Global ad spending hits $1.14 trillion as commerce overtakes TV

WPP Media projects 8.8% growth in 2025 advertising revenue, reaching $1.14 trillion globally, with commerce surpassing TV for first time at $178.2B.

WPP Media projects 8.8% growth in 2025 advertising revenue, reaching $1.14 trillion globally, with commerce surpassing TV for first time at $178.2B.

Global advertising revenue will reach $1.14 trillion in 2025, marking 8.8% growth year-over-year, according to WPP Media's This Year Next Year Global End-of-Year forecast released on December 10, 2025. The projection represents an upward revision from mid-year estimates, driven by more favorable trade tariff outcomes than initially anticipated and continued investment in artificial intelligence infrastructure across the advertising ecosystem.

This momentum extends into 2026, with forecasted growth of 7.1%, both figures excluding U.S. political advertising expenditure. Over a five-year period, the global advertising market is expected to achieve a compound annual growth rate of 6.3%, according to the research conducted by WPP Media's Global Business Intelligence division led by President Kate Scott-Dawkins.

Subscribe PPC Land newsletter ✉️ for similar stories like this one

The forecast arrives during what WPP Media characterizes as "creative destruction," referencing economist Joseph Schumpeter's framework for technological disruption. Streaming video continues displacing linear television viewership, retail media captures budget from traditional digital channels, and AI-powered answer engines begin reshaping search behavior patterns. Concurrently, creator-driven content displaces professionally produced media, forcing industry adaptation to established distribution models.

Commerce advertising represents the most significant structural shift documented in the forecast. Revenue from commerce channels will reach $178.2 billion in 2025, surpassing total television advertising revenue for the first time in the industry's history. This milestone reflects retail media's rapid expansion, with projections indicating the sector will capture approximately 20% of total global advertising revenue by 2030, representing more than $300 billion in spending.

Within the commerce category, pressure to consolidate and demonstrate measurable value has intensified as AI-powered interfaces threaten to cannibalize retail media revenue streams. Major platforms including Amazon, which reported $15.7 billion in advertising revenue during Q2 2025, compete for advertiser budgets while retail media networks expand beyond traditional e-commerce environments into travel, financial services, and other verticals.

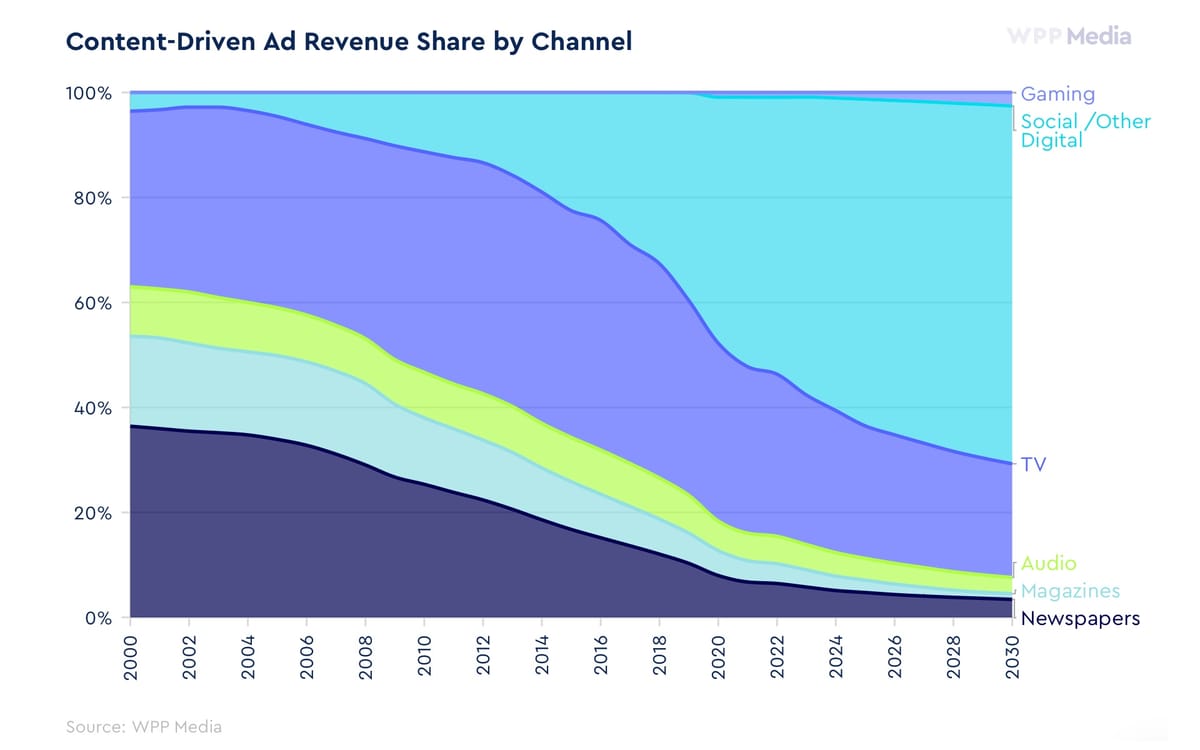

Content-driven advertising remains the largest category at $663.5 billion, representing 58.0% of global revenue. However, distribution within this category reflects fundamental shifts in consumer behavior and advertiser allocation. Streaming television advertising demonstrates particularly strong momentum, with Connected TV budget share doubling from 14% in 2023 to 28% in 2025 according to multiple industry analyses tracking the migration of television viewership to internet-connected platforms.

Gaming emerged as the fastest-growing content advertising channel, expanding 29.5% to reach $8.5 billion in 2025, though absolute revenue represents just 0.7% of total advertising expenditure. The growth rate significantly outpaces other categories despite relatively small market size, indicating advertiser recognition of gaming environments as viable advertising inventory sources.

Traditional media formats face divergent trajectories. Newspaper advertising shows near-term stabilization at $31.4 billion in 2025 before projected declines resume in subsequent years. Digital out-of-home advertising demonstrates more favorable outlook, with forecasts indicating DOOH will represent 43.9% of total OOH revenue by 2030, reaching $31.4 billion and effectively achieving parity with traditional outdoor formats.

The forecast introduces several methodological updates that reflect the industry's structural transformation. WPP Media has reclassified "search" as "Intelligence," acknowledging how AI-powered answer engines and search features have fundamentally altered the discovery and information retrieval process. Additional forecast categories include gaming, financial services media networks, and travel media networks, recognizing the broadening landscape of advertising sellers and platforms beyond traditional publishers.

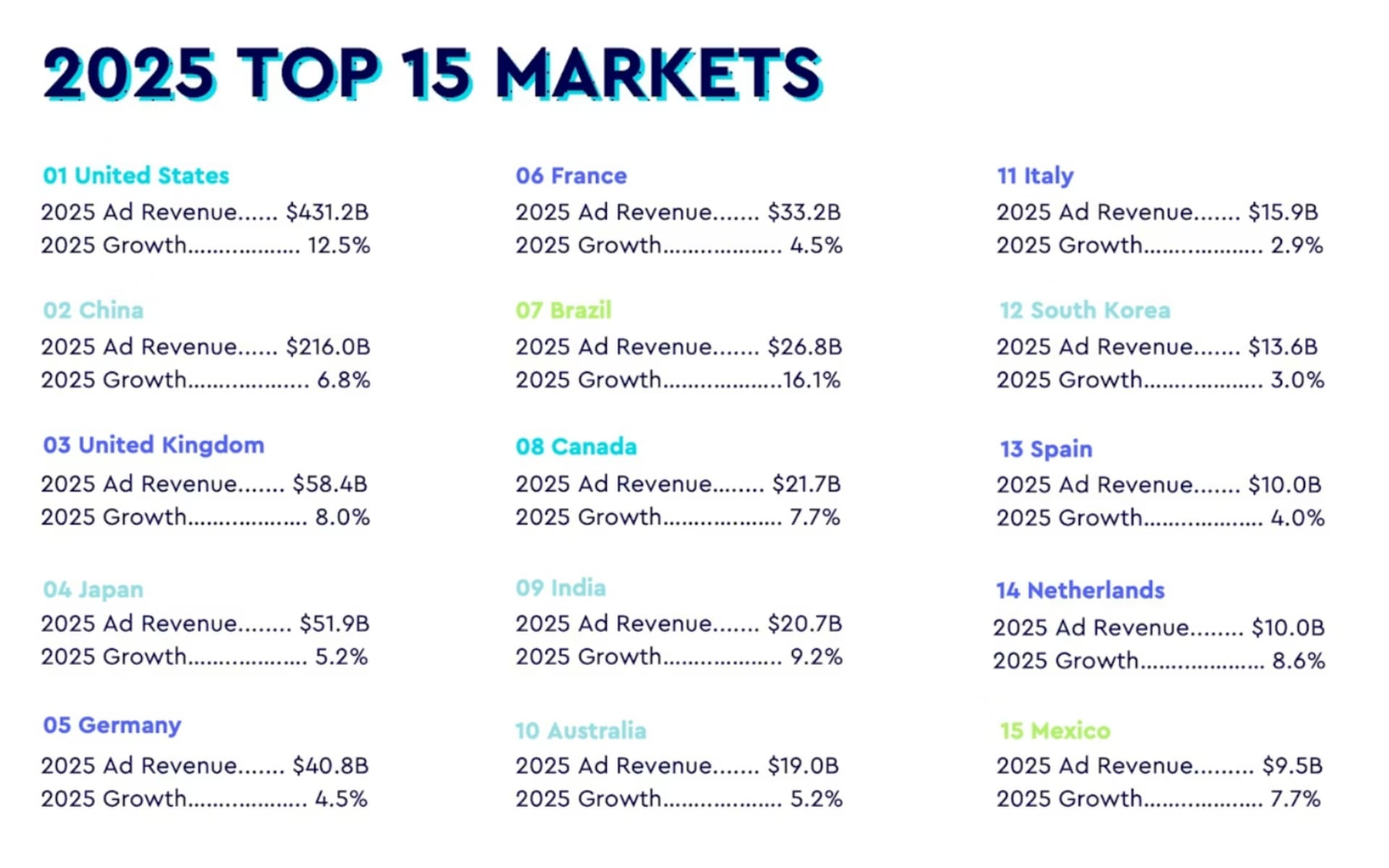

Geographic distribution of advertising expenditure reveals concentrated growth across 15 major markets. The United States leads with $431.2 billion in advertising revenue and 12.5% growth in 2025. China follows at $216.0 billion with 6.8% growth, while the United Kingdom projects $58.4 billion in revenue with 8.0% expansion. Japan ($51.9 billion, 5.2% growth) and Germany ($40.8 billion, 4.5% growth) complete the top five markets by absolute spending.

Emerging markets demonstrate stronger growth rates despite smaller absolute revenue figures. Brazil projects 16.1% growth to reach $26.8 billion, while India shows 9.2% expansion to $20.7 billion. These growth differentials reflect varying stages of digital transformation and advertising market maturity across geographic regions.

Market-specific commerce advertising data reveals concentration in the United States and China, which collectively dominate global commerce media spending. U.S. commerce advertising revenue significantly exceeds other individual markets, while Chinese commerce advertising follows distinct growth trajectories influenced by domestic platform ecosystems including Alibaba, JD.com, and emerging retail media networks.

Buy ads on PPC Land. PPC Land has standard and native ad formats via major DSPs and ad platforms like Google Ads. Via an auction CPM, you can reach industry professionals.

Artificial intelligence functions as the primary catalyst for industry disruption documented throughout the forecast. The technology influences content creation, media planning, measurement methodologies, and consumer interaction patterns. AI adoption in advertising creative production has accelerated dramatically, with platforms including Google, Meta, and Amazon deploying generative AI capabilities across their advertising interfaces.

The advertising industry's prior integration of machine learning positions it favorably for adapting to generative AI capabilities, according to WPP Media's analysis. However, challenges around brand safety, measurement standardization, and creative quality have emerged as significant concerns for advertisers navigating AI-powered campaign automation. Industry research indicates 61% of media professionals express excitement about AI-generated content opportunities, while 53% simultaneously cite unsuitable adjacencies as a top challenge for 2026.

Platform consolidation continues reshaping competitive dynamics within the advertising ecosystem. Google reported 10% growth in search advertising during Q2 2025, while Meta achieved 22% advertising revenue growth during the same period. These divergent growth rates reflect varying success in adapting to AI integration and maintaining advertiser demand amid regulatory scrutiny and market saturation concerns.

The forecast's upward revision from mid-year projections reflects improved macroeconomic conditions compared to earlier 2025 expectations. Trade tariff negotiations produced more favorable outcomes than anticipated during the first half of 2025, reducing uncertainty that had previously constrained advertiser spending commitments. Additionally, sustained investment in AI infrastructure across technology companies created incremental advertising demand as platforms marketed new capabilities to business customers.

WPP Media introduces the Future of Advertising Intelligence Framework alongside the forecast, assessing companies on data assets, AI and technology capabilities, distribution infrastructure, commerce integration, and content and media assets. The framework posits that future advertising will be "Personalized, Pervasive, and Proactive," requiring companies to develop comprehensive capabilities across multiple domains. Full framework definitions and scoring rubric will be released in January 2026 at CES, according to the announcement.

The framework reflects industry recognition that advertising success increasingly depends on integrated capabilities rather than excellence in isolated functions. Companies that combine first-party data infrastructure with AI-powered optimization, cross-channel distribution, and commerce integration position themselves more favorably than organizations excelling in single domains. This holistic approach addresses fragmentation challenges that have limited programmatic adoption across commerce media and other emerging formats.

Measurement and attribution remain persistent challenges as advertising diversifies across channels and formats. Connected television measurement capabilities have advanced substantially, with deterministic tracking solutions enabling advertisers to connect streaming exposure to qualified visits and conversions. However, standardization across retail media networks has lagged, with 42% of commerce media programs describing themselves as operationalized or advanced despite significant capability gaps according to research examining network maturity.

Privacy regulation continues influencing advertising technology architecture and revenue distribution across markets. The phase-out of third-party cookies has accelerated advertiser reliance on first-party data and contextual targeting methodologies. Retail media networks benefit from these shifts, as their direct consumer relationships provide targeting capabilities unavailable through traditional digital advertising channels facing data restrictions.

The forecast period coincides with significant regulatory developments affecting major advertising platforms. Antitrust enforcement actions in the United States and European Union target platform market dominance and data collection practices, potentially influencing competitive dynamics and revenue distribution across the ecosystem. These regulatory pressures create uncertainty for long-term planning while simultaneously creating opportunities for alternative platforms to capture market share.

Global economic conditions present mixed signals for advertising growth sustainability. Inflation rates have moderated from 2022-2023 peaks in major markets, while interest rates remain elevated compared to historical averages. Consumer spending patterns reflect divergent trajectories across income segments and geographic regions, with luxury categories demonstrating resilience while mass-market segments face affordability pressures affecting retail advertising demand.

The $1.14 trillion projected for 2025 represents substantial expansion from pre-pandemic advertising levels, though growth rates have normalized from the recovery period following 2020 disruptions. According to broader economic analysis of digital advertising's impact, the sector now represents between 0.6% and 1.1% of U.S. GDP, with big tech companies playing central roles in this expansion.

Programmatic advertising transactions continue expanding across channels and formats, with Connected TV seeing three-fourths of spending transacted programmatically according to platform analyses. This automation enables efficiency gains and targeting precision that manual insertion orders cannot match, though concerns about transparency and control persist among advertisers managing automated campaigns.

Publisher economics face mounting pressure as traffic patterns shift toward platform-controlled environments. Google's network advertising revenues, which support third-party publishers, declined 1% year-over-year during Q2 2025 while the company's owned properties grew substantially. This dynamic reflects broader trends where social media and search engines retain users within their own ecosystems rather than sending referral traffic to external publishers.

The forecast's introduction of gaming, financial services media networks, and travel media networks as distinct categories acknowledges how advertising sellers have diversified beyond traditional publishers. Financial institutions including PayPal and banks have established advertising businesses monetizing their customer data and digital properties. Travel companies including airlines and hotel chains have similarly launched media networks, capturing advertising budgets previously allocated to online travel agencies and search platforms.

Market analysts note that advertising industry transformation toward 2030 will be shaped by AI creative dominance, biometric standardization, sustainability priority shifts, virtual reality adoption timelines, and privacy fragmentation across regulatory jurisdictions. These interconnected trends create complex planning requirements for marketers developing multi-year strategies across evolving platform capabilities and consumer expectations.

The December 10 release timing positions WPP Media's forecast as the definitive year-end assessment for advertising professionals planning 2026 budgets and strategies. The upward revisions compared to mid-year projections provide confidence for increased investment commitments, while the detailed channel and geographic breakdowns enable granular allocation decisions across markets and formats.

Industry observers emphasize that the $1.14 trillion figure excludes U.S. political advertising, which represents significant incremental spending during election years but creates volatility that complicates year-over-year comparisons. The 2024 U.S. elections generated substantial advertising revenue for platforms and broadcasters, creating difficult comparison periods for 2025 non-election year performance.

Looking beyond 2026, the five-year CAGR projection of 6.3% suggests sustained expansion despite near-term economic uncertainties and platform disruption. This growth trajectory depends on continued digital transformation across industries, sustained consumer engagement with digital media, and advertiser confidence in measurement and attribution capabilities that justify increased spending commitments.

Subscribe PPC Land newsletter ✉️ for similar stories like this one

Subscribe PPC Land newsletter ✉️ for similar stories like this one

Who: WPP Media's Global Business Intelligence division led by President Kate Scott-Dawkins conducted the forecast research, analyzing advertising spending patterns across 15 major global markets and multiple advertising channels affecting marketers, platforms, publishers, and agencies worldwide.

What: Global advertising revenue will reach $1.14 trillion in 2025, growing 8.8% year-over-year excluding U.S. political spending, with commerce advertising ($178.2 billion) surpassing total TV revenue for the first time, content-driven advertising maintaining largest share at $663.5 billion (58.0%), gaming recording fastest growth at 29.5% expansion to $8.5 billion, and DOOH projected to achieve parity with traditional outdoor formats by 2030 at $31.4 billion.

When: The This Year Next Year Global End-of-Year forecast was released on December 10, 2025, analyzing projected 2025 performance and 2026 growth of 7.1%, with the full Future of Advertising Intelligence Framework scheduled for release in January 2026 at CES.

Where: The forecast covers the top 15 global advertising markets including United States ($431.2 billion, 12.5% growth), China ($216.0 billion, 6.8% growth), United Kingdom ($58.4 billion, 8.0% growth), Japan, Germany, France, Brazil, Canada, India, Australia, Italy, South Korea, Spain, Netherlands, and Mexico, representing comprehensive coverage across North America, APAC, Europe, Latin America, and Middle East & Africa regions.

Why: The upward revision from mid-year projections reflects more favorable trade tariff outcomes than initially anticipated and sustained AI investment boom driving technology platform advertising demand, while structural shifts including streaming displacement of linear television, retail media budget capture from traditional digital channels, AI-powered answer engines reshaping search behavior, and creator-driven content displacing professionally produced media force industry adaptation to what WPP Media characterizes as "creative destruction" requiring comprehensive capabilities across data assets, AI technology, distribution, commerce integration, and content assets to succeed in increasingly personalized, pervasive, and proactive advertising environments.