Retail media accounting rules create hidden revenue gaps for CMNs

IAB Europe and Mediasense explain how IFRS accounting rules shape retail media revenue reporting, creating gaps between public figures and actual CMN performance data.

IAB Europe and Mediasense explain how IFRS accounting rules shape retail media revenue reporting, creating gaps between public figures and actual CMN performance data.

The numbers rarely add up. That is the problem IAB Europe set out to address on March 12, 2026, when it published the third paper in its five-part series on the convergence of trade and media in retail media - this time with a subject that most industry conversations quietly sidestep: accounting.

Produced in collaboration with Mediasense and authored by Lauren Wakefield, the paper is titled "The Convergence and Coexistence of Trade and Media in Retail Media Series - Part 3: Retailer Accounting for Retail Media Sales." It targets a fundamental structural problem. According to the document, even among publicly listed companies, "commerce media" rarely appears as a clean, standalone line item in financial reporting, and when it does, the numbers may not align with the figures communicated by Commerce Media Network (CMN) leadership.

That disconnect is not accidental. It is, according to IAB Europe and Mediasense, largely a product of how accounting standards treat retail media sales in the first place.

At the heart of the issue is a classification question. According to the paper, sales of digital retail media by retailers are classified in accounting terms as supplier receipts. The logic follows directly from the commercial relationship: the advertiser that ordinarily supplies goods to the retailer is now also making payments to buy media from that same retailer. In accounting terms, the two activities are intertwined.

Under International Financial Reporting Standards (IFRS), which govern reporting for the majority of publicly listed European companies, supplier receipts are presumed to be a reduction in the purchase price of goods acquired from the advertiser. They are netted against the cost of goods sold (COGS) line item, not recorded as incremental revenue. Similar rules apply under US GAAP, with the relevant equivalents being ASC 606, ASC 280, and ASC 205-20.

The practical consequence is significant. As retail media grows, a retailer operating under the default IFRS treatment would record decreasing costs of goods sold rather than increasing revenues. The top line stays flat, or grows only from product sales, while the benefit of retail media quietly offsets procurement costs beneath the gross profit line.

This is why sizing the retail media market remains so difficult. Analysts tracking publicly reported revenue figures may be looking at numbers that exclude a substantial and growing portion of what CMN leadership considers media income.

The paper identifies three incentives driving retailers to pursue an alternative accounting treatment - one that records retail media sales as revenues rather than cost offsets.

First, revenue is a key financial metric. Growing it draws positive attention internally from senior management and externally from investors and analysts. Second, retailers increasingly view themselves as builders of media businesses, not simply as companies reducing the purchase price of goods. Recording retail media as revenue, according to the document, more accurately reflects the underlying economics from their perspective. Third, there is a budget access dimension: if retail media spend is treated as marketing operating expense on the advertiser side (rather than an offset against the advertiser's own revenues), it becomes easier for digital retail media to draw from advertiser brand marketing budgets - a larger and typically more flexible pool of funds than trade budgets.

These pressures are not trivial. European retail media advertising reached €13.7 billion in 2024, a 21.1% increase year-over-year according to IAB Europe data from October 2025. At that scale, whether revenue is classified above or below the gross profit line has material implications for how investors read balance sheets.

For retailers to shift to revenue recognition rather than COGS offset, the paper sets out a rigorous standard. The retailer must demonstrate genuine independence - that the advertiser buying retail media was doing so separately from its status as the retailer's supplier. According to the document, three conditions govern when retail media can be counted as revenue.

The first condition concerns the contract structure. If sales of retail media are covered in the main commercial supplier agreement, the media will be deemed linked and offset against the price of goods purchased from that advertiser. Keeping retail media in a separate contract is a necessary but not sufficient condition for revenue treatment.

The second condition is more demanding. Even in a separate contract, the advertising must be generic - brand-building or universal price promotions - rather than specific to the retailer. The paper provides a sharp illustrative example: if a retailer offered top-pick banner placements or exclusive pricing, the benefit is not considered distinct because it functions as an incentive within the existing commercial relationship. The ad sales would, in that case, remain as a cost deduction to COGS regardless of how the contract is structured.

The third condition requires the retailer to demonstrate that the retail media was sold at fair value. This is an objective pricing test, and its implications stretch into how retailers set rate cards and negotiate placements with supplier-advertisers.

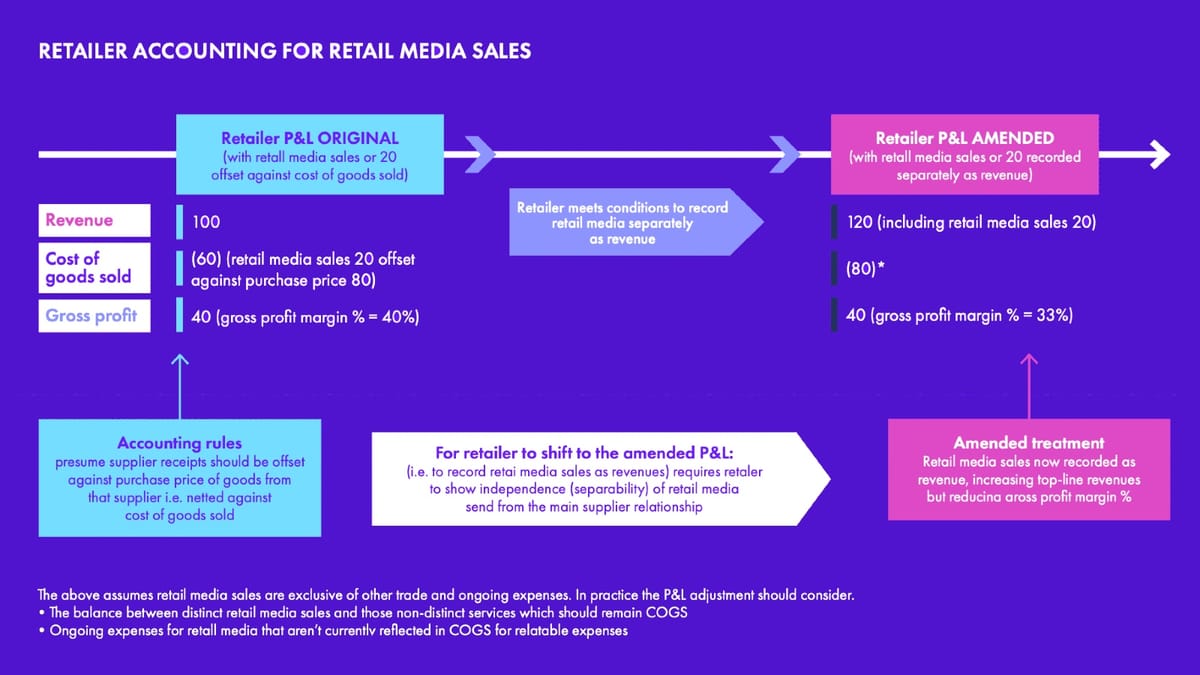

The paper includes a worked example that clarifies the stakes. In the original P&L, a retailer records revenue of 100, cost of goods sold of 60 (with retail media sales of 20 already offset against a purchase price of 80), and gross profit of 40 - a gross profit margin of 40%.

Under the amended treatment, where retail media sales of 20 are recorded separately as revenue, the top line becomes 120. The cost of goods sold adjusts to 80. Gross profit remains at 40, but the gross profit margin percentage falls to 33%.

The headline revenue figure increases, but the margin percentage declines. This is a point that deserves attention. A retailer that successfully reclassifies retail media as revenue will report a larger top line - but also a lower gross margin. Analysts and investors who track margin ratios rather than absolute revenue figures may interpret the change differently depending on how well it is explained in disclosure notes.

The paper draws a clear distinction between traditional retailers and online marketplaces - a distinction with direct relevance for platforms such as Amazon and eBay.

The key variable is the principal/agent question: does the marketplace take control of the goods being sold? According to the document, if the online marketplace buys the goods, stores them in its warehouse, sets the price, and so on, it is acting as principal. In that scenario, sales of retail media to suppliers will be offset against the cost of goods purchased from them, unless the separability conditions described above are satisfied.

If, however, the supplier stores the inventory, sets the price, and bears the returns risk, the online marketplace is acting as agent. In this scenario, there is no cost of goods sold for the marketplace - it never owns the goods. Any sales of digital retail media must therefore automatically be recorded as revenue. The accounting treatment, in this case, is not a choice: it is a structural outcome of the business model.

This distinction helps explain why certain marketplace operators have consistently reported clean, growing retail media revenue lines while traditional supermarket retailers have faced more ambiguity in how to present equivalent income.

Regardless of which treatment a retailer applies, disclosure obligations apply. According to the paper, both IFRS and US GAAP require retailers and online marketplaces to disclose material categories of income and their impact on revenue and/or cost of goods sold.

The relevant IFRS standards are IFRS 15 (Revenue Recognition), IFRS 8 (Operating Segments), and IAS 1 (Presentation of Financial Statements). The US GAAP equivalents are ASC 606, ASC 280, and ASC 205-20. The paper summarizes the disclosure rule clearly: if retail media is reported separately within the information regularly reviewed by senior management, it also merits separate disclosure in the external annual report.

This is an important point for the marketing community. If a retailer's leadership team receives regular reports on retail media performance as a standalone business segment, then investors and analysts should, in principle, be able to access equivalent information in the annual report. Where that separate disclosure is absent, questions arise about whether retail media has been formally constituted as a distinct internal reporting segment.

The paper closes with a specific explainer on what makes advertising "generic" and therefore eligible for distinct revenue recognition under IFRS 15. The standard it describes is demanding.

According to the document, advertising is only distinct if it provides a generic, retailer-agnostic benefit - such as brand building or universal promotions - rather than support that is specific to selling through a particular retailer. The test is essentially one of independence: does the advertising create value that exists beyond the specific commercial relationship?

The paper offers a concrete illustration of advertising that passes the test: promotion of a supplier's brand through non-price-specific messaging, delivered both on and off the retailer's platform, directing consumers to the supplier's own website rather than to a retailer-exclusive product page. This creates what the document describes as broader demand generation that exists independently of the trading relationship. Such advertising meets the criteria for being generic and distinct under IFRS 15 and can be recognized as revenue for the retailer.

This framing has direct implications for how Commerce Media Networks structure their advertising products. Networks that offer only retailer-specific placements - for instance, sponsored positions tied exclusively to that retailer's category hierarchy - may face a harder case for revenue recognition than those offering broader brand-building formats that run across channels.

The accounting questions raised in this paper have consequences well beyond the finance department. IAB Europe research has consistently found that 53% of buyers cite lack of standardization as the key barrier to retail media investment. The accounting inconsistencies described here are one structural reason why standard comparisons are so difficult to make.

If one retailer records retail media as revenue and another nets it against COGS, their reported financial profiles look materially different - even if the underlying commercial arrangements are identical. Market sizing exercises that aggregate publicly reported figures without adjusting for this difference will produce unreliable totals. That problem has been noted at PPC Land in coverage of the IAB Europe retail media statistics and in analysis of how commerce media maturity lags across industries.

Brands and agencies negotiating retail media deals may also find these distinctions commercially relevant. If a retailer structures media sales within the main supplier agreement, the accounting treatment on both sides changes. Advertisers may find that spend which they categorize as a marketing operating expense is being treated by the retailer as a reduction in purchase price - with different tax and margin implications for each party.

IAB Europe has been pushing toward standardized definitions and measurement frameworks since at least March 2025, when updated pan-European definitions covering on-site, off-site, and in-store retail media were published. The certification programme, which saw Albert Heijn become the first certified retail media network in September 2025, addresses measurement transparency. But accounting treatment sits upstream of measurement: it determines what figures enter the reporting pipeline in the first place.

The paper is the third in a five-part series. The first two papers, "Defining Trade and Media" (co-published with IAB US) and "The Case for Breaking Down Silos," examined the challenge through a business and operational lens. IAB Europe has indicated that further content in the series will be released in the coming weeks. The full paper is available for download from the IAB Europe website at 58.79 KB.

Who: IAB Europe and Mediasense, with the paper authored by Lauren Wakefield of IAB Europe.

What: The third paper in a five-part series examining the intersection of trade and media in retail media, focused specifically on how retailers and online marketplaces account for retail media sales under IFRS and US GAAP. The paper explains when retail media income can be recorded as revenue versus when it must be netted against cost of goods sold, and what conditions govern each treatment.

When: Published on March 12, 2026, as part of an ongoing series with further papers expected in the coming weeks.

Where: Published by IAB Europe, the Brussels-based European-level association for the digital marketing and advertising ecosystem, at iabeurope.eu.

Why: Accounting treatment directly shapes how different Commerce Media Networks report, classify, and interpret their revenue - creating inconsistencies that complicate market sizing, investor comparisons, and budget decisions by brands and agencies. As European retail media spending reached €13.7 billion in 2024 and continues to grow, the lack of clarity on how that revenue is recognized across companies has become a structural challenge for the industry.