Two-thirds of marketers brace for AI to upend consumer behavior

Boston Consulting Group and Moloco survey 238 marketing leaders revealing 67% expect major AI disruption to consumer journeys as traditional search declines.

Boston Consulting Group and Moloco survey 238 marketing leaders revealing 67% expect major AI disruption to consumer journeys as traditional search declines.

Boston Consulting Group and Moloco today unveiled the Consumer AI Disruption Index, a comprehensive analysis revealing that 67 percent of senior marketing leaders expect high levels of artificial intelligence-driven disruption to consumer behavior. The research, released January 21, 2026, combines survey data from 238 marketing executives across five global regions with performance metrics from more than 3,200 mobile applications representing over 200 billion downloads.

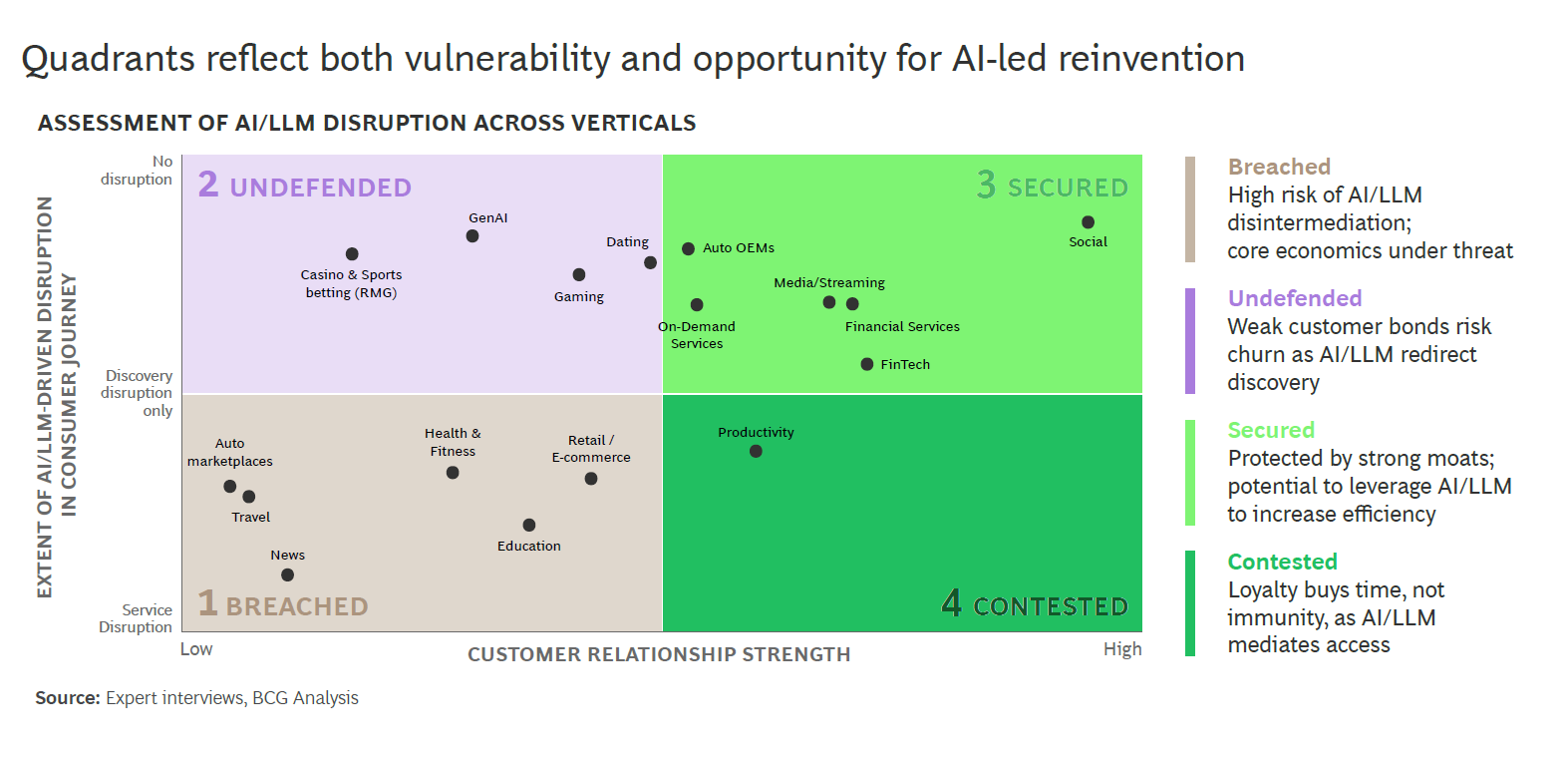

The study maps 17 consumer-facing industry verticals along two critical dimensions: vulnerability to AI-driven disintermediation and strength of customer relationships. News, travel, auto marketplaces, and retail face the highest disruption risk, while automotive original equipment manufacturers, fintech, financial services, media streaming, and social platforms demonstrate the lowest vulnerability, according to the joint research.

"AI is fundamentally reshaping how consumers interact with brands," said Giorgo Paizanis, a BCG partner and co-author of the report published in "Battle for the Interface: Introducing the Consumer AI Disruption Index." The research indicates marketers must build defensibility on three fronts: discovery, service, and customer relationships to convert disruption into competitive advantage.

The Consumer AI Disruption Index quantifies disruption risk across ten marketing channels, finding that paid search, organic search, programmatic display, and affiliate channels face significant AI-driven transformation. A 2024 Seer study cited in the report showed paid and organic click-through rates decreased by 50 percent and 70 percent respectively when AI snippets appeared in search results.

Traditional search engines face stagnating or declining traffic patterns as closed-loop ecosystems like in-app environments become critical for sustained brand visibility, according to the BCG and Moloco analysis. The shift represents what Paul D'Arcy, Moloco chief marketing officer and co-author, characterized as a behavioral transformation from "the world of search to the world of answers."

Channels with direct engagement and access to first-party data—including organic direct traffic, e-commerce and retail media, email and CRM, and in-app marketing—demonstrate stronger positioning as AI enhances personalization and closed-loop performance. Bernstein estimates cited in the report indicate that AI shopping agents have improved conversion rates by 30 percent compared to conventional methods, driving increased prioritization of retail media networks by global marketers.

The research arrives as the advertising industry confronts multiple simultaneous disruptions. Google's December 2025 core algorithm update devastated Discover traffic for news publishers, with some experiencing 70-85 percent declines during the crucial holiday advertising season. Meanwhile, platforms have accelerated AI agent deployment, with Amazon, Google, and IAB Tech Lab introducing autonomous campaign management tools throughout late 2025.

Search-heavy sectors including news, health and fitness, and on-demand services face greater discovery risk, while verticals with strong in-app marketing capabilities like productivity software, financial services, and dating platforms demonstrate lower disruption exposure, the index reveals. The research evaluated discovery disruption by analyzing each vertical's digital channel mix across paid search, organic search and social, display advertising, affiliates, social media, video platforms, organic direct traffic, e-commerce and retail media, email and CRM, and in-app marketing.

Consumer software, financial services, and fintech derive more than 60 percent of traffic from organic direct and in-app marketing channels. Travel and news verticals, in contrast, depend heavily on paid and organic search, making them particularly vulnerable as AI platforms compress discovery and comparison workflows.

Service disruption risk depends on three factors: technical ability to replicate workflows, data accessibility, and regulatory barriers. News, travel, education, productivity software, retail, and auto marketplaces face high service disruption as AI demonstrates proven capability to replicate key workflows in those verticals.

AI agents can easily replicate aggregation and summarization workflows for news publishers, the research found. Pure-play news and review platforms face especially high vulnerability. Travel experiences high disruption risk for pure aggregator and agentic models handling itinerary planning and price comparisons, though players controlling customer service layers and exclusive listings maintain stronger defensive positions.

Productivity software confronts a nuanced situation. Niche productivity applications face disruption risk as workflows prove easy for large language models to integrate. In contrast, entrenched platforms like Microsoft Word, Excel, and Google Sheets occupy stronger positions. The research notes that gaming, dating, and generative AI verticals face moderate disruption but weak brand ties, requiring strategies to convert transactional relationships into durable loyalty through personalization and AI partnerships.

The index assessed customer relationship strength through three quantitative metrics: acquisition strength measured by the proportion of organic versus paid traffic, sustained loyalty calculated through Day 30 versus Day 7 retention ratios, and platform engagement depth determined by time spent on brand applications versus websites.

Social platforms, fintech, and financial services demonstrated the highest performance in customer relationship strength across at least two of three metrics. Social platforms achieved a composite score of 9.6 out of 10, driven by strong unpaid traffic shares at 77 percent, exceptional Day 30 to Day 7 retention ratios at 86 percent, and near-complete app engagement at 99 percent.

Travel and auto marketplaces performed poorly across all three relationship metrics. The travel vertical scored 5.4 out of 10 on customer relationship strength, with 58 percent unpaid traffic, 50 percent Day 30 to Day 7 retention, and just 25 percent app engagement. Auto marketplaces achieved a 5.3 composite score with similarly weak metrics across acquisition, loyalty, and engagement dimensions.

The research identifies four distinct archetypes based on plotting AI-driven disruption against customer relationship strength. "Breached" verticals including travel, retail, and news face high disruption risk with weak customer bonds. Their survival depends on strengthening relationships and embedding AI within their own platforms.

"Undefended" verticals such as gaming, dating, and casino and sports betting face moderate disruption with weak brand ties. These sectors must convert transactional relationships into durable loyalty. "Secured" verticals including fintech, financial services, and media streaming face the lowest risk, with inherent trust and regulatory moats enabling them to use AI for efficiency gains.

"Contested" verticals like productivity software combine strong customer equity with service disruption exposure, positioning them to define how AI integrates into their sectors. The Consumer AI Disruption Index builds on accumulating evidence of AI's impact on consumer behavior. Ahrefs research published in June 2025 found that while AI search traffic accounted for just 0.5 percent of website visits, these visitors generated 12.1 percent of signups—a conversion rate 23 times higher than traditional organic search traffic.

The BCG and Moloco survey of 238 senior marketing leaders across 17 verticals revealed that 77 percent prioritize first-party data capture, 72 percent emphasize AI-driven ad formats, and 67 percent focus on building in-house AI capabilities. Only 52 percent identified rebalancing brand versus performance mix as a priority response to AI-driven discovery changes.

Travel, education, and retail verticals lead in first-party data capture prioritization, while traditional finance and productivity sectors emphasize AI-driven advertising formats. The survey findings suggest significant variation in strategic responses across industries facing different levels of AI disruption.

Forty-five percent of consumers feel comfortable letting AI make purchases on their behalf, signaling the emergence of agentic commerce, according to the research. This behavioral shift fundamentally rewires digital discovery as traditional open-web channels including organic search, paid search, and programmatic display face stagnating or declining traffic.

The timing of the Consumer AI Disruption Index release coincides with intensifying debate over AI's impact on digital advertising. Industry veteran Andy Batkin challenged the Interactive Advertising Bureau on January 15 over its 2026 Annual Leadership Meeting agenda, arguing the organization abandoned publishers during an existential revenue crisis. The IAB's February 1-3 conference features zero sessions dedicated to generating new publisher revenue, according to Batkin's critique.

The research arrives as traditional search traffic to news publishers declined from 51 percent to 27 percent between 2023 and 2025, while Google Discover feed traffic climbed to 68 percent. Publishers face mounting pressure as AI platforms capture discovery while traditional advertising models face structural challenges.

The report outlines specific actions marketers should prioritize to counter discovery disruption, service disruption, and strengthen customer relationships. To reclaim discovery, brands should adopt Answer Engine Optimization through on-site optimization, off-site strategies, and ecosystem integrations ensuring visibility in AI-generated responses.

Credit Karma updated its website with question-and-answer-style content easily indexed to improve visibility in large language model queries, the report notes. The RealReal invested in Answer Engine Optimization tools tracking which queries surface their brand versus competitors. Skyscanner focuses on live pricing feeds and stricter inventory syncing to meet requirements for AI overviews.

Diversifying channel investment represents a second critical strategy. Brands should shift spending from declining channels toward video, social, influencer, and in-app advertising where consumer attention now concentrates. A leading music streaming platform is reallocating budget from search into out-of-home and social channels as Generation Z adopts new discovery methods, according to examples in the research.

Increasing first-party data collection through logins, structured onboarding, and progressive profiling enables personalized experiences while reducing dependence on external platforms. Coursera builds profiles gradually as users explore courses, while The RealReal requires login even before accessing listings, ensuring every interaction generates first-party data.

To counter service disruption, brands must decide whether to embed large language model functionality into owned channels, strategically interact with LLMs by opening or closing platforms, or directly integrate into AI assistants through application programming interfaces. Notion launched features allowing users to create custom agents completing tasks and acting autonomously. Flo built "Ask Flo," an in-app AI assistant for women's health trained on proprietary medical datasets reviewed by doctors.

Amazon closed its listings from LLM crawlers, limiting discovery to category-level searches while embedding AI functionality in its own channels. Etsy chose the opposite approach, integrating with ChatGPT to allow direct access to product listings including add-to-cart options. Canva embedded design tools directly into ChatGPT via the GPT App SDK, while Shopify integrated products and checkout services into ChatGPT for seamless in-chat purchases.

Improving customer relationships requires combat AI's disruption with differentiation through proprietary data, certified outcomes, or human expertise that AI cannot replicate. L'Oréal expanded dermatologist-led skin assessments and certified in-store diagnostics to complement AI-driven recommendations. Coursera added AI-powered features to safeguard assessments against integrity threats through plagiarism detection and proctoring.

Network building embeds products in communities and social graphs to create switching costs. Bumble expanded "Bumble For Friends" through acquiring Geneva, a Generation Z community-groups application. Spotify created global cultural touchpoints like Spotify Wrapped and collaborative playlist-sharing features transforming individual listening into collective cultural experiences.

Anchoring consumer journeys within applications using logins, persistent accounts, AI features, and gamification mechanics secures first-party data while protecting margins. Duolingo gamifies language learning with streaks, points, levels, and leaderboards driving daily engagement and habit formation. FanDuel invested in its app ecosystem with all betting flows, promotions, and AI-driven recommendations running in-app with required logins.

The research warns that AI infrastructure costs drive platform consolidation, reducing advertiser negotiating power. The trend mirrors search engine consolidation during the previous decade where capital requirements and network effects created winner-take-most dynamics. Twenty-eight marketing executives predict agentic AI will replace static automation during 2026.

Digital advertising revenue concentration among the top 10 technology companies now reaches 80.8 percent, with companies ranked 11 through 25 holding 11.0 percent, according to IAB Tech Lab research. This concentration squeezes independent publishers while AI companies valued at billions profit from using publisher content without compensation.

The measurement framework attempts to isolate causal impact rather than crediting conversions that would have occurred without advertising exposure. However, AI shopping agents fundamentally change purchase paths, making traditional attribution obsolete before new measurement models emerge, the research warns.

Multiple platforms announced AI agent capabilities throughout 2025. LiveRamp introduced agentic orchestration capabilities on October 1, enabling autonomous AI agents to access identity resolution, segmentation, and measurement tools. Adobe launched its Experience Platform Agent Orchestrator on September 10 for managing agents across Adobe and third-party ecosystems.

The research methodology combined qualitative expert interviews with quantitative performance data to construct the Consumer AI Disruption Index. BCG and Moloco conducted the study between June and September 2025, surveying VP-level and C-suite marketing leaders from North America, Europe, Asia-Pacific, Latin America, and Middle East markets.

Performance data included anonymized vertical benchmarks from Moloco advertisers covering metrics for retention, user value, and acquisition cost from both organic and paid traffic sources. The research team supplemented this with data from Sensor Tower and Semrush analyzing web and app traffic patterns across the 17 studied verticals.

"As consumers move from the world of search to the world of answers, we're seeing a behavioral shift that risks disrupting digital brands across a broad range of industries," said D'Arcy. "The companies that will thrive in this new age of AI will focus on longer-term customer relationships, owned digital surfaces like apps, and strategies that strengthen brand and loyalty."

The research identifies agentic commerce as a fundamental force reshaping consumer behavior patterns. Forty-five percent of consumers feel comfortable letting AI make purchases on their behalf, according to the BCG and Moloco survey. This behavioral shift represents what the report characterizes as the emergence of AI agents acting autonomously within user-defined parameters.

McKinsey research cited in industry coverage projects that agentic commerce could orchestrate between $900 billion and $1 trillion in revenue in the United States B2C retail market alone by 2030, with global projections reaching $3 trillion to $5 trillion. The transformation extends beyond simple automation to fundamentally alter how consumers discover products, evaluate options, and execute transactions.

Payment infrastructure providers have mobilized to support autonomous shopping systems. Visa positioned itself at the forefront of agentic commerce infrastructure, developing payment protocols that allow AI agents to make purchases on behalf of consumers while maintaining security standards. Mastercard introduced Agent Pay infrastructure on January 11, citing PYMNTS Intelligence data showing 39 percent of United States consumers have used generative AI for online shopping.

Adobe Analytics documented traffic to United States retail websites from generative AI sources jumping 1,200 percent during the first quarter of 2025, providing empirical evidence of behavioral transformation already underway. Google launched the Universal Commerce Protocol on January 11 with major retailers including Shopify, Etsy, Wayfair, Target, and Walmart, establishing open-source technical standards for AI agents to execute purchases across different retail platforms without requiring custom integrations.

The protocol developments arrived alongside concrete implementations. Microsoft launched Copilot Checkout on January 8, enabling shoppers to complete purchases entirely within the Copilot interface without redirecting to merchant websites. According to Microsoft's internal data, journeys including Copilot led to 53 percent more purchases within 30 minutes of interaction compared to journeys without the AI assistant.

Amazon deployed comprehensive AI shopping features on November 18, 2025, reporting 250 million users for its Rufus conversational shopping assistant. Products available through Buy for Me, Amazon's agentic AI experience that purchases items from brand websites not available in Amazon's store, increased from 65,000 at launch to over half a million presently.

The commercial viability of autonomous shopping remains contested despite platform investments. Independent analyst Andrew Lipsman published detailed analysis on October 6, 2025, questioning agentic commerce adoption despite OpenAI's instant checkout features. The analysis examined eight structural challenges including retailer incentives against AI intermediation, high e-commerce return rates, and consumer preferences for evaluating options before purchasing.

Lipsman's probability analysis assigned estimates to each necessary condition for successful agentic commerce transactions: shoppers must know how to prompt AI agents (50 percent probability), trust agents with financial information (50 percent probability), authorize autonomous transactions (50 percent probability), and accept products selected without direct inspection (25 percent probability). The cumulative probability calculation suggests substantial mathematical challenges facing widespread agentic commerce adoption.

Research published on November 25, 2025, showed 85 percent of United Kingdom consumers planning AI-assisted holiday shopping would trust autonomous agents to place orders and execute payments. However, privacy, fraud, and accuracy concerns remain significant barriers, with 49 percent worried about data handling, 46 percent about fraud, and 41 percent fearing AI might select the wrong item.

Platform strategies toward agentic commerce reveal fundamental business model conflicts. Amazon explicitly blocks competing AI agents from accessing its marketplace, implementing technical restrictions against OpenAI, Anthropic, Meta, and other platforms. The divergent strategies reflect incompatible business models, with Amazon protecting $56 billion in annual advertising revenue by preventing third-party agents from helping consumers discover products outside Amazon's controlled channels.

The Consumer AI Disruption Index reveals that verticals face dramatically different risk profiles requiring customized strategic responses. News publishers confront existential threats as AI agents can easily replicate aggregation and summarization workflows. Pure-play news and review platforms face especially high vulnerability, with AI platforms compressing discovery processes that historically drove traffic to publisher websites.

Travel experiences high disruption risk for pure aggregator and agentic models handling itinerary planning and price comparisons. A Visa executive example cited in the report illustrated family vacation planning with four children—previously a four-hour comparison shopping project across hotels, airlines, locations, weather, and activities—now compressed to 30 minutes through prompt-based recommendations. The discovery funnel's first 80 percent collapses rapidly as AI handles research traditionally requiring manual effort.

Retail and e-commerce face what the report characterizes as agentic commerce models that exist within large language models, enabling comparison which disrupts generic marketplaces. However, retailers with loyalty ecosystems, first-party data, and fulfillment capabilities maintain defensive positions. The research notes that retailers have accelerated retail media infrastructure development, with over 90 percent of advertisers now partnering with retailers to access first-party data.

Auto marketplaces face pure lead-generation and review marketplace disruption as AI large language model agents directly connect buyers and sellers. The vertical demonstrates weak performance across all three customer relationship metrics, with just 58 percent unpaid traffic, 50 percent Day 30 to Day 7 retention, and 25 percent app engagement, leaving little defensive positioning against AI-driven disintermediation.

Education platforms confront AI large language models already showing traction in knowledge delivery, making pure-play content hubs vulnerable. However, platforms offering certifications maintain defensibility. Coursera added AI-powered features to safeguard assessments against integrity threats through plagiarism detection, proctoring, and interactive question-and-answer capabilities to verify learner authenticity and ensure credential credibility.

Productivity software faces nuanced positioning. Niche productivity applications including calendar and notes face disruption risk as workflows prove easy for large language models to integrate. In contrast, entrenched platforms like Microsoft Word, Excel, and Google Sheets occupy stronger positions through network effects and switching costs. The report notes these platforms can shape industry standards by leveraging scale and trust to define how AI integrates into productivity workflows.

Financial services, fintech, and media streaming demonstrate the lowest disruption risk, with inherent trust and regulatory moats providing durable barriers to AI substitution. Social platforms achieve the highest customer relationship strength scores at 9.6 out of 10, driven by 77 percent unpaid traffic, 86 percent Day 30 to Day 7 retention ratios, and 99 percent app engagement. These verticals can focus on using AI to drive efficiency and hyper-personalized engagement rather than defensive positioning.

Dating platforms face moderate disruption with weak brand ties despite strong app engagement at 65 percent. The challenge involves converting transactional relationships into durable loyalty. Bumble expanded "Bumble For Friends" through acquiring Geneva, a Generation Z community-groups application, embedding the platform within friendship and social graphs to increase switching costs.

Casino and sports betting verticals demonstrate heavy reliance on paid acquisition, rendering them highly exposed as AI reshapes discovery channels. The vertical scored 7.1 on customer relationship strength but faces discovery disruption as reduced brand visibility across search, programmatic, and affiliate channels threatens growth models. FanDuel invested in its app ecosystem with all betting flows, promotions, and AI-driven recommendations running in-app with required logins to anchor behavior within controlled environments.

The Consumer AI Disruption Index warns that AI shopping agents fundamentally change purchase paths, making traditional attribution obsolete before new measurement models emerge. Traditional attribution frameworks assume human decision-making processes that no longer apply when AI intermediaries make purchasing decisions.

Consumer adoption of AI shopping agents creates new attribution challenges as autonomous systems research products, compare prices, and execute purchases on behalf of humans. Marketing professionals face pressure to shift from journey mapping to real-time decisioning frameworks, the research suggests.

The advertising industry confronts what industry analysis characterizes as a measurement crisis where AI attribution does not solve underlying challenges. The measurement framework attempts to isolate causal impact rather than crediting conversions that would have occurred without advertising exposure. However, when AI systems mediate discovery and purchase decisions, determining which touchpoints influenced outcomes becomes exponentially more complex.

Platform consolidation accelerates due to AI infrastructure costs, reducing advertiser negotiating power. The trend mirrors search engine consolidation during the previous decade where capital requirements and network effects created winner-take-most dynamics. Energy demands where typical AI data centers consume power equivalent to 100,000 households create insurmountable barriers for independent publishers competing with Big Tech AI infrastructure.

The research arrives as digital advertising revenue concentration among the top 10 technology companies reaches 80.8 percent, with companies ranked 11 through 25 holding 11.0 percent. This concentration squeezes independent publishers while AI companies valued at billions profit from using publisher content without compensation, according to IAB Tech Lab research documented throughout 2025.

Marketing professionals should monitor consumer trust in AI-generated content and AI-targeted advertising within specific categories, the report recommends. Consumer perception varies substantially across product categories and demographic segments, requiring category-specific measurement rather than industry-wide assumptions.

The BCG and Moloco survey findings reveal that 77 percent of marketing leaders prioritize first-party data capture, 72 percent emphasize AI-driven ad formats, and 67 percent focus on building in-house AI capabilities. These investment patterns demonstrate broad recognition of AI's transformative impact while revealing significant gaps in strategic execution.

Only 52 percent identified rebalancing brand versus performance mix as a priority response to AI-driven discovery changes. This relatively low prioritization may prove problematic as industry analysts predict that direct response advertising will fade while brand advertising gains importance as marketers attempt to influence consumers before they instruct their agents what to purchase.

Travel, education, and retail verticals lead in first-party data capture prioritization at 86 percent, 87 percent, and 86 percent respectively. Traditional finance and productivity sectors emphasize AI-driven advertising formats at 85 percent and 82 percent. The vertical-specific prioritization patterns generally align with the Consumer AI Disruption Index risk assessments, suggesting marketing leaders accurately perceive their exposure levels.

Nineteen percent of surveyed marketing leaders prioritize in-app marketing as a response to AI-driven changes in discovery, with dating platforms showing highest adoption at 65 percent. The relatively low overall prioritization of in-app marketing represents a potential strategic gap, as the research demonstrates that closed-loop ecosystems including in-app environments become critical to sustained visibility as traditional open-web channels decline.

The survey reveals that 13 percent to 20 percent of marketing leaders across verticals prioritize managing Reddit and user-generated content presence, recognizing that AI platforms increasingly cite community conversations when generating recommendations. The RealReal invested in Answer Engine Optimization tools tracking which queries surface their brand versus competitors while engaging in user-generated community conversations that are often cited by large language models.

Twenty-eight marketing executives predict agentic AI will replace static automation during 2026, according to industry analysis. Chris Marriott states that "journeys will be a thing of the past for leading brands. Agents will personalize journeys at customer level, determining timing, channel, and offer in real-time." This projection suggests the velocity of transformation may exceed current strategic planning horizons for many organizations.

The report emphasizes that brands must adopt Answer Engine Optimization through on-site optimization, off-site strategies, and ecosystem integrations to ensure visibility in AI-generated responses. This represents a fundamental shift from traditional search engine optimization focused on ranking in lists of links to optimization focused on being cited as the authoritative source within AI-generated answers.

On-site optimization involves updating websites with question-and-answer-style content that can be easily indexed to improve visibility in large language model queries. Credit Karma updated its website structure, expanding FAQ sections, improving schema markup, and reducing JavaScript barriers so core content remains fully crawlable. These technical improvements increase the odds of being cited as the expert for financial questions within AI-generated responses.

Off-site optimization strategies include cultivating user-generated content, editorial mentions, and affiliate content relationships that reinforce brand authority across third-party environments. The RealReal engages in user-generated community conversations on platforms like Reddit which are often cited by large language models. These strategies represent key off-site optimization levers for improving brand visibility in AI-mediated discovery.

Ecosystem integrations require building trust and avoiding suppression for inaccuracies through live pricing feeds, instant-checkout readiness, and API-level connectivity that strengthen reliability and usability of brand data within AI systems. Skyscanner invested in stricter inventory syncing to meet requirements for AI overviews, ensuring citation in large language models and AI overviews by demonstrating data accuracy.

Several technology providers emerged throughout 2025 offering Answer Engine Optimization tools. Microsoft published comprehensive guidance in January 2026 revealing when products disappear from AI recommendations, emphasizing operational e-commerce infrastructure requirements for AI agent visibility. The guide establishes that retailers must maintain accurate inventory data, competitive pricing, and seamless checkout experiences to remain visible in AI-mediated shopping.

The shift toward Answer Engine Optimization represents what industry analysis characterizes as a transformation from optimizing for lists of links to optimizing for citations within synthesized answers. Traditional search engine optimization metrics including rankings and click-through rates become less relevant as consumers increasingly receive answers without clicking through to publisher websites.

The Consumer AI Disruption Index provides detailed recommendations for brands to counter service disruption through strategic decisions about AI integration. The report identifies three distinct approaches: embedding large language model functionality into owned channels, strategically interacting with large language models by opening or closing platforms, or directly integrating into AI assistants through application programming interfaces.

Notion launched features allowing users to create custom agents completing tasks, searching across connected tools, and acting autonomously to increase stickiness and monetization as AI embeds in everyday workflows. Flo built "Ask Flo," an in-app AI assistant for women's health trained on Flo's proprietary medical dataset and reviewed by doctors. Ask Flo can generate clinically reliable answers that are more trustworthy than generic large language model results, demonstrating differentiation through proprietary data and human expertise.

Platform positioning decisions reveal fundamental strategic trade-offs between prioritizing discovery and prioritizing customer ownership. Amazon closed its listings from large language model crawlers, limiting discovery to category-level searches while protecting data ownership and advertising revenues. This approach risks declining visibility as consumer journeys shift toward large language models but maintains control over first-party data and monetization.

Etsy chose the opposite approach, integrating with ChatGPT to allow direct access to product listings including add-to-cart options without leaving the large language model interface. This move expands visibility for Etsy sellers and captures incremental AI-driven reach beyond traditional search. The trade-off involves relinquishing control over first-touch discovery and pricing transparency, heightening commoditization risk.

Canva embedded design tools directly into ChatGPT via the GPT App SDK, keeping Canva central to design creation as large language models generate visual content. This prevents AI platforms from bypassing Canva's ecosystem. Shopify integrated products and checkout services into ChatGPT for seamless in-chat purchases, ensuring Shopify merchants remain part of the transaction layer as shopping shifts into large language model platforms.

The choice to directly integrate into AI assistants comes at the cost of first-party data capture and monetization integrity while promoting price-and-feature commoditization. Brands must carefully evaluate whether maintaining visibility in AI-mediated discovery justifies the loss of direct customer relationships and data ownership that integration entails.

The research emphasizes that embedding products in communities and social graphs creates compounding network effects that make switching costly. By investing in communities, social sharing, and partnerships, companies can turn individual adoption into defensibility that protects against AI-driven commoditization.

Bumble expanded beyond dating into friendship formation, creating multiple relationship types within a single platform that increase switching costs. The acquisition of Geneva, a Generation Z community-groups application, strengthened these network effects by embedding Bumble within friendship and social graphs where platform abandonment requires disrupting multiple relationship types simultaneously.

Spotify created global cultural touchpoints like Spotify Wrapped and collaborative playlist-sharing features that transform individual listening into collective cultural experiences. Users share their Wrapped results across social media networks, creating organic marketing while reinforcing loyalty. These social sharing mechanics strengthen brand equity and protect against AI disruption by making Spotify participation a cultural phenomenon rather than purely functional music consumption.

Duolingo gamifies language learning with streaks, points, levels, and leaderboards that drive daily engagement and habit formation. The gamification mechanics create psychological switching costs beyond functional utility, making platform abandonment feel like losing accumulated progress and social standing within leaderboards. This approach anchors users through multiple reinforcement mechanisms.

L'Oréal expanded dermatologist-led skin assessments and certified in-store diagnostics to complement AI-driven recommendations. The strategy grounds recommendations in human expertise and verified results, reinforcing loyalty and credibility. By distinguishing between AI-provided suggestions and expert-validated advice, L'Oréal creates defensibility through proprietary professional relationships that AI cannot easily replicate.

FanDuel invested in its app ecosystem with all betting flows, promotions, and AI-driven recommendations running in-app with required logins for every interaction. This strategy anchors behavior within FanDuel's environment, minimizes leakage to search or affiliates, and builds a rich data moat which strengthens retention. Keeping the entire journey within owned properties provides maximum control over customer experience and data capture.

Who: Boston Consulting Group and Moloco conducted the research, surveying 238 senior marketing leaders (VP/C-level) across 17 consumer-facing verticals from five global regions. Co-authors include Giorgo Paizanis (BCG Partner), Ernesto Pagano (BCG Managing Director and Senior Partner), Rob Derow (BCG Managing Director and Partner), Janet Balis (BCG Managing Director and Partner), Siddharth Modi (BCG Project Leader), Paul D'Arcy (Moloco Chief Marketing Officer), and Kim Gardner (Moloco Director of Thought Leadership and Content).

What: The Consumer AI Disruption Index assesses 17 consumer verticals along two dimensions: AI-driven disruption (discovery and service) and customer relationship strength (acquisition, loyalty, engagement). The study combines survey data with performance metrics from 3,200+ apps representing 200+ billion downloads. Research reveals 67% of marketing leaders expect high AI-driven disruption to consumer journeys, with news, travel, auto marketplaces, and retail facing highest risk while fintech, financial services, media streaming, and social platforms demonstrate lowest vulnerability.

When: Released January 21, 2026. Research conducted between June and September 2025.

Where: Global study covering five regions (North America, Europe, Asia-Pacific, Latin America, Middle East) examining 17 verticals: travel, education, productivity, retail/e-commerce, health and fitness, fintech, media/streaming, financial services, dating, social, on-demand services, gaming, casino and sports betting, auto OEMs, auto marketplaces, news, and generative AI platforms.

Why: Traditional marketing channels face fundamental disruption as AI platforms compress consumer discovery and comparison processes. Paid and organic search click-through rates declined 50-70% when AI snippets appeared in results. Traditional search traffic to publishers fell from 51% to 27% between 2023-2025 while AI-mediated discovery grows. Forty-five percent of consumers now feel comfortable letting AI make purchases on their behalf, signaling emergence of agentic commerce. Marketers need frameworks to assess vulnerability and build defensibility across discovery, service, and customer relationships as AI reshapes the entire consumer journey from inspiration to loyalty.