Finland got its first structured overview of the retail media market on February 25, 2026, when IAB Finland's retail media working group released a landscape document mapping the full ecosystem of players operating in the country. The publication arrives as the sector draws increasing interest from Finnish and international advertisers trying to navigate a fragmented field of retailers, marketplaces, technology suppliers, and specialist networks.

The document, produced by IAB Finland's retail media working group, is described by the organisation as "a concrete step toward a more transparent and clearly outlined market." Its stated purpose is to help Finnish and international marketers, media agencies, and brands understand where retail media can be used, which consumer categories can be reached, and through which companies and networks purchasing is possible.

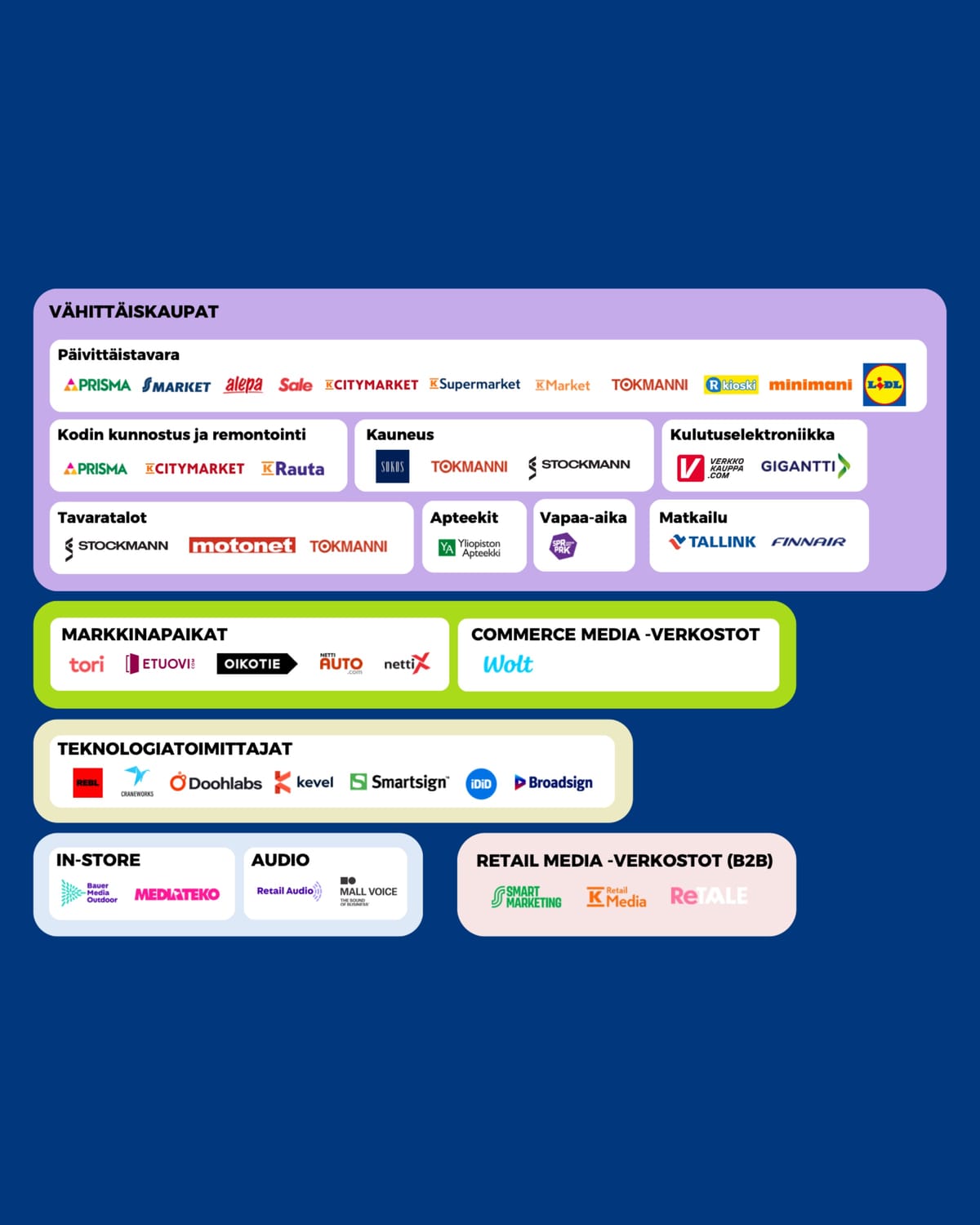

The landscape covers four broad layers. At the base sit the vähittäiskaupat - retailers - divided into six vertical categories: grocery (päivittäistavara), home improvement and renovation (kodin kunnostus ja remontointi), beauty (kauneus), department stores (tavaratalot), pharmacies (apteekit), leisure (vapaa-aika), consumer electronics (kulutuselektroniikka), and travel (matkailu). Above that sits a layer of markkinapaikat - marketplaces - alongside what the document labels commerce media networks. A third layer covers teknologiatoimittajat, or technology vendors. Supplementary categories address in-store advertising, audio formats, and B2B retail media networks.

The breadth of named participants is notable. In grocery alone, the landscape lists Prisma, S-Market, Alepa, Sale, K-Citymarket, K-Supermarket, K-Market, Tokmanni, R-kioski, Minimani, and Lidl. Home improvement features Prisma, K-Citymarket, and K-Rauta. The beauty category includes Sokos, Tokmanni, and Stockmann. Department stores are represented by Stockmann, Motonet, and Tokmanni. In pharmacies, Yliopiston Apteekki appears as the named player. Finnair and Tallink cover the travel vertical, while Verkkokauppa.com and Gigantti appear under consumer electronics. SPR/PRK covers the leisure category.

The marketplace layer lists Tori, Etuovi, Oikotie, Netti Auto, and NettiX. Commerce media is represented by a single entry: Wolt, the Helsinki-founded delivery platform now owned by DoorDash, which has been building retail media capabilities across its international network.

On the technology side, the landscape names REBL, Craneworks, Doohlabs, Kevel, Smartsign, iDiD, and Broadsign. Broadsign is a Canadian out-of-home advertising technology company that has been expanding its programmatic guaranteed capabilities in European markets. Kevel is an ad server infrastructure provider for retail media. The in-store advertising category includes Bauer Media Outdoor and Mediateko. The audio layer lists Retail Audio and Mall Voice. The B2B retail media networks segment includes Smart Marketing, K Retail Media, and ReTale.

The release reflects a gap that has been growing as the Finnish market adds participants faster than it has been able to describe itself. According to IAB Finland, the field "is growing and developing rapidly," with new players, networks, and technology vendors entering continuously - a dynamic the organisation says has increased demand for a shared, market-wide overview.

The timing of this domestic mapping effort sits within a much broader European context. European retail media advertising reached €13.7 billion in 2024, growing 21.1% compared to the prior year, according to IAB Europe data released in October 2025. The channel now accounts for approximately one-fifth of total digital advertising expenditure across European markets. IAB Europe forecasts the figure will more than double by 2028, reaching €28.8 billion. Intermediate projections set milestones at €16.9 billion in 2025, €20.8 billion in 2026, and €24.9 billion in 2027. Historical data shows the acceleration: European retail media stood at €7.4 billion in 2021, climbed to €9.6 billion in 2022, and reached €11.3 billion in 2023 before the 2024 figure.

IAB Europe had already updated its pan-European Retail & Commerce Media Landscape Map in October 2025, documenting the accelerated pace at which new platforms and technology providers continue entering the sector. That continental map organises hundreds of companies across eight distinct categories - Retail & Commerce Media Networks, In-Store RMN/CMN Ad Tech Providers, Demand Side Platforms and Ad Tech Providers, Data Collaboration tools, Verification services, Attribution and Measurement providers, Media Agencies, and Supply Side Platforms. The Finnish landscape takes a similar architectural approach but focuses exclusively on domestic participants and locally relevant verticals.

Measurement remains a persistent challenge across European markets, not just in Finland. IAB Europe research has found that 53% of retail media stakeholders cite lack of standardisation as the key barrier to investment. Against that backdrop, IAB Finland's effort to clarify which companies operate in which part of the value chain carries practical weight: marketers who cannot easily identify available partners struggle to allocate budgets effectively. The Finnish document does not attempt to set measurement standards or definitions - that work has been done at the European level through IAB Europe's updated retail and commerce media definitions published in March 2025 - but it does provide a clearer structural picture of who is available for buying.

The categorisation of players into on-site retailers, marketplaces, commerce media networks, technology vendors, in-store, audio, and B2B networks maps closely to how IAB Europe segments the broader pan-European ecosystem. The Finnish taxonomy recognises that retail media is not a single channel but a set of environments - from sponsored product placements on grocery retailer websites to audio advertising in physical stores to programmatic digital out-of-home screens. Each layer requires different technology infrastructure and different buying processes.

The technology vendor section is particularly relevant for media agencies and advertisers assessing how to activate campaigns programmatically. Broadsign operates digital out-of-home infrastructure across multiple European markets. Kevel provides retail media ad server technology that allows retailers to build monetisation programmes without relying on third-party platforms. Doohlabs specialises in digital out-of-home software. Smartsign and iDiD operate digital signage platforms with relevance to in-store environments. The inclusion of these vendors in a Finnish-specific landscape suggests that in-store and DOOH retail media formats are becoming relevant at the market level, not just theoretically.

The in-store category features Bauer Media Outdoor and Mediateko, two players with physical screen infrastructure. The audio category's inclusion of Retail Audio and Mall Voice reflects growing interest in sound-based advertising within retail environments - a format that remains relatively niche in European retail media but has attracted attention as an extension of in-store media. The B2B retail media networks - Smart Marketing, K Retail Media, and ReTale - offer routes to market that aggregate demand across multiple retail environments, making them relevant for brands seeking broader reach without managing relationships with individual retailers.

The release coincides with a separate IAB Finland announcement, published two days later on February 27, reporting that Finland's digital out-of-home (DOOH) advertising market reached €66.8 million in 2025, up approximately 9.5% from €61 million in 2024. That figure was produced by IAB Finland's digital out-of-home working group. The proximity of the two publications - the retail media landscape on February 25 and the DOOH market estimate on February 27 - reflects an active period for Finnish industry data production.

For international advertisers and agencies that include Finland in European campaign plans, the landscape provides a practical directory of where media can be purchased. The combination of domestic grocery chains, a strong marketplace layer, and technology vendors supporting programmatic buying suggests a market with both scale and complexity. Wolt's presence as the sole named commerce media network reflects the platform's growing relevance as an advertising surface. DoorDash's 2024 acquisition of Wolt brought the Finnish delivery platform into a larger retail media strategy, and Criteo serves as a demand partner for that network, giving brands access to delivery-commerce audiences that overlap with grocery and convenience spending.

The Finnish market's structural characteristics - a concentrated retail sector with dominant players like the S Group (Prisma, S-Market, Alepa, Sale) and the K Group (K-Citymarket, K-Supermarket, K-Market, K-Rauta, K Retail Media) - mean that a relatively small number of retailers command significant reach. Tokmanni appears across three separate verticals - grocery, beauty, and department stores - reflecting its discount generalist positioning. Stockmann appears in both beauty and department stores. Lidl completes the grocery category with its Finnish operations.

IAB Finland's retail media working group states its broader mandate: advancing the development of the Finnish retail media market by producing definitions and guidelines and facilitating industry discussion. The landscape document is described as a step toward greater transparency. It is available for download as a PDF from IAB Finland's website.

Timeline

- 2021: European retail media advertising stands at €7.4 billion across the continent.

- 2022: European retail media reaches €9.6 billion.

- 2023: European retail media grows to €11.3 billion.

- March 26, 2025: IAB Europe publishes updated pan-European definitions for retail and commerce media, establishing consensus terminology for on-site, off-site, and in-store digital retail media across European markets.

- April 17, 2025: IAB Europe releases its Guide to Sponsored Products, documenting 22.1% retail media growth in Europe versus 6.1% for the overall ad market in 2024.

- May 2025: IAB Europe releases the first version of its Pan-European Retail & Commerce Media Landscape Map.

- October 7, 2025: IAB Europe reports European retail media advertising reached €13.7 billion in 2024, a 21.1% increase year-over-year.

- October 14, 2025: IAB Europe releases an updated version of its pan-European landscape map, reflecting continued ecosystem growth and new entrants.

- October 6, 2025: Criteo announces multi-year partnership with DoorDash - which owns Wolt - for retail media advertising across delivery marketplaces.

- November 13, 2025: Broadsign, StackAdapt, and Branded Cities announce collaboration enabling automated in-advance DOOH transactions, extending Broadsign's programmatic guaranteed capabilities now visible in the Finnish landscape.

- February 25, 2026: IAB Finland's retail media working group publishes the first comprehensive retail media landscape for Finland, mapping retailers, marketplaces, technology vendors, in-store formats, audio, and B2B networks.

- February 27, 2026: IAB Finland separately reports that Finland's DOOH advertising market reached €66.8 million in 2025, growing approximately 9.5% from €61 million in 2024.

Summary

Who: IAB Finland's retail media working group, representing the Finnish interactive advertising industry body, produced and published the document. The landscape covers dozens of named companies across Finnish retail, marketplace, technology, and media categories.

What: The first comprehensive retail media landscape map for Finland, categorising domestic participants into retailers (six verticals including grocery, beauty, home improvement, consumer electronics, pharmacies, and travel), marketplaces, commerce media networks, technology vendors, in-store formats, audio advertising, and B2B retail media networks.

When: The landscape was published on February 25, 2026.

Where: The document covers the Finnish market specifically, produced by IAB Finland and available for download from its website. It reflects a domestic ecosystem that sits within the broader European retail media market, which reached €13.7 billion in 2024.

Why: IAB Finland states the field is growing rapidly with continuous new entrants, creating a need for a shared, market-wide overview. The document aims to help Finnish and international marketers, agencies, and brands identify where retail media can be used, which consumer categories can be reached, and through which companies and networks buying is possible - addressing transparency gaps that the organisation describes as a structural challenge for the market.

Share this article

The link has been copied!