DoubleVerify study reveals advertisers face mounting brand suitability concerns

DoubleVerify surveyed 22,000 consumers and 1,970 marketers across 21 countries, finding 65% of advertisers express brand suitability concerns in walled gardens.

DoubleVerify surveyed 22,000 consumers and 1,970 marketers across 21 countries, finding 65% of advertisers express brand suitability concerns in walled gardens.

DoubleVerify released comprehensive research on November 18, 2025, examining how consumers and marketers interact with walled garden advertising environments. The ad verification company surveyed 22,000 consumers and 1,970 marketing decision-makers across 21 countries to assess platform behavior, influencer impact, and brand safety challenges within closed advertising ecosystems.

The research documented significant concerns among advertisers about content adjacency and brand suitability. Almost two-thirds of marketers who advertise on social media expressed concerns about brand suitability in these placements, according to the report. Larger companies show heightened worry about ad placement appropriateness within walled gardens.

Consumer attention patterns reveal generational divides in platform preferences and news consumption habits. YouTube captures 72% of consumer usage globally, followed by Facebook at 69%, Instagram at 54%, and TikTok at 45%. Platform preferences correlate strongly with demographic factors, with Facebook dominating among older and female users while younger cohorts favor video-first platforms.

Your go-to source for digital marketing news.

No spam. Unsubscribe anytime.

News consumption demonstrates stark age-based differences. Consumers aged 18–44 cited social media platforms and YouTube as their primary news sources, with over 40% of respondents in both the 18–24 and 25–34 age brackets identifying these channels as their top method for consuming news content. Traditional television news channels retain dominance among consumers aged 45 and older, with usage rising from 38% among 35–44 year-olds to 71% among those 65 and above.

Influencer marketing shows substantial purchase influence across consumer segments. The research found that 54% of consumers reported social media influencers impact their purchase decisions. Micro influencers with 1,000 to 100,000 followers generated the highest engagement rates, with 24% of consumers interacting with this category. Social commerce penetration reached 30% globally, with 30% of consumers making purchases directly through social platforms in the past year.

Regional variations in social commerce adoption reveal mobile-first markets driving higher penetration rates. Indonesia led adoption at 52%, followed by the Philippines at 50% and India at 49%. Markets with more established e-commerce infrastructure showed lower rates, with Japan at 8% and France at 9%.

Artificial intelligence-generated content proliferation emerged as a verification challenge. The study found that 57% of consumers said they have seen AI-generated content on social media, more than double the 26% who encountered such content in search results. This content authenticity issue compounds existing brand suitability concerns as distinguishing between human-created and AI-generated material becomes increasingly difficult.

Context and content adjacency significantly influence consumer brand perception. The research showed 64% of consumers say the genre of nearby content influences their perception of ads. Lifestyle content generated the most positive brand perception at 53%, while horror content produced the most negative impact at 23%. Reality television and gaming content also registered negative perceptions at 15% each.

Ad adjacency effects doubled negative perception rates compared to general platform suitability. While 16% of consumers considered social platforms generally unsuitable for brand advertising, this figure increased to 32% when consumers evaluated specific content with adjacent advertisements. This doubling effect underscores the importance of contextual placement beyond platform-level brand safety measures.

Marketer challenges center on audience reach limitations within algorithm-driven environments. The research identified audience reach as the biggest challenge for 46% of marketers advertising on social media. Platform algorithms increasingly personalize content visibility, restricting how widely advertisements are distributed even within targeted demographic segments. Keeping up with content trends ranked second at 38%, followed by return on ad spend calculation at 33%.

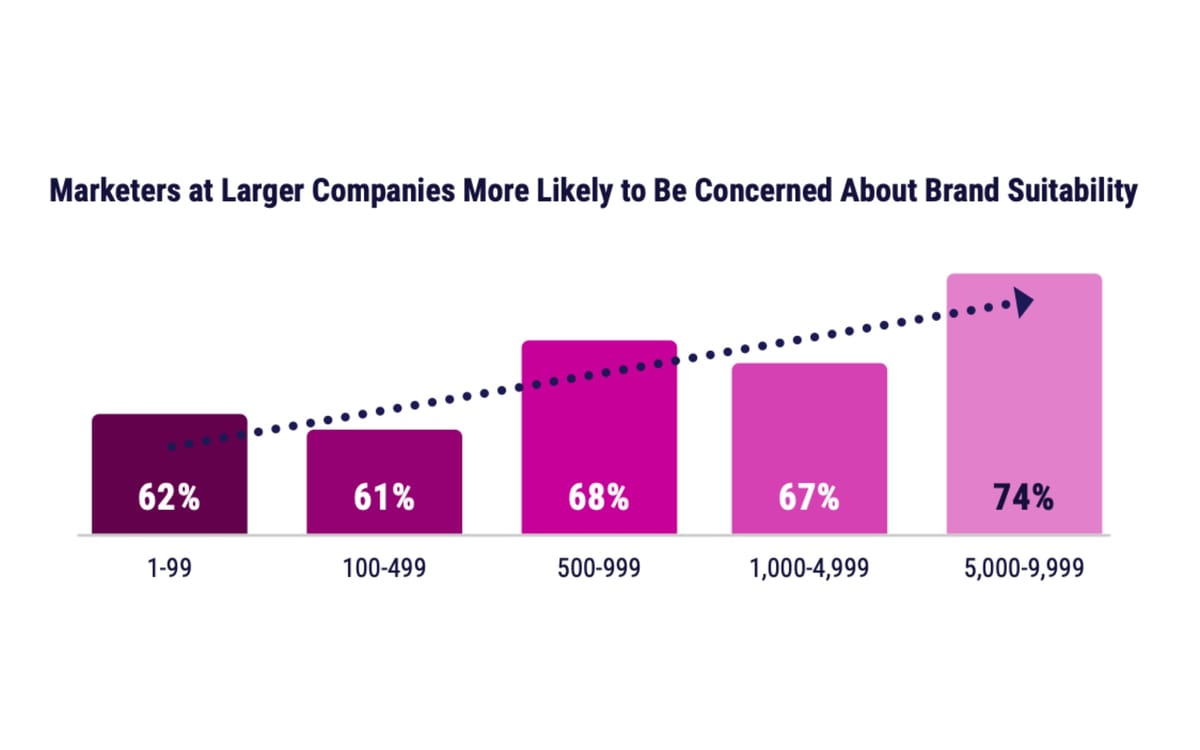

Brand suitability concerns intensified among larger organizations and regulated industries. Concerns regarding ad placement appropriateness increased proportionally with company size, rising from 62% among organizations with 1–99 employees to 74% among companies with 5,000–9,999 employees. Banking and finance along with healthcare and pharmaceutical sectors demonstrated heightened sensitivity to content adjacency issues.

Regional brand suitability concern levels varied substantially. Brazil registered the highest concern rate at 86%, followed by Japan at 78% and Canada at 79%. European markets showed more moderate concern levels, with DACH countries at 40% and France at 9%. These variations reflect different regulatory environments, cultural attitudes toward advertising standards, and market maturity levels.

Third-party verification tools gained importance as marketers seek transparency across closed platforms. The research found that 51% of marketers indicated audience targeting and verification are the most crucial third-party tools for enhancing media planning and buying. Media quality post-bid measurement followed at 48%, with content alignment pre-bid controls at 42%.

Marketer confidence in walled garden advertising increased despite persistent challenges. YouTube led confidence metrics at 72%, followed by Instagram at 71% and TikTok at 68%. Confidence levels varied by region, with APAC showing a 10 percentage point increase for YouTube compared to global averages, while North America demonstrated disproportionate confidence growth in LinkedIn.

Platform usage for different funnel stages revealed strategic segmentation patterns. Instagram, Facebook, YouTube, and TikTok primarily serve upper-funnel campaign objectives, with 48%, 44%, 50%, and 46% of usage respectively focused on awareness and consideration. Smaller platforms with lower consumer penetration rates like Zalo, Reddit, and Twitch saw higher allocation to mid- and lower-funnel objectives.

Facebook and Instagram commanded $192 billion in global advertising spend in 2025, according to the research. TikTok followed with $34 billion in global advertising expenditure. These figures represent the concentration of advertising investment within major walled garden environments.

Consumer leisure time allocation favors social media expansion. The study found that 28% of consumers expect to spend more time on social media platforms in the next year, compared to 22% planning to increase streaming user-generated content consumption and 15% expecting to watch more broadcast television.

Buy ads on PPC Land. PPC Land has standard and native ad formats via major DSPs and ad platforms like Google Ads. Via an auction CPM, you can reach industry professionals.

Mark Zagorski, CEO of DoubleVerify, emphasized the importance of transparency in walled garden advertising environments in the report's foreword. "The digital advertising ecosystem has never been more impactful — or more complex," Zagorski stated. "The brands that win will be those that bring discipline and clarity to every stage of the media journey: verifying the quality of their media; optimizing performance through data, AI and automation; and proving outcomes with independent, trusted measurement."

The research methodology employed online partner panels for data collection. Interviews were conducted by Sapio Research in March 2025 through email invitation and online survey. Consumer survey results carry a margin of error of plus or minus 0.7 percentage points at 95% confidence intervals. Marketer survey results carry a margin of error of plus or minus 2.2 percentage points at 95% confidence intervals.

Platform preference fragmentation across demographic segments necessitates multi-channel strategies for comprehensive audience reach. Facebook's user base skews older and more female, while younger demographics concentrate on visually-driven, video-first platforms. These preference patterns remain fluid among younger users, with emerging platforms potentially diverting attention from established social networks.

The research positioned walled gardens as offering scale and engagement through personalized algorithm-driven experiences. However, these opportunities introduce complexities including fragmentation, shifting audience behaviors, and tradeoffs between performance, protection, and efficiency. Missed audiences, wasted spend, and potential brand risk constitute the costs of inadequate measurement and verification.

Third-party verification priorities differed across geographic regions. EMEA and North America emphasized audience targeting and verification at 51% and 54% respectively, while LATAM and APAC prioritized media quality post-bid measurement at 51% and 57% respectively. These regional variations reflect different market maturity levels and regulatory frameworks.

Meta's advertising platform evolution continued throughout 2025 with enhanced AI optimization systems. The company reported that value optimization solutions delivered 29% higher return on ad spend compared to campaigns optimizing for conversion volume. This performance improvement accompanied broader industry movement toward automated advertising systems that reduce manual control in favor of algorithmic efficiency.

Pre-bid activation emerged as a recommended approach for avoiding unsuitable content in dynamic walled garden environments. The fast-changing nature of social media feeds requires real-time content evaluation before ad serving occurs. Brand safety measurement capabilities expanded across platforms throughout 2024 and 2025, with verification providers introducing content-level controls for Facebook, Instagram, Meta Threads, and other major social networks.

The shift toward AI-powered content creation tools raises authenticity questions for advertisers. Marketers concerned about brand suitability must now consider whether content adjacent to advertisements originated from human creators or AI generation systems. This verification layer adds complexity to existing brand safety frameworks developed for traditional user-generated content environments.

Consumer research behavior increasingly incorporates social media alongside traditional information sources. While online reviews at 45% and search engines at 41% remained the top pre-purchase research methods, social media ranked fifth at 27%, ahead of video reviews or tutorials at 26%. The algorithmic curation of social feeds surfaces relevant content tailored to individual interests, making platforms effective product discovery channels.

Google Analytics integration with Meta and TikTok cost data enables unified campaign analysis across competing advertising ecosystems. The October 2025 launch addressed persistent challenges in cross-platform measurement, automatically importing advertising expenses, clicks, and impressions from both platforms into Analytics properties.

Industry movement toward enhanced brand suitability controls accelerated in 2025. Google introduced brand suitability controls for Demand Gen campaigns in November, while Amazon DSP launched brand suitability settings in open beta the same month. These developments reflect broader recognition that advertiser demand for contextual relevance extends beyond basic brand safety protections.

The research concluded that sustainable performance in walled gardens depends on transparency and trust rather than scale alone. Marketers must balance the audience reach and engagement opportunities these platforms provide against the need for verification, measurement, and brand safety assurance. Third-party measurement tools offer consistent evaluation methods across proprietary platform metrics that vary in methodology and accessibility.

Subscribe PPC Land newsletter ✉️ for similar stories like this one

Subscribe PPC Land newsletter ✉️ for similar stories like this one

Who: DoubleVerify surveyed 22,000 consumers across 21 countries and 1,970 marketing and advertising decision-makers worldwide. The research examined how people engage with major social media platforms including YouTube, Facebook, Instagram, TikTok, and others.

What: The company released comprehensive research examining consumer behavior patterns, influencer impact on purchasing decisions, brand suitability concerns among marketers, and measurement challenges within walled garden advertising environments. Key findings included 65% of marketers expressing brand suitability concerns and 54% of consumers reporting influencer impact on purchase decisions.

When: DoubleVerify released the 2025 Global Insights Report on November 18, 2025. Sapio Research conducted the surveys in March 2025 through online partner panels using email invitation and web-based questionnaires.

Where: The research covered 21 countries across APAC (Australia, India, Indonesia, Japan, Philippines, Singapore, Thailand, Vietnam), EMEA (France, Germany, Italy, Netherlands, Saudi Arabia, Spain, UAE, UK), LATAM (Brazil, Colombia, Mexico), and North America (Canada, US). Findings apply to major walled garden platforms including Meta's Facebook and Instagram, Google's YouTube, TikTok, and other social networks.

Why: The research addresses the growing complexity marketers face in walled garden advertising environments where attention is fragmented across platforms, data is locked behind proprietary systems, and the path from investment to outcome has become difficult to measure. With Facebook and Instagram commanding $192 billion in global ad spend and TikTok generating $34 billion, understanding consumer behavior and marketer concerns within these environments has become essential for effective advertising strategy.