Alphabet advertising revenues climb 14% as Gemini App reaches 750 million users

Description: Alphabet reported $113.8 billion in Q4 2025 revenues, with Google advertising up 14% and Gemini App hitting 750 million monthly active users, while announcing CapEx will reach $175-185 billion in 2026.

Alphabet Q4 2024: Gemini App reaches 750M users, YouTube hits $60B in ads and subscriptions

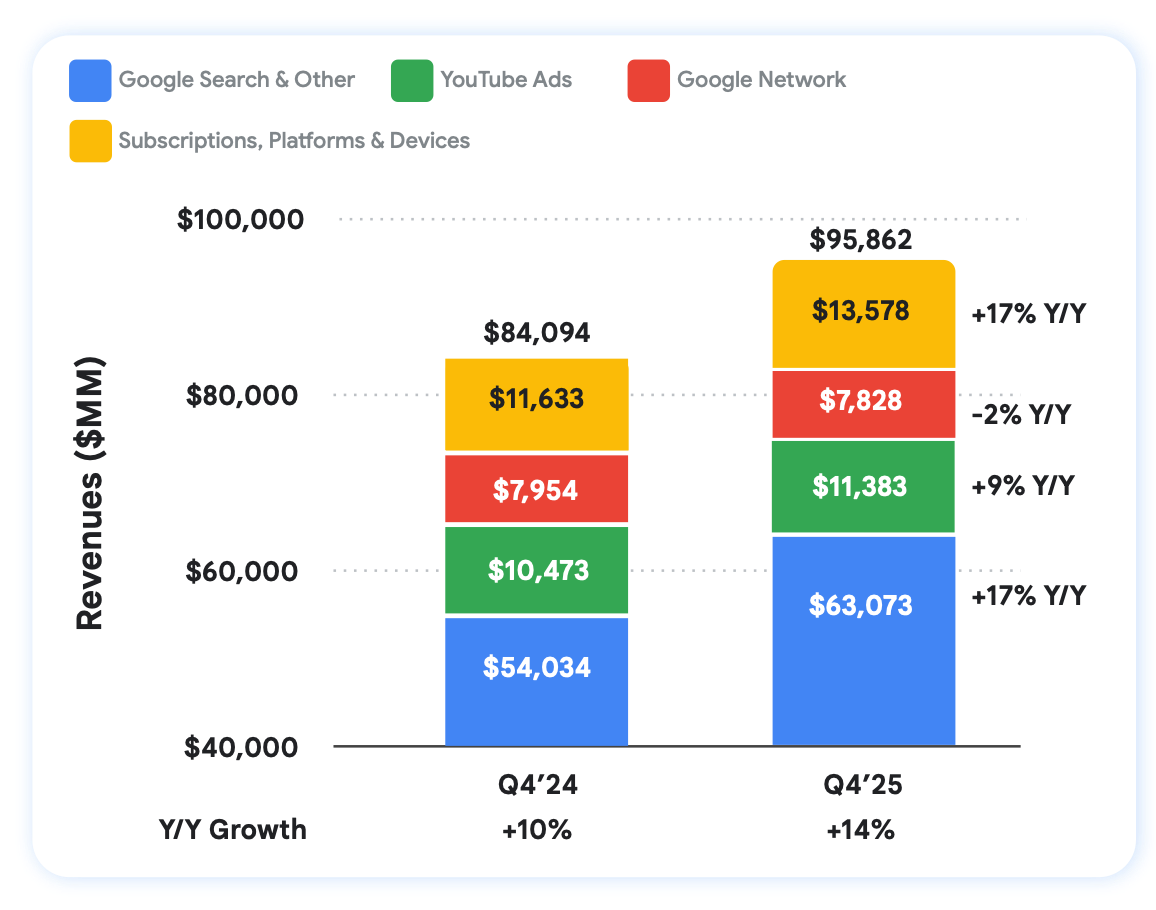

Alphabet today reported fourth quarter 2025 revenues of $113.8 billion, representing an 18% year-over-year increase, as the company disclosed that its Gemini App has grown to 750 million monthly active users and announced capital expenditure investments between $175 billion and $185 billion for 2026. The Mountain View-based technology company's advertising business generated $81.5 billion during the quarter, growing 14% from $71.5 billion in the prior year period, according to the earnings announcement released on February 4, 2026.

The advertising performance came despite ongoing concerns about Google Network revenues declining, which have faced pressure throughout 2025 as AI features increasingly retain users within Google's interface. The quarterly results demonstrate continued momentum across Google's owned properties including Search, YouTube, and expanding AI capabilities that are fundamentally reshaping how advertising operates across the company's ecosystem.

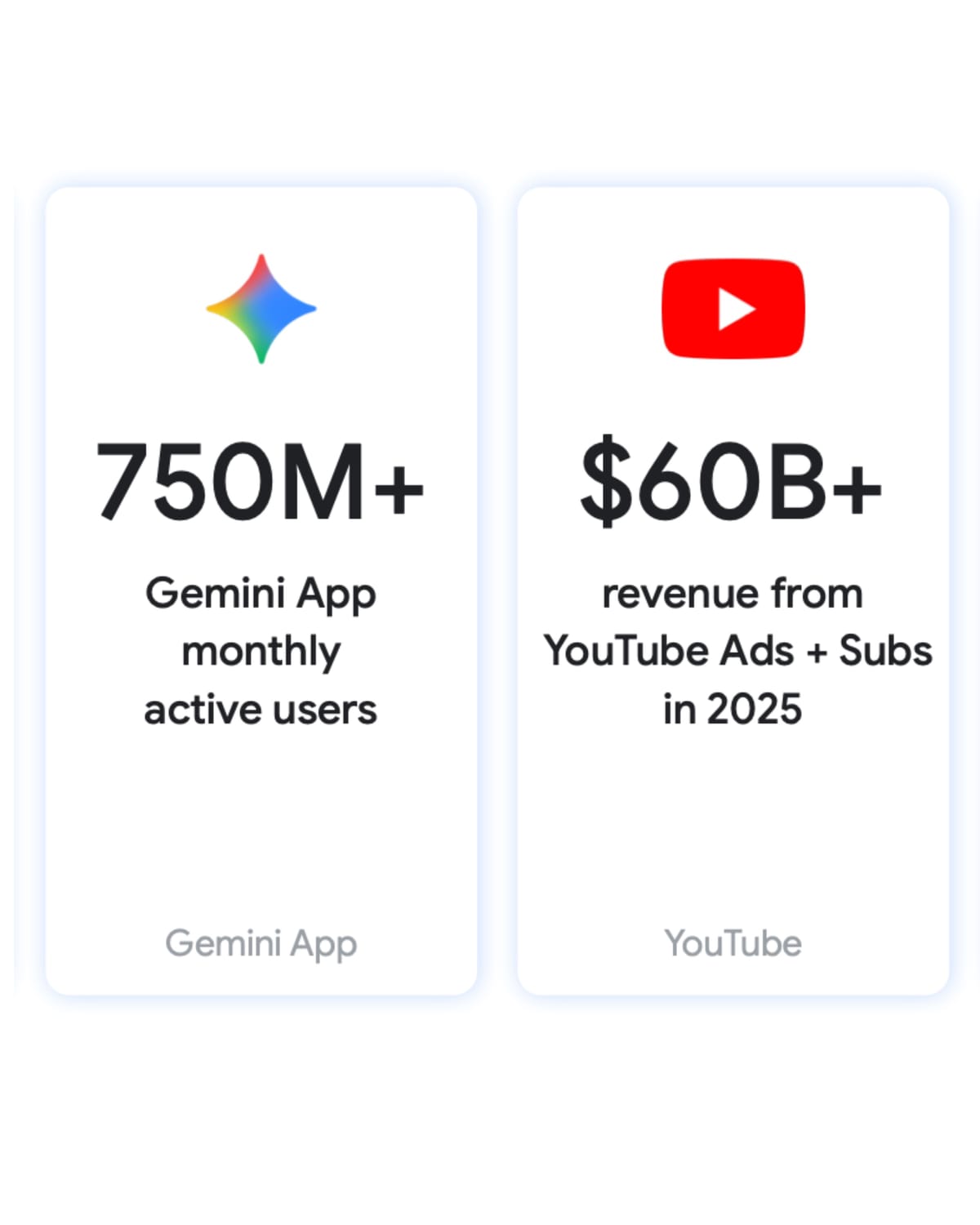

"It was a tremendous quarter for Alphabet and annual revenues exceeded $400 billion for the first time," stated Sundar Pichai, CEO of Alphabet and Google, according to the earnings announcement. "The launch of Gemini 3 was a major milestone and we have great momentum. Our first party models, like Gemini, now process over 10 billion tokens per minute via direct API use by our customers, and the Gemini App has grown to over 750 million monthly active users."

The results arrived as the company faces continued scrutiny over its publisher relationships, with advertising revenue distribution reaching 90% on owned properties during 2025 - a historic shift that has created tension between Google's role as a search engine directing users to relevant websites and its position as an advertising platform monetizing attention within owned properties.

Search advertising accelerates across major verticals

Google Search and other revenues reached $63.5 billion in the fourth quarter of 2025, marking a 14% increase from $55.8 billion in Q4 2024. The search advertising growth accelerated from previous quarters where performance had shown steady but not spectacular gains, with the company attributing the strength to improvements across nearly every major vertical category and the integration of advanced AI capabilities.

"Search saw more usage in Q4 than ever before, as AI continues to drive an expansionary moment," Pichai stated in the announcement. "We've executed with incredible speed. We shipped over 250 product launches within AI Mode and AI Overviews just last quarter."

According to Philipp Schindler, Senior Vice President and Chief Business Officer at Google, retail, finance, and health drove the greatest contribution to Search revenue during the quarter. "Nearly every major vertical actually accelerated in Q4," Schindler stated during the earnings call. The acceleration marks a significant shift from earlier 2024 periods when certain verticals, particularly financial services, had shown weaker performance that constrained overall growth rates.

The search advertising improvements came as Google integrated Gemini 3 directly into AI Mode, enabling the platform to better understand queries, dive deeper on the web, and generate interactive user interface experiences. According to the earnings call transcript, Google upgraded AI Overviews to Gemini 3 in late January 2026, providing users with enhanced responses at the top of the search results page.

User engagement patterns shifted substantially during the quarter, demonstrating how AI features are changing search behavior. In the United States, daily AI Mode queries per user doubled since launch, while queries in AI Mode averaged three times longer than traditional searches. Nearly one in six AI Mode queries now use non-text formats including voice or images, and Circle to Search expanded availability to over 580 million Android devices.

"The ongoing innovation, as you know, core to what we do and the enhancements to the user and the advertiser experience, really continue to drive our performance and make hundreds of these changes every quarter," Schindler stated during the call. "We see AI Overviews and AI Mode continue to drive greater Search usage and growth in overall queries, including important and commercial queries."

The emphasis on commercial queries represents a critical distinction for advertising performance. While AI features drive increased overall query volume, the proportion of queries with commercial intent - those where users are seeking to make purchases or evaluate products - determines revenue potential. Schindler's commentary suggests that AI features are successfully driving growth in these higher-value query categories rather than simply increasing informational queries that generate minimal advertising revenue.

Gemini-based improvements in Search Ads helped Google better match queries and craft creatives for advertisers, according to Schindler's remarks. The improvements extend understanding of intent, significantly expanding the platform's ability to deliver ads on longer and more complex searches that were previously difficult to monetize. This capability becomes increasingly important as users adopt more conversational search patterns through AI Mode, where traditional keyword-based matching proves less effective.

The quarter marked a inflection point where AI-driven changes to search behavior translated into measurable advertising revenue acceleration. Comparing Q4 2025's 14% growth with earlier 2024 quarters that showed more modest single-digit or low double-digit growth rates, the acceleration suggests Google's investments in AI capabilities are beginning to deliver tangible financial returns across its core search advertising business.

AI Max unlocks billions of net new advertising queries

AI Max for Search campaigns, which Google introduced in May 2025, continued expanding during the quarter with adoption by hundreds of thousands of advertisers. According to Schindler's comments during the earnings call, the automated campaign type "continues to unlock billions of net new queries" - a reference to advertising opportunities on searches that traditional campaign types failed to monetize effectively.

The platform leverages Gemini-based improvements that help Google better match queries and craft creatives for advertisers, enabling the company to serve relevant ads on longer, more complex searches that were previously difficult to monetize. "I talked about the understanding of intent and how this has significantly expanded our ability to deliver Ads on longer and more complex searches that were, frankly, previously difficult to monetize," Schindler explained during the call.

The AI Max infrastructure builds on Google's broader automation strategy through Performance Max campaigns, which have served as the testing ground for balancing automation efficiency with advertiser control requirements throughout 2024 and 2025. According to the earnings call, Google uses Gemini to generate millions of creative assets via text customization in AI Max and Performance Max campaigns, dramatically scaling the production of advertising creative without proportional increases in human labor.

Small and medium-sized business advertisers showed particular strength during the quarter, expanding their budgets and adopting automation tools that delivered improved return on investment. "We see strength with SMB advertisers expanding their budgets and adopting automation tools leading to better ROI," Schindler stated during the call. "On the creative side, we're using Gemini to generate millions of creative assets via text customization in AI Max and PMax and so on. So we're very pleased with what we're seeing here."

The SMB advertiser strength represents a important validation of Google's automation strategy. Smaller advertisers typically lack the resources for sophisticated campaign management and creative production that larger advertisers employ, making them ideal candidates for AI-powered automation. The budget expansion Schindler referenced suggests these tools are delivering measurable performance improvements rather than simply reducing management workload.

The emphasis on AI-powered creative production reflects Google's strategy of consolidating advertising operations within automated systems. The company launched Asset Studio in September 2025, providing advertisers with centralized creative generation capabilities powered by Imagen 4 and other generative AI models. By the fourth quarter, these capabilities had matured to the point where Google could generate millions of variations automatically, enabling scale and testing velocity impossible with traditional creative production workflows.

The "billions of net new queries" Schindler referenced represents advertising inventory that didn't exist under traditional campaign structures. These queries - typically longer, more conversational, and more complex than historical search patterns - couldn't be effectively matched with relevant ads using keyword-based systems. AI Max's ability to understand intent and generate appropriate creative for these queries creates incremental advertising opportunities that drive revenue growth beyond what simple query volume increases would generate.

YouTube advertising generated $17.2 billion during the fourth quarter of 2025, growing 13% year-over-year and pushing the platform's annual revenues past $60 billion for the first time when combining advertising and subscription services. The quarterly performance demonstrates sustained momentum across YouTube's multiple revenue streams including direct response advertising, brand campaigns, and expanding subscription services.

"YouTube's annual revenues surpassed $60 billion across ads and subscriptions," Pichai stated in the announcement. "We now have over 325 million paid subscriptions across consumer services, led by strong adoption for Google One and YouTube Premium."

The platform's advertising growth occurred despite competitive pressures from TikTok, which industry analysis suggests could surpass YouTube's advertising revenues excluding China by late 2025 or early 2026. YouTube's strategy has focused on positioning the platform as television rather than just online video, attempting to access the massive pool of traditional TV advertising dollars as the platform's growth rate continues its multi-year deceleration from peak rates exceeding 40% in 2021.

According to Schindler's comments during the earnings call, YouTube advertising performance reflected strength in direct response advertising followed by brand campaigns. The platform maintained its position as the number one streaming platform by watch time on television screens in the United States for 17 consecutive months through mid-2024, a metric that YouTube has leveraged to attract premium advertising inventory typically reserved for traditional television.

Connected TV viewing emerged as a critical growth driver for YouTube's advertising business during 2025. The platform redesigned its television playback interface in December 2025, repositioning controls and improving subscriber experiences across TV screens. The interface modifications support advertising growth by enhancing viewer experiences that encourage session duration and platform engagement, both critical metrics for advertising inventory value and campaign performance.

YouTube's advertising infrastructure expanded throughout the quarter with new targeting capabilities and creative formats designed to enhance campaign effectiveness. The platform launched specialized activation partners program in October 2025, providing advertisers with access to third-party experts including Channel Factory, MiQ Digital, Pixability, and Zefr for campaign optimization support. These partnerships acknowledge that YouTube's advertising complexity requires specialized expertise that many agencies and advertisers struggle to develop internally.

The platform introduced 30-second and 60-second non-skippable ads on YouTube Select and YouTube TV in May 2024, creating longer advertising formats that depend on sustained viewer engagement during extended playback sessions. Premium inventory quality on television screens attracts advertiser investment seeking reach comparable to traditional television buys but with digital advertising's measurement and targeting capabilities.

The subscription milestone of 325 million paid subscriptions across consumer services demonstrates user willingness to pay for enhanced experiences across Google's product portfolio. YouTube Premium removes advertisements and provides access to YouTube Music, while Google One offers expanded cloud storage and additional benefits across Google services. The subscription growth complements advertising revenues by diversifying YouTube's business model beyond purely advertising-supported content.

YouTube achieved revenue parity between Shorts and traditional video formats in the United States during the third quarter of 2025, according to earnings disclosures. This milestone demonstrates that YouTube successfully monetized the short-form video format that emerged as the primary competitive threat from TikTok. However, some creators have expressed concerns about home feed modifications that reduce long-form video prominence in favor of Shorts content, potentially affecting the type of advertising inventory YouTube can offer.

The $60 billion annual revenue milestone positions YouTube as one of the largest advertising platforms globally, generating revenues comparable to entire television networks. The platform's scale creates network effects where advertisers must maintain presence simply because audiences spend substantial time on YouTube, even as return on investment calculations become more challenging amid rising costs and competitive alternatives.

Google Network revenues continue downward trajectory

Google Network advertising revenues reached $7.3 billion in the fourth quarter of 2025, declining 3% from $7.5 billion in Q4 2024 and continuing the downward trajectory observed throughout 2025. The Network segment, which encompasses AdSense for website publishers, AdMob for mobile app monetization, and Google Ad Manager for programmatic advertising management, has faced mounting pressure as Google's advertising revenue distribution shifted to 90% on owned properties during the year.

The Network revenue decline represents a fundamental transformation in digital advertising economics, with millions of websites dependent on Google's advertising ecosystem experiencing reduced monetization opportunities. According to industry analysis following earlier quarters' earnings announcements in 2025, AI features increasingly retain users within Google's search interface rather than directing traffic to external websites where Network advertisements generate revenue.

"The 2% decline in Google Network revenues to $7.3 billion in Q1 2025 represents a significant shift in Alphabet's advertising ecosystem that can be directly linked to the company's strategic pivot toward Demand Gen campaigns," according to PPC Land's analysis of earlier quarterly results. While Q4 2025 showed a 3% decline, the pattern demonstrates consistent pressure on publisher monetization throughout the year.

The Network revenue trajectory contrasts sharply with growth across Google's owned properties, creating tension between the company's role as a search engine directing users to relevant websites and its position as an advertising platform monetizing user attention within owned properties. Publishers filed antitrust complaints with the European Commission in June 2025 alleging that Google's AI-powered search features caused significant harm including traffic, readership and revenue loss.

Jason Kint, president of Digital Content Next, highlighted the acceleration of this trend in August 2025: "Just updated data in light of eye-popping acceleration of 'zero-click' searches as Google's AI Overview scheme captures web traffic. I've been watching G's ad revenue mix shift from network (publishers) to its own properties for over a decade. It just hit 90% for first time."

Traffic acquisition costs reached $15.9 billion during the quarter, representing payments to distribution partners who direct search queries to Google properties including browser manufacturers, mobile device makers, and telecommunications carriers. TAC as a percentage of advertising revenues remained relatively stable compared to earlier periods, indicating that while absolute payments increased with revenue growth, the proportion of revenues shared with distribution partners did not change materially.

The Network decline occurred despite Google's attempts to provide publishers with enhanced monetization capabilities through programmatic advertising infrastructure. The company has systematically prioritized Demand Gen campaigns that route advertiser spending toward YouTube, Discover, and other Google-owned surfaces rather than directing investment toward third-party publisher websites through traditional Display campaigns.

BuzzFeed warned in its Q2 2025 Form 10-Q filing that AI-generated summaries often provide answers directly on the search results page, leading to fewer users clicking through to publisher websites. The warning signals potential industry transformation toward subscription, membership, or direct-pay content models as publishers reduce dependence on advertising revenue tied to search traffic volumes.

The minimal discussion of Network revenue performance during the earnings call suggests management views the decline as an expected outcome of strategic platform changes rather than a concern requiring detailed explanation. Schindler's brief acknowledgment of the decline without extensive commentary indicates Google has accepted reduced publisher revenue sharing as a necessary consequence of prioritizing owned property monetization and AI feature development.

Google Cloud achieves $17.6 billion in quarterly revenues

Google Cloud generated $17.6 billion in revenues during the fourth quarter of 2025, accelerating growth to 34% year-over-year from Q4 2024's performance. The cloud division reached an annual run rate exceeding $70 billion, driven primarily by demand for AI products and Google Cloud Platform adoption among enterprise customers seeking infrastructure to support their own AI initiatives.

"Google Cloud ended 2025 at an annual run rate of over $70 billion, representing a wide breadth of customers, driven by demand for AI products," Pichai stated in the announcement. The cloud performance demonstrates accelerating momentum as businesses adopt generative AI capabilities and migrate workloads to cloud infrastructure equipped to handle AI training and inference workloads.

According to comments during the earnings call, Google Cloud signed more deals exceeding $1 billion in value through 2025 than during the previous two years combined. New Google Cloud Platform customer additions increased 34% year-over-year, while existing customer engagement deepened with over 70% of current customers utilizing AI products. The dual metrics of new customer acquisition and expanded usage among existing customers suggest Google Cloud is capturing both market share and wallet share in the enterprise cloud market.

The cloud division's AI focus has driven substantial improvements in operating leverage throughout 2025. Previous quarters showed cloud operating income reaching $2.2 billion in Q1 2025 with operating margins improving year-over-year as the business scaled. The fourth quarter results suggested continued profitability expansion as the cloud business grows and achieves greater economies of scale.

Google Cloud's infrastructure investments support both enterprise customer needs and Alphabet's broader AI ambitions across all business segments. The company announced during the earnings call that approximately 60% of its 2025 capital expenditure investment went toward machines including servers, with 40% directed toward long-duration assets including data centers and networking equipment. For 2026, just over half of machine learning compute is expected to serve the Cloud business, with the remainder supporting Search, YouTube, and other consumer-facing products.

The cloud division released comprehensive agentic AI framework guidelines in November 2025, establishing standards for developing production-grade agentic AI systems. The 54-page technical document addresses the transition from predictive AI models to autonomous systems capable of independent problem-solving, providing developers, architects, and product leaders with foundations for building reliable, secure, and scalable applications.

Industry projections suggest the agentic AI market could reach approximately $1 trillion by 2035-2040, with over 90% of enterprises planning integration within three years. Google Cloud's positioning in this emerging market provides substantial growth opportunities beyond traditional cloud infrastructure and platform services. The company's survey datafrom September 2025 indicated that 88% of agentic AI early adopters achieve positive return on investment across multiple business applications.

The cloud division's technical leadership manifests in multiple dimensions. Google was the first cloud provider to offer NVIDIA's Blackwell B200 and GB200 GPUs, according to previous earnings calls, and will offer the next-generation Vera Rubin GPUs. This early access to cutting-edge AI training hardware provides Google Cloud with performance advantages that attract customers running large-scale AI workloads requiring the latest computational capabilities.

The $70 billion annual run rate positions Google Cloud as a significant player in the enterprise cloud market, though still substantially smaller than Amazon Web Services and Microsoft Azure. The 34% growth rate in Q4 2025 exceeds the overall cloud market growth rate, suggesting Google Cloud is gaining market share despite its third-place position in the competitive landscape.

Gemini 3 launch drives user engagement spike

The launch of Gemini 3 represented a major milestone during the quarter, with the AI model achieving state-of-the-art performance across major benchmarks. According to the earnings call, Gemini 3 scored 1501 Elo score on the LMArena Leaderboard and demonstrated PhD-level reasoning with 37.5% performance on Humanity's Last Exam - a benchmark designed to test capabilities on problems that would challenge expert humans.

"I think we definitely saw, I would say, extraordinary creative growth in Q4 for Gemini App," Pichai stated during the earnings call. "It's not just a growth in monthly active users, but there was a sharp increase in engagement per user on the app. So all the metrics, be it active usage, the intensity of usage, retention, all showed distinct progress across iOS, web, Android, et cetera, and geographically globally."

The Gemini App added 100 million monthly active users during the fourth quarter alone, reaching 750 million total users by the end of 2025. According to Pichai's comments, product experience improvements including work with Nano Banana and progress with Gemini models translated into strong momentum that continued into 2026.

First-party models including Gemini now process over 10 billion tokens per minute through direct API access by enterprise customers, representing substantial growth in technical infrastructure supporting AI capabilities. According to previous quarterly disclosures, the company processed over 1.3 quadrillion monthly tokens across all surfaces by October 2025, representing more than 20-fold growth over a 12-month period.

The Gemini 3 integration extended beyond the standalone app into Search experiences, fundamentally changing how users interact with Google's core product. According to the earnings call, Google integrated Gemini 3 directly into AI Mode in Search, enabling the platform to better understand queries, dive deeper on the web, and generate interactive UI experiences. The company upgraded AI Overviews to Gemini 3 in late January 2026, providing users with best-in-class AI responses at the top of search results pages.

"Obviously, there are many people who are getting a deeply AI-native experience in the context of AI Mode and Search as well, and we are definitely seeing strong growth and progress," Pichai stated during the call. "And the introduction of Gemini 3 in AI Mode was a very positive driver as well."

The technical architecture supporting Nano Banana Pro, built on the Gemini 3 Pro foundation, provides advanced image generation and editing capabilities for advertisers and creators. Google announced the system in November 2025, delivering studio-quality creative capabilities directly within Google Ads and marking a significant expansion of artificial intelligence integration across the company's advertising infrastructure.

The monetization strategy for Gemini App remains focused on free tier and subscription offerings rather than advertising integration, though management signaled openness to future advertising opportunities. According to Schindler's comments during the earnings call, the company focuses first and foremost on creating a great user experience with Ads and AI Overviews and early experiments in AI Mode. "In terms of the Gemini App, today, we are focused on the free tier and subscriptions and seeing great growth, as Sundar discussed," Schindler stated. "But Ads have always been part of scaling products to reach billions of people, and if done well, Ads can be really valuable and helpful commercial information."

Reports emerged in December 2025 that Google representatives told advertisers that ads would come to Gemini in 2026, though senior executives swiftly and publicly denied those claims. The conflicting signals highlight internal tensions around monetizing conversational AI experiences while the company already tests ads within AI Mode, its separate AI-powered search product launched in March 2025.

Capital expenditure guidance reaches unprecedented levels

Alphabet announced capital expenditure investments for 2026 will range between $175 billion and $185 billion, representing a substantial increase from 2025 levels and reflecting the company's commitment to AI infrastructure development. The CapEx guidance significantly exceeds previous investment levels and underscores the scale of infrastructure required to support expanding AI capabilities across Google's product portfolio.

"We're seeing our AI investments and infrastructure drive revenue and growth across the board," Pichai stated in the announcement. "To meet customer demand and capitalize on the growing opportunities we have ahead of us, our 2026 CapEx investments are anticipated to be in the range of $175 to $185 billion."

According to Anat Ashkenazi, Chief Financial Officer at Alphabet, during the earnings call, approximately 60% of the 2026 investment will go toward machines including servers, with 40% directed toward long-duration assets including data centers and networking equipment. The allocation reflects the computational intensity of training and serving large language models and other AI capabilities across Google's products.

The infrastructure investment supports multiple business priorities across Alphabet's operations. For 2026, just over half of machine learning compute is expected to serve the Cloud business, according to Ashkenazi's comments during the call. The remaining compute capacity supports Search, YouTube, and other Google products that increasingly rely on AI capabilities for core functionality including AI Mode, AI Overviews, Gemini integration, and automated advertising features.

The CapEx announcement drew scrutiny from investors concerned about the spending levels relative to near-term revenue generation and return on investment timelines. According to social media commentary captured in earnings analysis, some observers questioned whether the massive infrastructure investments could be justified by current revenue growth rates: "185 billion in Capex in one year, all into AI. Stock fell as investors worried about this spending."

Previous capital expenditure levels had already increased substantially throughout 2025. The company invested $91.4 billion in purchases of property and equipment during the trailing twelve months ending Q4 2025, according to the cash flow reconciliation in the earnings release. The 2026 guidance represents approximately doubling of infrastructure investment compared to 2025 levels, reflecting management's conviction that AI capabilities will drive future revenue growth across multiple business segments.

The infrastructure spending includes investments in NVIDIA's Blackwell GPUs and future Vera Rubin GPUs, according to previous earnings calls throughout 2025. Google maintains its position as the first cloud provider to offer these advanced AI training chips, providing competitive advantages in both enterprise cloud offerings and internal AI model development. The early access enables Google to train larger models more efficiently and serve inference workloads at lower cost compared to competitors using previous-generation hardware.

Ashkenazi explained during the call that long-duration assets like data center buildings might depreciate over 40 years or longer, while server equipment depreciates over shorter periods. This depreciation structure means the $175-185 billion investment doesn't translate directly into annual expense charges, spreading the accounting impact across multiple years while requiring upfront cash outlays that affect free cash flow calculations.

The question of CapEx allocation between Cloud business and other segments reveals strategic priorities. Allocating just over half of machine learning compute to Cloud in 2026 indicates that enterprise customer demand for AI infrastructure represents substantial revenue opportunity. However, the remaining compute supporting consumer-facing products like Search suggests Google views AI capabilities as critical to maintaining competitive positioning and user engagement even in products with established market dominance.

Comparative analysis with 2024 performance

Alphabet's Q4 2025 performance demonstrated significant acceleration across most metrics compared to the prior year period. Total revenues of $113.8 billion in Q4 2025 increased 18% from $96.5 billion in Q4 2024, while advertising revenues grew 14% from $71.5 billion to $81.5 billion. The year-over-year comparisons reveal strengthening momentum as AI capabilities mature and contribute meaningfully to advertising performance.

Google Search and other revenues reached $63.5 billion in Q4 2025, growing 14% from $55.8 billion in Q4 2024. The search advertising acceleration marked a notable improvement from mid-2024 quarters when growth rates had been more modest. According to previous analysis, Q2 2024 showed search revenues at $54.2 billion with 12% growth, suggesting the Q4 2025 performance represented meaningful acceleration in the company's core business as AI features matured.

YouTube advertising revenues increased 13% to $17.2 billion in Q4 2025 from $15.2 billion in Q4 2024. The growth rate remained relatively consistent with earlier 2024 and 2025 quarters, though industry analysis suggested YouTube's advertising growth has decelerated from peak rates of 45.9% in 2021 to current mid-teens percentage growth as the business matures and faces increased competition from TikTok and other short-form video platforms.

Google Network revenues declined 3% to $7.3 billion in Q4 2025 from $7.5 billion in Q4 2024, continuing and accelerating the pattern of Network advertising pressure observed throughout 2024 and intensifying in 2025. The year-over-year decline accelerated from the 1% decrease observed in some earlier 2025 quarters, suggesting mounting challenges for publisher monetization through Google's advertising programs as AI features captured more user attention.

Google Cloud revenues grew 34% to $17.6 billion in Q4 2025 from $13.1 billion in Q4 2024. The cloud acceleration represented the fastest growth rate among Alphabet's major business segments and demonstrated strong demand for AI infrastructure and platform services. The cloud performance contrasted with more modest growth in advertising, highlighting how AI investments were driving expansion differentially across different parts of the business.

Comparing full year 2025 results with full year 2024 provides additional context for the company's trajectory. Total revenues reached $402.8 billion in 2025, growing 15% from $350.0 billion in 2024. The milestone of exceeding $400 billion in annual revenues underscores Alphabet's continued expansion despite operating in mature markets where maintaining double-digit growth becomes progressively more challenging.

Total advertising revenues for full year 2025 reached $310.5 billion, growing 14% from $272.4 billion in 2024. The advertising segment represented 77% of total Alphabet revenues, demonstrating continued dependence on advertising despite diversification efforts into cloud computing and subscription services. The consistency of advertising's revenue contribution suggests that near-term diversification away from advertising remains challenging despite cloud growth.

The geographic revenue distribution showed strength across all major markets during Q4 2025. United States generated $55.4 billion, representing 17% growth from Q4 2024. EMEA contributed $33.1 billion with 17% growth in constant currency terms, while Asia-Pacific reached $18.5 billion with 22% growth. Other Americas generated $6.9 billion with 20% growth, demonstrating broad-based demand across global markets.

Marketing community implications

The Q4 2025 earnings results carry substantial implications for marketing professionals managing advertising campaigns across Google's platforms. The continued growth in Search advertising combined with AI Max adoption reaching hundreds of thousands of advertisers suggests that automated campaign types will increasingly dominate advertising strategies, requiring marketers to develop expertise in AI-powered optimization rather than manual campaign management.

The Network revenue decline creates ongoing challenges for marketing strategies that rely on Display advertising reaching audiences through publisher websites. Previous analysis indicated that 90% of Google's advertising revenue now flows to owned properties rather than through publisher partnerships, fundamentally altering the economics of display advertising campaigns. Marketers may need to continue shifting budgets toward Demand Gen campaigns targeting YouTube, Discover, and other Google-owned surfaces to maintain reach and performance.

The YouTube advertising performance demonstrates continued viability of video advertising despite competitive pressures from TikTok and other platforms. The platform's focus on Connected TV viewing and premium television inventory creates opportunities for marketers seeking to reach audiences in living room environments where attention levels typically exceed mobile viewing. However, the home feed modifications that reduce long-form video prominence in favor of Shorts content may require adjustments to creative strategies and content format priorities.

The emphasis on AI-powered creative production through Asset Studio and text customization capabilities reflects Google's strategic direction toward automated asset generation. Marketers will increasingly need to provide brand guidelines, style references, and strategic direction to AI systems rather than creating individual advertising assets manually. The ability to generate millions of creative variations enables testing and optimization at scale previously impossible with human-only production workflows.

The CapEx guidance of $175-185 billion for 2026 signals Google's commitment to maintaining technological leadership in AI capabilities. For marketing professionals, this investment trajectory suggests continuous improvements in advertising targeting, creative optimization, and performance measurement capabilities throughout 2026 and beyond. However, the scale of infrastructure spending also raises questions about how aggressively Google will pursue monetization of AI features to generate returns on these investments.

The "billions of net new queries" that AI Max unlocks represents a significant expansion of addressable advertising inventory. Marketers who successfully adopt AI-powered campaign types can access audiences during longer, more complex searches that traditional keyword-based campaigns couldn't effectively monetize. This creates competitive advantages for early adopters while potentially disadvantaging advertisers who rely exclusively on traditional campaign structures.

The advertising cost environment continues evolving as AI features change user behavior and competitive dynamics. According to previous benchmarks, Google Ads costs rose 10.43% year-over-year in 2024, with cost per click reaching $4.66 across industries. The Q4 2025 results don't provide specific cost metrics, but the revenue growth suggests continued healthy advertiser demand that typically correlates with rising costs per click.

Conference call highlights and executive commentary

The Q4 2025 earnings call provided substantial detail about Google's advertising performance and strategic priorities for 2026. Schindler's commentary emphasized that search advertising acceleration resulted from strength across multiple verticals rather than any single driver, suggesting broad-based demand improvement rather than isolated category spikes that might prove temporary.

"The acceleration we saw in Search was not due to a single driver, but was really the result of many different parts of our business showing strength and working well together," Schindler stated during the call. "And maybe I'll quickly add the vertical perspective: Retail, Finance, Health drove actually the greatest contribution to Search revenue. Nearly every major vertical actually accelerated in Q4."

The multi-vertical strength contrasts with earlier 2024 periods when financial services weakness offset gains in other categories like retail. The fourth quarter 2025 performance suggests that whatever factors had constrained financial services advertising in early 2024 had resolved by year-end 2025, allowing all major verticals to contribute positively to growth.

Pichai's emphasis on the "expansionary moment" in search usage highlights management's conviction that AI features are growing the addressable market for search advertising rather than simply redistributing existing query volumes. The doubling of daily AI Mode queries per user in the United States since launch supports this narrative, though questions remain about whether AI-driven query growth translates proportionally into advertising revenues given that AI Overviews can answer queries without users clicking through to websites.

The discussion of Gemini App cannibalization addressed investor concerns about whether AI chatbot usage might reduce traditional search volumes and thereby impact advertising revenues. "Right now, overall, I think we are giving people choice," Pichai stated. "People are obviously using Search, experiencing AI Overviews and AI Mode as part of it, and Gemini App as well. The combination of all of that, I think, creates an expansionary moment. I think it's expanding the type of queries people do with Google overall. So overall, some of it is what we see as a growth opportunity, and we haven't seen any evidence of cannibalization there."

This commentary represents management's attempt to reassure investors that AI capabilities complement rather than cannibalize traditional search usage. The lack of observed cannibalization through Q4 2025 provides evidence supporting this view, though long-term dynamics remain uncertain as AI capabilities continue improving and user behavior continues evolving.

Questions about CapEx depreciation and allocation provided insight into how Alphabet manages its massive infrastructure investments. Ashkenazi explained that approximately 60% of investment goes toward machines with relatively shorter depreciation schedules, while 40% funds long-duration assets including buildings that might depreciate over 40 years or longer. The allocation of machine learning compute, with just over half supporting Cloud business in 2026, reveals how infrastructure serves both external customer needs and internal product development.

The minimal discussion of Network revenue performance during the call suggests management views the decline as an expected outcome of strategic platform changes rather than a concern requiring detailed explanation. Schindler's brief acknowledgment of the decline without extensive commentary indicates Google has accepted reduced publisher revenue sharing as a necessary consequence of prioritizing owned property monetization and AI feature development.

One analyst asked about premium subscriptions playing a role in monetizing AI search activity, given the more conversational nature and longer engagement periods that might not translate well to traditional advertising models. The question highlights investor uncertainty about how Google will monetize AI features that provide answers directly without directing users to advertiser websites or generating traditional ad clicks.

Regulatory and competitive landscape context

The earnings results arrive amid ongoing regulatory scrutiny of Google's advertising business across multiple jurisdictions. Court rulings in April 2025 found Google illegally monopolized publisher ad server and exchange markets, with remedies trials concluding in November 2025. The regulatory outcomes could affect Google's ability to operate its advertising technology stack as currently structured, particularly regarding publisher monetization through Network advertising programs.

The European Commission investigations continue examining whether Google's AI-powered search features cause disproportionate harm to publishers. According to previous reports throughout 2025, publishers filed antitrust complaints alleging that AI Overviews and AI Mode significantly reduce traffic, readership and revenue for content creators whose material trains the AI systems. The earnings results showing continued Network revenue declines and 90% of advertising revenue flowing to owned properties provide evidence supporting publisher concerns about the business impact of AI features.

Competitive dynamics with OpenAI's ChatGPT remain relevant despite Gemini App's substantial user growth to 750 million monthly active users. According to industry analysis, ChatGPT maintains a commanding lead in U.S. AI chatbot traffic, though Google Gemini has climbed rankings throughout 2025. The competition for AI search usage will likely intensify in 2026 as both platforms improve capabilities and pursue different monetization strategies.

The relationship with Apple regarding Search default placement faces uncertainty following disclosure during the Department of Justice antitrust trial. According to the earnings call, previous agreements involved revenue sharing arrangements, but management commentary suggested future partnerships might require different alignment approaches as AI search and Gemini integration provide utility beyond traditional search revenues. "If you think about the utility that you're driving through AI search and through Gemini on those platforms, it may be less related to the actual quote-unquote Search revenue," one analyst noted during Q&A.

The announcement of CapEx reaching $175-185 billion in 2026 creates competitive pressure for other technology companies pursuing AI capabilities. The scale of Google's infrastructure investment establishes barriers to entry for potential competitors while signaling management's conviction that AI will drive future business growth. However, the spending levels also create expectations for revenue acceleration that management must deliver to justify the capital allocation.

Financial summary and full-year 2025 results

For the full year 2025, Alphabet reported total revenues of $402.8 billion, representing 15% growth from $350.0 billion in 2024. The milestone of exceeding $400 billion in annual revenues underscores the company's scale and continued growth trajectory despite facing mature market dynamics in search advertising and competitive pressures in cloud computing and video platforms.

Total advertising revenues reached $310.5 billion for full year 2025, growing 14% from $272.4 billion in 2024. The advertising segment represented 77% of total Alphabet revenues, demonstrating continued dependence on advertising despite diversification efforts into cloud computing and subscription services. The percentage remained relatively stable compared to prior years, suggesting that near-term material shifts in revenue composition remain challenging.

Google Services, which encompasses advertising plus subscriptions and devices, generated $356.6 billion in revenues for full year 2025, representing 12% growth year-over-year. The segment achieved operating income of $134.6 billion with a 37.8% operating margin, demonstrating the profitability of advertising-driven business models even as costs associated with AI development and infrastructure increase.

Google Cloud full year revenues reached $70.3 billion, accelerating growth to 33% from prior years. The cloud division achieved $11.0 billion in operating income with a 15.6% operating margin, marking continued progress toward profitability targets and demonstrating that the business can generate meaningful profits at scale. The cloud performance reflects increasing adoption of AI infrastructure services and Google Cloud Platform across enterprise customers.

Operating cash flow for full year 2025 reached $164.7 billion, providing substantial resources for capital expenditures and strategic investments. Free cash flow totaled $73.3 billion after deducting $91.4 billion in capital expenditures, reflecting the scale of infrastructure investment required to support AI capabilities across Google's product portfolio. The free cash flow represents approximately 18% of revenues, indicating healthy cash generation despite massive infrastructure spending.

The company ended Q4 2025 with $95.1 billion in cash, cash equivalents, and marketable securities. Long-term debt increased to $23.6 billion from $10.9 billion at the end of 2024, primarily due to senior unsecured notes issued in May 2025 for $12.5 billion in net proceeds. The debt increase provides additional financial flexibility for infrastructure investments without requiring asset sales or equity issuance while maintaining conservative leverage ratios.

Other income and expense for Q4 2025 totaled $3.2 billion, including $2.3 billion in gains on equity securities that increased net income by $1.8 billion after tax effects. The equity gains contributed $0.15 to diluted earnings per share, highlighting how fluctuations in investment portfolio value can significantly impact reported earnings in individual quarters.

Net income reached $35.0 billion for Q4 2025, increasing 33% from the prior year period. Diluted earnings per share grew 35% to $2.87, reflecting both revenue growth and operating leverage improvements across the business. The earnings growth exceeded revenue growth, demonstrating improving profitability as the company scales its operations.

Timeline

December 31, 2025 - Alphabet Q4 2025 quarter ends with $113.8 billion in revenues

February 4, 2026 - Alphabet announces Q4 2025 earnings results with Gemini App reaching 750 million users

January 2026 - AI Overviews upgraded to Gemini 3, improving search result quality

Who: Alphabet Inc., Google's parent company, announced quarterly results with CEO Sundar Pichai highlighting AI achievements and CFO Anat Ashkenazi providing financial metrics and 2026 capital expenditure guidance during the earnings call.

What: Alphabet reported Q4 2025 revenues of $113.8 billion (18% growth year-over-year), with advertising revenues of $81.5 billion (14% growth), Google Cloud reaching $17.6 billion (34% growth), and Gemini App growing to 750 million monthly active users. The company announced 2026 capital expenditure investments between $175-185 billion to support AI infrastructure development.

When: The fourth quarter ended December 31, 2025, with earnings announced on February 4, 2026. Full year 2025 revenues exceeded $400 billion for the first time in company history, reaching $402.8 billion.

Where: Results span global operations with United States generating $55.4 billion (17% growth), EMEA contributing $33.1 billion (17% constant currency growth), Asia-Pacific reaching $18.5 billion (22% growth), and Other Americas generating $6.9 billion (20% growth) during Q4 2025.

Why: The financial performance reflects successful AI integration across advertising products including AI Mode and AI Overviews driving increased search usage and unlocking billions of net new advertising queries through AI Max adoption by hundreds of thousands of advertisers. YouTube advertising maintained mid-teens growth rates reaching $60 billion annually combined with subscriptions. Google Cloud accelerated adoption of AI infrastructure services with enterprise customers demanding capabilities to support their own AI initiatives. Gemini App achieved substantial user growth to 750 million monthly active users following Gemini 3 launch with state-of-the-art AI performance. The massive 2026 CapEx guidance of $175-185 billion signals management's conviction that AI capabilities will drive future revenue growth across multiple business segments despite near-term investment intensity requiring substantial infrastructure spending.

Share this article

The link has been copied!

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Your link has expired. Please request a new one.

Great! You've successfully signed up.

Great! You've successfully signed up.

Welcome back! You've successfully signed in.

Success! You now have access to additional content.