VIOOH released its 2026 State of the Nation report on programmatic digital out-of-home advertising, revealing that the channel is forecast to appear in nearly half of all campaigns globally within 18 months - a notable step up from the 34% share recorded over the preceding 18 months. The supply-side platform, headquartered in London, published the findings this month, drawing on a survey of 1,050 advertisers and agencies conducted in partnership with research consultancy MTM.

The numbers are considerable. Among recent buyers of programmatic DOOH (pDOOH), 99% expect to increase or maintain investment, and the average anticipated uplift stands at 44% over the next 18 months. That figure rises to 49% among US respondents, the highest forecast of any market surveyed. For context, the equivalent increase projected in 2024 across core markets was 30%, meaning the expected growth rate has accelerated materially in two years.

"The 2026 State of the Nation report paints a picture of a channel that has crossed a critical threshold," said Jean-Christophe Conti, Chief Executive Officer at VIOOH. "Programmatic DOOH is no longer a nascent or specialist channel, it is a core part of how marketers plan and buy programmatic media."

How the survey was constructed

VIOOH partnered with MTM to survey 1,050 advertisers and agencies across four markets: the US, UK, France, and - for the first time in the annual series - the Middle East, represented by Qatar, Saudi Arabia, and the UAE. Participants had either purchased pDOOH in the past 12 months or were digital buyers open to purchasing it. Unless stated otherwise, year-over-year comparisons in the global report use the three core markets of the US, UK, and France as the baseline, consistent with prior editions.

The previous global State of the Nation was published in September 2024. In 2025, VIOOH issued special editions for guest markets including the Nordics and China. The China report, released on August 4, 2025, showed programmatic DOOH adoption at 30% in mainland China - a 6-percentage-point gain from 24% in 2023. The 2026 global edition now adds the Middle East as a fourth core market, signalling VIOOH's intent to broaden the geographic scope of its annual benchmarking work.

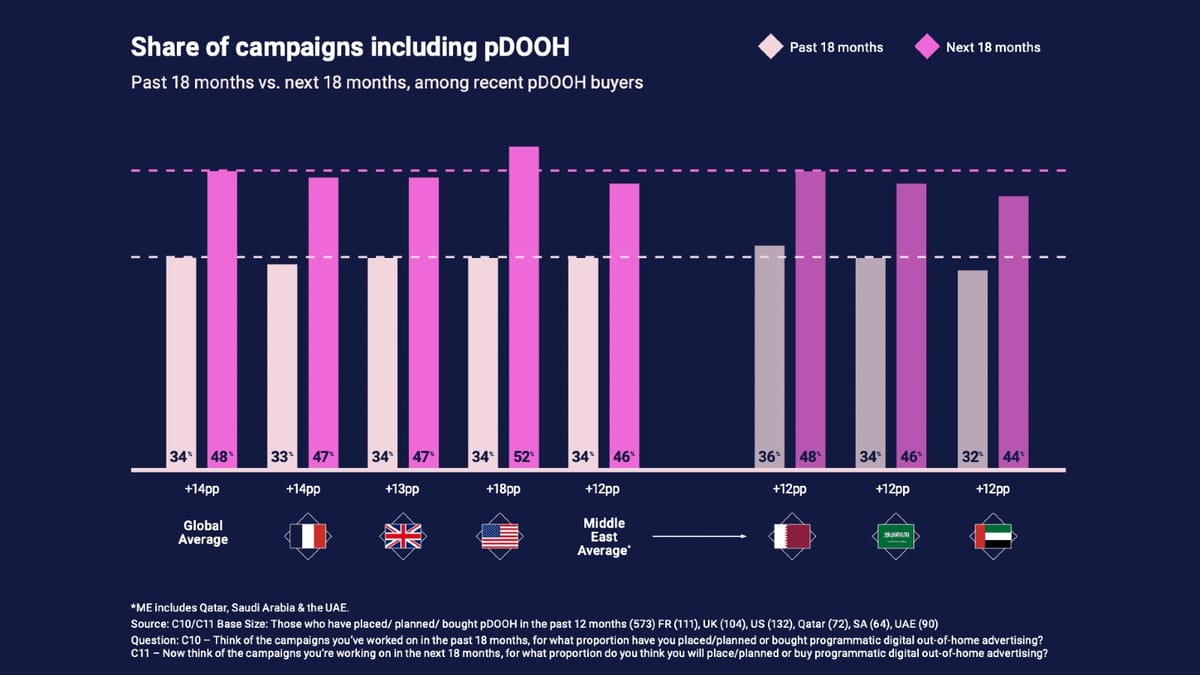

Market-by-market share of campaigns

Across all six markets surveyed, pDOOH featured in 34% of campaigns during the past 18 months - up from 28% recorded in 2024 across France, the UK, and the US. The projected forward share across the global sample is 48%. But the market-level variation is what gives the data its texture.

The US sits at 34% for the past period and is expected to reach 52% - the highest of any market in the survey and a projected increase of 18 percentage points. That growth rate is also the steepest, reflecting what the report describes as an advanced adoption base continuing to scale rapidly. US marketers forecast a 49% average increase in pDOOH spend, well above the 30% increase they forecast in 2024. According to the US market highlights, 68% of American respondents now prioritize programmatic buying and optimization capabilities in their decision-making.

The UK recorded 34% for the past 18 months, up from 31% in 2024, with an expected forward share of 47%. Notably, 92% of UK marketers say pDOOH has been planned as part of broader digital or programmatic activity in the last 12 months - a figure that underscores its integration into omnichannel workflows. The UK report also identifies efficiency as a central investment driver: 70% of UK marketers prioritize value and cost-effectiveness, and 64% place a premium on optimized supply paths and supply chain transparency.

France shows 33% for the past period, rising to 47% projected - consistent with its trajectory but slightly behind the UK and US in absolute terms. French marketers who have bought pDOOH expect spend to increase by an average of 45% over the next 18 months, well above the 28% growth they forecast in 2024. According to the France market highlights, 68% of French respondents now rate trigger-based buying as very or quite important, while 64% value the ability to use first- or third-party data across multiple digital channels.

The Middle East - comprising Qatar, Saudi Arabia, and the UAE - represents the newest addition to the survey. Among recent pDOOH buyers in the region, the channel featured in 34% of campaigns over the past 18 months, with a forward projection of 46%. The regional average for expected investment increase stands at 42%. According to the Middle East highlights, pDOOH is already most often planned as part of wider digital or programmatic activity by 88% of respondents, and campaigns are primarily run at national scale (51%), with execution largely agency-led. General media agencies and OOH specialist agencies were equally identified as responsible for planning and buying - a pattern that suggests buying structures in the region remain more agency-concentrated than in some Western markets.

Budget flows: where the money comes from

One of the report's more telling findings concerns where increased pDOOH budgets originate. On a global level, 95% of those planning to increase pDOOH spend expect to reallocate budget from other digital channels - including DOOH itself. Only 25% globally report that entirely new budget is being added.

Who controls the buy influences where the money comes from. When out-of-home teams lead pDOOH purchasing, increased investment is more often funded from traditional OOH, with 62% citing this route compared to the 49% global average. When digital or programmatic teams lead the buy, budgets are more likely to come from other digital channels - 63% versus the 61% global average. The distinction has structural implications: different internal teams draw from different budget pools, and the team in control of pDOOH buying shapes the competitive dynamics within the broader media mix.

Where a dedicated pDOOH team is in place, 36% of marketers report that entirely new budget is being added, versus 25% globally. The report interprets this as evidence that deeper channel expertise functions as an enabler of incremental spend - a pattern that will likely encourage media owners and agencies to invest in specialist pDOOH capabilities.

Workflow integration deepens significantly

Perhaps the most striking trend in the 2026 data is the degree to which pDOOH has embedded itself in programmatic workflows. According to the global report, 89% of respondents globally planned pDOOH as part of wider digital programmatic activity in the last 12 months. That compares to just 37% in 2023 across core markets. The scale of that shift - from well under half to almost nine in ten - suggests the channel has moved from specialist consideration to standard practice.

Digital and programmatic teams are now the most prevalent route to market for pDOOH, cited by 88% of respondents globally, up from 75% in core markets in 2024. The use of dedicated programmatic DOOH teams has also increased significantly, rising from 32% in 2024 to 53% in 2026 across core markets. That latter figure points to a growing layer of specialist expertise sitting within agencies and advertisers, separate from the general digital or OOH buying function.

The IAB Australia programmatic DOOH buyers guide, published in August 2025, described the practical mechanics of how pDOOH slots into programmatic infrastructure: demand-side platforms bid against supply-side platform inventory in real-time, with campaign delivery optimized against audience and performance signals. The VIOOH 2026 data suggests that workflow has now become routine for most practitioners across core markets.

Curated marketplaces: the emerging structural layer

The 2026 report gives significant attention to curated marketplaces as a mechanism for scaling pDOOH adoption. Globally, 58% of marketers say they are likely to consider curated environments in the near future. The figure is consistent across markets: 57% in France, 59% in the UK, 59% in the US, and 58% across the Middle East.

The structural rationale is fragmentation. DOOH inventory is spread across numerous media owners, each operating with varying platforms. A buyer seeking national reach must traditionally negotiate multiple deals, manage multiple deal IDs, and reconcile reporting from multiple sources. Curated marketplaces address this by bundling inventory under a single deal ID, allowing buyers to achieve national or multi-market reach while maintaining targeting precision and brand safety.

According to the global report, preference for private marketplace (PMP) deals is projected to climb from 30% in 2024 to 50% by 2026 across the FR/UK/US markets. The curated model essentially fuses the advantages of a PMP - price certainty, inventory quality, brand safety - with the operational simplicity of a single trading relationship. From a supply-side platform's perspective, it also strengthens the SSP's role in the transaction chain by placing curation logic at the platform level rather than at the individual media owner.

VIOOH's own supply expansion has moved in parallel. The VIOOH and OUTFRONT partnership announced on March 9, 2026 connected more than 7,600 digital screens and 18 billion monthly impressions to VIOOH's platform, covering approximately 25% of the US DOOH market. Combined with the Vengo partnership from August 2025 - 65,000 screens and 13 billion monthly impressions - VIOOH has rapidly assembled a substantial share of US pDOOH supply. More recently, the partnership with Dolphin OOH in January 2026 added over 5,000 screens across grocery stores and transit hubs. And in Europe, the JCDecaux Ireland partnership in February 2026 opened 32% of the Irish digital OOH market through 288 screens and 311 million monthly impressions. The supply accumulation strategy directly supports the curated marketplace model by giving buyers more inventory to pool under single deal structures.

ROI confidence rises; pDOOH overtakes DOOH for the first time

Confidence in pDOOH's return on investment has increased, and for the first time it now exceeds standard DOOH on this measure. In 2026, 60% of global respondents say pDOOH is likely to deliver ROI, compared to 56% for DOOH and 52% for traditional OOH. That reversal is notable: in 2024, pDOOH trailed DOOH on this measure, at 56% versus 57%.

The contextual attributes of pDOOH are also perceived to be strengthening. Globally, 59% of marketers associate pDOOH with reaching the right people at the right time, rising to 60% across core markets - up from 56% in 2024, and ahead of DOOH at 57%. Flexibility remains a differentiator, with 64% of respondents linking it to pDOOH versus 60% for DOOH and 50% for traditional OOH. And 84% agree that pDOOH is creating innovative opportunities for advertisers, placing it ahead of channels such as display and search on this dimension.

Dynamic creative optimisation (DCO) - the capability that allows creative to adapt in real time to weather, time of day, audience data, or other triggers - is closely associated with pDOOH. According to the global report, 65% of respondents associate pDOOH with DCO, compared to 58% for standard DOOH. That 7-percentage-point differential reflects pDOOH's advantage in enabling data-triggered creative execution at scale.

AI integration: 90% already using it somewhere in the workflow

AI is now part of pDOOH execution for nearly all practitioners surveyed. According to the global report, 90% of respondents are currently using AI at some point during the campaign process. Creative generation leads the specific applications, cited by 40%, followed by predictive forecasting at 38% and intelligent inventory selection at 37%.

Those percentages vary by market. The US leads on AI adoption intensity: only 4% of US respondents report using none of the listed AI applications, compared to a higher proportion globally. The US also leads on DCO execution, with 11% of US respondents actively integrating DCO, versus 7% globally. According to the US market highlights, AI is "already embedded across pDOOH workflows" and the US "leads globally on DCO execution."

The broader pDOOH-AI relationship has been evolving. The analysis published on PPC Land in December 2025 noted that AI is expected to optimize the manual and repetitive aspects of OOH campaign planning rather than displace creative judgment - a framing consistent with the 2026 State of the Nation's depiction of AI as a workflow tool rather than a replacement for human strategy. The 40% of respondents using AI for creative generation represents a meaningful adoption level, but 60% are not yet doing so, indicating runway for further uptake as tools mature and barriers to use fall.

DCO: intent outpaces execution

DCO adoption tells a more complex story. Active DCO implementation has eased to 8% in core markets, down from 13% in 2024. The barriers are well documented: training gaps are cited by 49% of respondents, budget constraints by 47%, and limited creative resource by 46%. Despite these constraints, 66% of global respondents say they will make greater use of DCO in the next 18 months.

That gap between stated intent and current execution is one the industry has been aware of for several years. The 2026 data suggests it has not yet closed, and may have widened slightly on the active implementation metric. For media owners and technology platforms, the persistence of this gap points to a product and education challenge rather than a demand problem: marketers want DCO but face practical barriers to using it at scale.

France illustrates the shift in where barriers sit. According to the France market highlights, lack of awareness has fallen as a barrier from 54% to 25% - suggesting that the industry education efforts of the past two years have been effective. However, training needs have risen from 46% to 52%, and budget constraints from 33% to 48%. The barrier profile has shifted from ignorance to capability and resource - a different problem requiring a different response from the industry.

First-party data: the key unlock for larger advertisers

First-party data integration is identified as one of the leading improvements that would drive greater pDOOH investment, cited by 34% of respondents globally. Among those managing ad spend above £/€/$150 million, that figure rises to 41% - a meaningful gap suggesting that larger, more data-sophisticated advertisers have a sharper appetite for data-led pDOOH strategies than the general sample.

According to the global report, 68% of respondents plan to make greater use of data to plan pDOOH campaigns in the next 18 months. The UK market highlights note that 63% of UK marketers expect to integrate pDOOH more closely into multi-channel campaigns over the next year, a figure likely connected to the drive toward more data-integrated planning workflows.

The cross-channel data question sits within a broader industry conversation about audience measurement and identity in out-of-home. VIOOH's own positioning as a platform has incorporated data partnerships to extend targeting precision beyond geographic and time-of-day parameters. The January 2025 ECN and VIOOH partnership explored how office environments could serve as a targeting context for reaching business decision-makers - an example of the kind of audience-led pDOOH activation that first-party data integration could enable at scale.

Sustainability: still valued, less decisive than in 2024

Sustainability continues to be associated with pDOOH. In 2026, 62% of marketers associate the channel with sustainable or eco-efficient reach. That figure reinforces the credential, particularly given VIOOH's own emissions data: the platform reported in November 2025 an emissions intensity of 0.041g CO2e per ad impression for 2024, more than 20 times more carbon-efficient than programmatic display at 0.84g CO2e per impression.

However, sustainability has become a less prominent decision-making factor than it was in 2024. In the UK, France, and the US, the share ranking sustainability in their top three investment considerations has fallen from 32% in 2024 to 15% in 2026. The credential remains intact, but it has receded as a primary commercial driver. Whether this reflects satisfaction that the sustainability case has been made and is now assumed, or a shift in advertiser priorities toward efficiency and ROI, the data does not resolve. What it does suggest is that sustainability arguments, on their own, carry less weight in budget conversations than they did two years ago.

The Middle East: a market establishing its pDOOH infrastructure

The addition of the Middle East to the 2026 survey provides a baseline from which to track development in a region that has been expanding its digital OOH footprint. Among Middle East pDOOH buyers, the channel featured in 34% of campaigns over the past 18 months, projected to rise to 46% - a 12-percentage-point increase, broadly in line with the global average.

The average expected investment increase for the Middle East is 42%. Execution is currently national in scale for 51% of campaigns, and predominantly agency-led. According to the Middle East market highlights, 88% of respondents plan pDOOH as part of wider digital or programmatic activity - a high integration figure for a market entering the benchmark series for the first time.

Curated marketplaces are seen as an important next step, with 58% of Middle East marketers likely to use such solutions in the future. The focus on reaching the right audience in relevant environments, cited in the regional highlights, aligns with the broader global theme around contextual precision and programmatic workflow integration.

Mazen Mroueh, Head of Performance Product and Operations at Publicis, MENA, was quoted in the global report: "pDOOH is still growing massively, we are seeing double-digit growth every year."

The report in context for marketing professionals

The 2026 State of the Nation data arrives at a moment when programmatic advertising investment is expanding across channels. Broader market data cited in PPC Land's coverage has noted that 72% of marketers planned to increase programmatic spending in 2025, up from 62% in 2024. Within that trajectory, pDOOH's projected 44% investment increase would make it one of the faster-growing segments of programmatic spend.

For media planners, the workflow integration figures carry particular significance. The jump from 37% planning pDOOH as part of digital programmatic activity in 2023 to 89% in 2026 means that, within three years, the channel has shifted from a minority consideration to a near-standard element of omnichannel planning. That shift makes pDOOH literacy increasingly relevant for buyers who primarily operate in digital channels, not just for OOH specialists.

The growth of curated marketplace adoption - expected to hit 58% intent globally within 18 months - will likely reshape how inventory is packaged and sold. By consolidating fragmented supply under single deal structures, curation changes the competitive dynamics between media owners, SSPs, and buyers. Platforms that can offer quality curated environments at scale will hold structural advantages over those relying purely on open auction inventory.

Timeline

- 2018: VIOOH launches in London as a premium global digital out-of-home supply-side platform, initially trading in the UK and US. JCDecaux holds a 93.5% ownership stake.

- September 2024: VIOOH releases its previous global State of the Nation report, with market-specific editions for the US, UK, Australia, Germany, France, and Brazil.

- November 6, 2024: VIOOH reports carbon emissions of less than 0.35g CO2e per ad impression for 2023. Coverage on PPC Land

- December 17, 2024: VIOOH and FRAMEN announce partnership for programmatic advertising in Australian coworking spaces. Coverage on PPC Land

- January 8, 2025: ECN and VIOOH announce a partnership bringing programmatic DOOH to European offices across 870 screens in the UK, France, and Germany.

- August 4, 2025: VIOOH releases its State of the Nation 2025 Mainland China report, showing pDOOH adoption at 30%. Coverage on PPC Land

- August 21, 2025: IAB Australia publishes a comprehensive programmatic DOOH buyers guide. Coverage on PPC Land

- August 26, 2025: VIOOH announces a partnership with Vengo covering 65,000 US screens and 13 billion monthly impressions, representing 9% of the US digital OOH market. Coverage on PPC Land

- October 23, 2025: VIOOH announces a partnership with London Lites covering 49 screens and 74.5 million monthly impressions, representing 23% of the London roadside digital OOH market. Coverage on PPC Land

- November 5, 2025: BIG OUTDOOR integrates inventory into VIOOH's platform across seven US markets. Coverage on PPC Land

- November 6, 2025: VIOOH announces a partnership with RZK Digital covering 800 screens in 43 Brazilian bus terminals with 75 million monthly visitors. Coverage on PPC Land

- November 20, 2025: VIOOH reports 0.041g CO2e per impression for 2024, more than 20 times more carbon-efficient than programmatic display. Coverage on PPC Land

- January 8, 2026: VIOOH announces a partnership with Dolphin OOH covering 5,000 US screens across grocery stores and transit environments. Coverage on PPC Land

- January 25, 2026: Polish DOOH network Jet Line integrates its MORE network with VIOOH, adding over 600 screens across Poland's eight largest cities. Coverage on PPC Land

- February 24, 2026: VIOOH and JCDecaux Ireland announce a partnership covering 288 screens and 311 million monthly impressions, representing 32% of the Irish digital OOH market. Coverage on PPC Land

- March 9, 2026: VIOOH announces a partnership with OUTFRONT covering 7,600 US screens and 18 billion monthly impressions, representing 25% of the US DOOH market. Coverage on PPC Land

- March 19, 2026: VIOOH releases the 2026 State of the Nation global and market reports, surveying 1,050 advertisers and agencies across the US, UK, France, and the Middle East. Published on PPC Land today.

Summary

Who: VIOOH, the London-based premium global digital out-of-home supply-side platform, in partnership with international research and strategy consultancy MTM. The research covered 1,050 advertisers and agencies across the US, UK, France, and the Middle East (Qatar, Saudi Arabia, and UAE).

What: The 2026 State of the Nation report on the programmatic DOOH market, showing the channel featured in 34% of campaigns over the past 18 months, expected to rise to 48% over the next 18 months. Average anticipated investment uplift stands at 44% globally, rising to 49% for the US. The report also covers curated marketplaces, AI integration, DCO adoption, first-party data, and sustainability.

When: The report was released today, March 21, 2026. The survey was conducted across markets in 2026, with year-over-year comparisons using the US, UK, and France as core market baselines. The previous global edition was published in September 2024.

Where: The research covers four markets - the US, UK, France, and the Middle East (Qatar, Saudi Arabia, UAE). The Middle East is included in the global series for the first time. VIOOH currently trades programmatically in 36 markets and connects to more than 50 DSPs globally.

Why: The report matters because it documents a structural shift in how programmatic media is planned and bought. With 89% of practitioners now planning pDOOH as part of broader digital programmatic activity - up from 37% in 2023 - the channel has moved from specialist consideration to standard practice in omnichannel campaigns. The 44% projected investment increase, the emergence of curated marketplaces as a fragmentation solution, and the near-universal adoption of AI in pDOOH workflows all indicate that the channel's role in programmatic budgets is set to grow substantially over the near term.

Share this article

The link has been copied!