Netflix ad revenue reaches $11.5B in Q3 despite margin challenges

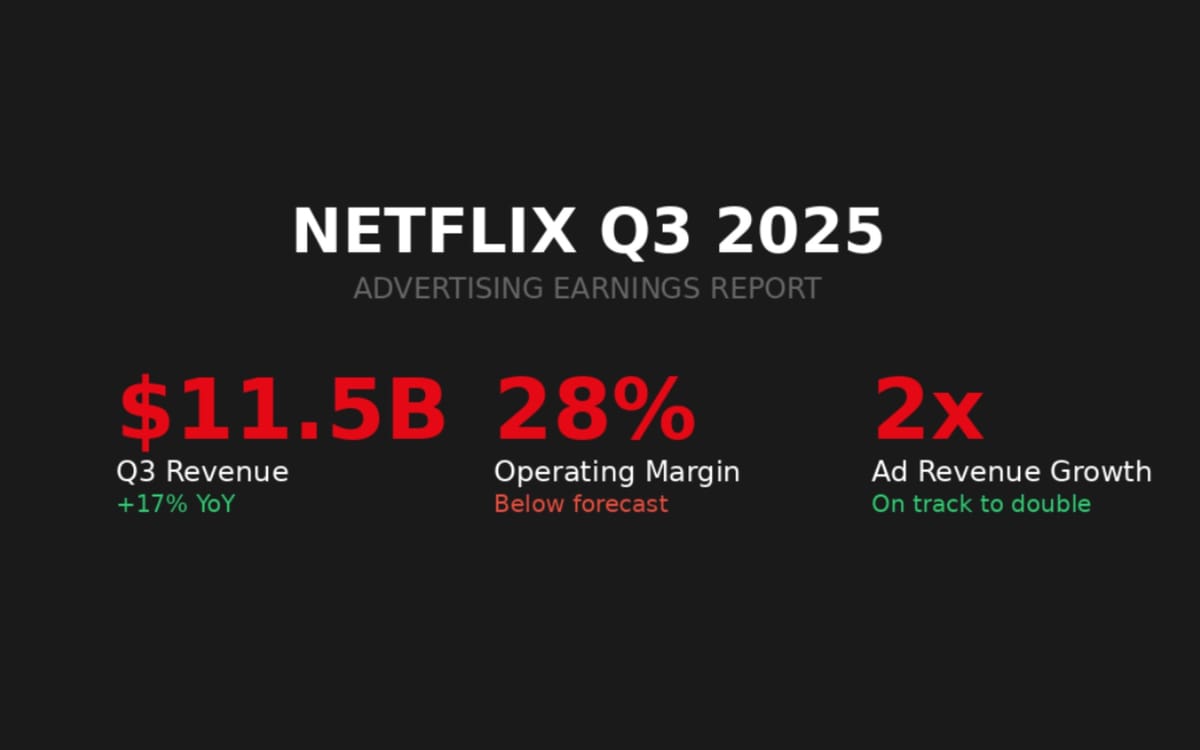

Netflix reported $11.51B revenue for Q3 2025 with advertising business on track to double annually, though Brazilian tax dispute reduced operating margin to 28% from expected 31.5%.

Netflix reported $11.51B revenue for Q3 2025 with advertising business on track to double annually, though Brazilian tax dispute reduced operating margin to 28% from expected 31.5%.

Netflix disclosed financial results for Q3 2025 on October 21, showing revenue reached $11.51 billion, representing 17% growth compared to the same period last year. The streaming platform reported its advertising business recorded the strongest quarterly sales performance in company history, positioning the division to more than double revenue throughout 2025.

The operating margin for the quarter measured 28%, falling below the company's 31.5% forecast. Spencer Neumann, Chief Financial Officer, attributed the variance to an unexpected $619 million expense related to Brazilian tax authorities. The expense covered periods spanning 2022 through Q3 2025 and involved disputes over the Contribution for Intervention in Economic Domain, a 10% tax on certain payments made by Brazilian entities to companies outside Brazil.

"It's not an income tax. It's a cost of doing business in Brazil," Neumann stated during the earnings call. The Brazil Supreme Court reached a 7-4 decision in August 2025 against an unrelated company, ruling the tax applies to service payments that don't involve technology transfer. This ruling prompted Netflix to reevaluate its position and record the expense in cost of revenues.

Approximately 20% of the Brazilian tax expense relates to 2025, with the remaining 80% covering 2022-2024. Neumann emphasized the company doesn't expect this matter to materially impact future results. Without this expense, Netflix would have exceeded its Q3 operating margin forecast.

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Gregory Peters, Co-CEO and President, confirmed Netflix recorded its best advertising sales quarter in company history. The streaming platform more than doubled upfront commitments in the United States compared to the previous year. These commitments will contribute to revenue partly in 2025 and partly in 2026.

"We've got a highly attentive and engaged audience," Peters explained when discussing advertiser enthusiasm. The company achieved record TV view share in Q3 2025 in both the United States and United Kingdom. Netflix captured 8.6% of total TV time in the US and 9.4% in the UK, according to Nielsen and Barb data respectively.

The Netflix Ads Suite rollout across all advertising markets enabled the company to iterate quickly based on client feedback. Peters highlighted that programmatic advertising experienced even higher growth rates than upfront sales. Programmatic represents an increasingly important component of incremental revenue contribution going forward.

Advertising technology expert Karsten Weide noted on social media October 22 that Netflix's ad business growth appears solid despite stock market reactions. "To be sure, it's not Netflix' ad business' fault - up 17% to $11.5B in Q3," Weide posted. He compared Netflix's Q2 2025 advertising revenue against competitors: Google generated $71 billion, Meta reached $47 billion, and Amazon Ads totaled $16 billion.

Weide identified persistent challenges facing Netflix's advertising division. "Limited inventory due to only a minority of subscribers signed up to the ad-supported plan, which restricts available impressions and makes narrow targeting difficult," he wrote. High CPMs and steep minimum spends create barriers for smaller advertisers attempting to access the platform.

Buy ads on PPC Land. PPC Land has standard and native ad formats via major DSPs and ad platforms like Google Ads. Via an auction CPM, you can reach industry professionals.

Total view hours grew faster in Q3 2025 compared to the first half of 2025. The quarter saw several breakout hits across multiple content categories. Wednesday Season 2 accumulated 114 million views, while Happy Gilmore 2 starring Adam Sandler reached 126 million views and set a Nielsen streaming record with 2.9 billion viewing minutes during its opening weekend.

Theodore Sarandos, Co-CEO and President, emphasized the company's massive opportunity for growth. "We're only about 7% of the addressable market, in terms of consumer spending and only about 10% of time spent on TV in our biggest market," Sarandos stated.

KPop Demon Hunters became Netflix's most popular film ever with 325 million views. The animated feature generated over 950 million owned impressions across Netflix's social channels. HUNTR/X became the first K-pop girl group to reach number one on Billboard's Hot 100, and characters from the film ranked as the top five most-searched Halloween costumes.

Netflix announced October 21 that Mattel and Hasbro each secured positions as global co-master toy licensees for KPop Demon Hunters. This unprecedented partnership between the two toy manufacturers reflects massive fan demand for merchandise inspired by the film. The company continues releasing apparel through the Netflix Shop and retail partners including Amazon, Zara, Target, Gap, Old Navy, and Hot Topic.

International content contributed significantly to Q3 performance. Bon Appétit, Your Majesty from South Korea attracted 32 million views. Hostage from the UK reached 35 million views, while Billionaires' Bunker from Spain garnered 22 million views. Argentina's In the Mud accumulated 15 million views, and India's The Ba**ds of Bollywood* reached 9 million views.

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

The Canelo versus Crawford boxing match attracted more than 41 million viewers, making it the most-viewed men's championship boxing match this century. The event reached number one on Netflix in 30 countries and appeared in the top 10 in 91 countries. Canelo/Crawford trended number one on X in the United States and appeared in trending lists across 21 additional countries.

"We believe these big events that attract mass audiences are kind of differentially valuable for our members," Sarandos explained. Live events represent a small portion of Netflix's content spending and account for minimal viewing within the platform's 200 billion annual hours viewed, yet they generate outsized positive impacts on conversation and acquisition.

Peters noted the company continues developing live capabilities beyond the United States. The World Baseball Classic from Japan represents an example of international live event expansion planned for 2026.

Netflix scheduled several major live events for Q4 2025 and beyond. The NFL Christmas Gameday doubleheader features Dallas Cowboys versus Washington Commanders and Detroit Lions versus Minnesota Vikings. Jake Paul fights Gervonta "Tank" Davis on November 14. Future events include WWE programming every week, the SAG awards, and FIFA's Women's World Cup in 2027 and 2031.

Netflix deployed its proprietary ad technology stack, the Netflix Ads Suite, across all 12 advertising markets during Q3. The platform supports more formats, enhanced measurement capabilities, and additional buying methods compared to previous infrastructure.

Peters outlined Q4 priorities including ad interactivity features launching later in the quarter. Looking toward 2026, the company plans to develop more buying methods, expanded data for targeting and media planning capabilities globally, additional modular interactive ad formats with enhanced AI capabilities, and increased measurement functionality across all markets.

"In 2027, we get to pivot to make more focused investments in data capabilities such as ML-based optimization, advanced measurement, advanced targeting," Peters stated. Netflix expects to move more quickly than competing streamers by leveraging pre-existing technology and data science assets.

The company recently integrated Amazon's DSP globally and AJA's DSP in Japan into its programmatic offering, with availability beginning in Q4 2025. This follows earlier programmatic partnerships established with The Trade Desk, Google Display and Video 360, Yahoo DSP, and Microsoft.

Fill rates have improved as the company develops go-to-market capabilities, measurement tools, and targeting options. Peters emphasized that overall revenue represents the most important metric the company seeks to optimize rather than focusing exclusively on fill rates.

Netflix forecast Q4 2025 revenue of $11.96 billion, representing 17% reported growth or 16% on a foreign exchange neutral basis. The company projects Q4 operating margin of 23.9%, marking a two percentage point year-over-year improvement.

For full year 2025, Netflix expects $45.1 billion in revenue, representing 16% growth on a reported basis and 17% on a foreign exchange neutral basis. The company now forecasts a 2025 operating margin of 29% both on a reported basis and based on foreign exchange rates as of January 1, 2025. The outlook decreased from prior expectations for 30% reported operating margin due to the Brazilian tax matter impact.

UCAN region revenue reached $5.07 billion in Q3, growing 17% year-over-year. EMEA generated $3.70 billion, increasing 18% compared to Q3 2024. LATAM revenue totaled $1.37 billion, up 10% year-over-year and 20% on a foreign exchange neutral basis. APAC produced $1.37 billion in revenue, growing 21% on a reported basis and 20% on a foreign exchange neutral basis.

Free cash flow totaled $2.66 billion for Q3 2025 compared to $2.19 billion in Q3 2024. Netflix now expects 2025 free cash flow of approximately $9 billion, plus or minus a few hundred million dollars, up from prior forecast of $8-8.5 billion. This revised forecast reflects timing of cash payments and lower content spend.

Netflix announced a video co-exclusive partnership with Spotify in Q3, securing a curated selection of top podcasts for the platform. The initiative provides entertainment options spanning pop culture, lifestyle, sports, and true crime content. Peters described the partnership as an opportunity to integrate high-quality video content that broadens Netflix's offering beyond films, series, live events, stand-up specials, and games.

The company rolled out party games playable on television with phones serving as game controllers. Titles include Boggle Party, Pictionary: Game Night, LEGO Party!, Tetris Time Warp, and Party Crashers. These games represent Netflix's broader focus on interactivity as complementary to linear storytelling.

Real-time voting represents the company's first live interactive feature, currently testing on Dinner Time Live with David Chang. The capability will roll out more broadly starting with Star Search in January 2026. Netflix expects to provide additional interactive features to deepen engagement with live events in the future.

Peters outlined the company's games strategy focusing on immersive narrative games based on Netflix IP, games for kids with no ads or in-app payments, mainstream established titles, and socially engaging party games. Examples include Squid Game: Unleashed, Thronglets from the Black Mirror universe, Golf with Happy Gilmore, Grand Theft Auto, and Peppa Pig.

Netflix leverages Generative AI to enhance member experience, empower creators, and improve advertising effectiveness. The company beta tests a conversational search experience allowing members to use natural language for content discovery. GenAI tools help localize promotional assets in multiple languages so titles can more easily reach global audiences.

Filmmakers used GenAI coupled with ML and Eyeline's proprietary volumetric capture technologies to de-age characters during the opening flashback scene in Happy Gilmore 2. Producers of Billionaires' Bunker used various GenAI tools during pre-production for pre-visualization to explore wardrobe and set designs.

In advertising, Netflix uses AI to test new ad formats, generate relevant ad creative and placement for members, and enable faster development of media plans. Peters stated that with these advancements, the company expects to test, iterate, and innovate on dozens of ad formats by 2026.

The company released production guidance for creators to use new technologies responsibly. Sarandos emphasized that "it takes a great artist to make something great" and AI primarily serves as a tool for creative enhancement rather than replacement.

Sarandos addressed potential industry consolidation following merger announcements from competitors. Netflix maintains a "builders not buyers" approach while evaluating significant M&A opportunities through a clear framework. The company assesses whether acquisitions represent big opportunities, whether IP strengthens entertainment offerings, if ownership provides additional value, and whether transactions strengthen existing capabilities or accelerate strategy.

"We have no interest in owning legacy media networks, so there's no change there," Sarandos confirmed. The company remains predominantly focused on organic growth, aggressive investment into business expansion, and returning excess cash flow to shareholders through share repurchases.

Peters noted that industry consolidation doesn't fundamentally shift the competitive landscape. "The range of activities that we and our competitors have to get great at has never been assembled in a single company before," Peters stated. He emphasized that developing necessary capabilities requires hard work in the trenches day to day rather than simply acquiring another company also developing those same capabilities.

Netflix faces competition from streaming services, linear TV, social media, video gaming, theatrical movies, and all leisure time options consumers possess. The company competes by focusing on a few key areas and delivering continuous improvement. Peters highlighted that combining great technology, product development, and content from around the world represents a complex challenge requiring sharp focus and bold creative choices.

Third-party content licensing remains available to Netflix despite potential consolidation among competitors. Sarandos noted that Netflix proved time and again that licensing to the platform represents the best method to build audience, generate revenue, and create value for intellectual property. Examples include Suits, Peaky Blinders, and Breaking Badwhere Netflix played positive roles in the lifecycle of other companies' IP.

During the October 21 earnings interview, executives addressed analyst questions about business health, advertising progress, content strategy, and financial outlook. Spencer Wang served as Vice President of Finance, Corporate Development and Investor Relations for the call.

Regarding 2026 financial guidance, Neumann stated the company will issue full year 2026 revenue and operating income guidance on the January 2025 earnings call. Financial objectives remain unchanged: sustain healthy revenue growth, expand margins, and increase free cash flow.

Netflix repurchased 1.5 million shares for $1.9 billion during Q3 2025, leaving $10.1 billion remaining under the existing share repurchase authorization. The company ended the quarter with gross debt of $14.5 billion and cash and cash equivalents of $9.3 billion.

Diluted earnings per share reached $5.87 compared to $5.40 in Q3 2024, representing 9% year-over-year growth. The result fell $1.00 below forecast due to lower than forecasted operating income stemming from the Brazilian tax expense.

Total streaming content obligations totaled $20.9 billion as of September 30, 2025, down from $23.2 billion at December 31, 2024. These obligations comprise content liabilities on the balance sheet plus obligations not yet meeting recognition criteria.

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Subscribe PPC Land newsletter ✉️ for similar stories like this one. Receive the news every day in your inbox. Free of ads. 10 USD per year.

Who: Netflix executives including Co-CEOs Gregory Peters and Theodore Sarandos, CFO Spencer Neumann, and VP of Finance Spencer Wang announced quarterly results. Advertising technology expert Karsten Weide provided industry analysis.

What: Netflix reported Q3 2025 revenue of $11.51 billion with 17% year-over-year growth. The advertising business recorded its strongest quarter and remains on track to more than double annual revenue. Operating margin reached 28%, below 31.5% forecast due to a $619 million Brazilian tax expense. The company achieved record TV view share in the US and UK while deploying its proprietary Netflix Ads Suite across all advertising markets.

When: Netflix released Q3 2025 financial results and held its earnings interview on October 21, 2025. The quarter covered July 1 through September 30, 2025.

Where: Results reflect Netflix's global operations across more than 190 countries. The company operates advertising-supported streaming in 12 markets including the United States, United Kingdom, Germany, France, Japan, and Brazil. Regional revenue performance varied with UCAN generating $5.07B, EMEA producing $3.70B, LATAM reaching $1.37B, and APAC totaling $1.37B.

Why: The advertising business matters to the marketing community because Netflix achieved unprecedented scale as a premium video advertising platform. The completion of the Netflix Ads Suite deployment enables sophisticated targeting, measurement, and buying capabilities that compete with established digital advertising platforms. Record engagement metrics, including 8.6% US TV share and 9.4% UK TV share, demonstrate Netflix captured significant audience attention during Q3. The more than doubling of upfront commitments signals advertiser confidence in the platform's ability to deliver results. However, challenges persist including limited inventory due to minority ad-supported subscriber penetration, high CPMs, and steep minimum spend requirements that restrict smaller advertiser access. These dynamics create opportunities for agencies and brands with sufficient budgets while highlighting the platform's premium positioning in the streaming advertising landscape.