Marketers bet on AI media despite struggling with generative AI adoption

Mediaocean survey shows 54% of marketers increasing AI media spend while 42% struggle with data quality issues preventing broader AI implementation.

Mediaocean survey shows 54% of marketers increasing AI media spend while 42% struggle with data quality issues preventing broader AI implementation.

Marketers plan to increase advertising spend on AI platforms like ChatGPT and Google AI Overviews at higher rates than traditional search advertising, yet paradoxically struggle to implement generative AI tools within their own organizations. These contradictory findings emerged from Mediaocean's 2026 H1 Advertising Outlook Report, which surveyed 320 marketing professionals in November 2025 about their planned media investments and technology adoption for the first half of 2026.

According to the report, 54% of marketers plan to increase investment in AI media compared to 47% planning to boost search advertising spend. This marks the first time in the survey series that a nascent advertising channel has surpassed search in planned investment growth. The shift reflects growing marketer interest in advertising on conversational AI platforms, despite the fact that most of these platforms have not yet formally launched advertising products.

Mediaocean conducted this research through SurveyMonkey, gathering responses from marketers, agencies, media companies, measurement firms, and tech platforms. The company has published similar reports twice yearly since late 2021, compiling data from more than 6,100 respondents across nine survey waves. This particular survey reflects the ninth installment in the series, with data collection occurring during November 2025.

Digital video formats dominate marketer investment plans for the first half of 2026. Connected TV and digital display/video tied at 63% of respondents planning to increase spending in each channel. Social platforms followed closely at 61%, reinforcing the continued strength of video-driven ecosystems and creator-led content across the advertising landscape.

The budget momentum toward digital channels continues a multi-year pattern tracked in previous Mediaocean surveys. Connected TV advertising spend has grown substantially, with projections showing CTV's share of media budgets doubling from 14% in 2023 to 28% in 2025. The current survey data suggests this trajectory will continue through at least the first half of 2026.

Influencer and creator marketing claimed 53% of marketers planning increased investment, placing it ahead of search advertising and demonstrating the maturation of creator-led content as a core marketing channel rather than an experimental budget line. The growth in influencer spending aligns with broader shifts toward authentic, personality-driven content that resonates particularly strongly with younger demographics.

Retail media showed more modest growth expectations, with 40% planning to increase spend. However, the majority intend to maintain existing levels rather than decrease investment, reflecting retail media's durability in bottom-funnel performance and commerce-driven campaigns. Retail media networks have expanded rapidly across verticals, with recent industry projections showing the sector capturing approximately 20% of total global advertising revenue by 2030.

Traditional media faces continued pressure. Local TV, national TV, and print showed the sharpest planned decreases at 36%, 34%, and 49% respectively. Radio and out-of-home advertising also demonstrated elevated decrease rates compared to digital-only categories. These declines reflect ongoing budget migration toward channels offering greater precision, flexibility, and dynamic optimization capabilities.

The survey introduced cross-platform orchestration as a tracked capability for the first time, revealing it as a top priority alongside AI adoption. Both AI and cross-platform orchestration captured 39% of respondents identifying them as most critical advertising capabilities given current macroeconomic conditions.

This represents a significant shift in how marketers conceptualize their technology requirements. Rather than optimizing individual channels in isolation, marketing teams increasingly recognize the need for unified systems that connect insights, workflows, and activation across multiple environments. The rise of orchestration reflects what Mediaocean characterized as a movement beyond siloed point solutions toward systems that consistently apply decisions across CTV, social, display, retail media, and other channels.

Performance-driven paid media maintained the top position at 51%, followed by brand advertising and measurement and attribution capabilities, each at 48%. The persistence of these established priorities demonstrates that even as new capabilities emerge, fundamental advertising functions remain essential to marketing operations.

Privacy concerns showed significant movement, increasing 33% since May 2025 to reach 24% of respondents. This jump reflects mounting concern over signal loss, tightening regulation, and inconsistent data access across platforms. The operational consequences of identity deprecation have become more visible to marketers, driving demand for better compliance frameworks and governance structures.

Automation captured 30% of respondents, positioning it as an essential companion to AI adoption. As AI capabilities accelerate across advertising platforms, automation helps teams scale outputs, streamline workflows, and operate more efficiently with constrained resources.

First-party data mastery dropped significantly from previous waves, falling to just 19%. This decline suggests marketers have shifted focus from long-term infrastructure building to near-term performance needs. Creative testing and experimental budgets also saw meaningful pullbacks, indicating that experimentation is giving way to pragmatism as economic pressures mount.

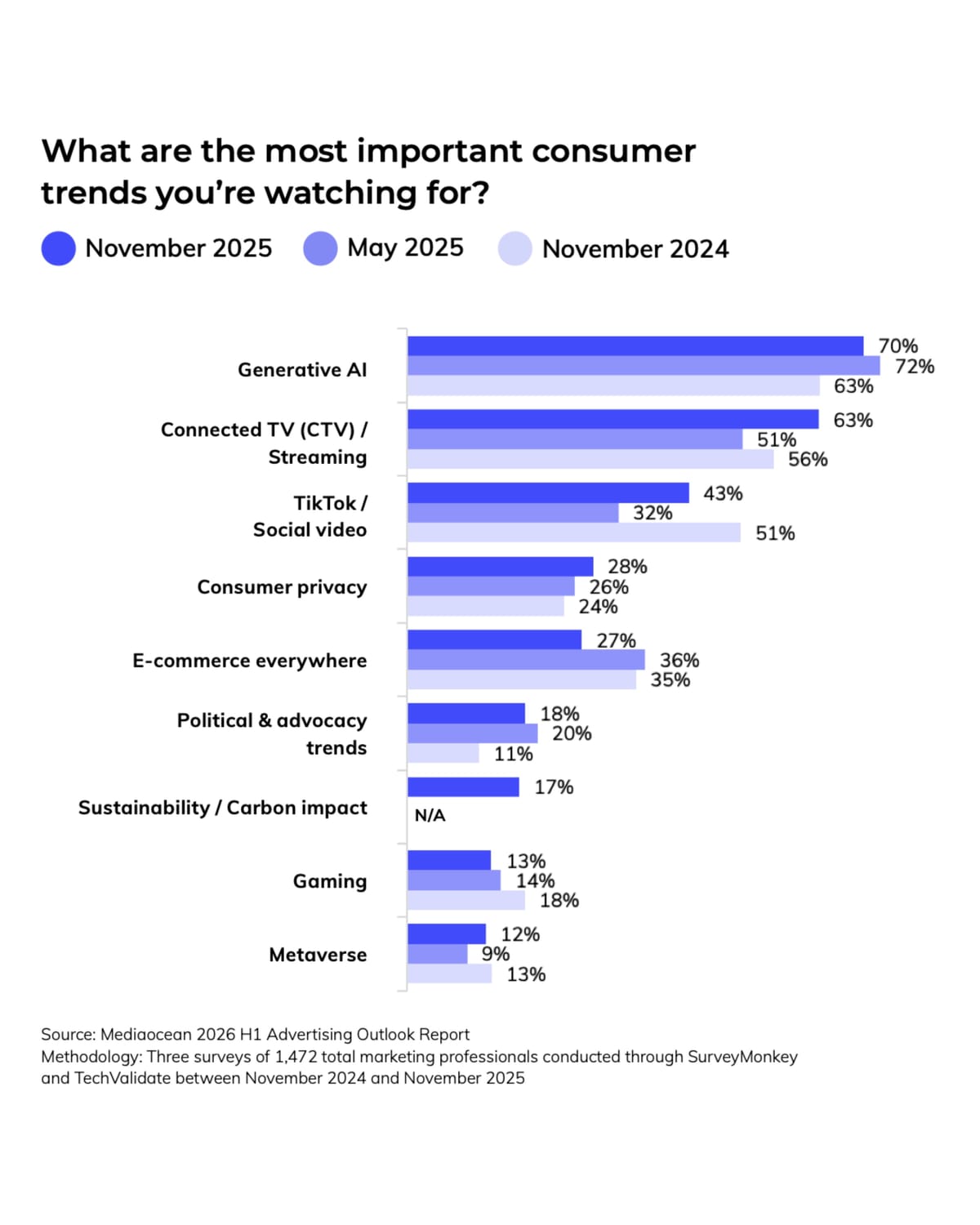

For the third consecutive survey, generative AI remained the most important consumer trend that marketers are monitoring. The technology captured 70% of respondents, though this represented a slight decline from the previous report. Despite the minor dip, generative AI continues to dominate marketer attention, reflecting the technology's expanding role in everyday consumer behavior from search and discovery to content creation and problem-solving.

Video-driven environments surged in perceived importance. Connected TV and streaming jumped sharply to 63%, representing a 24% increase from May 2025. This growth stems from ongoing shifts in viewing habits and the proliferation of premium, on-demand content options across streaming platforms.

TikTok and social video also saw significant gains, rising to 43% and marking one of the steepest increases across all tracked categories. Together, the gains in CTV and social video highlight a marketplace where short-form video, discovery algorithms, and streaming ecosystems increasingly shape culture and consumption patterns. Industry experts have noted persistent challenges in adapting creative assets across these platforms, with 72% of marketers reusing or slightly modifying assets rather than developing tailored creative for different environments.

Consumer privacy captured 28% of marketers monitoring this trend, while political and advocacy trends registered at 18%. Gaming maintained 13% attention, and the metaverse held at 12%, though none of these trends approached the dominance of AI or video ecosystems.

The report introduced sustainability and carbon impact of media and technology as a newly tracked trend, with 17% of marketers now monitoring the environmental footprint of digital advertising. The emergence of this category reflects growing expectations for transparency, responsibility, and environmentally conscious decision-making in media planning.

E-commerce everywhere declined to 27% after years of heightened pandemic-era relevance. As shopping behavior stabilizes, marketers appear to be reallocating attention toward emerging forces reshaping discovery, engagement, and conversion, namely AI and video-first platforms.

Marketers are gravitating toward AI applications that directly support insight generation and campaign performance. Data analysis and market research each captured 43% of respondents currently using generative AI for these purposes, reflecting AI's ability to simplify decision-making and process complex datasets.

Adoption is expanding into creative and activation-focused areas. Creative development reached 33% adoption, campaign optimization 31%, creative personalization 23%, and campaign orchestration 19%. This progression signals that AI has moved beyond back-end intelligence functions and increasingly shapes how concepts are built, iterated, and delivered across platforms.

More mature creative workflows showed broad but softening adoption. Copywriting maintained 29% usage while image generation held at 23%, suggesting teams are refining where AI provides the clearest performance improvements. Technical applications saw the steepest declines, with website development at just 6% and software coding at 8%. These drops indicate marketers are moving away from engineering-heavy AI uses and gravitating toward functions closer to creative acceleration and campaign performance.

Search engine optimization represented one of the weakest AI adoption areas at just 10%, despite SEO being a natural fit for AI-powered content optimization. The low adoption rate may reflect uncertainty about how AI-generated content impacts search rankings or concerns about quality and authenticity in SEO applications.

However, the barriers preventing broader AI adoption reveal significant systemic challenges. Data quality or access issues topped the constraint list at 42%, followed closely by difficulty connecting AI insights across multiple systems at 41%. Brand safety or compliance concerns captured 40%, while integration challenges with existing tech stacks reached 39%.

These four top barriers all map directly to areas where AI could deliver the greatest value if properly implemented. The finding creates a paradox where the obstacles slowing AI adoption are precisely the problems AI systems could potentially solve with proper infrastructure and data governance.

Ethical or governance concerns affected 36% of respondents, lack of internal expertise 31%, and cost or ROI uncertainty 27%. These constraints point to the need for clearer frameworks and organizational alignment as AI deployments scale across marketing functions.

Industry analysis examining AI implementation across advertising platforms has documented similar challenges, noting that while platforms have introduced agentic AI capabilities for autonomous campaign management, the promise of complete automation remains largely theoretical. Most implementations maintain approval workflows for brand-sensitive decisions rather than enabling wholesale automation across client portfolios.

Marketers identified fragmentation across platforms and publishers as their largest area of concern at 56%. This fragmentation makes it increasingly difficult to manage audiences, performance, and creative across an expanding omnichannel environment. The finding underscores how the proliferation of digital channels has created coordination challenges that manual processes cannot efficiently resolve.

The complexity of cross-channel measurement and optimization captured 49% of marketers as a major concern. As budgets shift toward CTV and AI-driven environments, the challenge extends beyond simply buying across channels to understanding how those channels interact. Consistent metrics, unified frequency management, and clear optimization loops remain elusive despite years of industry effort to standardize measurement approaches.

AI integration introduced substantial operational tension alongside its innovation potential. Three of the top five concerns related specifically to AI deployment: balancing AI adoption with brand safety, accuracy, and creative control at 43%; managing AI-driven automation without losing oversight at 42%; and uncertainty around AI governance and compliance at 38%.

These AI-related concerns sit at the intersection of data quality, platform control, interoperability, and organizational readiness. The findings strengthen the case for orchestration frameworks that can provide clearer governance and oversight as AI systems gain more autonomy in campaign management. Recent industry developments around agentic AI infrastructure reflect attempts to address these concerns through standardized protocols and unified management interfaces.

Despite the urgency around orchestration, most advertising technology stacks remain far from unified. Only 10% of marketers described their systems as fully unified across all channels. Nearly half (48%) characterized their environments as only partially unified with significant silos that limit data movement and insight sharing.

These infrastructure gaps contribute to numerous downstream challenges including inconsistent measurement, creative redundancy, and inefficiency in campaign pacing and optimization. The fragmentation affects basic operations like budget allocation, frequency capping, and attribution modeling across different platforms.

Yet conviction around orchestration's importance remains unmistakable. A combined 86% of marketers stated that cross-channel orchestration is important, with more than half (53%) calling it extremely important. The disconnect between aspiration and current infrastructure reality highlights what Mediaocean termed a critical turning point for the advertising industry.

The measurement infrastructure supporting orchestration has evolved substantially over the past year, with multiple platforms introducing unified measurement capabilities that enable media mix modeling and incrementality analysis directly within secure data environments. However, adoption of these advanced measurement approaches remains limited by the same data quality and integration challenges that constrain AI implementations.

The survey results arrive amid significant platform developments around AI advertising formats. Google expanded ads in AI Overviews to 11 additional countries in December 2025, while OpenAI moved closer to monetizing ChatGPT through advertising, with internal discussions centering on sponsored content appearing within AI responses.

The marketer interest in AI media captured by the Mediaocean survey predates formal advertising product launches from most conversational AI platforms. This suggests advertisers are positioning themselves early for a category they believe will become significant, even though the specific advertising formats and targeting capabilities remain largely undefined.

Search advertising's relatively lower planned growth at 47% does not indicate declining importance but rather reflects its maturity as a channel. Search maintains resilience as a performance marketing staple, though its momentum trails newer digital formats that offer novel audience access and engagement models.

The emergence of AI media as a spending priority reflects what industry analysts have characterized as fundamental shifts in how consumers discover information and interact with digital content. However, significant questions remain about measurement standards, attribution methodologies, and effectiveness metrics for conversational AI advertising environments.

The survey findings reveal marketing organizations entering 2026 with heightened confidence about digital channel effectiveness but facing substantial operational challenges in technology implementation. The gap between AI media spending plans and generative AI adoption rates within marketing functions suggests marketers believe in AI's consumer-facing potential more strongly than they trust their organizations' ability to deploy AI tools internally.

Debra Aho Williamson, founder and chief analyst at Sonata Insights and author of the report's foreword, characterized 2026 as a year defined by tension between maturity and disruption. Advertisers demonstrate maturity in their approach to digital channel investment and decision-making discipline, recognizing that both brand advertising and performance marketing remain necessary. Yet AI integration creates significant disruption, with marketers eager to invest in AI platforms while struggling to implement generative AI within their own operations.

The orchestration challenge represents what Mediaocean termed an organizational and operational mindset shift beyond technical solutions. Achieving unified campaign management requires better data flows, clearer system design, stronger controls, and shared operational standards that bring intelligence and activation into alignment.

Success in 2026 will likely favor marketing organizations that can address foundational infrastructure challenges around data quality, system integration, and governance frameworks. These capabilities enable both effective AI deployment internally and intelligent participation in emerging AI media channels externally. Organizations that treat orchestration as a strategic priority rather than a technical project may gain competitive advantages as media environments become more fragmented and autonomous systems gain more operational control.

The survey methodology involved 320 marketing professionals surveyed through SurveyMonkey in November 2025. Respondents included marketers and agencies as primary cohorts, with additional representation from media companies, measurement firms, tech platforms, and other industry participants. This marks the ninth survey in Mediaocean's series, with the first published at the end of 2021 and more than 6,100 total respondents contributing data across all waves.

Who: Mediaocean surveyed 320 marketing professionals including marketers, agencies, media companies, measurement firms, and technology platforms through SurveyMonkey in November 2025.

What: The 2026 H1 Advertising Outlook Report reveals marketers plan to increase AI media spending (54%) at higher rates than search advertising (47%), while 63% plan to boost CTV and digital display investment. However, 42% cite data quality issues preventing broader AI implementation, and only 10% report fully unified advertising technology systems despite 86% identifying orchestration as important.

When: Survey data was collected in November 2025, with the report published in January 2026 covering marketer plans and priorities for the first half of 2026. This represents the ninth survey in Mediaocean's series begun at the end of 2021.

Where: The research covers global marketing professionals managing advertising investments across digital channels including connected TV, social platforms, search, display, AI media platforms, retail media, and traditional media formats. Findings reflect investment priorities across both domestic and international markets.

Why: The research matters because it documents a fundamental shift where marketers demonstrate greater confidence in AI as a consumer-facing advertising channel than in their organizations' ability to implement AI tools internally. The findings expose critical infrastructure gaps around data quality, system integration, and cross-platform orchestration that prevent marketers from fully capitalizing on AI capabilities, despite widespread recognition of these technologies' importance for future competitive advantage.