IAB Australia published its tenth annual Audio Advertising State of the Nation report on March 3, 2026, marking a decade since the inaugural survey first brought together traditional and streaming radio players in one study. The findings confirm that Australian digital audio advertising has crossed $339 million in annual spend, growing 8.2% year-on-year from 2024 to 2025, yet the same structural constraint - fragmented measurement - that has shadowed the channel for years shows no sign of resolution.

The report, conducted in November and December 2025, drew 128 survey responses from the advertising buy-side. According to the report, 95% of respondents came from media, creative, and digital advertising agencies, with 5% from brands buying advertising directly. Large holding-group agencies represented 68% of the agency sample, while smaller independent agencies made up the remaining 32%. All respondents either placed or planned audio advertising campaigns, making this one of the more focused datasets available on practitioner intentions in Australia's audio market.

The market in numbers

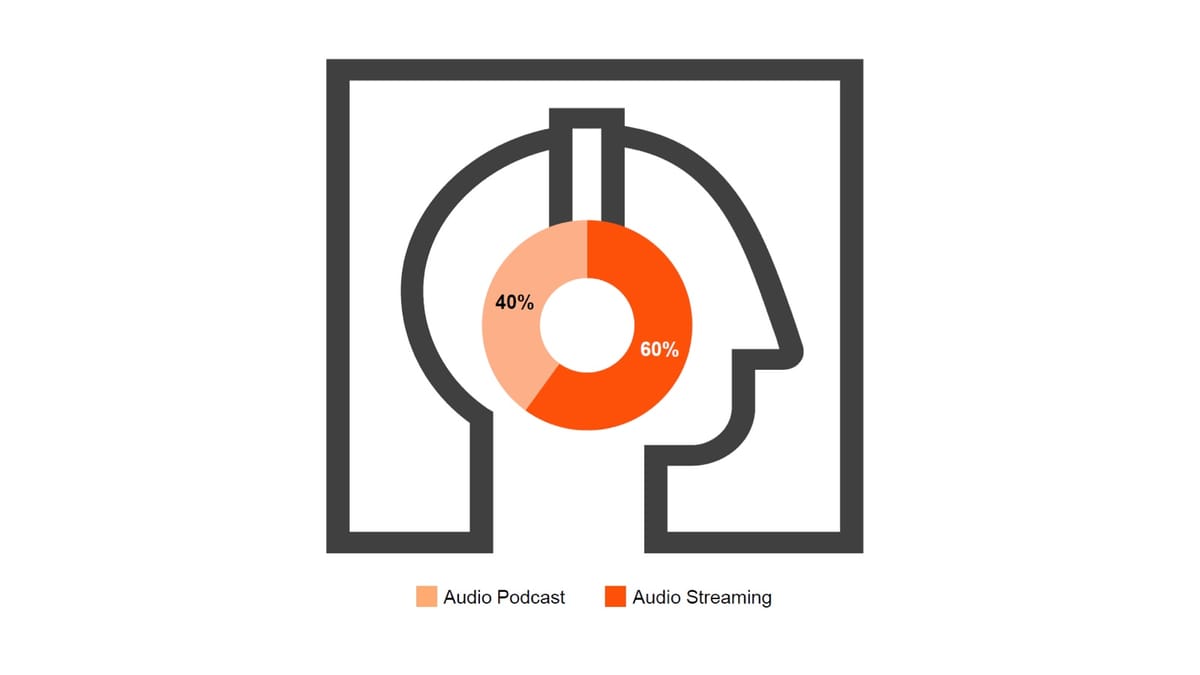

The $339 million figure, sourced from the IAB Australia Internet Advertising Revenue Report for calendar year 2025 and prepared by PwC, breaks into two distinct sub-segments. Streaming audio generated $205 million, up 5.0% on 2024. Podcast advertising reached $134 million, expanding at a faster 13.5% clip - more than double the streaming rate. Audio as a whole represents 4.5% of total 2025 general display advertising expenditure in Australia.

The trajectory goes back further. Total audio stood at just $220 million in 2022, climbed to $266 million in 2023, then $313 million in 2024 before reaching $339 million in 2025. Podcast spend specifically has moved from $81 million in 2022 to $99 million, $118 million, and now $134 million in successive years. Streaming audio followed a shallower but consistent path: $139 million in 2022, rising to $167 million, $195 million, and $205 million in 2025. The divergence in growth rates signals that advertiser appetite for on-demand, creator-led formats is pulling capital away from live and linear streaming.

Investment intentions for 2026

Forward-looking sentiment in the report is notably positive. According to the report, 69% of respondents plan to at least slightly increase investment in original content podcast advertising in 2026, while 56% plan to increase spending on streaming music advertising. These figures sit against a backdrop in which nearly every other audio format - broadcast AM/FM, DAB+ only stations, catch-up radio - commands a smaller share of growth intent.

The shift toward sponsorships and custom integrations is particularly sharp. Two-thirds of respondents plan to use audio advertising sponsorship or custom integration, such as presenter reads, brand mentions, and branded content, in 2026. That compares to 59% who actually bought these formats in 2025 - a 7 percentage point increase in intention. Over half of respondents (54%) also intend to buy digital audio combined with other media opportunities and extensions such as video, social, events, and competitions in 2026, up from 46% who did so in 2025. Self-service buying and retail or in-store audio advertising also show growing planned adoption.

On the performance versus brand split, 37% of respondents plan to at least slightly increase the share of spend on performance advertising relative to brand in 2026, while 27% expect to shift slightly more toward brand. This tilt toward performance reflects a cost-conscious environment in which, as one practitioner quoted in the report put it, "a lot of marketers are concerned about sales results at the moment rather than brand uplift."

Why audiences matter more than reach

The report identifies a notable shift in what drives audio investment. Audience attention and engagement ranked as the number one driver for using digital audio advertising, cited by 56% of respondents and up 6 percentage points on the previous year. Access to talent and content creators rose even more sharply, jumping 10 percentage points to 51% - now the second-ranked driver. Brand building capabilities climbed 9 percentage points, and brand integrations and custom executions rose 8 percentage points.

At the same time, digital audio's role in delivering incremental reach alongside other media weakened as a primary driver. This suggests that planners are repositioning audio less as a reach extension channel and more as a brand-building and engagement vehicle in its own right, particularly through creator relationships. Australian podcast listenership reached 9.6 million monthly listeners in 2025, representing 47% of the population aged 15 and older, according to separate research published in 2025. That audience base provides the foundation for the creator-driven approach now registering so clearly in buyer intentions.

Recorded spots and host-read podcast ads remain the most widely used creative formats, both increasing in usage by 5 percentage points year-on-year according to the report. Recorded spots were used by 84% of respondents, host reads by 82%. Repurposed radio spots came in at 66%, publisher-created podcast-specific spots at 63%.

Video-enabled podcast formats occupy a more ambiguous position. According to the report, 75% of respondents have had some level of consideration of placing ads in video podcasts, with 50% having researched or discussed the opportunity, 18% having tested a few placements, and 7% regularly including the format in campaigns. The report notes that high appetite to experiment with video-enabled and branded podcasts existed in 2025 as well, but that strong intention last year did not translate into significantly higher actual usage. Whether 2026 breaks that pattern remains to be seen.

Six in ten respondents (61%) have experience using podcast creators and talent as part of their creator marketing strategy, with 43% having tested the approach in a few campaigns and 18% including it regularly. A further 17% are researching or discussing the opportunity. The report draws a comparison to US data from the IAB US 2025 Outlook Study, which projected US Creator Economy ad spend to reach $37 billion in 2025, growing 26% - four times faster than the media industry overall.

Programmatic audio: stable, but shifting toward guaranteed

Programmatic buying remains stable. According to the report, 72% of respondents bought audio programmatically in 2025, up from 63% in 2023, and 70% plan to continue in 2026. The composition of that programmatic activity is shifting, however. Among those buying streaming audio programmatically in 2025, 55% used private marketplace deals. In 2026, 68% plan to buy streaming audio via guaranteed deal - a significant move toward certainty over open exchange exposure. The pattern repeats for podcast advertising: 43% used guaranteed deals in 2025, rising to an intended 62% in 2026.

Data and targeting continues to dominate the reasons for choosing programmatic audio, cited by 74% of those buying programmatically. Flexible buying options (48%) and price (43%) follow, both rising year-on-year. One anonymous agency director quoted in the report captured the broader ambition: "The biggest impact for the audio industry would come from making digital audio fully accessible programmatically with clear transparency."

Triton Digital introduced enhanced audience intelligence tools in August 2025, combining survey data with download metrics to deliver demographic insights across 200 podcasts - reflecting the broader push to bring better targeting data into the audio programmatic stack.

Demographic and geographic targeting remain the most common audience targeting approaches when buying digital audio, used by 92% and 79% of respondents respectively. Contextual signals rose 9 percentage points year-on-year to 59%, while third-party data overlay increased 8 percentage points to 54%.

Measurement: the persistent constraint

The report's section on effectiveness measurement confirms that the channel's growth ceiling is partly a ceiling on proof. Campaign audience reporting (reach and frequency) is used by 67% of respondents, campaign volume reporting by 64%, and digital brand lift surveys by 63%. For measuring sales impact and ROI specifically, Market Mix Modelling has become the leading tool, used by 44% of respondents, followed by online conversion tracking at 32%.

Yet fragmentation creates persistent problems. According to the report, 29% of respondents cited fragmented audio formats preventing holistic measurement as the top challenge, followed by lack of standardised audience data for digital audio planning at 27%, and lack of standardised audience data spanning both digital and traditional audio at 25%. Last-touch attribution models undervaluing audio were cited by 25%. The cost of measurement outweighing the ad investment itself ranked at 23%.

One agency director summarised the structural problem directly in the report's open-ended responses: "The current audio landscape is highly fragmented. Listeners consume content across numerous platforms and devices - streaming music, podcasts on different apps, smart speakers, video podcasts on YouTube - and each silo often uses different tracking methods. This makes it incredibly difficult for advertisers to get a single, accurate view of campaign performance."

Another practitioner was more specific about what a solution should look like, calling for "standardised metrics for reach, incremental reach, verified listens and attribution," while noting that download counts are a poor proxy for actual listening. The demand for a standardised listen-through rate and verified play count - bringing audio measurement closer to the digital video standard - has appeared in previous waves of the survey and continues unresolved.

When asked what would be the most impactful action the industry could take, respondents pointed to proof of effectiveness and improved attribution as the leading priorities. "If we could unify attribution, allow cross platform frequency control and deliver genuine incremental reach visibility, more dollars would move into audio simply because it becomes easier to justify investment to stakeholders," one agency strategist is quoted as saying.

Acast and Barometer launched an episode-level pre-bid targeting integration in January 2026, processing every newly published episode in real time against IAB categories and contextual signals. That development addresses the brand safety side of the measurement picture, but the deeper accountability questions around reach deduplication and ROI attribution remain industry-wide problems without equivalent solutions yet.

AI: welcome in optimization, cautious in content

The report dedicates significant space to AI adoption, and the split in attitudes is stark. Australian ad buyers are substantially more comfortable with AI in advertising optimization than in content production. According to the report, 94% of respondents are at least somewhat comfortable with AI being used in dynamic creative optimisation (DCO), with 47% very comfortable. Content and creative post-production - editing, voice enhancement, timing adjustments - attracts 79% at least somewhat comfortable.

AI-generated host reads and voice clones for personal endorsements are another matter entirely. Six in ten respondents (59%) are not at all comfortable or unsure about this application. The concern centers on authenticity: the same qualities that make host-read podcast advertising effective - the personal endorsement, the sense of a trusted voice speaking from experience - are precisely what synthetic voice threatens to undermine. The report notes that 95% of US brands have concerns about using AI in creator marketing, with the predominant concern being lack of authenticity or human connection, referencing IAB US data.

On the opportunity side, the top AI use cases respondents identified for audio advertising planning, activation, and analysis were: analysing and reporting performance against goals (25%), determining optimal media mix, pacing, and pricing (22%), predictive real-time budget and bid adjustments (21%), and tracking and optimising ad delivery and conversions (20%). Marketing Mix Model optimisation ranked at 18%.

The voice-enabled commerce dimension also features in the report. Prior to conversational AI, voice-assisted shopping generated $4.6 billion in global sales revenue in 2021. That figure is projected by referenced sources to reach $81.8 billion in 2025, representing a 1,700% increase. Conversational shopping more broadly is projected to rise from $41 billion in 2021 to $473 billion in 2026. Australian ad buyers flagged this as an opportunity in open-ended responses while noting real reservations: voice-enabled advertising has not historically gained traction in the Australian market, and clients are expected to proceed cautiously.

What this means for marketers

The tenth-wave report captures an industry that has moved convincingly from emerging to established, without fully resolving the tensions that have accompanied it. The $339 million total is real money. The 8.2% growth rate outpaces many traditional media categories. The 69% of respondents planning podcast investment increases represents genuine forward intent.

But the measurement infrastructure has not kept pace with the commercial opportunity. Global research published in December 2025 showed that advertisers directed just 43.5% of age-targeted podcast impressions toward the 25-34 demographic while neglecting the 55-64 and 65+ cohorts - a pattern traceable in part to the same fragmentation problems the Australian report identifies. Separate data from AdsWizz showed consumers spending 31% of media time with audio while advertisers allocate only 9% of budgets, a 22-point gap that reflects confidence problems more than audience availability problems.

The IAB Australia Audio Council, which co-produces the State of the Nation series and includes member representatives from Acast, ARN, Spotify, The Trade Desk, Magnite, GroupM, Publicis, Nova Entertainment, and others, launched the series in 2015 with the goal of educating marketers and agencies on the value of digital audio. Ten years of data now exist. The question the tenth wave poses clearly is whether a further decade of growth can be sustained without a shared measurement currency that makes planning, optimisation, and proof of ROI as straightforward in audio as it already is in digital video.

Timeline

- 2015 - IAB Australia launches the Audio Council and inaugurates the Audio Advertising State of the Nation survey series, bringing traditional and streaming radio players together for the first time

- 2022 - Total Australian digital audio and podcast advertising expenditure reaches $220 million ($139m streaming, $81m podcast)

- 2023 - Total audio spend climbs to $266 million ($167m streaming, $99m podcast); programmatic audio buying rises to 63% adoption among surveyed buyers

- August 2024 - Australian podcast listenership grows 8.7% year-over-year in the January-June 2024 period, with 42% total increase over two years

- August 2025 - IAB Australia releases alcohol advertising compliance guides for digital audio, reflecting the category's regulatory maturation

- August 2025 - Australian podcast listenership reaches 9.6 million monthly listeners (47% of population aged 15+), up 7% year-on-year; blue-collar workers emerge as fastest-growing segment

- August 19, 2025 - Triton Digital launches enhanced podcast audience targeting tools drawing on Q2 2025 data, covering more than 40 demographic and purchase intent segments across 200 shows

- November/December 2025 - IAB Australia conducts the 10th-wave Audio Advertising State of the Nation survey, collecting 128 responses from buy-side professionals

- December 2025 - Global Podcast Advertising Compass 2025 reveals advertisers concentrate 43.5% of age-targeted impressions on the 25-34 demographic, neglecting high-value 55+ audiences

- January 2026 - AdsWizz research confirms 22-point gap between consumer audio engagement (31% of media time) and advertiser budget allocation (9%)

- January 21, 2026 - Acast and Barometer launch podcast industry's first pre-bid episode-level targeting integration, processing newly uploaded episodes against IAB categories in real time

- February 2026 - IAB Australia Audio Advertising State of the Nation Report Wave 10 is produced, covering calendar year 2025 expenditure data sourced from the IAB Australia Internet Advertising Revenue Report prepared by PwC

- March 2, 2026 - IAB Australia Internet Advertising Revenue Report for calendar year 2025 is released, confirming total audio at $339 million and the broader Australian market at $18.4 billion

- March 3, 2026 - IAB Australia publishes the Audio Advertising State of the Nation 2026 report on its website

Summary

Who - IAB Australia and its Audio Council, in collaboration with supporting organisations including Acast, ARN, Spotify, The Trade Desk, Magnite, Google, Foxtel, Nova Entertainment, GroupM, Publicis, WPP Media, Zenith, News Corp Australia, Nine, SCA, Triton Digital, Yahoo, and Earmax Media.

What - Publication of the tenth annual Audio Advertising State of the Nation report, a survey-based study of 128 Australian advertising buy-side professionals covering investment intentions, creative formats, programmatic buying behaviour, measurement tools and challenges, and AI adoption in digital audio advertising. The report confirms total Australian digital audio and podcast advertising reached $339 million in calendar year 2025, up 8.2%, and documents forward intentions showing 69% of respondents plan to increase original content podcast investment in 2026.

When - The survey was conducted in November and December 2025. The report was published on March 3, 2026. The underlying expenditure data covers calendar year 2025.

Where - Australia. The survey covers the Australian advertising buy-side. Expenditure data comes from the IAB Australia Internet Advertising Revenue Report for calendar year 2025, prepared by PwC. The report is produced under IAB Australia, the country's peak trade association for online advertising.

Why - The report exists to give the IAB Audio Council, advertisers, agencies, and platform operators a current picture of where audio advertising investment is heading and what is constraining growth. Ten years of longitudinal data allow year-on-year comparisons across investment plans, creative format adoption, programmatic behaviours, and measurement practices. The recurring finding that measurement fragmentation prevents confident planning and holds back budget allocation gives the report ongoing relevance as the industry seeks to convert audience engagement - now representing 47% of the Australian population aged 15 and older listening to podcasts monthly - into proportionate advertising investment.

Share this article

The link has been copied!