioned their budgets between $50 and $100, with only 8% planning expenditures in the $100 to $200 range and 3% budgeting above $200.

The tension between aggregate spending growth and individual budget constraints reflects a bifurcated market where a minority of high spenders drive total expenditure increases while most consumers exercise restraint. The average planned spending of approximately $50 to $75 among the majority cohort stands well below the $199.78 per-person average reported in broader industry surveys, suggesting concentration of spending among affluent demographics.

Price inflation affected Valentine's Day plans for 39% of consumers surveyed, yet this impact manifested primarily as strategic adaptation rather than complete abandonment of celebrations. Among those adjusting their approach, 39% indicated plans to dine at home instead of visiting restaurants - the single largest behavioral shift documented in the research. This dining preference represented a substantial increase from InMarket's 2025 Valentine's Day survey, where 39% of total respondents chose home dining, compared to 56% of all celebrators in 2026.

The home dining trend aligns with broader consumer spending patterns documented in retail research showing 68% of consumers cutting back on fine dining and 65% reducing casual restaurant expenditures amid ongoing economic pressures. Restaurant operators face intensifying competition for the 34% of Valentine's celebrators still planning to dine out, with 53% of that cohort preferring local establishments over chain restaurants.

Nearly three in ten consumers affected by higher prices, specifically 29%, stated they would forgo Valentine's Day purchases entirely this year. An additional 25% planned to actively seek sales, promotions, and coupons, while 21% intended to purchase lower-cost alternatives. Sixteen percent opted to create homemade gifts rather than purchasing commercial products, and 14% reduced their total gift counts compared to previous years. Eleven percent selected less expensive dining venues to maintain the tradition of eating out while controlling costs.

The proportion of consumers unaffected by price increases - 61% - demonstrates remarkable resilience considering broader economic anxieties. This stability suggests Valentine's Day maintains protected status in household budgets despite financial pressures affecting discretionary spending in other categories. The protected status reflects the holiday's emotional significance, where relationship maintenance and social obligations create spending motivation that persists through economic uncertainty.

Overall Valentine's Day participation reached 41% among survey respondents, representing a substantial decline from typical celebration rates. Among participants, 22% planned only experiential celebrations such as cooking special dinners, dining out, or taking trips, without accompanying gift purchases. Nine percent intended to purchase or create gifts while forgoing experiential components, and 10% combined both gift-giving and celebratory experiences.

The majority at 59% indicated no plans to purchase gifts or celebrate Valentine's Day at all. This abstention rate significantly exceeds historical norms and suggests potential long-term shifts in holiday observance patterns, particularly among younger demographics navigating financial constraints and evolving relationship structures.

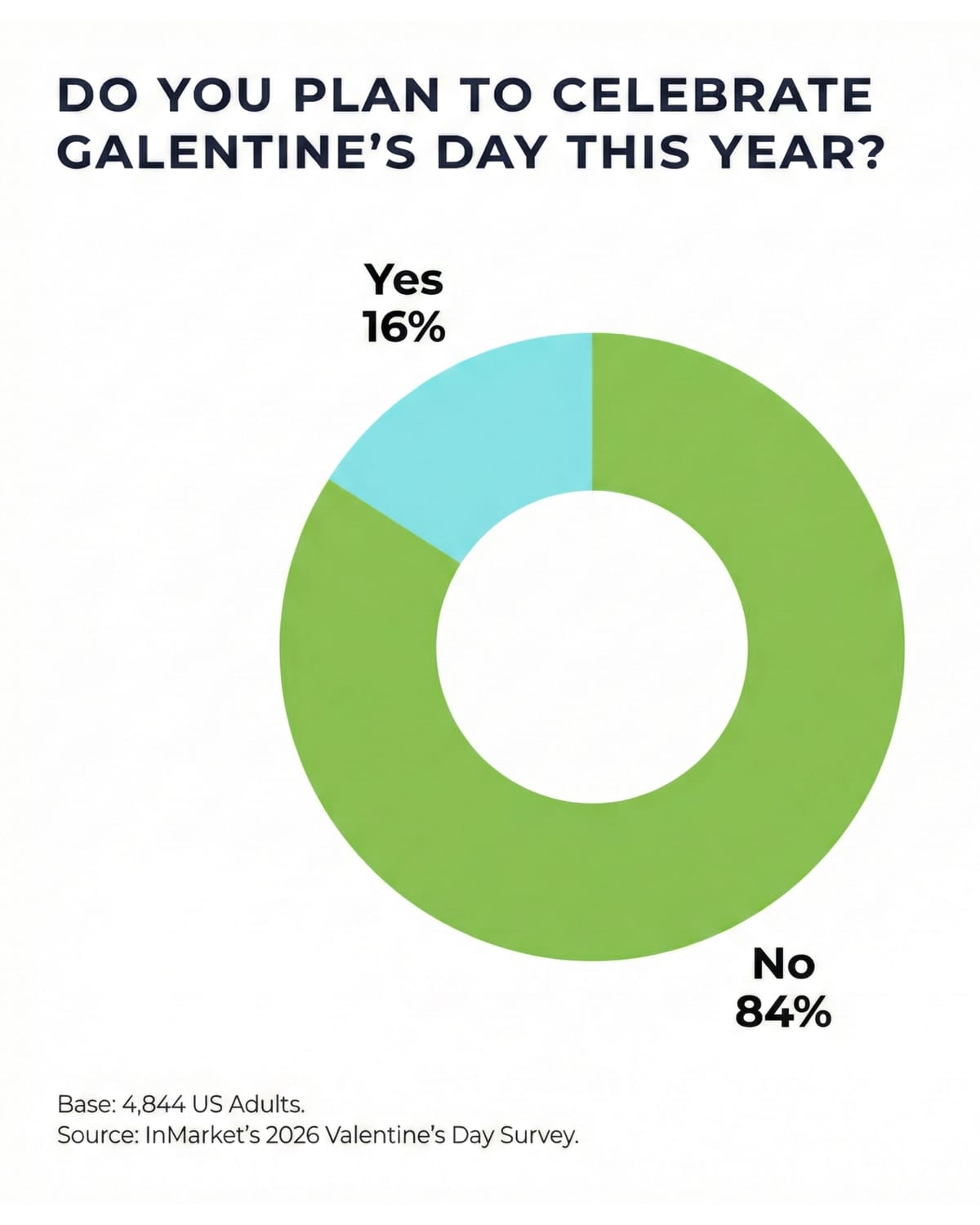

Galentine's Day, the friendship-focused celebration occurring around Valentine's Day, attracted 16% of consumers. The friend-based occasion encourages group spending and shareable experiences, creating opportunities for brands targeting platonic relationship celebrations. Galentine's Day spending skews toward casual dining, coffee shops, and confectionery rather than traditional romantic gifts like jewelry and flowers.

Traditional gift categories maintained their dominance despite budget pressures. Chocolate and candy topped planned purchases at 53%, followed by greeting cards at 45% and flowers at 24%. These accessible categories align with prevailing budget constraints, offering meaningful gestures at price points compatible with the $25 to $100 spending range where most consumers position themselves.

Higher-cost categories demonstrated predictably lower adoption rates. Experiences including concerts, shows, or special events attracted 13% of gift-givers, while jewelry and watches appealed to 7%. Electronics registered just 2% adoption, reflecting both the category's expense and limited romantic relevance.

Gift cards emerged as a meaningful component at 12% of planned purchases, providing flexibility for both givers and recipients while maintaining predetermined spending limits. The gift card adoption rate aligns with patterns documented across holiday shopping periods, where consumers increasingly favor practical giving options that avoid potential preference mismatches.

Among chocolate purchasers, 54% planned to buy boxed Valentine's Day chocolates from brands like Russell Stover and Whitman's Sampler. Twenty-five percent selected bags of assorted candy or chocolate brands, while 22% chose individual chocolate pieces and an equal proportion selected bags of individual chocolate brands. Fifteen percent opted for bags of individual candy brands.

Dove Chocolate led brand preferences at 34%, followed by Ghirardelli at 29%, Reese's Peanut Butter Cups at 27%, and Hershey's at 22%. Russell Stover and Ferrero Rocher each captured 20% of planned purchases, while M&M's attracted 18%. The brand preferences reflect established market positions and seasonal product availability, with most leading manufacturers offering Valentine's-specific packaging and assortments.

InMarket's 2025 commerce data revealed chocolate spending increased 39% in early February compared to late January, with Godiva demonstrating 83% growth, Ferrero expanding 33%, and Ghirardelli rising 24%. These growth rates significantly exceeded overall Valentine's spending increases, indicating chocolate's disproportionate importance during the holiday period.

Sour Patch Kids and Skittles tied at 14% for candy preferences, followed by Nerds at 13%. Twizzlers and SweeTarts each captured 8%, while Starburst attracted 7%. The candy preferences skew toward fruit-flavored and sour varieties, contrasting with chocolate's dominance of traditional romantic gifting.

Forty-two percent of Valentine's shoppers planned to visit big-box stores for their purchases, reflecting these retailers' broad product selection and competitive pricing. Grocery stores attracted 32%, while online-only retailers captured 29% and warehouse clubs drew 13%. Dollar and discount stores appealed to 19% of shoppers seeking value options.

For chocolate and candy specifically, 54% of purchasers planned to shop at big-box stores, with 35% selecting grocery stores and 22% choosing specialty chocolate and candy retailers. The specialty store proportion declined notably from approximately one-third in InMarket's 2025 survey, suggesting price sensitivity drove consumers toward mass-market channels offering promotional pricing and bulk options.

Shopping channel preferences demonstrated strong omnichannel behavior. Fifty percent of respondents planned to shop both in-store and online, while 36% focused primarily on in-store purchasing. Just 14% intended to shop exclusively online, indicating Valentine's Day shopping maintains substantial physical retail components despite digital commerce growth across other categories.

The high in-store shopping rate at 86% (combining pure in-store and omnichannel shoppers) aligns with holiday shopping research showing 80% of consumers preferring physical retail for tactile product evaluation and immediate availability. Valentine's gift categories - particularly flowers, chocolates, and greeting cards - benefit from sensory assessment capabilities unavailable through digital channels.

Florist visits increased 300% in the two weeks preceding Valentine's Day 2025 compared to late January, while jewelry store traffic rose 65% during the same period. These dramatic traffic spikes demonstrate how certain specialized categories remain anchored to physical retail despite broader e-commerce expansion.

The finding that 55% of consumers prioritize thoughtfulness over other factors represents the most significant attitudinal shift documented in the research. Price ranked second at 43%, followed by value and quality at 38% each. Sales and special offers influenced 24% of shoppers, while health and wellness considerations affected 16%.

Convenience mattered to 14% of respondents, while family and friend requests drove 6% of purchase decisions. Brand name influenced 3% of shoppers, as did inspiration from social media and viral moments. Loyalty programs motivated 2% of consumers.

The thoughtfulness premium suggests consumers willing to celebrate Valentine's Day despite economic pressures seek meaningful expressions rather than expensive gestures. This creates opportunities for brands emphasizing personalization, customization, and recipient-specific attributes rather than premium pricing or luxury positioning.

The value consciousness - where 38% explicitly cited value alongside 43% prioritizing price - indicates consumers actively evaluate cost-to-benefit ratios rather than simply seeking lowest prices. Products and experiences delivering meaningful impact at accessible price points align with this dual consideration of thoughtfulness and value.

The 61% of celebrators unaffected by higher prices demonstrates Valentine's Day's protected budget status. This resilience occurred despite broader consumer anxiety, where InMarket's separate 2026 Inflation Outlook survey found 81% of consumers cutting discretionary purchases.

The protected status reflects Valentine's Day's role in relationship maintenance and social signaling, where celebration absence carries potential relationship costs exceeding the monetary expense of participation. This emotional valuation creates price inelasticity within certain spending ranges, particularly for established relationship milestones.

However, the shift toward home dining and away from expensive gifts indicates boundaries to this resilience. Consumers protect the celebration itself while adjusting components to align with budget constraints. The 56% planning home dining versus 34% choosing restaurants marks a significant reversal from traditional patterns emphasizing restaurant celebrations.

Restaurant operators face challenges from this dining migration, though opportunities exist in takeout and delivery options combining home celebration with professional meal preparation. Value-oriented promotions and prix fixe menus targeting budget-conscious celebrators may capture spending from consumers otherwise choosing fully home-prepared meals.

The research findings present several implications for Valentine's Day marketing strategies. The thoughtfulness emphasis suggests messaging should highlight personalization, recipient consideration, and meaningful gestures rather than product expense or luxury positioning. Brands can differentiate through customization options, personal touches, and demonstration of care in product selection.

The $25 to $100 sweet spot where 59% of celebrators position their spending indicates product and promotion strategies should emphasize value within this range. Bundle offerings, gift sets, and promotional pricing creating perceived value at accessible price points align with prevailing budget constraints.

The home dining trend creates opportunities for grocery retailers and food brands to promote Valentine's meal components, recipe suggestions, and cooking instructions enabling impressive home preparations. Ready-to-cook meal kits, premium ingredients, and dessert components position between full restaurant expense and basic home cooking.

Physical retail's continued importance - with 86% shopping at least partially in-store - justifies continued investment in in-store promotions, displays, and experiential elements. The two-week period preceding Valentine's Day represents peak shopping activity, requiring concentrated promotional focus during early February.

The chocolate category's 39% spending increase in early February versus late January demonstrates clear seasonal sales spikes, indicating the importance of promotional timing and inventory positioning. Early promotional launches risk diluting urgency, while late activations miss early purchasers planning ahead.

The Galentine's Day opportunity at 16% participation enables brands to extend Valentine's season beyond romantic partnerships to friendship celebrations. Group-oriented products, shareable items, and platonic gift options expand addressable markets beyond traditional couple-focused positioning.

Who: InMarket surveyed 4,844 U.S. adults aged 18 and older in January 2026, with results weighted to U.S. Census Bureau age and gender data. The research also analyzed third-party commerce data from January 18 - February 14, 2025.

What: The research found only 11% of Valentine's Day celebrators plan to spend over $100, with 59% budgeting between $25 and $100. Thoughtfulness ranked as the top purchase factor at 55%, exceeding price considerations at 43%. While 61% said higher prices haven't changed celebration plans, 39% of those affected plan to dine at home instead of restaurants. Chocolate dominates gift preferences at 53%, followed by cards at 45% and flowers at 24%.

When: The survey was fielded in January 2026 ahead of Valentine's Day 2026 on February 14. Historical commerce data analysis covered the 2025 Valentine's season from late January through mid-February.

Where: The survey covered U.S. consumers nationwide, with shopping behavior analysis focusing on major retail channels including big-box stores (42% of shoppers), grocery stores (32%), online retailers (29%), and warehouse clubs (13%). Eighty-six percent plan to shop at least partially in physical stores.

Why: The findings matter for marketers because they reveal a bifurcated market where most consumers maintain modest budgets despite aggregate spending records, requiring value-focused messaging emphasizing thoughtfulness over expense. The shift toward home dining from restaurants, with 56% of celebrators choosing to dine at home, indicates significant behavioral adaptation to economic pressures that creates opportunities for grocery retailers and food brands while challenging restaurant operators.